- Smart Packaging

- Glass Bottles and Containers Market

Glass Bottles and Containers Market Size, Share, and Growth Forecast, 2026 - 2033

Glass Bottles and Containers Market by Product Type (Bottles, Vials, Others), Capacity (Medium Bottles (250-750 ml), Small Bottles (up to 250 ml), Others), Glass Color, Application, and Regional Analysis for 2026 - 2033

Glass Bottles and Containers Market Size and Trends Analysis

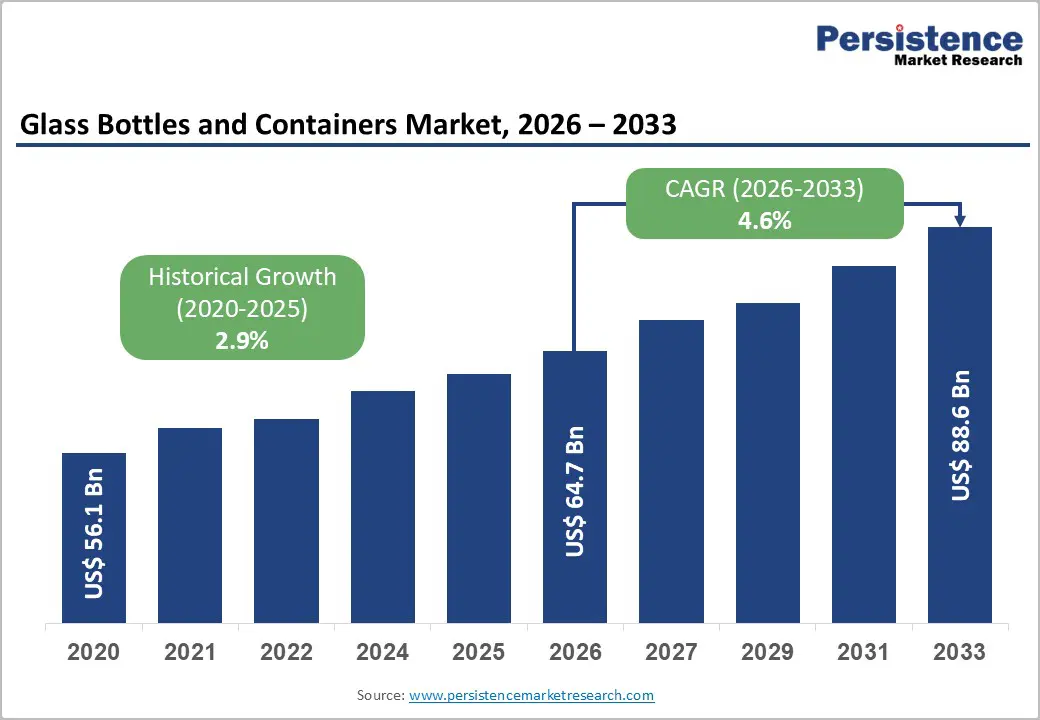

The global glass bottles and containers market size is likely to be valued at US$64.7 billion in 2026 and is expected to reach US$88.6 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033, driven by steady demand from beverages and pharmaceuticals, increasing preference for recyclable packaging, and capacity investments by major container manufacturers.

Sustainability policies, lightweight glass technologies, and rising middle-class consumption in emerging markets continue to support long-term growth, while energy cost volatility, raw material price fluctuations, and trade regulations remain structural challenges. The following analysis provides a structured, data-driven overview designed for strategic decision-making and investment planning.

Key Industry Highlights

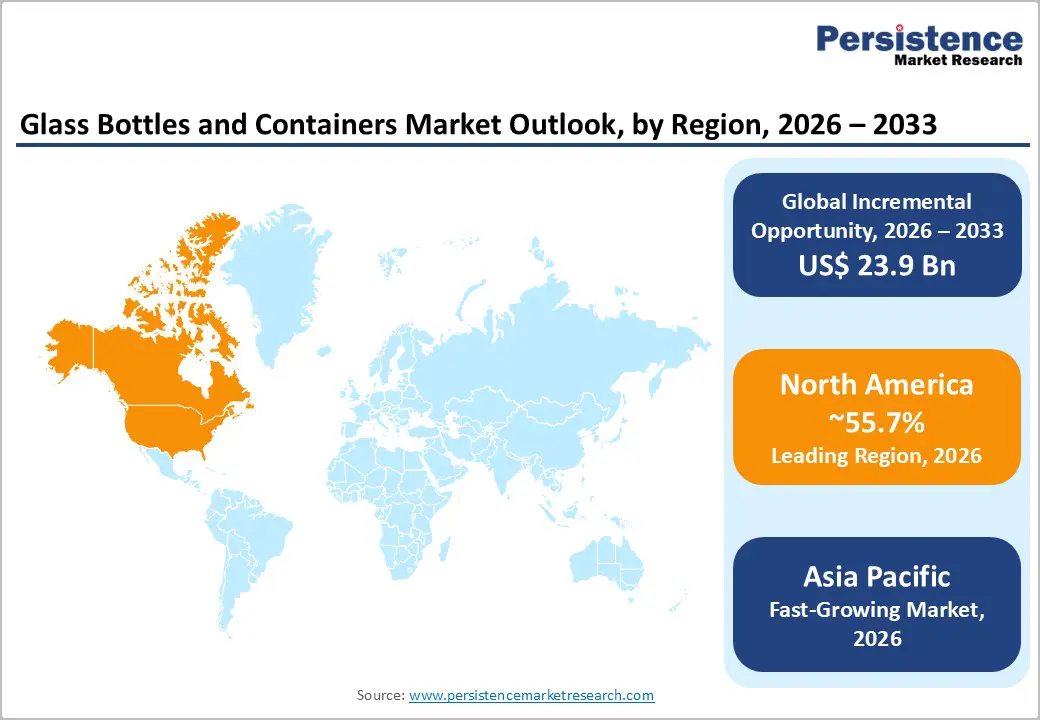

- Leading Region: North America is projected to lead the market, accounting for approximately 55.7% of market revenue, supported by strong beverage consumption, premium spirits demand, and a well-established glass manufacturing infrastructure.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, driven by rising beverage consumption, expanding pharmaceutical manufacturing, and increasing packaging demand across emerging economies such as China and India.

- Investment Plans: Major manufacturers are investing in furnace modernization, lightweight glass technologies, and higher recycled-content production, enabling improved energy efficiency, supporting sustainability goals, and expanding production capacity.

- Dominant Product Type: Bottles are the dominant product type, accounting for approximately 59.3% of market revenue, primarily driven by strong demand in beverage packaging applications.

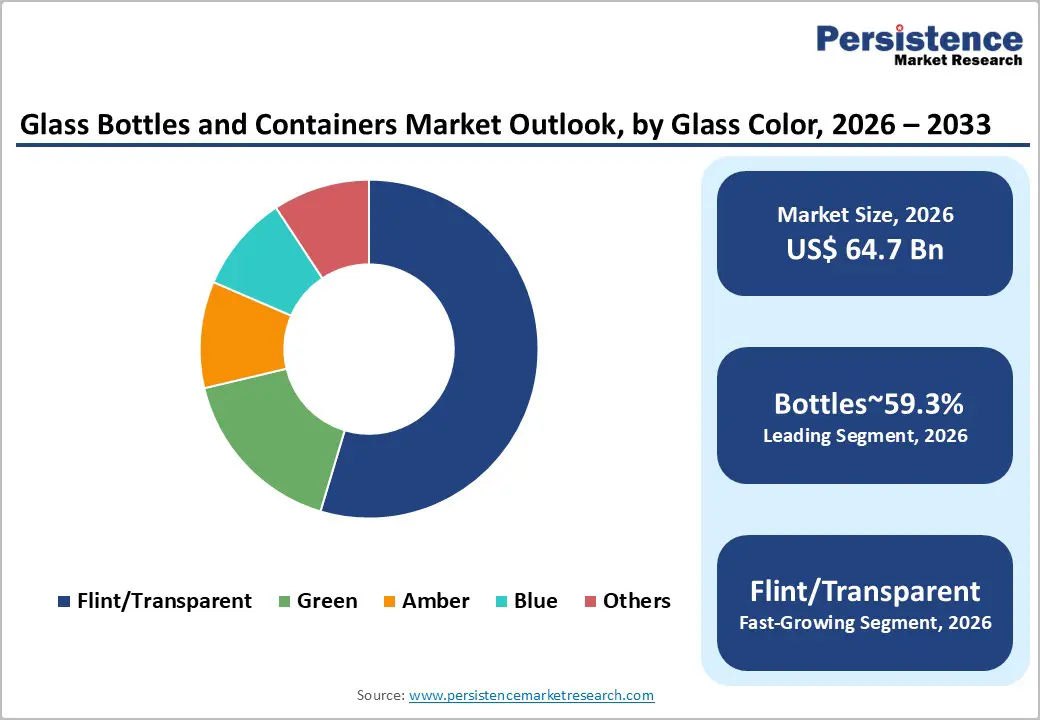

- Leading Glass Color: Flint or transparent glass is the leading color segment, anticipated to hold around 46.5% of market share, owing to its wide adoption across beverage, food, cosmetic, and pharmaceutical packaging industries.

| Key Insights | Details |

|---|---|

| Glass Bottles and Containers Market Size (2026E) | US$64.7 Bn |

| Market Value Forecast (2033F) | US$88.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Beverage Consumption and Premiumization

The beverage industry represents the largest application segment for glass containers, accounting for approximately 46.1-52.3% of market value. Demand for bottled alcoholic beverages such as wine, craft beer, and premium spirits continues to expand globally, driving steady consumption of glass bottles. Glass packaging is widely preferred in these categories because it preserves flavor integrity and conveys a premium brand image. Growing consumer preference for artisanal beverages and premium non-alcoholic drinks has further increased demand for customized bottle designs, embossed logos, and heavier base bottles. Manufacturers are investing in modern furnaces and lightweight bottle designs to improve production efficiency while maintaining durability and aesthetic appeal. These innovations reduce shipping weight and logistics costs, strengthening glass packaging’s competitiveness within the beverage supply chain.

Sustainability Regulations and Circular Packaging Initiatives

Global sustainability initiatives are accelerating the adoption of recyclable packaging materials, strengthening demand for glass containers. Governments and environmental agencies are implementing extended producer responsibility (EPR) programs, packaging recycling targets, and waste reduction policies that encourage circular packaging systems. Glass is uniquely positioned in this transition because it can be recycled indefinitely without loss of quality. Many manufacturers have increased the use of recycled glass, known as cullet, in production processes to reduce energy consumption and raw material use. Higher cullet usage lowers carbon emissions associated with glass melting while improving manufacturing efficiency. These sustainability advantages have made glass packaging a preferred choice for environmentally conscious brands, particularly in beverages, cosmetics, and pharmaceuticals.

Technological Advancements in Lightweight and Recycled Glass

Technological innovation in glass manufacturing has significantly improved production efficiency and product performance. Advanced forming techniques, such as press-and-blow and narrow-neck press-and-blow processes, enable manufacturers to produce lighter yet stronger bottles while maintaining structural integrity. Lightweighting technologies reduce the amount of glass used per unit while preserving durability and product safety. At the same time, modern furnace designs and improved sorting technologies allow greater integration of recycled glass into production. Higher recycled content reduces the energy required for melting raw materials, lowering both operational costs and carbon emissions. These technological improvements enable manufacturers to meet sustainability targets while maintaining competitive pricing and high product quality.

Barrier Analysis - Energy-Intensive Manufacturing and Cost Volatility

Glass manufacturing requires extremely high furnace temperatures, making the industry highly energy-intensive. Fuel costs, electricity prices, and raw material expenses represent a significant portion of production costs. Periods of elevated energy prices can compress profit margins and force manufacturers to adjust production levels or temporarily idle furnaces. Smaller producers are particularly vulnerable to energy price fluctuations because they often operate with lower economies of scale. In many production facilities, energy expenses account for approximately 15-25% of total manufacturing costs, making the sector sensitive to fuel market volatility.

Trade Regulations and Import Competition

International trade dynamics also influence the glass container market. Some regions face competitive pressure from imported glass containers produced in countries with lower energy costs and labor expenses. Import surges in specific bottle formats can disrupt domestic pricing structures and complicate capacity planning for local manufacturers. Anti-dumping regulations, tariffs, and trade policies can introduce uncertainty into supply chains, affecting long-term investment decisions. These factors create operational challenges for manufacturers operating in highly competitive global markets.

Opportunity Analysis - Customized and Premium Glass Packaging

Brand differentiation and premium product positioning are creating opportunities for customized glass packaging solutions. Beverage and cosmetic companies increasingly seek distinctive packaging designs that enhance brand identity and shelf visibility. Decorative techniques such as embossing, screen printing, color coatings, and specialty closures enable manufacturers to offer high-value packaging solutions. Limited-edition bottle designs and bespoke molds are particularly attractive to craft beverage producers and premium spirits brands. By offering integrated design, manufacturing, and decoration services, glass packaging companies can strengthen customer relationships and increase revenue per unit.

Expansion of Pharmaceutical Glass Packaging

The pharmaceutical industry is among the fastest-growing application segments for glass containers. Injectable medicines, biologics, and vaccines require chemically stable packaging materials that prevent contamination and maintain product integrity. Glass vials, ampoules, and cartridges remain essential components of pharmaceutical packaging because they provide excellent barrier properties and chemical resistance. As global healthcare systems expand and biotechnology innovations accelerate, demand for pharmaceutical-grade glass packaging is expected to increase significantly. Manufacturers capable of producing high-purity glass containers in controlled environments can secure long-term supply agreements with pharmaceutical companies.

Category-wise Analysis

Product Type Insights

Bottles are anticipated to account for approximately 59.3% of market revenue in 2026, making them the dominant product category in the market. Their leadership is primarily driven by the beverage industry, which relies heavily on glass bottles for alcoholic beverages, carbonated drinks, juices, bottled water, and specialty drinks. Glass bottles provide strong barrier properties that preserve flavor, carbonation, and product freshness while preventing contamination. They are also widely used in the food sector for sauces, condiments, syrups, and specialty oils. For example, global beverage brands in the beer and wine industries consistently use glass bottles for packaging due to their premium appearance and superior product protection.

Large beverage manufacturers typically establish long-term supply agreements with glass container producers to ensure consistent product quality, stable supply chains, and standardized bottle specifications across markets. Continuous innovations such as lightweight bottle designs and enhanced molding techniques introduced by leading glass manufacturers are further strengthening this segment by reducing material consumption, lowering transportation costs, and improving overall production efficiency.

Vials represent the fastest-growing product type segment, largely driven by the rapid expansion of the pharmaceutical and biotechnology industries. Injectable medicines, vaccines, biologics, and specialty pharmaceutical formulations require sterile and chemically stable packaging solutions that can maintain product integrity throughout storage and transportation. Glass vials are particularly suitable for these applications as they offer high chemical resistance, excellent temperature tolerance, and strong protection against contamination. The increasing global production of vaccines, insulin products, and biologic drugs has significantly boosted demand for pharmaceutical-grade glass vials.

For instance, large pharmaceutical manufacturers and contract manufacturing organizations depend on high-quality borosilicate glass vials to package injectable treatments and advanced therapies. Rising investments in vaccine manufacturing facilities and biologic drug development pipelines are further accelerating demand for pharmaceutical glass containers. Manufacturers capable of meeting strict pharmaceutical manufacturing standards, including clean-room production and quality validation requirements, are expected to benefit substantially from this expanding market segment.

Glass Color Insights

Flint or transparent glass is anticipated to account for around 46.5% of market share in 2026, making it the leading color segment in the global glass bottles and containers market. Transparent glass remains widely preferred because it allows consumers to clearly see the product inside the container, improving product visibility and reinforcing perceptions of freshness and quality. It is commonly used for beverages, packaged foods, cosmetics, and pharmaceutical products where product appearance plays a key role in purchasing decisions.

Transparent glass also supports diverse branding strategies because it can be easily combined with a wide range of labels, decorative coatings, embossing, and closures. For example, many premium water brands, cold-pressed juice producers, and gourmet food companies use clear glass containers to showcase the natural color and quality of their products. The versatility of flint glass across multiple end-use industries ensures sustained production volumes and widespread adoption among global packaging manufacturers.

Green glass represents the fastest-growing color segment, supported by increasing demand for premium beverage packaging and traditional beverage presentation. Many wine, beer, and specialty beverage brands prefer green glass because it effectively protects against light exposure, helping preserve flavor stability and product quality. The color is also closely associated with heritage wine packaging and premium craft beverages, making it a popular choice for brand differentiation.

For instance, numerous European wine producers and craft breweries use green glass bottles to emphasize authenticity and product heritage. Green glass packaging also supports premium brand positioning in craft beverage markets where distinctive packaging plays a critical role in consumer appeal. As environmentally conscious branding continues to gain traction, green glass containers are increasingly linked with sustainability messaging and traditional beverage production practices, which further supports their growing adoption in the global market.

Regional Insights

North America Glass Bottles and Containers Market Trends - Premium Beverage Demand and Recycling-Driven Production Expansion

North America is projected to lead the global glass bottles and containers market with approximately 55.7% market share in 2026, driven by strong beverage consumption, a mature packaging industry, and advanced manufacturing infrastructure. The United States represents the largest national market in the region, supported by extensive production capacity and well-established supply chains connecting glass manufacturers with beverage and food companies. The U.S. beverage industry remains the primary driver of demand, particularly in alcoholic beverages such as wine, spirits, and craft beer.

Growing consumer preference for premium beverages has increased demand for decorative and customized glass bottles. The region also benefits from a strong pharmaceutical manufacturing sector, which requires high-quality glass containers for injectable medicines and laboratory applications.

Government initiatives promoting recycling and sustainable packaging further strengthen the glass container market in North America. Recycling infrastructure in the region supports large-scale collection and reuse of glass materials, enabling manufacturers to incorporate recycled content into production processes. Sustainability commitments by beverage brands have also accelerated the shift toward recyclable packaging solutions.

Investment trends in the region include modernization of glass furnaces, expansion of lightweight bottle production, and improvements in energy efficiency. Major manufacturers continue to invest in new production technologies and plant upgrades to improve productivity and reduce carbon emissions. Strategic collaborations between packaging manufacturers and beverage companies are also becoming more common, ensuring stable supply agreements and supporting long-term market growth.

Europe Glass Bottles and Containers Market Trends-Wine Industry Demand and Circular Packaging Regulations

Europe represents one of the most established markets for glass bottles and containers, supported by strong demand from the wine, spirits, and specialty food industries. Countries such as Germany, France, the U.K., and Spain play key roles in regional production and consumption. Germany maintains a highly advanced glass manufacturing sector, with companies investing in energy-efficient furnaces and high recycled-content production processes. France remains a global hub for wine and spirits production, which generates significant demand for decorative and premium glass bottles. Spain and the United Kingdom contribute to the regional market through beverage manufacturing, food packaging, and export activities.

European environmental policies strongly support the glass container industry. The region has implemented comprehensive packaging waste regulations and recycling targets that encourage circular packaging systems. Glass packaging performs well under these regulatory frameworks because it can be reused and recycled multiple times without degradation. Manufacturers across Europe are investing in decarbonization technologies, including furnace electrification and waste heat recovery systems. These initiatives aim to reduce greenhouse gas emissions associated with glass production while maintaining high product quality. Investments in decorative finishing technologies are also expanding as beverage brands seek distinctive packaging solutions for premium products.

Asia Pacific Glass Bottles and Containers Market Trends - Rapid Beverage Consumption Growth and Manufacturing Expansion

Asia Pacific is likely to be the fastest-growing region in the market, driven by rapid economic development, urbanization, and increasing consumer spending. Countries such as China, Japan, India, and several Southeast Asian nations are experiencing strong demand for packaged beverages, cosmetics, and pharmaceutical products. China remains the largest manufacturing hub in the region, with extensive production capacity and integrated supply chains supporting both domestic consumption and export markets. The country’s beverage industry continues to expand, driving demand for glass packaging across alcoholic and non-alcoholic drink categories. Japan specializes in high-precision glass manufacturing, particularly for pharmaceutical containers and specialty packaging. Japanese manufacturers focus on quality, innovation, and advanced production technologies that enable high-performance glass packaging.

India represents one of the fastest-expanding markets in Asia Pacific due to growing urban populations and increasing demand for consumer packaged goods. Investments in new glass manufacturing facilities and modernization of existing plants are supporting the country’s expanding beverage and pharmaceutical sectors. Regional governments are implementing policies that encourage domestic manufacturing and environmental sustainability. These policies support investments in modern glass production facilities and recycling infrastructure. As consumer demand for premium products continues to increase, the Asia Pacific is expected to play an increasingly important role in the global glass container industry.

Competitive Landscape

The global glass bottles and containers market consists of several large multinational manufacturers along with numerous regional producers serving local markets. Leading companies operate integrated manufacturing networks that include furnace operations, forming lines, decoration facilities, and logistics infrastructure. Market concentration is moderate, with a few global companies controlling significant production capacity while smaller manufacturers serve niche markets. Competitive advantage often depends on technological innovation, production efficiency, and the ability to offer customized packaging solutions.

Leading manufacturers are focusing on technological innovation, sustainability initiatives, and geographic expansion. Investments in lightweight glass production, higher recycled content, and energy-efficient furnaces are improving operational efficiency. Companies are also expanding decoration services and forming strategic partnerships with beverage and pharmaceutical firms to secure long-term supply agreements.

Key Industry Developments

- In February 2026, Ardagh Group announced the launch of two new American-made 8-oz ring-neck glass bottles for the U.S. food market, designed for applications such as sauces, dressings, and marinades. The bottles are manufactured using flint glass and are fully recyclable, expanding the company’s food-packaging portfolio while supporting demand for premium and sustainable glass containers.

- In August 2025, Verallia launched “Vista,” a packaging solution made from 100% post-consumer recycled glass, enabling beverage brands to adopt fully recycled glass bottles and strengthen their sustainability positioning in premium spirits and beverage markets.

Companies Covered in Glass Bottles and Containers Market

- Ardagh Group

- O-I Glass

- Verallia

- Vidrala

- Vetropack Holding

- BA Glass Group

- Gerresheimer

- Stoelzle Glass Group

- Heinz-Glas

- SGD Pharma

- AGI Greenpac

- Piramal Glass

- Saverglass Group

- Zignago Vetro

- Wiegand-Glas

- Şişecam

- Hindusthan National Glass & Industries

- Beatson Clark

Frequently Asked Questions

The global glass bottles and containers market size is estimated to be US$64.7 billion in 2026.

The glass bottles and containers market is projected to reach US$88.6 billion by 2033.

Key market trends include increasing adoption of recyclable and sustainable packaging, growing premium beverage packaging demand, rising pharmaceutical glass vial consumption, and technological advancements in lightweight glass manufacturing and high recycled-content production.

The bottles segment is the leading product category, anticipated to account for approximately 59.3% of market revenue, largely driven by extensive use in alcoholic beverages, soft drinks, bottled water, and food packaging applications.

The glass bottles and containers market is expected to grow at a CAGR of 4.6% between 2026 and 2033.

Some of the major companies include Ardagh Group, O‑I Glass, Verallia, Vidrala, and Piramal Glass.