- Plastics, Polymers & Resins

- Greenhouse Films Market

Greenhouse Films Market Size, Share, and Growth Forecast 2026 - 2033

Greenhouse Films Market by Resin Type (Low-density Polyethylene – LDPE, Linear Low-density Polyethylene – LLDPE, Ethylene-vinyl Acetate – EVA, Polyvinyl Chloride – PVC), by Thickness (80 to 150 Micron, 150 to 200 Micron, More than 200 Micron), by Application (Vegetables, Fruits, Flower & Ornaments, Others), and Regional Analysis for 2026 - 2033

Greenhouse Films Market Size and Trend Analysis

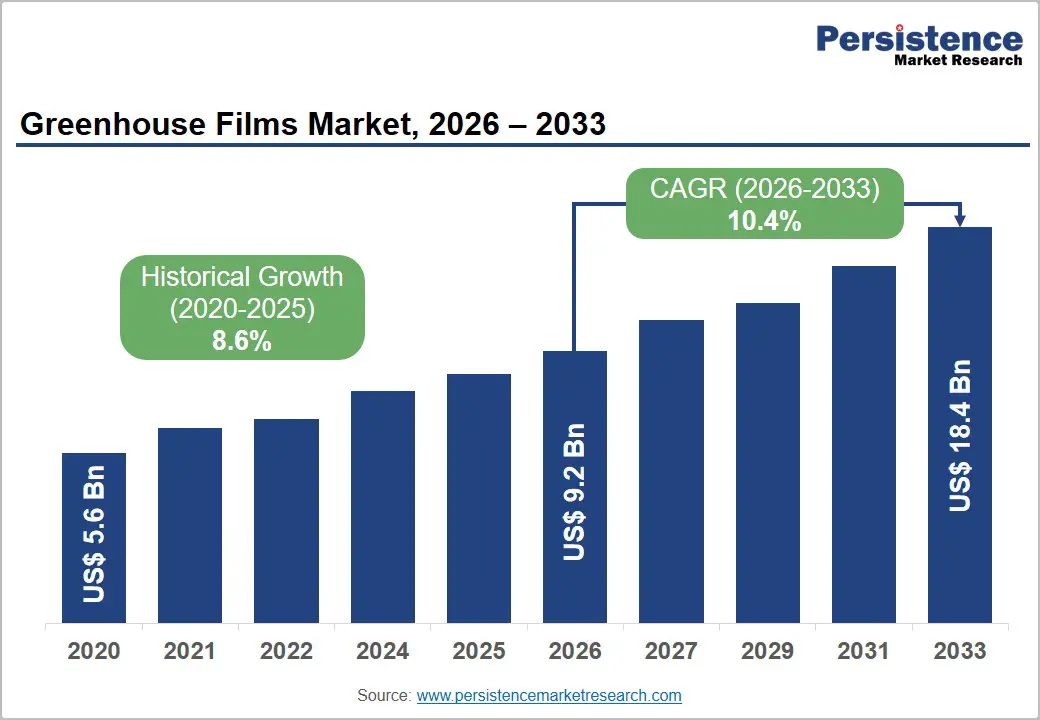

The global greenhouse films market size is expected to be valued at US$ 9.3 billion in 2026 and is projected to reach US$ 18.4 billion, growing at a CAGR of 10.4% between 2026 and 2033.

The inclination toward enhancing global food security, shift toward protected cultivation in response to extreme weather volatility, and rising demand for year-round fresh produce supply in both developed and emerging economies is driving growth. The Food and Agriculture Organization of the United Nations (FAO) projects that global food demand will increase by 50% by 2050, intensifying the adoption of controlled-environment agriculture where greenhouse films are the most cost-effective structural component.

Key Industry Highlights:

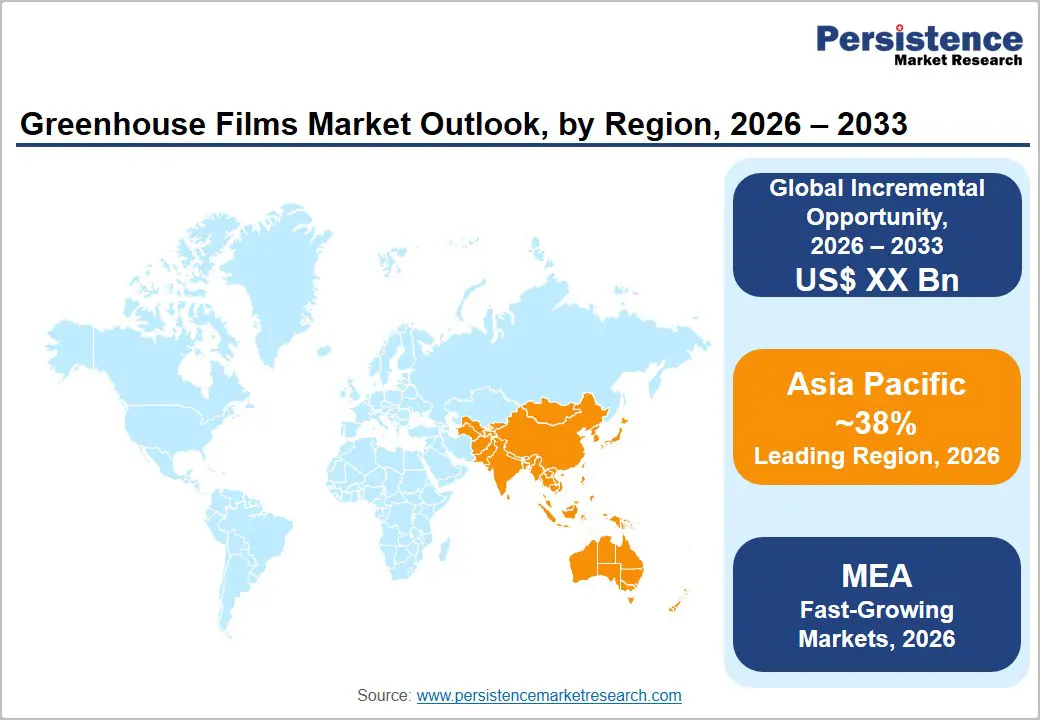

- Leading Region: Asia Pacific is likely to lead the global greenhouse films market with approximately 38% share in 2026, anchored by China's 3–4 million hectares of protected cultivation.

- Fast-Growing Market: Middle East & Africa is the fast-growing regional market, projected at an estimated CAGR of approximately 13%, driven by Saudi Arabia's Vision 2030 and UAE's National Food Security Strategy 2051, committing sovereign investment exceeding SAR 18 billion to controlled-environment agriculture infrastructure that mandates high-UV-stabilised premium greenhouse film procurement at large-scale commercial facilities.

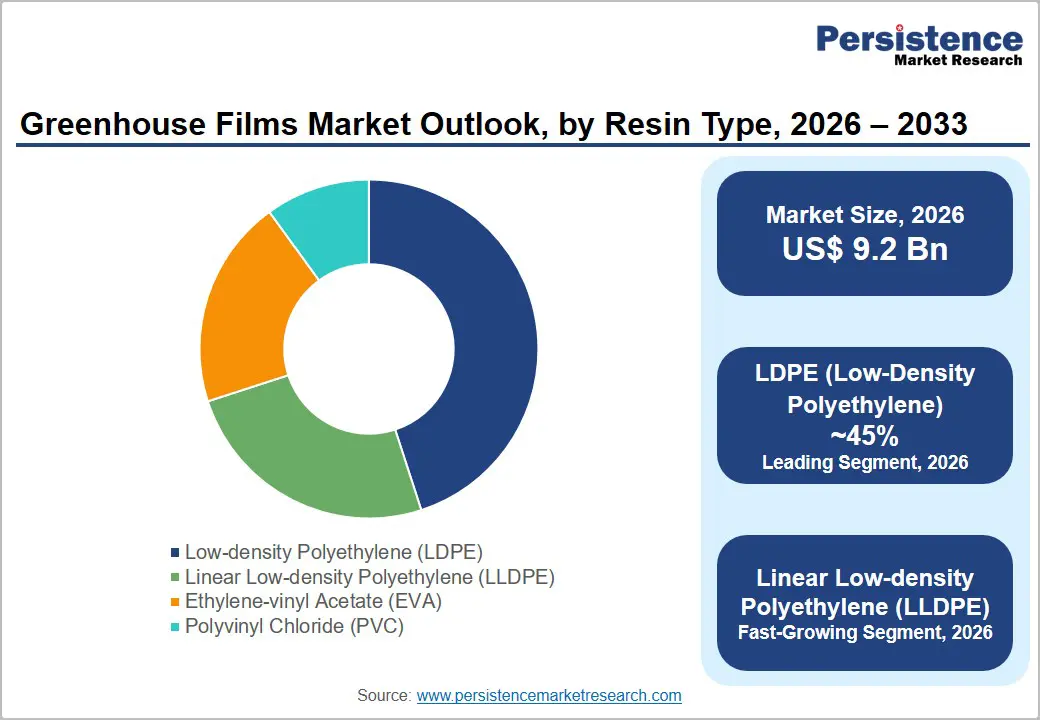

- Dominant Resin Type Segment: LDPE (Low-Density Polyethylene) dominates the resin type segment with approximately 45% market share in 2026, sustained by its industry-leading cost-effectiveness, broad global feedstock availability from ExxonMobil, LyondellBasell, and SABIC, and adequate performance characteristics for most commercial greenhouse applications.

- Fast-Growing Resin Type Segment: EVA (Ethylene-vinyl Acetate) films are the fast-growing resin type at an estimated CAGR of approximately 12.5%, driven by superior NIR-blocking, light diffusion, and thermicity properties that deliver measurable crop yield and energy efficiency advantages in high-technology greenhouse operations with premium ASPs 25–40% above standard LDPE equivalents.

- Key Opportunity: The highest-value market opportunity lies in government-funded greenhouse expansion programs across the Middle East, Africa, and South Asia, where Saudi SADF financing, India's NHM subsidies, and Egypt's national food security programs are creating policy-backed procurement pipelines for greenhouse films.

DRO Analysis

Drivers - Global Food Security Mandates and Protected Cultivation Expansion Driving Structural Demand

The increasing globalization of food supply chains and the rising frequency of climate-related agricultural disruptions are driving investments in protected cultivation infrastructure worldwide. According to the World Meteorological Organization, severe droughts, frost events, and irregular precipitation patterns are becoming more common across major agricultural regions.

As a result, governments and agribusinesses are increasingly adopting greenhouse cultivation systems, where greenhouse films act as a critical enabling material for crop protection and productivity enhancement. The FAO's State of Food Security and Nutrition report confirms that over 733 million people faced hunger in 2023, creating urgent policy momentum toward productivity-enhancing agricultural technologies.

Technological Advancement in Multi-Layer Film Formulations Elevating Performance and Replacement Demand

Advanced multi-layer greenhouse film formulations incorporating EVA, anti-drip, NIR (Near Infrared) diffusion additives, UV stabilisers, and anti-dust coatings are generating both a product upgrade cycle and per-unit revenue premiums that structurally support market value growth above volume growth. The European Committee for Standardisation (CEN) under EN 13206 sets performance certification benchmarks for greenhouse covering films that incentivise the adoption of technically superior multi-layer formulations.

These advanced films, offering 3–5-year operational lifespans versus 1–2 years for basic LDPE films, are creating an accelerated replacement market as growers in the Netherlands, Japan, and Israel systematically upgrade aging film installations. Leading producers Plastika Kritis and Armando Alvarez Group report that premium multi-layer films constitute an increasing share of total revenue, delivering ASP premiums of 25–40% over standard mono-layer equivalents.

Restraints - Plastic Waste Regulation and End-of-Life Film Disposal Burden Constraining Market Expansion

Increasingly stringent plastic waste regulation across the European Union, particularly the EU Single-Use Plastics Directive (2019/904/EC) and Extended Producer Responsibility (EPR) frameworks being applied to agricultural plastics, is creating compliance cost pressure and reputational headwinds for greenhouse film producers and agricultural plastic users.

The European Crop Protection Association estimates that agricultural plastic waste from mulch films, silage wrap, and greenhouse films generates over 1 million tonnes of plastic waste annually in Europe, with greenhouse films representing a significant fraction.

Volatility in Petrochemical Feedstock Prices Compressing Manufacturer Margins

Greenhouse films manufactured predominantly from LDPE, LLDPE, and EVA resin feedstocks derived from petrochemical processes are directly exposed to crude oil and natural gas price fluctuations that create manufacturing cost volatility. The U.S. Energy Information Administration (EIA) documented crude oil price variance exceeding 35% annually for 2020–2023, propagating margin instability across the plastic film value chain.

For greenhouse film manufacturers competing in a price-sensitive agricultural procurement market where growers routinely solicit competitive bids and frequently switch suppliers on price input cost spikes that cannot be fully passed through to customers, compressing operating margins and constraining R&D investment capacity at mid-tier producers.

Opportunities - EVA and Specialty Multi-Layer Films for High-Technology Greenhouse Applications

Ethylene-vinyl acetate (EVA) based greenhouse films represent the highest-growth opportunity within the resin type segment, projected at an estimated CAGR of approximately 12.5% in the forecast period. EVA copolymers offer superior optical properties, including high light diffusion capability, NIR-blocking performance, and strong heat retention characteristics.

These advantages make them the preferred material for advanced greenhouse operations across Northern Europe, Japan, and Israel, where improved light utilization and thermal efficiency help maximize crop yields while reducing energy costs. Evonik Industries' VESTOPLAST and Exxon Mobil's Escorene Ultra EVA grades are enabling film producers to develop highly differentiated specialty films targeting premium greenhouse segments.

Middle East & Africa Greenhouse Expansion Creating a High-Growth Frontier Market

The Middle East and Africa present the highest-growth frontier opportunity in the global greenhouse films market, with countries including Saudi Arabia, UAE, Egypt, Morocco, and Kenya implementing large-scale government-sponsored greenhouse development programs as part of food security and agricultural self-sufficiency strategies.

Saudi Arabia's Vision 2030 agricultural transformation plan and the UAE's National Food Security Strategy 2051 are committing billions in sovereign investment to controlled-environment agriculture infrastructure that is directly generating premium greenhouse film procurement demand at scales previously unseen in the region. Saudi Aramco's Wa'ed Ventures and the Saudi Agricultural Development Fund (SADF) have deployed over SAR 18 billion in agricultural development financing, a significant portion targeting greenhouse complex construction.

Category-wise Analysis

Resin Type Insights

Low-Density Polyethylene (LDPE) holds the dominant position in the global greenhouse films market by resin type, commanding approximately 45% of total market share in 2025. LDPE's market leadership is rooted in its unmatched combination of cost-effectiveness, processing versatility, and adequate optical and mechanical performance for standard commercial greenhouse applications.

LDPE's relatively low raw material cost enabled by large-scale global polyethylene production at ExxonMobil, LyondellBasell, and SABIC allows film producers to deliver competitively priced greenhouse covering solutions accessible to small and medium-scale growers in price-sensitive markets across Asia Pacific, Latin America, and Africa. According to Plastics Europe, LDPE remains the largest single polyethylene grade by global production volume, ensuring consistent feedstock availability and supply chain reliability that reinforces its specification preference for high-volume, cost-driven greenhouse film procurement.

Thickness Outlook Insights

The 80 to 150 Micron thickness range holds the leading position in the global greenhouse films market by thickness, accounting for approximately 48% of total market share in 2025. Films in this thickness band represent the optimal balance between material cost, mechanical durability, and installation handling ease for most commercial greenhouse applications from tunnel and multi-span structures in Spain and Morocco to Venlo-type glasshouse polymer cladding in Northern Europe.

The 80–150 micron range satisfies the structural requirements of most standard greenhouse designs under prevailing wind and snow load conditions, while delivering adequate light transmission (>85%) and acceptable UV stabilisation for 1–3 season service life at competitive cost per square metre.

Application Insights

Vegetables represent the dominant application segment in the global greenhouse films market, accounting for approximately 52% of the total share in 2026. Vegetable cultivation encompassing tomatoes, cucumbers, peppers, lettuce, and spinach drives the majority of commercial greenhouse construction globally due to the high economic returns per square metre achievable through controlled-environment production of premium-priced salad and cooking vegetables destined for urban retail, food service, and export markets.

The Netherlands' Wageningen University & Research documents that intensive hydroponic tomato cultivation in glass and plastic greenhouses achieves yields of 60–80 kg per square metre annually, approximately 10–15 times the open-field equivalent, validating the economic rationale for premium greenhouse infrastructure investment.

Regional Insights

North America Greenhouse Films Market Trends & Analysis

North America holds approximately 12% of the global greenhouse films market share in 2025, characterised by a high-technology, high-value greenhouse sector concentrated in the United States, Canada, and Mexico. The U.S. and Canadian greenhouse industries are dominated by large-scale commercial vegetable and cannabis production facilities deploying technically advanced multi-layer films with anti-drip, NIR, and UV-stabilisation properties.

Mexico's Sinaloa and Sonora states host extensive export-oriented vegetable greenhouse complexes supplying U.S. and Canadian retail chains, making Mexico a significant and growing greenhouse film consumer that is progressively upgrading from basic mono-layer LDPE to long-life multi-layer films that reduce annual replacement costs at large-scale operations.

U.S. Greenhouse Films Market Size

The United States holds approximately 88% of the North America greenhouse films market revenues in 2025, contributing an estimated US$ 975 million, growing at an approximate CAGR of 9.8% through 2033. U.S. market demand is anchored by the rapid commercial-scale expansion of CEA tomato, cucumber, and leafy greens operations anchored by AppHarvest (now Local Bounti), Gotham Greens, and Revol Greens, and the large-scale cannabis greenhouse industry across states where commercial cultivation is legalised, requiring compliant, light-management-optimised greenhouse film covering.

Europe Greenhouse Films Market Trends, Drivers, & Insights

Europe is likely to account for 30% of the share in 2026, representing the second-largest regional market, anchored by Spain, the Netherlands, Italy, France, and Turkey, collectively operating the world's highest-density commercial greenhouse cultivation infrastructure. European greenhouse films demand is characterised by a persistent upgrade cycle toward advanced multi-layer and specialty films, driven by rising energy costs, the EU Farm to Fork Strategy's sustainability mandates, and the continent's competitive premium fresh produce export economy.

European plastic film producers led by Plastika Kritis (Greece), Armando Alvarez Group (Spain), and Polifilm (Germany) maintain global technology and market leadership in EVA and multi-layer greenhouse film innovation, sustaining Europe's position as both the largest regional consumer and the world's primary exporter of premium greenhouse film technology.

Germany Greenhouse Films Market Size

Germany's greenhouse film market was valued at approximately US$ 304 million in 2025, representing approximately 12% of European greenhouse film revenues, advancing at an estimated CAGR of 9.2% through 2033. Germany's greenhouse sector, concentrated in the Baden-Württemberg, Bavaria, and North Rhine-Westphalia horticultural regions, drives demand for high-specification multi-layer films meeting DIN EN 13206 performance standards.

UK Greenhouse Films Market Size

UK greenhouse films market is likely to be valued at approximately US$ 207 million in 2026, reaching a CAGR of 8.8% in the coming years. The UK's greenhouse sector, dominated by tomato, cucumber, and soft fruit production in Kent, Lincolnshire, and Yorkshire relies on multi-layer EVA and LDPE greenhouse films supplied primarily through Berry Global and RPC BPI Group distribution channels.

France Greenhouse Films Market Size

France's greenhouse films market was valued at approximately US$ 258 million in 2026, growing at an estimated CAGR of 8.5%. French greenhouse cultivation led by tomato production in Bretagne and Pays de la Loire, and flower growing in the Provence-Alpes-Côte d'Azur region sustains consistent film replacement demand.

Asia Pacific Greenhouse Films Market Analysis

Asia Pacific is the largest and fastest-growing regional market, commanding approximately 38% of the global greenhouse films market share in 2026 and expanding at an estimated CAGR of approximately 12.2% through 2033. China alone accounts for the majority of Asia Pacific demand, operating an estimated 3–4 million hectares of protected cultivation, the world's largest national greenhouse area by a significant margin, according to the Chinese Academy of Agricultural Sciences (CAAS).

Japan's precision horticulture sector and South Korea's advanced greenhouse complex development contribute to high-technology, premium film demand, while India's rapidly expanding government-subsidised greenhouse programs.

China Greenhouse Films Market Size

China holds approximately 58% of the Asia Pacific greenhouse films market revenues in 2026, equivalent to an estimated US$ 1.86 billion, growing at a CAGR of approximately 11.8%. China's market is driven by the country's 3–4 million hectares of protected cultivation area, including solar greenhouses in northern provinces and plastic tunnel systems across Central and Southern China, generating the world's highest absolute volume of annual greenhouse film procurement.

India Greenhouse Films Market Size

India's greenhouse films market is likely to be valued at approximately US$ 449 million in 2025, growing at an estimated CAGR of approximately 14.2% in the coming years. India's protected cultivation area has expanded rapidly under National Horticulture Mission subsidies that cover 50% of greenhouse construction costs for small and marginal farmers, generating widespread first-generation greenhouse adoption.

Japan Greenhouse Films Market Trends

Japan's greenhouse films market represents approximately 10% of Asia Pacific revenues in 2026, contributing an estimated US$ 321 million, advancing at an estimated CAGR of 9.5%. Japan's highly sophisticated horticultural sector, characterised by premium produce quality standards and advanced controlled-environment cultivation practices, drives demand for technically superior multi-layer EVA and LLDPE films meeting JIS (Japan Industrial Standards) specifications.

Competitive Landscape

The global greenhouse films market is moderately fragmented, with Plastika Kritis, Armando Alvarez Group, Berry Global, Polifilm, and GINEGAR collectively holding an estimated 35–40% of global revenues at the premium film tier, while a large number of regional producers in China, India, Turkey, and Latin America compete on commodity LDPE price at standard specification tiers. Key competitive differentiators include proprietary multi-layer co-extrusion technology, EN 13206 / DIN certification portfolios, long-life film formulations, and application-specific additive packages. Sustainability-driven product development focusing on bio-based, recyclable, and UV-degradable film formulations is an emerging strategic theme as EPR regulations tighten across European markets.

Key Developments:

- In June 2025, Agriplast launched Agri50 Pro, a new patented film using patented glass microsphere technology. It combines an exceptional Near IR barrier with high levels of brightness and diffusion, supporting proper plant growth.

- In April 2025, Plastika Kritis launched four next-generation greenhouse films in the market, which are designed to boost productivity, enhance crop quality, and support sustainable farming practices.

Companies Covered in Greenhouse Films Market

- Plastika Kritis S.A.

- Armando Alvarez Group

- Berry Global Group Inc. (RPC BPI Agriculture)

- Polifilm GmbH

- GINEGAR Plastic Products Ltd.

- Agrishow S.p.A.

- Sekisui Chemical Co. Ltd.

- Mitsubishi Chemical Group

- SABIC

- Trioplast Industrier AB

- Keder Greenhouse (XINBAO Plastic)

- Agriplast S.r.l.

- Al-Shaheen Plastic Film Industries

Frequently Asked Questions

The global Greenhouse Films market is expected to be valued at US$ 9.3 billion in 2026 and is projected to reach US$ 18.4 billion, growing at a CAGR of 10.4% over the forecast period, representing a cumulative incremental opportunity of US$ 9.1 billion, supported by global food security imperatives and accelerating protected cultivation investment.

The primary drivers are the FAO's documented global food security imperative, with demand projected to increase 50% by 2050, and the shift to protected cultivation driven by climate volatility.

LDPE (Low-Density Polyethylene) leads the resin type segment with approximately 45% share in 2026, driven by its cost-effectiveness, processing versatility, and adequate performance for standard commercial greenhouse applications.

Asia Pacific leads the global greenhouse films market with approximately 38% share in 2026, anchored by China's estimated 3–4 million hectares of protected cultivation area (CAAS), India's NHM subsidy-driven adoption, and premium EVA film demand in Japan.

The leading global greenhouse films market participants are Plastika Kritis S.A., Armando Alvarez Group, Berry Global Group (USA), Polifilm GmbH, GINEGAR Plastic Products, Agrishow S.p.A., Sekisui Chemical, and SABIC.