- Smart Packaging

- Tethered Caps Market

Tethered Caps Market Size, Share, and Growth Forecast, 2026 - 2033

Tethered Caps Market by Material (Plastic, Metal, Others), Product Design (Screw Caps, Single Tether, Others), Application, and Regional Analysis for 2026 - 2033

Tethered Caps Market Size and Trends Analysis

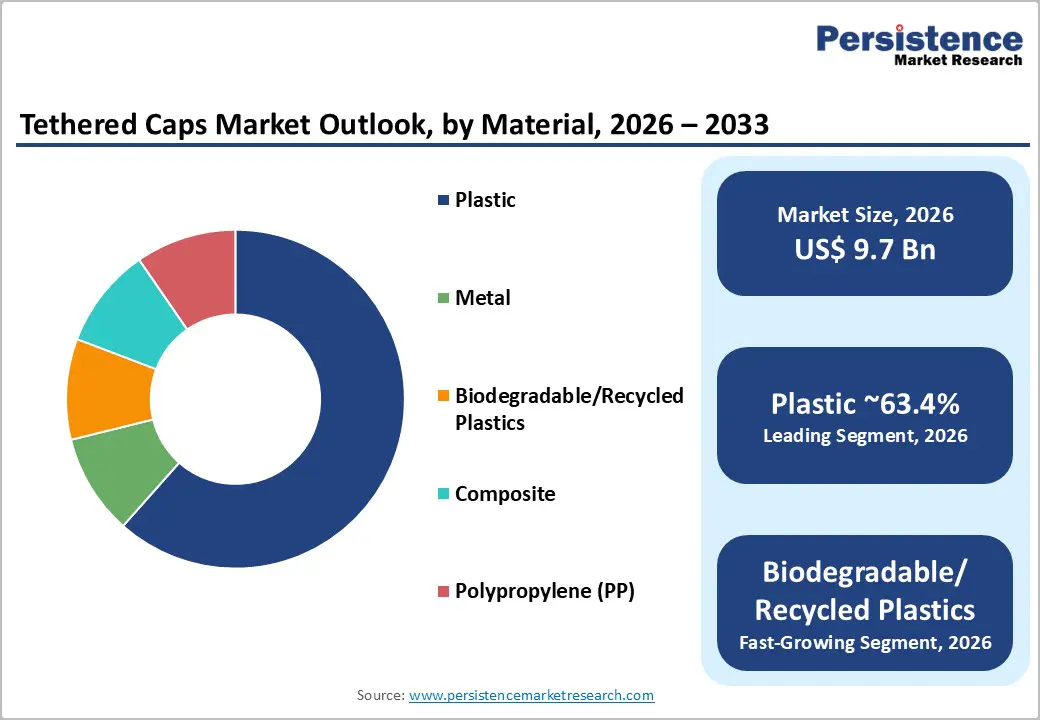

The global tethered caps market size is likely to be valued at US$9.7 billion in 2026 and is expected to reach US$15.8 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033, driven by the enforcement of mandatory tethered-cap regulations in Europe, alongside rising recycled-content requirements and broader packaging circularity objectives.

These factors are accelerating product redesign across the beverage and consumer goods sectors. The transition is structural in nature, generating sustained and recurring demand across the packaging value chain rather than a one-time adoption cycle.

Key Industry Highlights:

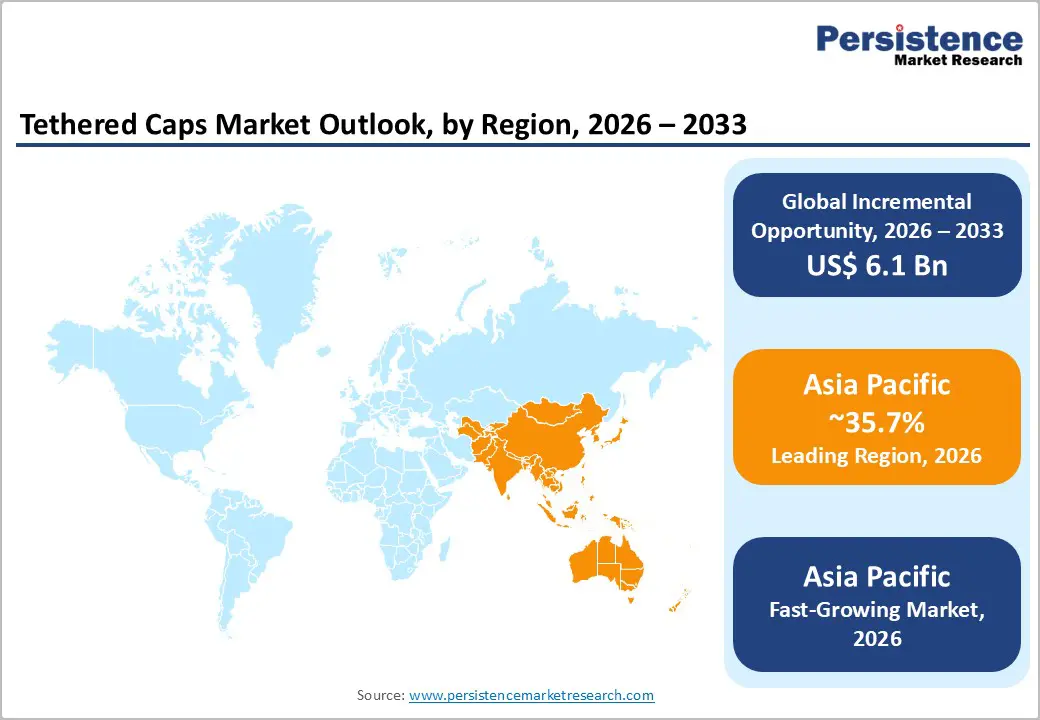

- Leading Region: Asia Pacific is projected to account for 35.7% of the market share, driven by strong manufacturing capabilities, rising packaged beverage consumption, and expanding industrial infrastructure across China, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid urbanization, increasing sustainability awareness, and growing investments in packaging and recycling ecosystems.

- Investment Plans: The market is witnessing significant investments in sustainable packaging and regional manufacturing expansion, with companies focusing on recyclable materials, lightweight designs, and new production facilities, particularly in Asia Pacific and Europe, to meet regulatory and demand requirements.

- Dominant Material: Plastic holds an anticipated 63.4% market share, due to its cost-effectiveness, lightweight properties, and compatibility with high-speed production and complex tethered designs.

- Leading Product Design: Screw caps lead with an anticipated 44.8% market share, driven by their widespread use in beverage packaging, ease of integration with tethered features, and compatibility with existing filling and sealing systems.

| Key Insights | Details |

|---|---|

| Tethered Caps Market Size (2026E) | US$9.7 Bn |

| Market Value Forecast (2033F) | US$15.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Regulatory Enforcement Driving Mandatory Adoption across Key Markets

Regulatory frameworks, particularly in Europe, are the most significant drivers of the tethered caps market. The requirement for beverage containers up to three liters to include attached caps from July 2024 has created a non-discretionary transition for manufacturers. This shift requires extensive redesign of closures, including cap geometry, hinge mechanisms, and sealing performance. The impact extends across the value chain, affecting beverage companies, packaging converters, and equipment manufacturers. As compliance deadlines are enforced, companies must upgrade production lines and tooling systems, leading to recurring capital expenditure and sustained demand for compliant closure systems.

Rising Circular Economy Initiatives and Recycling Targets

Global sustainability efforts are reinforcing the shift toward tethered caps. Current data indicate that only about 9% of plastic waste is recycled globally, highlighting inefficiencies in waste management systems. In more advanced markets, such as Europe, plastic packaging recycling rates have reached 40.7%, but policymakers are targeting higher recovery levels. Tethered caps support these objectives by ensuring that caps remain attached to bottles, improving collection rates and reducing litter. This alignment with circular economy principles is positioning tethered caps as a standardized solution for improving recyclability and meeting extended producer responsibility requirements.

Growth in Beverage Consumption Expanding Application Base

The steady increase in global beverage consumption, particularly bottled water, continues to expand the addressable market. In the U.S. alone, bottled water consumption reached 15.95 billion gallons in 2023, with per capita consumption at 47.1 gallons. This trend underscores the scale of demand for closures, as every packaged beverage requires a secure and user-friendly sealing solution. Tethered caps are increasingly integrated into traditional closure formats such as screw caps and sports caps, ensuring compatibility with existing packaging systems. The result is a large, recurring demand cycle driven by both consumption growth and regulatory compliance.

Restraint Analysis - High Conversion Costs and Operational Complexity

Transitioning to tethered caps involves significant capital investment and operational adjustments. Manufacturers must redesign molds, adjust torque specifications, and modify filling-line configurations to accommodate new closure systems. These changes can impact production efficiency, particularly during the initial transition phase. For small and mid-sized converters, the cost burden can delay adoption, especially in regions where regulatory enforcement is less stringent. This creates a temporary imbalance in adoption rates across markets, with cost sensitivity acting as a key limiting factor.

Uneven Recycling Infrastructure across Regions

Despite the sustainability advantages of tethered caps, their effectiveness depends on the presence of robust recycling systems. Many regions still lack adequate waste collection and processing infrastructure, limiting the practical benefits of attached closures. Significant investment is required to modernize recycling systems, particularly in developing markets. This creates a gap between regulatory intent and real-world implementation, where tethered caps may not achieve their full environmental impact. As a result, demand growth may remain uneven, with stronger adoption in regions that have advanced recycling ecosystems.

Opportunity Analysis - Adoption of Recycled-Content and Mono-Material Designs

The transition toward sustainable packaging presents a major opportunity for innovation in tethered caps. Manufacturers are increasingly focusing on post-consumer recycled (PCR) materials and mono-material designs to meet regulatory requirements and corporate sustainability targets. These solutions reduce reliance on virgin plastics while maintaining performance standards such as durability and food safety. Companies that can scale these innovations effectively are likely to gain a competitive advantage, particularly in markets with strict environmental regulations. This trend is expected to drive premiumization within the closure segment, as sustainability becomes a key differentiator.

Rapid Growth Potential in Asia Pacific

Asia Pacific represents the most significant growth opportunity, accounting for 35.7% of the global market and exhibiting the fastest growth rate. The region benefits from strong manufacturing capabilities, expanding beverage consumption, and increasing investments in packaging infrastructure. Countries such as China, India, and those in Southeast Asia are witnessing rapid urbanization and rising demand for packaged goods. Governments and industry players are beginning to align with global sustainability standards, creating a favorable environment for tethered cap adoption. This combination of volume growth and industrial expansion positions the region as a key driver of future market development.

Increasing Demand for Convenience-Driven Packaging Solutions

Consumer preferences are shifting toward packaging that offers ease of use, safety, and convenience. Tethered caps are evolving beyond regulatory compliance to incorporate features such as improved opening mechanisms, tamper evidence, and enhanced ergonomics. These features are particularly important in household and personal care products, where ease of handling and spill prevention are critical. As brands prioritize user experience alongside sustainability, tethered caps are becoming a value-added component of packaging design, opening new growth avenues beyond traditional beverage applications.

Category-wise Analysis

Material Insights

Plastic is expected to dominate the material segment, accounting for an anticipated 63.4% market share in 2026. Its leadership is driven by cost efficiency, lightweight properties, and compatibility with high-speed manufacturing processes. Plastic materials, particularly polypropylene (PP) and high-density polyethylene (HDPE), offer excellent moldability, chemical resistance, and durability, making them suitable for a wide range of applications, including beverages, food, and household products. The material also supports complex tethered designs, such as integrated hinges and tamper-evident bands, without compromising sealing integrity. For example, major beverage brands have widely adopted PP-based tethered closures to maintain production efficiency while complying with regulatory requirements. This combination of performance reliability and economic scalability ensures plastic remains the preferred choice for mass production.

Biodegradable and recycled plastics are likely to represent the fastest-growing segment. Growth is fueled by rising regulatory pressure and corporate sustainability commitments to reduce reliance on virgin plastics. These materials enable manufacturers to meet recycled-content mandates while maintaining functional performance in terms of strength, flexibility, and food safety compliance. For instance, several packaging companies are introducing closures made with post-consumer recycled (PCR) content to align with circular economy targets. Advances in polymer engineering are also improving the quality and consistency of recycled resins, making them more viable for high-volume applications. Although challenges such as higher costs, limited feedstock availability, and processing complexity persist, this segment is expected to gain momentum as supply chains strengthen and regulatory enforcement intensifies.

Product Design Insights

Screw caps are anticipated to lead the product design segment, holding an anticipated 44.8% market share in 2026. Their dominance is attributed to widespread use in beverage packaging, where they provide reliable sealing, leak prevention, and ease of use. Screw caps are highly compatible with various filling processes, including hot-fill, cold-fill, and aseptic systems, making them suitable for diverse liquid products such as bottled water, carbonated soft drinks, and dairy beverages. The integration of tethered features into traditional screw-cap designs allows manufacturers to comply with regulations without significantly altering existing production lines or consumer usage patterns. For example, many global beverage companies have transitioned to tethered screw caps while maintaining familiar opening and closing mechanisms. This ensures operational continuity and consumer acceptance, reinforcing their leading position.

Double-tether caps are likely to be the fastest-growing design segment. These designs provide enhanced functionality by ensuring that caps remain securely attached to the container while reducing interference during drinking or pouring. Improved hinge technology, flexible connectors, and ergonomic positioning allow the cap to stay away from the user’s face, enhancing convenience and safety. For instance, premium bottled water and sports drink brands are increasingly adopting double tether designs to improve user experience and differentiate their products. These closures also support stronger tamper-evident features and better recyclability by keeping all components attached. As manufacturers prioritize innovation and user-centric design, double tether caps are emerging as a next-generation solution that effectively balances regulatory compliance, usability, and sustainability objectives.

Regional Insights

North America Tethered Caps Market Trends - Sustainability-Led Innovation without Regulatory Mandates

North America is a mature market characterized by high consumption of packaged beverages and strong demand for innovative packaging solutions. The U.S. plays a central role, supported by a large beverage industry and an increasing focus on sustainability. While tethered caps are not yet mandated at a federal level, leading global packaging companies such as Amcor plc and Berry Global have proactively introduced compliant closure solutions to align with global regulatory trends, particularly those originating in Europe. The 2025 combination of these two companies has strengthened product development capabilities in closures, enabling faster rollout of tethered-cap technologies across North American operations.

Investments in recycling infrastructure and circular packaging initiatives are also shaping the market. Companies like Sonoco Products Company and Silgan Holdings are expanding sustainable packaging portfolios, including closure systems designed for improved recyclability. At the brand level, major beverage companies are gradually introducing tethered closures in select product lines to ensure global consistency and future regulatory readiness. As a result, market growth in North America is driven more by product upgrades, sustainability alignment, and premiumization, rather than large-scale regulatory-driven adoption seen in Europe.

Europe Tethered Caps Market Trends - Mandatory Adoption Driven by EU Packaging Regulations

Europe is the most advanced region in terms of regulatory implementation and market adoption, driven by strict environmental policies. The enforcement of tethered-cap requirements under the EU framework has accelerated a rapid and mandatory transition across the packaging industry. This has created a standardized shift toward tethered closures across beverage categories, including bottled water, soft drinks, and dairy packaging. Countries such as Germany, the U.K., France, and Spain are leading in adoption and innovation, supported by strong recycling infrastructure and policy alignment. Major industry players such as BERICAP Holding GmbH and Guala Closures have introduced a wide range of tethered-cap solutions tailored for different applications, including lightweight and mono-material designs. At the same time, carton packaging leader Tetra Pak has rolled out tethered caps across its beverage carton portfolio in Europe, setting a benchmark for large-scale implementation.

Brand-level adoption has also been significant. European bottled water and soft drink producers have rapidly transitioned to tethered caps to remain compliant, often redesigning packaging lines within short timelines. These developments have made Europe a benchmark market for innovation, standardization, and large-scale deployment, influencing packaging strategies globally.

Asia Pacific Tethered Caps Market Trends - High-Growth Market Powered by Manufacturing Scale and Rising Demand

Asia Pacific is the largest and fastest-growing regional market, accounting for 35.7% of market share in 2026, and is expected to remain the primary growth engine. Rapid industrialization, urbanization, and rising demand for packaged goods are driving market expansion. The region’s strong manufacturing base supports large-scale production, making it a key hub for both domestic consumption and export-oriented packaging solutions.

Significant investments by global packaging companies are accelerating market development. For example, ALPLA Werke Alwin Lehner GmbH & Co KG expanded its footprint in Southeast Asia with a new facility in Thailand that includes caps and closures production, strengthening regional supply capabilities. Similarly, Tetra Pak has been actively promoting recycling initiatives and sustainable packaging solutions in India, aligning product design with emerging circular economy frameworks. Local and regional beverage brands across China, India, and ASEAN countries are increasingly adopting advanced closure systems to enhance product quality and meet evolving consumer expectations. At the same time, governments in the region are gradually introducing stricter environmental regulations, encouraging the adoption of recyclable and compliant packaging formats. These combined factors, manufacturing scale, rising consumption, and growing regulatory alignment, position Asia Pacific as the most dynamic and opportunity-rich market for tethered caps.

Competitive Landscape

The global tethered caps market is moderately fragmented, with a mix of global leaders and regional players. Large multinational companies dominate innovation and large-scale production, while smaller firms cater to localized demand. Competitive advantage is driven by technological capabilities, regulatory compliance, and the ability to deliver cost-effective solutions. Market consolidation is gradually increasing as leading players expand their global presence.

Key players are focusing on product innovation, sustainability integration, and geographic expansion. Strategic priorities include developing recyclable materials, improving user experience, and enhancing production efficiency. Collaboration with beverage and consumer goods companies is becoming increasingly important to align product development with market needs.

Key Industry Developments:

- In March 2026, Amcor plc partnered with Vöslauer Mineralwasser to supply a customized tethered cap solution for its bottled water range, designed with a wide-angle opening and improved ergonomics to enhance consumer convenience while complying with EU regulations.

- In January 2026, Amcor plc collaborated with Spadel to launch a lightweight, recyclable tethered cap for the Wattwiller mineral water brand, focusing on material reduction, improved grip, and accessibility for consumers with limited dexterity.

Companies Covered in Tethered Caps Market

- Amcor plc

- AptarGroup, Inc.

- ALPLA Werke Alwin Lehner GmbH & Co. KG

- BERICAP Holding GmbH

- Silgan Holdings Inc.

- Guala Closures S.p.A.

- Crown Holdings, Inc.

- Sonoco Products Company

- Tetra Pak

- Elopak ASA

- Closure Systems International, Inc.

- Berry Global, Inc.

- Mold-Tek Packaging Ltd.

- Pact Group Holdings Ltd.

- United Caps Luxembourg S.A.

- Caprite Australia Pty Ltd.

Frequently Asked Questions

The tethered caps market is estimated to be valued at US$9.7 billion in 2026.

The tethered caps market is expected to reach US$15.8 billion by 2033.

Key trends include regulatory-driven adoption (especially in Europe), increasing use of recycled and mono-material plastics, innovation in ergonomic and user-friendly cap designs, and growing demand for sustainable and recyclable packaging solutions.

The plastic material segment leads the market with an anticipated 63.4% share, while screw caps dominate product design with around 44.8% share, primarily due to their widespread use in beverage packaging.

The tethered caps market is projected to grow at a CAGR of 7.2% from 2026 to 2033.

Some of the major players include Amcor plc, AptarGroup, Inc., BERICAP Holding GmbH, Silgan Holdings Inc., and ALPLA Werke Alwin Lehner GmbH & Co KG.