- Smart Packaging

- Reclosable Zipper Packaging Market

Reclosable Zipper Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Reclosable Zipper Packaging Market by Material Type (Polyethylene (PE, Bioplastics; Polypropylene (PP), Polyethylene Terephthalate (PET), Polyamide (PA/Nylon), Others), Zipper Type (Press-to-Close Zipper, Slider Zipper, Double Track Zipper, Child-Resistant Zipper, Tamper-Evident Zipper, Specialty Zipper), Packaging Format, Distribution Channel, End-User, and Regional Analysis, 2026 - 2033

Reclosable Zipper Packaging Market Size and Trend Analysis

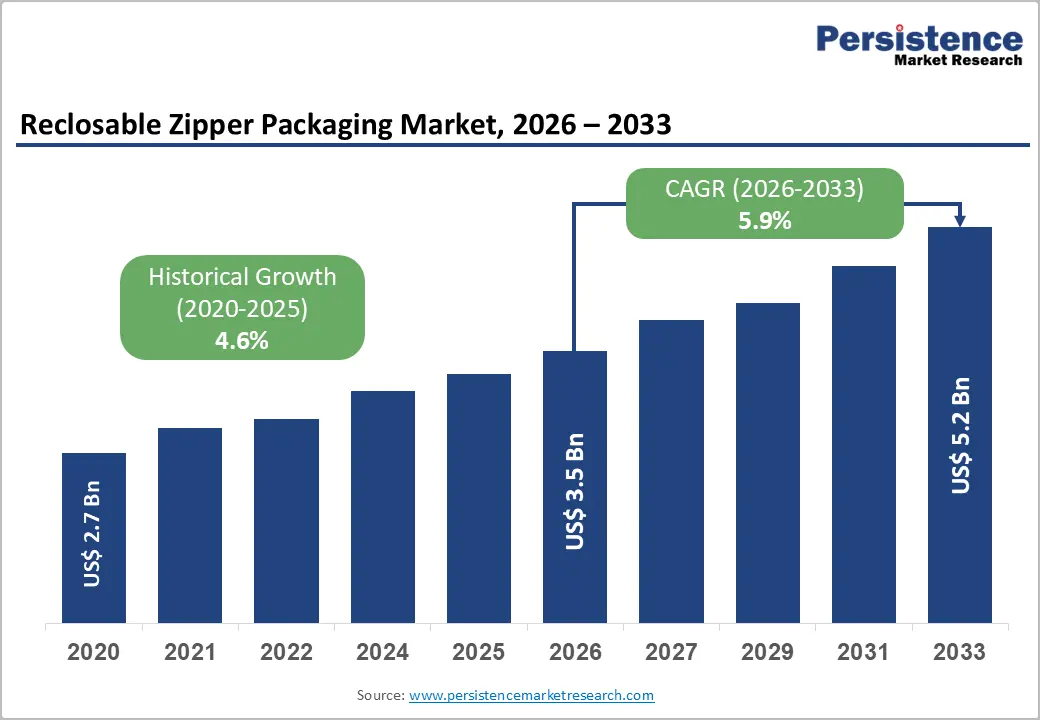

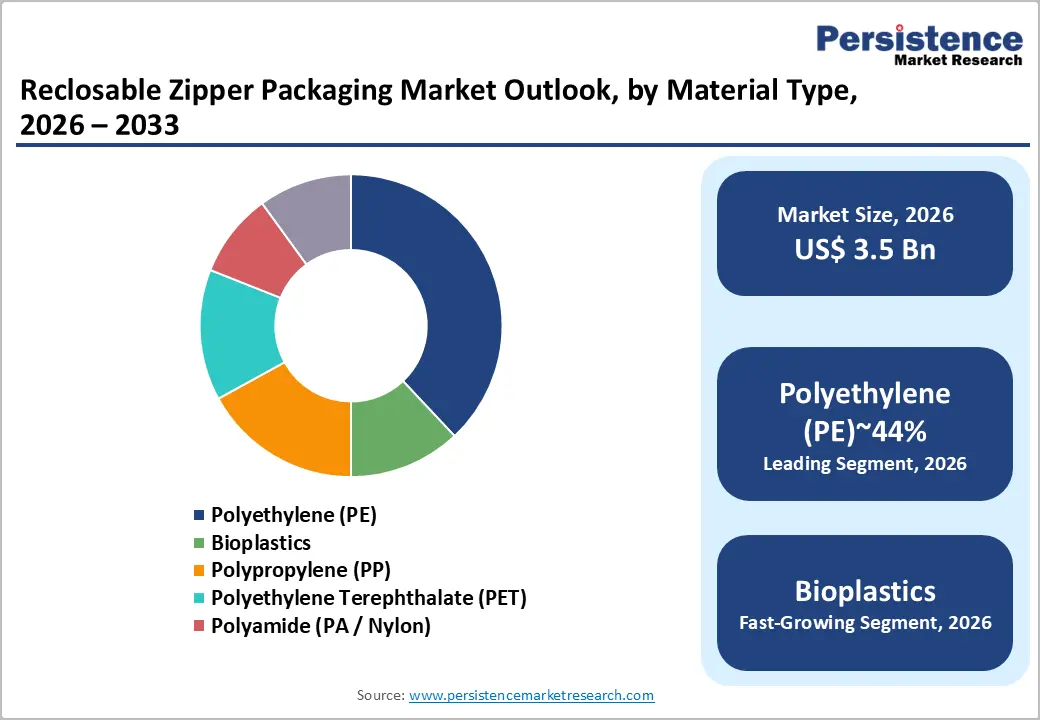

The global reclosable zipper packaging market size is likely to be valued at US$ 3.5 Billion in 2026 and is expected to reach US$ 5.2 Billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Robust demand from the food processing and retail sectors, rapid e-commerce expansion, and growing consumer preference for convenience-oriented, resealable packaging are the principal catalysts propelling market growth.

Key Industry Highlights:

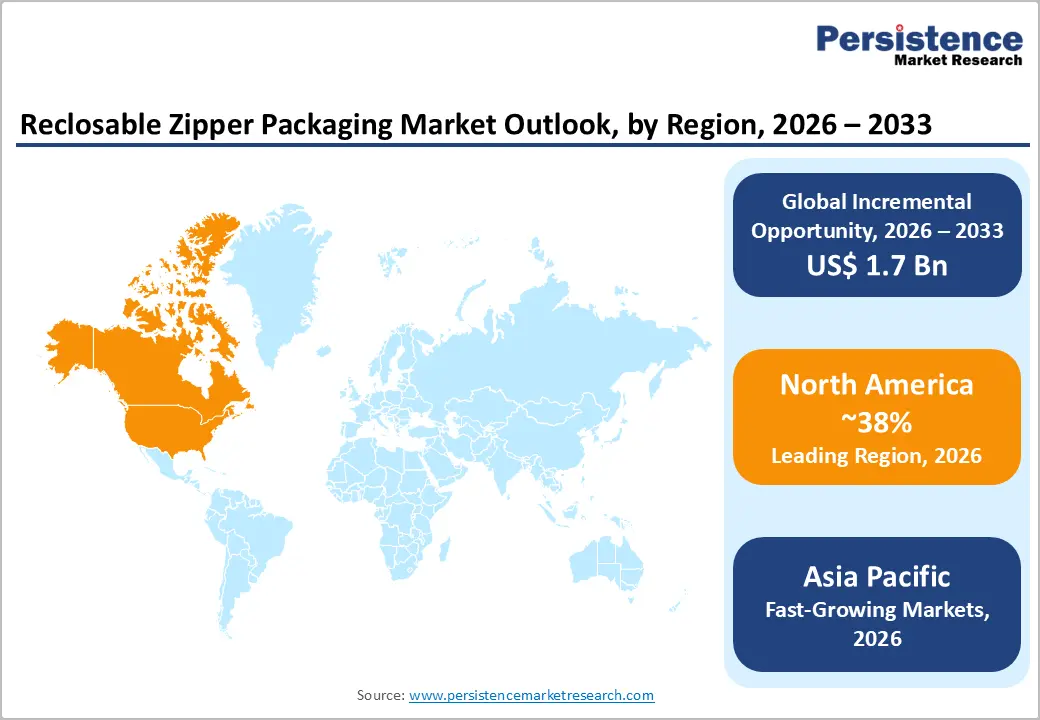

- Leading Region: North America leads the global reclosable zipper packaging market holding 38% share, driven by the U.S.'s mature food processing industry, robust e-commerce infrastructure, and stringent FDA and CPSC regulatory frameworks demanding premium zipper closure compliance across food and pharmaceutical packaging.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR of 6.8%, propelled by China's booming packaged food sector, India's organized retail expansion, and ASEAN's rising consumer goods consumption, collectively creating robust, above-average demand for reclosable zipper pouch formats through 2033.

- Dominant Segment: The Food Processing end-user segment dominates with approximately 46% market share, as virtually all packaged food categories, snacks, cheese, frozen foods, meat, pet food benefit structurally from reclosable zipper formats that extend shelf-life and reduce food waste.

- Fastest Growing Segment: Bioplastics-based reclosable zipper packaging is the fastest growing material sub-segment, driven by brand owner sustainability commitments, EU packaging regulations mandating recyclability by 2030, and rapidly expanding bioplastics production capacity from PLA and PHA resin producers.

- Key Market Opportunity: Child-resistant and tamper-evident zipper formats for the pharmaceutical and nutraceutical sector represent the highest-value opportunity, with PPPA and EU regulations mandating compliant packaging across a growing OTC and prescription drug product base.

| Key Insights | Details |

|---|---|

| Reclosable Zipper Packaging Market Size (2026E) | US$ 3.5 Billion |

| Market Value Forecast (2033F) | US$ 5.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 4.6% CAGR |

DRO Analysis

Drivers - Rising Consumer Demand for Convenient, Resealable Packaging Solutions to Reduce Food Waste and Extend Shelf Life Globally

Changing consumer lifestyles, including smaller household sizes, busy routines, and increasing awareness of food waste, are significantly driving demand for reclosable zipper packaging in the food processing and retail sectors. According to the United Nations Environment Programme (UNEP), nearly one-third of global food production, about 1.3 billion tonnes annually, is wasted, prompting both consumers and retailers to prioritize packaging solutions that extend product freshness.

Reclosable zipper packaging effectively addresses this issue by allowing multiple openings while maintaining product integrity, thereby reducing food waste and improving user convenience. Food manufacturers are increasingly adopting zipper closures across product categories such as snacks, cheese, frozen foods, meat, and pet food. This shift is strengthening long-term demand for zipper-based flexible packaging and encouraging OEMs to integrate such solutions into mainstream packaging strategies across global markets.

Rapid Expansion of Global E-Commerce Driving Demand for Durable, Resealable Packaging Across Multiple End-user Industries

The rapid expansion of the global e-commerce sector is creating strong growth opportunities for reclosable zipper packaging, particularly across consumer goods, food, and pharmaceutical industries. The United Nations Conference on Trade and Development (UNCTAD) reported that global e-commerce sales surpassed US$ 26 trillion in 2022 and have continued to grow steadily. E-commerce logistics require packaging that can withstand multiple handling stages, ensure product safety during transit, and offer easy resealing for consumers, requirements that zipper pouches effectively meet. The rise of direct-to-consumer (DTC) models, including online grocery platforms, meal-kit services, and subscription boxes, is further driving demand for premium resealable packaging formats. Stand-up pouches with zipper and slider closures are gaining popularity due to their durability, convenience, and enhanced user experience, creating a strong incremental demand channel for manufacturers in this market.

Restraints - Stringent Environmental Regulations and Plastic Waste Concerns Limiting Growth of Conventional Polyethylene-Based Zipper Packaging Solutions

Environmental concerns and increasing regulations on single-use plastics are posing significant challenges to the growth of conventional reclosable zipper packaging. Most zipper packaging solutions are made from polyethylene (PE) and polypropylene (PP), which are under strict regulatory scrutiny worldwide. Policies such as the European Union’s Single-Use Plastics Directive and packaging waste regulations are forcing manufacturers to rethink material choices and adopt sustainable alternatives.

Multi-layer plastic laminates commonly used in zipper packaging are difficult to recycle, making compliance with extended producer responsibility (EPR) regulations more complex and costly. As governments push for circular economy practices, packaging converters and brand owners must invest in redesigning products to meet recyclability standards. These compliance requirements increase operational costs and slow down adoption in highly regulated markets, thereby limiting overall market expansion.

High Manufacturing Complexity and Costs Restricting Adoption of Advanced Zipper Formats Among Small and Mid-Sized Converters

The production of advanced zipper formats, such as child-resistant, tamper-evident, and slider closures involves higher complexity compared to standard press-to-close zippers. These specialized formats require advanced converting equipment, precision tooling, and strict manufacturing standards, leading to higher capital investment and operational costs. As a result, small and mid-sized packaging converters often face entry barriers when attempting to compete in premium product segments.

Industry estimates suggest that child-resistant zipper pouches can cost around 30% more than standard zipper formats, making them less attractive for cost-sensitive applications. This cost difference is particularly impactful in emerging markets, where price competitiveness plays a critical role in purchasing decisions. Consequently, the high cost of production and limited affordability for certain end users restrict the widespread adoption of advanced zipper packaging solutions.

Opportunities - Growing Adoption of Bioplastics Enabling Sustainable Reclosable Zipper Packaging Solutions Aligned with Global Brand Sustainability Commitments

The growing focus on sustainable packaging solutions presents a major opportunity for reclosable zipper packaging manufacturers. Increasing environmental awareness and regulatory pressure are driving the adoption of bioplastics such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA). According to the European Bioplastics Association, global bioplastics production capacity is expected to grow from approximately 2.18 million tonnes in 2023 to over 7.43 million tonnes by 2028. This growth supports the development of eco-friendly zipper packaging solutions.

Leading consumer goods companies, including Nestlé, Unilever, and Procter & Gamble, have announced ambitious sustainability goals, encouraging the use of recyclable, compostable, or bio-based packaging materials. As a result, packaging converters investing early in bioplastic-based zipper technologies can gain a competitive advantage and capture emerging demand from sustainability-focused brands across global markets.

Expanding Pharmaceutical Sector Driving Demand for Child-resistant and Tamper-Evident Reclosable Zipper Packaging Solutions Globally

The pharmaceutical and nutraceutical industries are emerging as high-growth segments for reclosable zipper packaging, particularly for child-resistant and tamper-evident formats. Regulatory frameworks such as the Poison Prevention Packaging Act (PPPA) in the United States require child-resistant packaging for many medications and over-the-counter products, with similar regulations in Europe and the United Kingdom.

The steady expansion of the global OTC pharmaceutical market is increasing the demand for compliant packaging solutions. Flexible reclosable pouches with integrated zipper closures offer several advantages, including cost efficiency, portability, and improved shelf appeal compared to traditional rigid packaging. These formats are especially suitable for unit-dose packaging, nutraceutical products, and secondary packaging for medical devices. As regulatory requirements become stricter, the demand for advanced zipper solutions in the pharmaceutical sector is expected to grow significantly.

Category-wise Analysis

By Material Type Insights

Polyethylene (PE) is the leading material in the reclosable zipper packaging market, contributing around 44% of total material revenue. Its dominance is driven by easy processing, strong sealing performance, good moisture barrier properties, and cost-effectiveness compared to other polymers and bioplastics. Within this segment, Low-Density Polyethylene (LDPE) is the most widely used due to its high flexibility and excellent heat-sealing capability, making it ideal for food, retail, and household zipper pouch applications.

The strong global supply chain, supported by major producers such as LyondellBasell, Dow Inc., and SABIC, ensures reliable availability and stable pricing. At the same time, bioplastics are emerging as the fastest-growing sub-segment, as sustainability commitments from global consumer brands continue to rise. Increasing regulatory pressure and consumer demand for eco-friendly packaging are expected to further accelerate the adoption of biodegradable and renewable material alternatives.

By Zipper Type Insights

The Press-to-Close zipper segment leads the market, accounting for approximately 41% of total revenue. These zippers, also known as interlocking or profile zippers, are widely preferred due to their low cost and high production efficiency, making them suitable for mass-market applications. Their simple design allows easy opening and closing with minimal effort, enhancing consumer convenience across food, retail, and household products.

Their compatibility with standard flexible film laminates and low manufacturing complexity make them the default choice for products such as snack pouches, frozen food bags, and storage packaging. Companies like Zip-Pak, a division of Illinois Tool Works (ITW), continue to innovate in this segment by improving seal strength, durability, and user experience. As demand for cost-effective yet functional packaging solutions grows, press-to-close zippers are expected to maintain strong market adoption across both developed and emerging markets.

By Packaging Format Insights

Stand-up pouches dominate the packaging format segment, contributing nearly 38% of total market revenue. Their popularity is driven by strong shelf appeal, efficient material usage, and high consumer convenience, especially when combined with zipper closures. These pouches provide excellent product visibility and branding opportunities, making them highly attractive for food, pet care, and personal care applications.

According to the Flexible Packaging Association (FPA), stand-up pouches require significantly less material compared to rigid packaging formats, while also reducing transportation costs and carbon emissions. This aligns well with the sustainability goals of brand owners and retailers. Moreover, the growing demand for premium and high-barrier packaging solutions for products like coffee, snacks, and organic foods is further driving segment growth. As consumer preferences shift toward convenience and sustainability, stand-up pouches are expected to remain the preferred packaging format in the coming years.

By Distribution Channel Insights

Direct sales remain the dominant distribution channel in the reclosable zipper packaging market, accounting for approximately 52% of total revenue. Large food processors, pharmaceutical companies, and retail chains prefer sourcing packaging directly from manufacturers through long-term agreements. This approach enables them to access customized solutions, better pricing, and technical support for product development. Direct relationships also facilitate faster communication and improved supply chain efficiency.

Leading companies such as Amcor plc, Mondi, and ProAmpac have established dedicated key account teams to serve large global clients. Meanwhile, online sales channels are emerging as the fastest-growing segment, driven by small and medium-sized enterprises (SMEs) seeking flexible order quantities and customized packaging solutions. Digital procurement platforms are making it easier for smaller brands to access advanced zipper packaging, thereby expanding market reach and increasing competition among suppliers.

By End-user Insights

The food processing industry is the largest end-user segment, contributing around 46% of total market demand. This segment includes a wide range of products such as meat, seafood, dairy, snacks, baked goods, dry foods, pet food, and confectionery. Reclosable zipper packaging plays a critical role in preserving product freshness, maintaining quality, and preventing contamination after opening.

The ability to reseal packaging enhances convenience for consumers and reduces food wastage. The Food and Agriculture Organization (FAO) highlights the importance of effective packaging in minimizing post-harvest losses across global supply chains. Additionally, the growing demand for processed and packaged food, especially in emerging economies, is further driving segment growth. As consumer lifestyles become more fast-paced and convenience-oriented, the adoption of reclosable packaging solutions in the food processing sector is expected to remain strong in the future.

Regional Insights

North America Reclosable Zipper Packaging Market Trends

North America is a leading regional market for reclosable zipper packaging, with the United States driving significant demand. The region benefits from a well-developed food processing industry, a strong e-commerce sector, and high consumer awareness of convenient packaging formats. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the Consumer Product Safety Commission (CPSC) enforce strict packaging standards, particularly for safety and child-resistant features, encouraging the adoption of advanced zipper solutions.

Sustainability initiatives such as the Inflation Reduction Act and commitments under the U.S. Plastics Pact are driving investments in recyclable and bio-based packaging materials. Key market players, including Presto Products Company, Zip-Pak, and ProAmpac, are actively developing innovative and eco-friendly packaging solutions. These factors collectively position North America as a key innovation hub for high-performance and sustainable reclosable zipper packaging technologies.

Europe Reclosable Zipper Packaging Market Trends

Europe is recognized as the most regulation-driven market for reclosable zipper packaging, supported by strong environmental policies and sustainability goals. The European Union’s Packaging and Packaging Waste Regulation (PPWR), along with the European Green Deal and Circular Economy Action Plan, is pushing manufacturers toward recyclable and reusable packaging solutions. Germany leads the regional market due to its advanced packaging industry, while France and Spain show strong demand for premium zipper pouches in food and personal care applications.

The United Kingdom’s Plastic Packaging Tax is also encouraging the use of recycled materials in packaging production. As a result, converters are increasingly adopting mono-material polyethylene and polypropylene structures to meet regulatory requirements. Companies such as Mondi and Huhtamaki are leading innovation in recyclable and high-barrier packaging formats. These developments are shaping Europe as a global leader in sustainable packaging transformation.

Asia Pacific Reclosable Zipper Packaging Market Trends

Asia Pacific is both the largest and fastest-growing market for reclosable zipper packaging, driven by strong manufacturing capabilities and rising consumer demand. China leads the region with its extensive food processing industry and large-scale production capacity, while Japan contributes through advanced engineering in zipper closure technologies. India is experiencing rapid growth due to expanding organized retail and increasing consumption of packaged foods.

Regulatory bodies such as the Food Safety and Standards Authority of India (FSSAI) are strengthening packaging standards, encouraging the adoption of safer and more advanced packaging formats. Additionally, ASEAN countries, including Vietnam, Thailand, and Indonesia, are witnessing increased demand for affordable and convenient packaging solutions. The region’s cost advantages and large production base make it a key global supplier of zipper packaging products. This combination of demand growth and manufacturing strength continues to drive Asia Pacific’s market leadership.

Competitive Landscape

The global reclosable zipper packaging market is moderately fragmented, with a mix of large multinational companies and specialized suppliers competing across regions. Major players such as Amcor plc, Mondi, Huhtamaki, and ProAmpac dominate the market through their extensive product portfolios and global presence. At the same time, specialized companies like Zip-Pak and Presto Products Company focus on advanced zipper technologies and innovative closure solutions.

Companies are increasingly differentiating themselves through sustainability initiatives, including the development of recyclable and bio-based materials. Strategic partnerships with brand owners and investments in research and development are also key competitive strategies. In addition, mergers and acquisitions are being used to expand geographic reach and strengthen market position. The integration of high-speed packaging lines and customized solutions is further enhancing competitiveness in the market, ensuring continued innovation and growth.

Key Developments

- In March 2025: Amcor plc introduced the AmLite Ultra Recyclable range, a mono-material PE-based reclosable zipper pouch portfolio certified under RecyClass guidelines, designed to meet strict European sustainability regulations while maintaining high-barrier performance for food packaging applications.

- In October 2024: ProAmpac expanded its ProActive Sustainability portfolio with advanced high-barrier reclosable stand-up pouches containing up to 30% post-consumer recycled content, addressing growing demand for eco-friendly packaging in North America’s snack food and pet care segments.

- In June 2023: Mondi launched its BarrierPack Recyclable series at the Interpack 2023, featuring all-PE recyclable reclosable zipper solutions aimed at cheese and processed meat packaging, supporting circular economy goals and compliance with evolving European packaging regulations.

Companies Covered in Reclosable Zipper Packaging Market

- Amcor plc

- Huhtamaki

- Sonoco Products Company

- ProAmpac

- Mondi

- Glenroy, Inc.

- Presto Products Company

- Zip-Pak (Illinois Tool Works)

- CarePac

- SVP Packing Industry Pvt Ltd.

- Great American Packaging

- LPS Industries, LLC

- IMPAK Corporation

- Sealed Air Corporation

- Berry Global Group, Inc.

- Constantia Flexibles

- Coveris Holdings S.A.

Frequently Asked Questions

The global Reclosable Zipper Packaging Market is valued at US$ 3.5 Billion in 2026 and is projected to reach US$ 5.2 Billion by 2033, expanding at a CAGR of 5.9% over the forecast period.

The primary growth drivers include surging consumer demand for convenience and extended shelf-life in food packaging, supported by the UNEP's finding that 1.3 billion tonnes of food is wasted globally each year, and the rapid expansion of e-commerce, which demands flexible, resealable packaging that can withstand repeated handling during transit and last-mile delivery.

Stand-up Pouches are the leading packaging format segment, holding approximately 38% of format revenue, owing to their superior retail shelf presence, material efficiency, and seamless integration with zipper closure systems across food, pet care, and personal care product applications.

North America is the leading regional market, anchored by the United States' large and sophisticated food processing industry, expansive e-commerce infrastructure, and stringent FDA and CPSC compliance requirements that drive sustained adoption of premium zipper closure formats across multiple end-use sectors.

The most significant opportunity lies in child-resistant and tamper-evident zipper packaging for the pharmaceutical and nutraceutical sector. Regulatory mandates under the U.S. Poison Prevention Packaging Act (PPPA) and equivalent EU frameworks, combined with expanding OTC drug and nutraceutical markets, are driving structural demand for compliant, flexible zipper pouch alternatives to rigid containers.

Leading companies in the Reclosable Zipper Packaging Market include Amcor plc, Mondi, ProAmpac, Huhtamaki, Sonoco Products Company, Zip-Pak, Presto Products Company, Berry Global Group, Inc., Sealed Air Corporation, Constantia Flexibles, and IMPAK Corporation, among others.