- Plastics, Polymers & Resins

- Low Density Polyethylene Market

Low Density Polyethylene Market Size, Share, and Growth Forecast, 2026 - 2033

Low Density Polyethylene Market by Product Type (Film and Sheets, Extrusion Coatings, Injection Molded, Blow Molded, Others), Application (Agriculture, Packaging, Electrical & Electronics, Construction, Others), and Regional Analysis for 2026 - 2033

Low Density Polyethylene Market Size and Trends Analysis

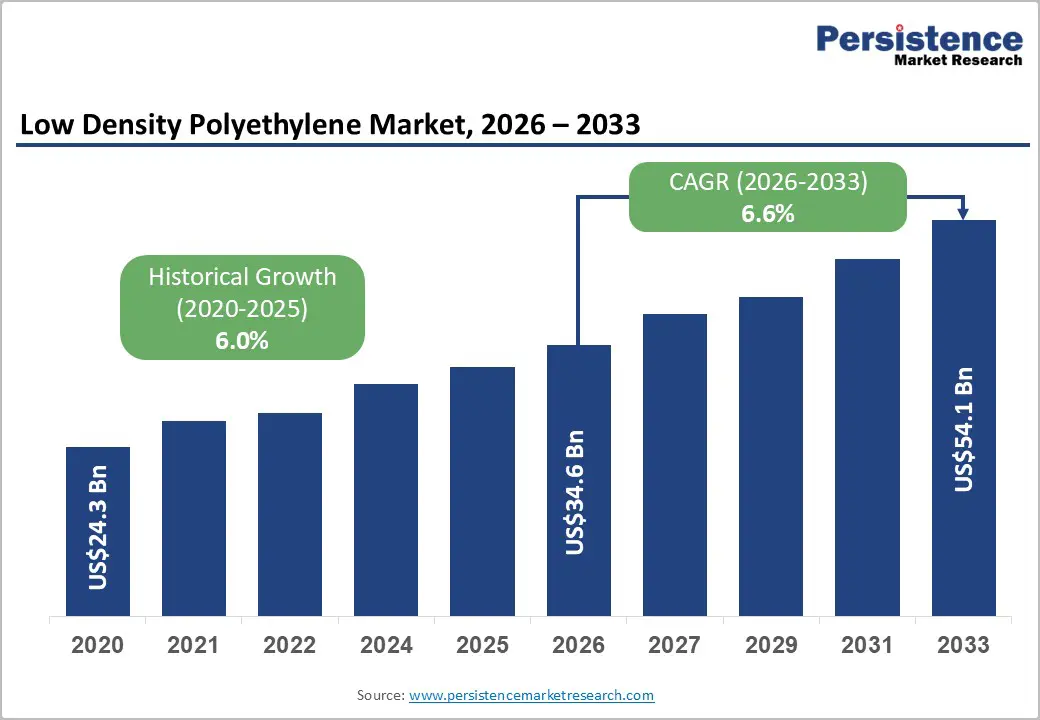

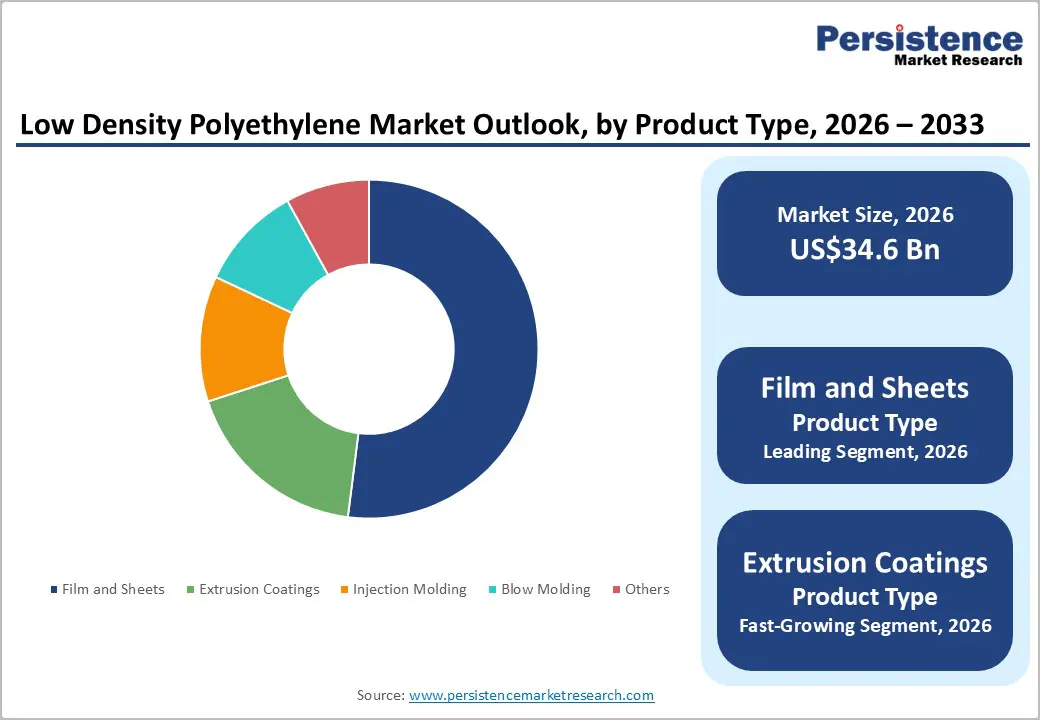

The global low density polyethylene market size is likely to be valued at US$34.6 billion in 2026, and is expected to reach US$54.1 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033, driven by strong demand for flexible packaging in food, e-commerce and consumer goods, increasing agricultural mulch film and greenhouse cover usage, rising construction activity requiring geomembranes and insulation films, and growing adoption in wire & cable insulation and injection molded consumer products.

The growing demand for film and sheets in packaging applications is accelerating adoption among converters and brand owners. Advances in autoclave and tubular LDPE grades, metallocene-modified resins, and recyclable formulations are further boosting uptake by offering excellent clarity, sealability, and downgauging potential. Increasing recognition of low-density polyethylene as a cost-effective, versatile, and lightweight material in emerging sustainable packaging, agricultural productivity, and infrastructure development markets remains a major driver of market growth.

Key Industry Highlights:

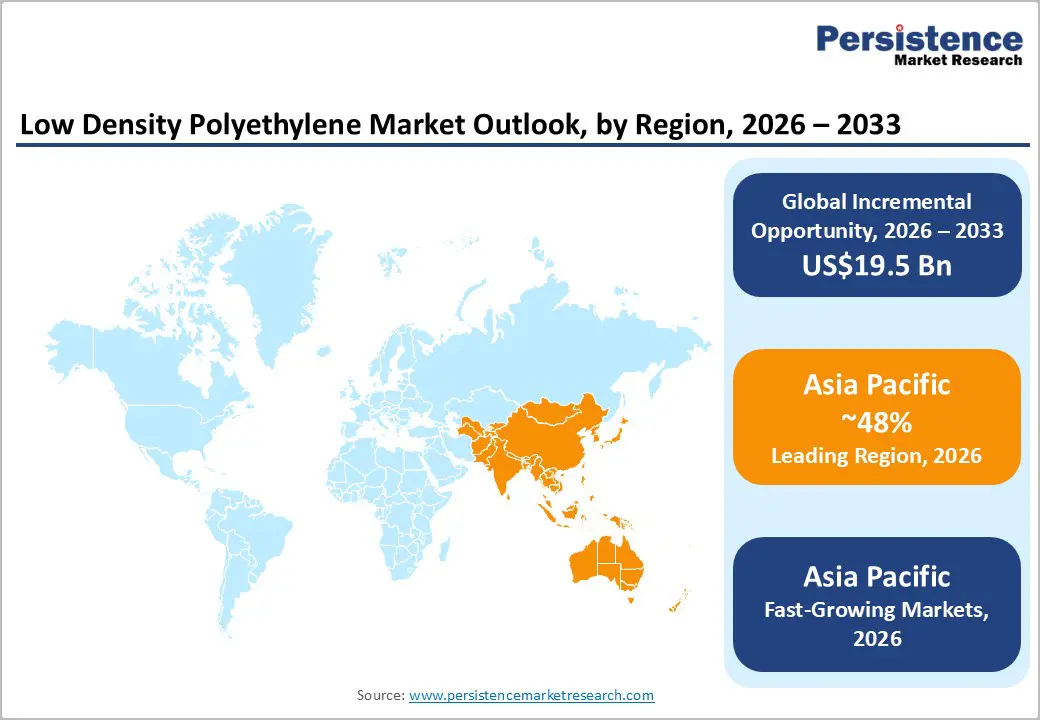

- Leading Region: Asia Pacific, anticipated to account for a 48% market share in 2026, driven by massive packaging production, agricultural film consumption, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by rapid e-commerce expansion, increasing greenhouse farming, and rising infrastructure investment.

- Dominant Product Type: Film and sheets, accounting for approximately 52% of the market share, as it remains the largest-volume application.

- Leading Application: Packaging, accounting for nearly 55% of market revenue due to the dominant consumption of flexible and rigid packaging.

| Key Insights | Details |

|---|---|

|

Low-Density Polyethylene Market Size (2026E) |

US$34.6 Bn |

|

Market Value Forecast (2033F) |

US$54.1 Bn |

|

Projected Growth CAGR (2026-2033) |

6.6% |

|

Historical Market Growth (2020-2025) |

6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis – Flexible Packaging Expansion and Agricultural Film Demand

The growing demand for lightweight, durable, and sustainable packaging solutions is driving rapid growth in the flexible packaging sector. Manufacturers are increasingly adopting materials such as polyethylene, polypropylene, and biodegradable polymers to create packaging that offers superior protection, a longer shelf life, and easier transport. The surge in e-commerce and food delivery services has further accelerated the need for flexible packaging, as it minimizes storage space and reduces shipping costs. Innovations in multilayer films and printable materials are also enabling brands to enhance product appeal and meet consumer expectations for convenience and aesthetics.

The agricultural sector is witnessing a significant increase in the use of plastic films for applications including mulching, greenhouse covers, silage, and irrigation systems. These films help improve crop yields by controlling temperature, moisture, and weed growth while reducing water usage. Advances in UV-resistant and biodegradable agricultural films are gaining traction, aligning with environmental sustainability goals and reducing plastic waste. The combination of enhanced performance, cost-effectiveness, and eco-friendly innovations is boosting adoption across both urban and rural markets, ensuring that flexible packaging and agricultural films continue to play a critical role in modern supply chains and farming practices.

Construction and Wire & Cable Sector Growth

The construction industry is experiencing a surge in activity driven by urbanization, infrastructure development, and government initiatives to modernize public facilities. Rising demand for residential, commercial, and industrial projects has increased the need for construction materials, machinery, and advanced technologies that improve efficiency and safety. Sustainable construction practices are also gaining traction, with builders increasingly incorporating energy-efficient materials, green buildings, and smart infrastructure solutions. This shift not only reduces environmental impact but also enhances long-term operational efficiency, making projects more attractive to investors and stakeholders.

The wire and cable sector is expanding in response to rising electricity consumption, industrial automation, and the growth of renewable energy installations. High-voltage transmission lines, underground cabling, and fiber-optic networks are being deployed to support expanding smart grids and digital communication systems. Innovations in lightweight, fire-resistant, and corrosion-resistant cables are supporting safer and more efficient installations across residential, commercial, and industrial sectors. The increasing adoption of electric vehicles and energy storage systems is further driving demand for specialized cables capable of handling higher currents and voltages.

Barrier Analysis – Feedstock Price Volatility and Supply Disruptions

Global industries are facing increasing challenges due to fluctuating feedstock prices and intermittent supply disruptions. Raw materials such as crude oil derivatives, polymers, and specialty chemicals are subject to market-driven price swings influenced by geopolitical tensions, regulatory changes, and seasonal demand variations.

Supply chain disruptions caused by natural disasters, transportation bottlenecks, or trade restrictions further complicate procurement planning. Companies are being compelled to diversify their supplier base, maintain higher inventory levels, and adopt agile sourcing strategies to mitigate risks.

Environmental Pressure and Recycling Challenges

Industries are under mounting pressure to reduce environmental impact as governments, consumers, and investors demand sustainable practices. Single-use plastics, packaging waste, and industrial byproducts are attracting increasing scrutiny, prompting companies to adopt eco-friendly materials, reduce emissions, and implement waste-minimization strategies.

Recycling remains a key challenge due to the complexity of multi-layered materials, contamination, and limited infrastructure for efficient collection and processing. While biodegradable and recyclable alternatives are emerging, scaling these solutions across supply chains is difficult and often cost-intensive.

Opportunity Analysis – Advancements in Recyclable and Bio-based LDPE Grades

Low-Density Polyethylene (LDPE) is evolving rapidly as manufacturers and consumers push for more sustainable alternatives to conventional plastics. Recent developments focus on producing recyclable and bio-based LDPE grades that retain the material’s inherent flexibility, durability, and chemical resistance while reducing environmental impact. These innovations allow LDPE to be reprocessed multiple times without significant loss of mechanical properties, enabling circular-economy practices and reducing plastic waste in landfills.

Bio-based LDPE, derived from renewable sources such as sugarcane or corn, is gaining popularity as it offers a smaller carbon footprint compared to fossil-fuel-based polymers. These grades are compatible with existing processing equipment and can be used in films, packaging, and agricultural applications, making the transition to greener materials smoother for manufacturers. Technological improvements in polymerization, compatibilizers, and additive packages are enhancing performance characteristics such as tensile strength, clarity, and barrier properties. This allows recyclable and bio-based LDPE to meet the same standards as traditional grades while addressing sustainability concerns.

Expansion in E-commerce Packaging

The rapid growth of online retail has significantly transformed packaging requirements, driving innovation and expansion in e-commerce packaging solutions. Businesses are increasingly seeking materials and designs that ensure products arrive safely while minimizing shipping costs and environmental impact. Lightweight, durable, and protective packaging has become a necessity, especially for fragile or high-value items, prompting the adoption of bubble wraps, padded mailers, corrugated boxes, and flexible packaging films.

Customization is another key trend, as brands aim to enhance customer experience through branded packaging, easy-to-open designs, and sustainable materials. Sustainable packaging solutions, such as recyclable, biodegradable, or compostable materials, are gaining traction in response to consumer demand for environmentally responsible practices. Automation and smart packaging technologies are also playing a role, enabling efficient packing, accurate sizing, and real-time shipment tracking.

Category-wise Analysis

Product Type Insights

Films and sheets are anticipated to dominate the market, accounting for 52% of the market share in 2026. Their dominance is driven by their versatility and wide range of applications. These products are extensively used in packaging, agriculture, construction, and industrial sectors because of their flexibility, lightweight nature, and cost-effectiveness. Their ability to provide protection, barrier properties, and easy customization makes them highly preferred by manufacturers and end-users. Amcor plc and its flexible film solutions. Amcor produces a wide range of polyethylene (PE) and polypropylene (PP) shrink and overwrap films used to protect, bundle, and display food, beverage, and industrial products.

Extrusion coatings represent the fastest-growing product type, due to their ability to enhance the functionality and durability of base materials such as paper, cardboard, and films. These coatings provide superior barrier properties against moisture, grease, and chemicals, making them ideal for food packaging, liquid containers, and industrial applications. Their seamless integration during manufacturing ensures strong adhesion, uniform coverage, and improved product lifespan. Dow Inc., which supplies DOW™ LDPE resins specifically formulated for extrusion-coating applications such as paperboard and foil used in food and packaging products. Their LDPE grades are designed to create strong moisture and vapor barrier layers when extrusion-coated onto substrates, helping protect products in transit and extend shelf life.

Application Insights

The packaging segment is expected to dominate the market, accounting for nearly 55% of revenue in 2026, driven by increasing demand for protective, convenient, and sustainable solutions. The rising e-commerce, food delivery, and retail sectors are driving demand for flexible, durable, and lightweight packaging materials. Manufacturers are adopting recyclable, biodegradable, and high-barrier films to preserve product quality while meeting environmental expectations. Innovations in customization, branding, and automation are enhancing consumer experience and operational efficiency. Tetra Pak, a global packaging company known for its aseptic carton solutions used by food and beverage brands worldwide. In 2024, Tetra Pak reported revenue of about €12.8 billion (US$$13.9 billion) from its packaging products, reflecting the strong contribution of its packaging segment to overall earnings.

The construction segment is the fastest-growing application, driven by rising infrastructure development, urbanization, and government investments in residential and commercial projects. Materials such as films, sheets, and coatings are increasingly used for insulation, moisture barriers, protective coverings, and surface finishing. These products improve durability, energy efficiency, and safety in buildings while reducing labor and maintenance costs. Demand for sustainable construction materials is encouraging the adoption of recyclable and high-performance polymers. E. I. du Pont de Nemours and Company and its Tyvek® building wrap products. DuPont’s Tyvek house wraps, a high-performance polyethylene material used as an air and moisture barrier in residential and commercial construction, have become widely adopted globally to protect buildings during construction and improve energy efficiency.

Regional Insights

North America Low Density Polyethylene Market Trends

North America market is propelled by its extensive use across the packaging, construction, agriculture, and consumer goods industries. The region has a well-established petrochemical infrastructure, supported by abundant shale gas resources that provide cost-effective raw materials for polyethylene production. The availability of feedstock enables manufacturers to maintain consistent production and supply to both domestic and export markets. Flexible packaging remains a major application area, particularly in food packaging, e-commerce shipping materials, and protective films, as companies prioritize lightweight and durable materials that improve logistics efficiency.

Sustainability trends are also shaping the LDPE market in North America. Companies are increasingly investing in recyclable materials, recycled-content films, and advanced polymer technologies that reduce environmental impact while maintaining performance. Growing consumer awareness and regulatory initiatives to reduce plastic waste are encouraging manufacturers to develop LDPE products that are easier to recycle and compatible with circular-economy initiatives.

Europe Low-Density Polyethylene Market Trends

Europe’s growth is fueled by strong sustainability initiatives, advanced recycling infrastructure, and steady demand from packaging and industrial applications. Policies such as circular-economy programs and packaging regulations are pushing manufacturers to develop recyclable LDPE films and to incorporate recycled content into packaging products. Packaging remains the primary driver of LDPE consumption in Europe, particularly in food packaging, shrink films, and protective wraps used in retail and logistics.

Film extrusion applications account for a significant portion of LDPE demand as manufacturers continue to develop lightweight, flexible, and high-barrier packaging solutions. The growing adoption of recycled and bio-based polyethylene materials. European producers are investing in chemical recycling technologies and partnerships to convert plastic waste into feedstock for new LDPE production. These efforts support the region’s long-term sustainability goals while maintaining material performance and supply stability.

Asia Pacific Low-Density Polyethylene Market Trends

Asia Pacific is expected to dominate and be the fastest-growing region, capturing 48% of revenue in 2026, driven by rapid industrialization, urbanization, and expanding consumer markets. Countries such as China, India, Japan, and South Korea are major contributors to regional demand, driven by their large manufacturing bases and growing populations. The increasing consumption of packaged food, beverages, and consumer goods has significantly increased demand for flexible packaging materials, where LDPE is widely used for films, bags, and protective wraps due to its flexibility and moisture resistance.

The rapid expansion of e-commerce platforms across the region is also accelerating the demand for lightweight and durable packaging solutions. LDPE films and mailing bags are commonly used to protect products during storage and transportation. The agriculture sector in many Asia Pacific countries relies heavily on LDPE films for greenhouse covers, mulch films, and irrigation applications, helping improve crop productivity and water management. Infrastructure development and construction activities are another important factor supporting LDPE demand.

Competitive Landscape

The global low density polyethylene (LDPE) market is characterized by strong competition between large integrated petrochemical companies and specialized resin producers. Major multinational companies such as Dow Inc., LyondellBasell Industries N.V., and Exxon Mobil Corporation dominate markets in North America and Europe due to their extensive production capacities, diversified product portfolios, and well-established relationships with packaging manufacturers. These companies focus heavily on research and development, introducing advanced polymer technologies such as metallocene-based polyethylene and exploring bio-based material innovations to meet evolving sustainability goals.

In the Asia Pacific region, regional manufacturers and emerging petrochemical companies compete by offering cost-effective LDPE solutions that support growing demand from the packaging, agriculture, and construction sectors. Competitive pricing and local supply chains allow these players to expand market accessibility in rapidly developing economies. Film and sheet applications continue to strengthen LDPE demand by improving packaging efficiency, reducing material consumption, and supporting large-scale conversion processes.

Key Industry Developments:

- In February 2026, NOVA Chemicals Corporation launched two new recycled polyethylene grades, SYNDIGO rPE-IN3 and SYNDIGO rPE-IN4, for general-purpose applications in North America. The company developed these grades using 100% post-consumer recycled (PCR) plastic films and produced them at its SYNDIGO1 mechanical recycling facility in Connersville, Indiana.

- In July 2025, Dow Inc. introduced INNATE™ TF 220 Precision Packaging Resin, a new material designed to improve the recyclability and performance of flexible plastic packaging. The company developed the resin to support circular economy initiatives by enabling the production of strong, flexible packaging that is easier to recycle.

Companies Covered in Low Density Polyethylene Market

- DuPont

- DOW

- Qatar Petrochemical Company (QAPCO) Q.P.J.S.

- LyondellBasell Industries Holdings B.V.

- Goodfish Group Ltd.

- RTP Company

- Exxon Mobil Corporation

- LG Chem

- Chevron Phillips Chemical Company LLC.

- SABIC

Frequently Asked Questions

The global low density polyethylene market is projected to reach US$34.6 billion in 2026.

The low-density polyethylene market is driven by the rapid growth of flexible packaging, along with increasing demand for construction and agricultural films.

The low density polyethylene market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Key market opportunities include the development of bio-based and recyclable polyethylene grades, along with the expansion of e-commerce packaging across the Asia Pacific region.

Dow, LyondellBasell, Exxon Mobil, SABIC, and Chevron Phillips Chemical are the key players.