- Advanced Materials

- Indium Tin Oxide Market

Indium Tin Oxide Market Size, Share, and Growth Forecast, 2026 - 2033

Indium Tin Oxide Market by Technique (Sputtering, Electron-Beam Evaporation, Others), Form (Coating, Powder, Others), Application, and Regional Analysis for 2026 - 2033

Indium Tin Oxide Market Size and Trends Analysis

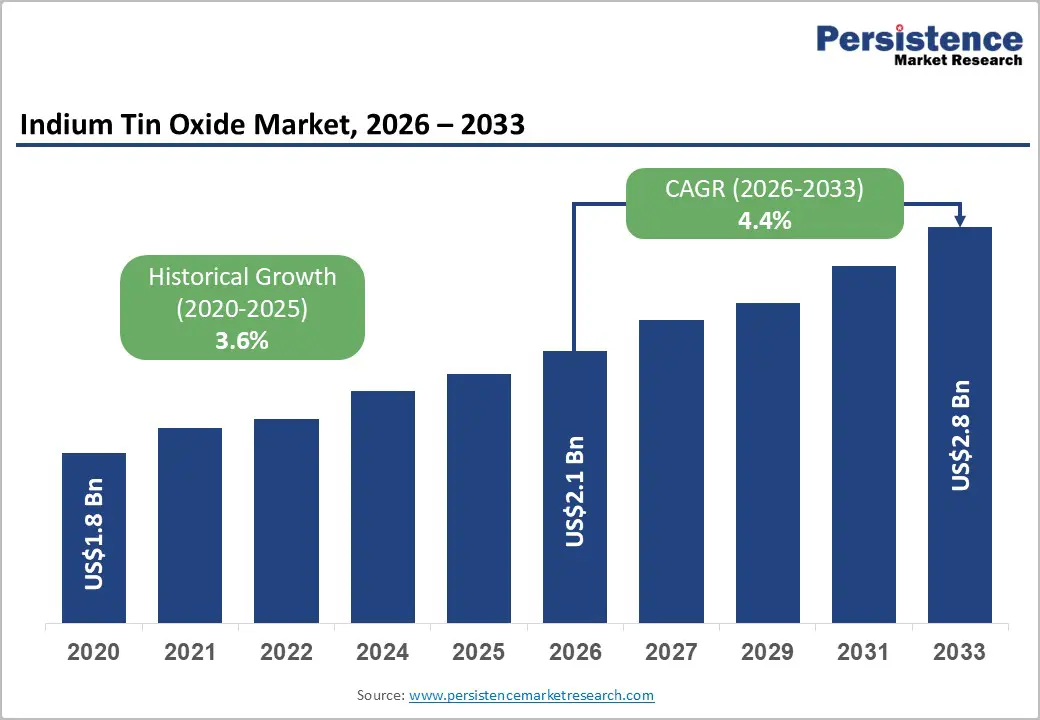

The global indium tin oxide market size is likely to be valued at US$2.1 billion in 2026 and is expected to reach US$2.8 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033, driven by sustained demand from flat-panel displays, touch-enabled devices, and transparent conductive coatings across electronics and renewable energy systems.

Growth is supported by increasing solar photovoltaic deployment and semiconductor manufacturing expansion, while supply concentration of indium and emerging material alternatives remain critical structural considerations influencing long-term market dynamics.

Key Industry Highlights:

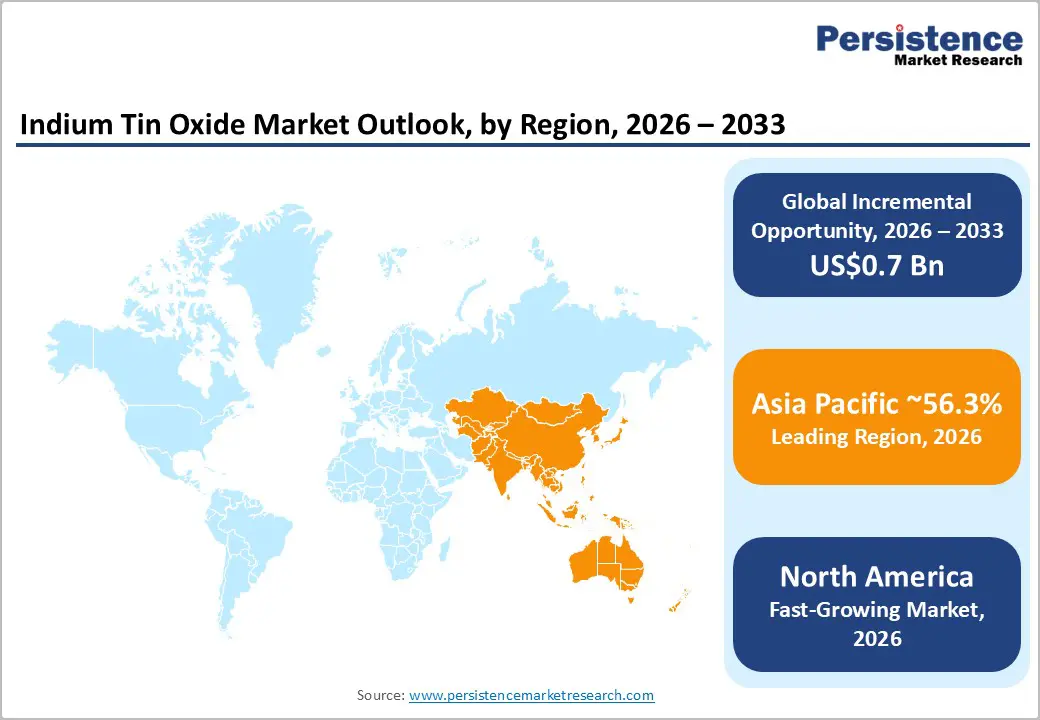

- Leading Region: Asia Pacific is projected to account for approximately 56.3% of the market share, supported by its strong electronics manufacturing base and leadership in display and solar production.

- Fastest-growing Region: North America is the fastest-growing region, driven by increasing investments in semiconductor manufacturing and renewable energy, with strong policy support accelerating regional demand for advanced materials.

- Investment Plans: Significant investments are being made in semiconductor fabs, solar manufacturing, and advanced material facilities, particularly in the U.S. and Asia Pacific, with capacity expansions and localization strategies strengthening supply chain resilience.

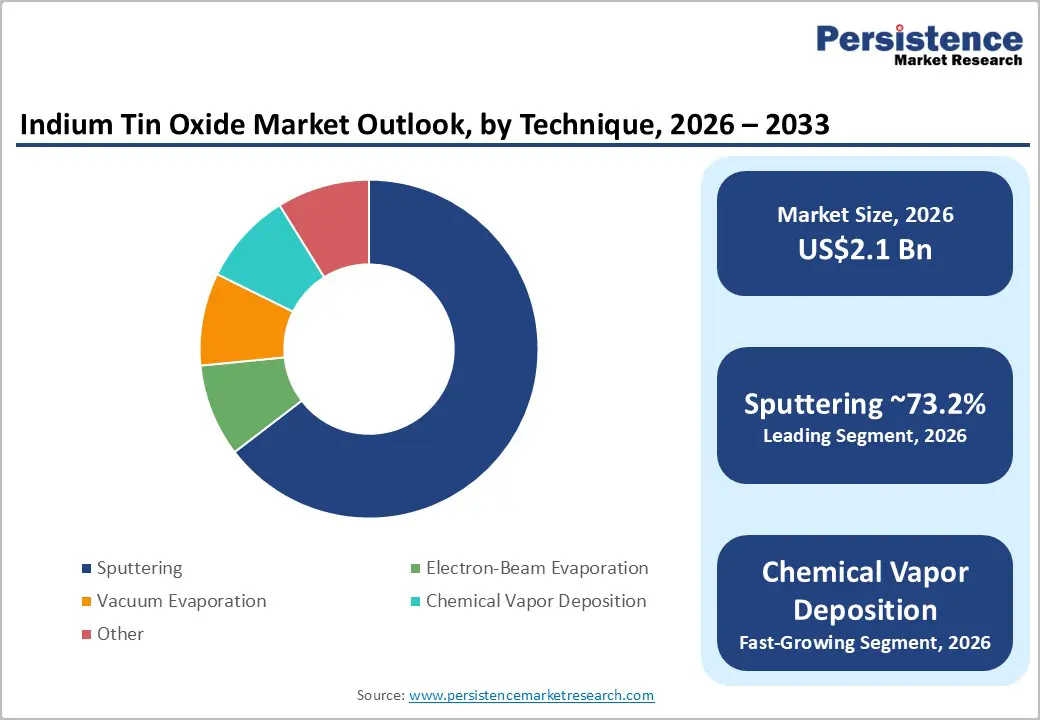

- Dominant Technique: Sputtering is anticipated to hold approximately 73.2% share, due to its superior capability in delivering uniform, high-quality thin films for large-scale display and electronic applications.

- Leading Application: Optoelectronics is estimated to lead with around 48.1% market share, driven by widespread use in flat-panel displays, touchscreens, and consumer electronic devices.

| Key Insights | Details |

|---|---|

| Indium Tin Oxide Market Size (2026E) | US$2.1 Bn |

| Market Value Forecast (2033F) | US$2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

DRO Analysis

Driver Analysis - Strong Demand from Display Technologies and Touch-Enabled Devices

The ITO market continues to be anchored by its essential role in flat-panel displays, particularly LCDs, where it serves as a transparent conductive coating. Its ability to provide high optical transparency and electrical conductivity makes it indispensable for display glass, touchscreens, and interactive devices. As consumer electronics penetration expands across emerging markets and device replacement cycles remain active in developed economies, demand for high-performance display components remains stable. The growth of large-format displays, automotive infotainment systems, and smart consumer interfaces further reinforces the importance of ITO in achieving consistent film uniformity and optical clarity across large substrates.

Expansion of Solar Photovoltaic and Clean Energy Infrastructure

The accelerating global transition toward renewable energy is significantly strengthening demand for transparent conductive materials such as ITO. Solar photovoltaic installations continue to grow due to supportive government policies, tax incentives, and declining system costs. Transparent conductive oxide coatings are critical in thin-film solar cells, where they enable efficient light transmission and electrical conduction. The expansion of building-integrated photovoltaics and energy-efficient glass solutions further broadens application scope. As global investments in solar energy infrastructure increase, ITO demand benefits directly from its integration into conductive coatings used in advanced photovoltaic technologies.

Rising Demand from Semiconductors, 5G, and Advanced Electronics

The rapid expansion of semiconductor manufacturing, driven by artificial intelligence, high-performance computing, and 5G infrastructure, is increasing the demand for high-purity materials such as ITO. Advanced communication technologies require materials that enhance signal transmission efficiency and reduce energy losses. ITO plays a role in optical and electronic components used in data centers, fiber-optic systems, and advanced circuitry. Government-backed semiconductor manufacturing initiatives and localization strategies are further strengthening demand for high-quality sputtering targets and thin-film materials, creating a stable growth base for ITO suppliers.

Restraint Analysis - Supply Concentration and Price Volatility of Indium

Indium, a key component of ITO, is primarily obtained as a by-product of zinc refining, making its supply inherently dependent on zinc production cycles. This creates structural supply constraints and exposes the market to fluctuations in availability and pricing. High import dependency in several regions increases vulnerability to geopolitical tensions and trade disruptions. Price volatility affects procurement strategies and cost structures for manufacturers, particularly in industries requiring consistent material quality and long-term supply agreements. These factors collectively introduce uncertainty in pricing and supply chain stability.

Increasing Regulatory Pressure and Emergence of Alternative Materials

Regulatory frameworks focusing on critical raw materials are intensifying scrutiny on indium sourcing, environmental impact, and recycling requirements. At the same time, ongoing research and development efforts are leading to the emergence of alternative transparent conductive materials that aim to reduce reliance on indium. These alternatives are being designed to improve process efficiency, reduce material waste, and lower production costs. While ITO maintains strong performance advantages, substitution risks are gradually increasing, particularly in applications where cost optimization and sustainability are prioritized.

Opportunity Analysis - Localization of Advanced Materials Manufacturing In North America

The increasing emphasis on domestic manufacturing capabilities in North America presents a significant opportunity for ITO producers. Investments in semiconductor fabrication plants and renewable energy infrastructure are driving demand for locally sourced advanced materials. The establishment of new production facilities for sputtering targets and thin-film materials enhances supply chain resilience and reduces dependency on imports. Companies that align with regional manufacturing initiatives can benefit from improved logistics, government incentives, and closer collaboration with end-use industries.

Advancements in High-Efficiency and Flexible Transparent Conductive Materials

Technological innovation in deposition techniques and material engineering is creating opportunities to improve the performance of ITO-based coatings. New formulations and processing methods aim to reduce defects, enhance conductivity, and improve manufacturing yield. These advancements are particularly relevant in applications such as flexible displays, wearable electronics, and next-generation automotive interfaces. The ability to deliver higher efficiency and lower total production costs strengthens the value proposition of ITO in competitive material environments.

Growth in Recycling and Circular Material Ecosystems

Recycling and recovery of indium from ITO scrap are becoming increasingly important as supply constraints intensify. Circular material systems enable manufacturers to reduce reliance on primary raw material extraction while improving sustainability metrics. The development of efficient recycling technologies and closed-loop supply chains can significantly lower production costs and mitigate supply risks. Companies investing in material recovery and reuse strategies are likely to gain a competitive advantage by enhancing supply security and meeting regulatory requirements.

Category-wise Analysis

Technique Insights

Sputtering is anticipated to dominate the market, accounting for 73.2% share in 2026. This technique is widely used for depositing ITO thin films due to its ability to produce highly uniform coatings across large substrates with precise control over thickness, conductivity, and optical transmittance. Sputtering remains the preferred method in flat-panel display manufacturing, particularly for LCD and OLED panels used in televisions, smartphones, and automotive displays, where consistency and scalability are critical. For example, large display manufacturers rely on magnetron sputtering systems to coat display glass for high-resolution panels and touch-enabled interfaces. Its compatibility with high-volume production lines and stringent quality requirements continues to position sputtering as the industry benchmark for transparent conductive coatings.

Chemical Vapor Deposition (CVD) is anticipated to be the fastest-growing technique among electron-beam evaporation, vacuum evaporation, and CVD. This growth is driven by its ability to deposit high-quality, uniform thin films at relatively lower temperatures, making it highly suitable for next-generation applications such as flexible electronics, wearable devices, and advanced optoelectronic components. CVD enables better control over film composition and thickness, which is critical for achieving consistent electrical conductivity and optical transparency in ITO coatings. The increasing demand for flexible displays, lightweight electronic devices, and emerging applications such as smart windows and transparent conductive layers in advanced photovoltaics is accelerating the adoption of CVD. For example, CVD processes are being explored for coating polymer substrates used in foldable smartphones and flexible OLED displays, where traditional sputtering or evaporation techniques may face limitations.

Application Insights

Optoelectronics is anticipated to lead the market, holding a 48.1% share in 2026. This segment includes flat-panel displays, touchscreens, LEDs, and other electronic devices that rely on transparent conductive materials for functionality. ITO is extensively used in smartphones, tablets, televisions, and in-vehicle infotainment systems, where it enables touch sensitivity and display clarity. For example, capacitive touchscreens in consumer electronics depend on ITO-coated glass to detect user input with high precision. Continuous advancements in display technologies, including higher resolution panels and foldable devices, are further strengthening demand within this segment.

Solar cells and photovoltaic applications are expected to be the fastest-growing segment, with a CAGR of 5%. The global transition toward renewable energy and increasing solar installations are key drivers of growth. ITO is used in conductive coatings for thin-film solar cells, where it facilitates efficient light transmission and electrical conductivity. Applications such as building-integrated photovoltaics (BIPV), solar windows, and energy-efficient façades are expanding the use of ITO beyond traditional solar panels. For instance, transparent conductive coatings are increasingly incorporated into smart glass used in commercial buildings to generate energy while maintaining transparency.

Regional Insights

North America Indium Tin Oxide Market Trends - Semiconductor & Solar Investments Driving High-Purity ITO Demand

North America is expected to be the fastest-growing region, driven by strong investments in semiconductor manufacturing, renewable energy, and advanced materials. The U.S. leads the region, supported by government initiatives aimed at strengthening domestic production capabilities. The expansion of semiconductor fabrication facilities, such as new fabs announced by Intel and TSMC in Arizona, has increased demand for high-purity sputtering targets and thin-film materials, directly benefiting ITO suppliers. The rapid growth of solar installations, supported by federal incentives, is also driving demand for transparent conductive coatings used in photovoltaic modules and energy-efficient glass.

Regulatory frameworks and financial incentives continue to encourage local manufacturing and reduce dependency on imports. The region also benefits from a strong innovation ecosystem, with companies such as Corning Incorporated advancing specialty glass used in displays and smart surfaces. In renewable energy, First Solar has expanded its U.S. manufacturing footprint, increasing demand for conductive coatings in thin-film solar modules. However, higher production costs and competition from established Asian manufacturers remain challenges. As a result, companies are focusing on automation, high-value applications, and localized supply chains to maintain competitiveness.

Europe Indium Tin Oxide Market Trends - Sustainable TCO Glass & Recycling Initiatives Shaping Premium ITO Market

Europe represents a high-value market characterized by strong regulatory oversight and a focus on sustainability. Countries such as Germany, United Kingdom, France, and Spain are key contributors to market growth. The region emphasizes energy efficiency, renewable energy adoption, and advanced manufacturing technologies. European glass and materials companies such as AGC Inc. and NSG Group are actively developing transparent conductive oxide (TCO) glass for architectural and solar applications, including smart windows and building-integrated photovoltaics.

Regulatory initiatives targeting critical raw materials and environmental sustainability are shaping market dynamics. Policies promoting circular economy practices have encouraged companies such as Umicore to expand recycling capabilities for critical metals, including indium recovery. Investments in energy-efficient infrastructure and green buildings are also increasing demand for high-performance coatings. For example, smart glass installations in commercial buildings across Germany and France are driving the adoption of ITO-based coatings. Europe’s focus on premium, sustainable applications positions it as a key market for advanced and environmentally compliant ITO solutions.

Asia Pacific Indium Tin Oxide Market Trends - Electronics Manufacturing Dominance Fueling Large-Scale ITO Consumption

Asia Pacific is the leading region, holding approximately 56.3% market share in 2026. The region’s dominance is driven by its extensive electronics manufacturing base, strong presence in display production, and leadership in solar energy deployment. Countries such as China, Japan, and South Korea play central roles in the regional market. Major display manufacturers such as BOE Technology Group, Samsung Electronics, and LG Display rely heavily on ITO coatings for LCD and OLED panels, reinforcing consistent demand for sputtering targets and thin films.

The region benefits from cost-effective manufacturing, well-established supply chains, and high production capacity. Japan and South Korea are key suppliers of high-purity materials, with companies such as Mitsui Mining & Smelting and JX Advanced Metals leading in sputtering target technologies. Meanwhile, China continues to expand its solar manufacturing capacity, with companies such as LONGi Green Energy driving large-scale photovoltaic deployment. ASEAN countries are also emerging as alternative manufacturing hubs, supporting regional diversification. The integration of upstream raw material processing, target manufacturing, and downstream electronics production provides a strong competitive advantage, reinforcing Asia Pacific’s leadership in the global ITO market.

Competitive Landscape

The global indium tin oxide market exhibits a moderately concentrated structure at the material supply level, with a limited number of specialized manufacturers controlling high-purity production and sputtering target capabilities. At the application level, the market is more fragmented, with numerous players across electronics, solar, and glass industries. Competitive positioning is defined by technological expertise, supply chain integration, and the ability to deliver high-performance materials at scale.

Key players are focusing on technological innovation, regional capacity expansion, and cost optimization. Companies are investing in advanced deposition techniques, improving material efficiency, and strengthening supply chain resilience. Circular economy initiatives and recycling capabilities are emerging as critical differentiators in addressing raw material constraints and sustainability requirements.

Key Industry Developments

- In March 2026, JX Advanced Metals Corporation announced the completion of a mass production line for high-purity CVD and ALD materials at its Ibaraki facility, aimed at supporting next-generation semiconductor applications and strengthening supply for advanced thin-film materials used in electronics.

- In September 2025, JX Advanced Metals Corporation announced a ¥7 billion investment to expand recycled material processing capacity by 50%, targeting increased recovery of critical metals from e-waste to strengthen supply chains for semiconductor and electronic materials.

Companies Covered in Indium Tin Oxide Market

- JX Advanced Metals Corporation

- Mitsui Mining & Smelting Co., Ltd.

- Umicore

- Indium Corporation

- Sumitomo Metal Mining Co., Ltd.

- Nitto Denko Corporation

- AGC Inc.

- NSG Group

- Corning Incorporated

- Materion Corporation

- Vital Materials Co., Ltd.

- ENAM Optoelectronic Material Co., Ltd.

- Advanced Nano Products Co., Ltd.

- Duksan Hi-Metal Co., Ltd.

- China Rare Metal Material Co., Ltd.

- Tosoh Corporation

Frequently Asked Questions

The global indium tin oxide market is estimated to be valued at US$2.1 billion in 2026.

The indium tin oxide market is projected to reach US$2.8 billion by 2033.

Key trends include the growing adoption of solar photovoltaic systems, increasing demand for high-performance display technologies, rising investments in semiconductor manufacturing, and a stronger focus on recycling and circular material use to address indium supply constraints.

The optoelectronics segment is the leading application, accounting for approximately 48.1% of the market share, supported by its extensive use in flat-panel displays, touchscreens, and electronic devices.

The indium tin oxide market is expected to grow at a CAGR of 4.4% between 2026 and 2033.

Some of the major players include JX Advanced Metals, Mitsui Mining & Smelting, Umicore, Corning Incorporated, and Indium Corporation.