- Smart Packaging

- Gable Top Liquid Cartons Market

Gable Top Liquid Cartons Market Size, Share, and Growth Forecast, 2026 - 2033

Gable Top Liquid Cartons Market by Capacity (250-500 ml, 500-750 ml, Others), Application (Food & Beverages, Juices, Others), Closure Type, Material Type, and Regional Analysis for 2026 - 2033

Gable Top Liquid Cartons Market Size and Trends Analysis

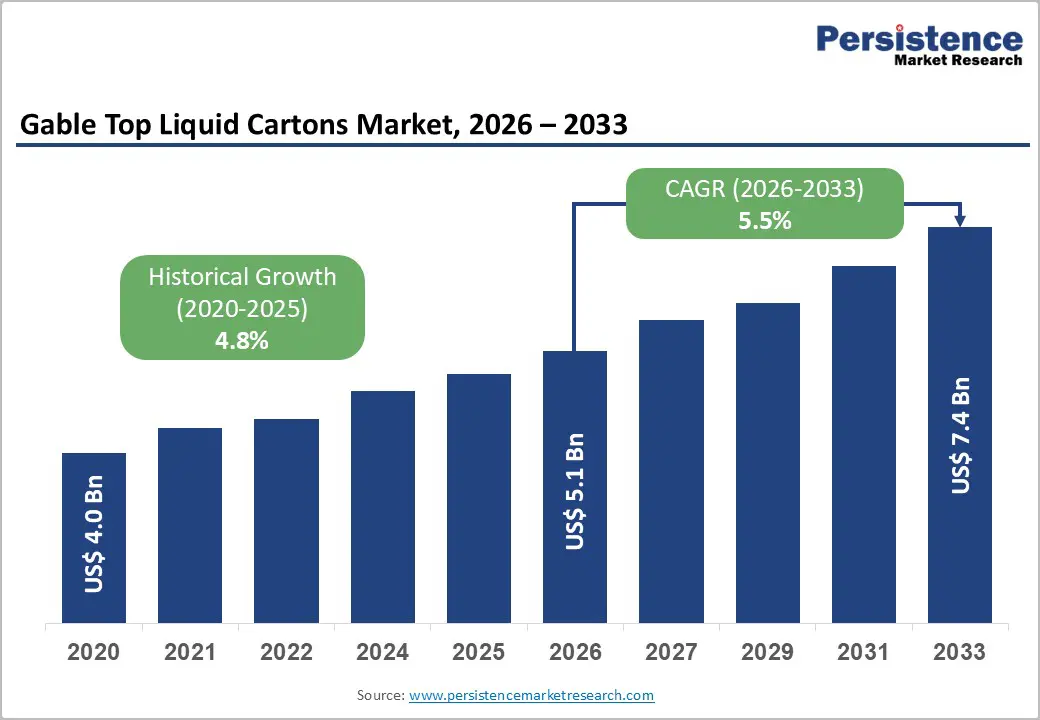

The global gable top liquid cartons market size is likely to be valued at US$5.1 billion in 2026 and is expected to reach US$7.4 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by steady demand for dairy packaging, rising adoption of shelf-stable and convenience-oriented beverages, and tightening packaging sustainability regulations worldwide.

Ongoing innovation in closure systems, fiber-based materials, and recycling infrastructure is strengthening product functionality and environmental performance. As a result, purchasing decisions increasingly balance packaging efficiency with sustainability outcomes, shaping long-term market evolution.

Key Industry Highlights:

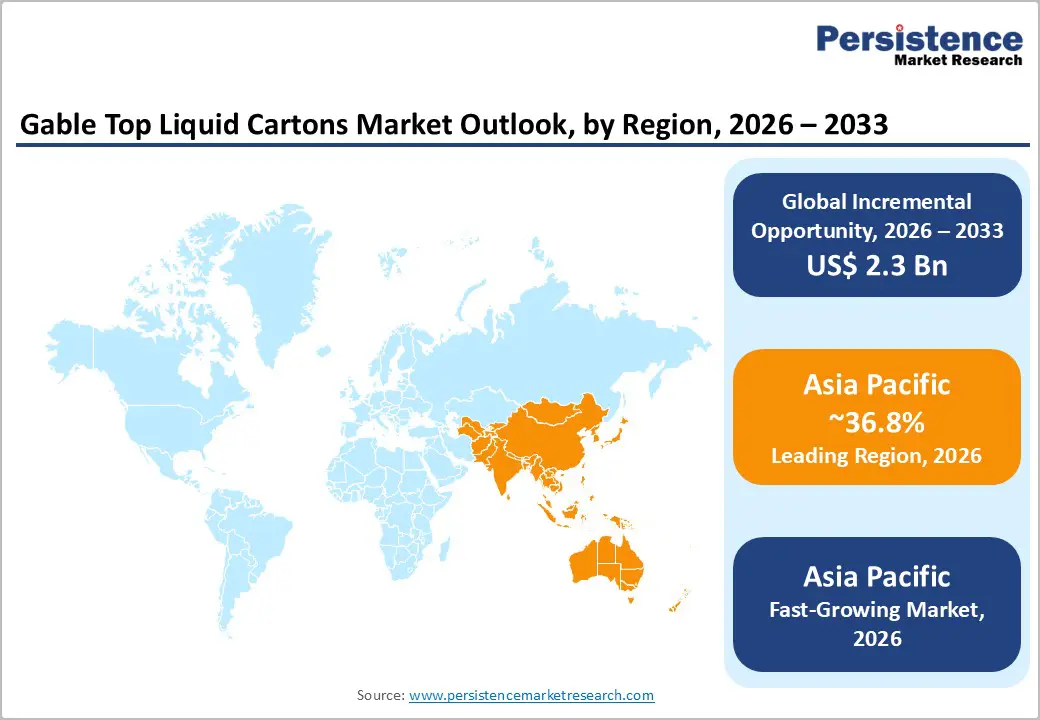

- Leading Region: Asia Pacific is projected to account for 36.8% of the market share, driven by strong dairy production, expanding beverage consumption, and increasing packaging infrastructure investments.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid urbanization, rising disposable incomes, and increasing adoption of packaged dairy and RTD beverages across China, India, and Southeast Asia.

- Investment Plans: The market is witnessing increased investments in localized manufacturing, recycling infrastructure, and sustainable material innovation, with companies expanding production capacities and focusing on low-carbon, fiber-based packaging solutions.

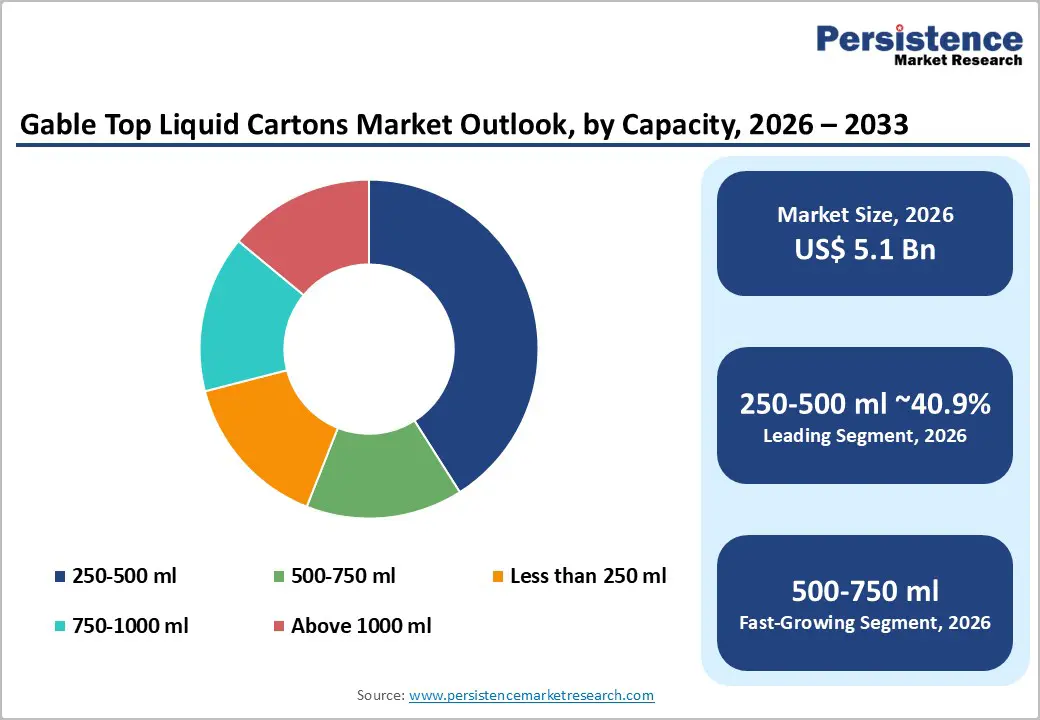

- Dominant Capacity: The 250-500 ml capacity segment is anticipated to dominate the market, holding 40.9% of market share, due to its widespread use in single-serve dairy and beverage applications.

- Leading Application: The food & beverages segment is estimated to lead with a 44.7% market share, primarily driven by strong demand for milk, fresh dairy products, and liquid food packaging.

| Key Insights | Details |

|---|---|

| Gable Top Liquid Cartons Market Size (2026E) | US$5.1 Bn |

| Market Value Forecast (2033F) | US$7.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

DRO Analysis

Driver Analysis - Expansion in Global Dairy Production and Aseptic Packaging Demand

Global dairy production continues to expand significantly, supporting consistent demand for liquid packaging solutions. Milk production has increased substantially over the past three decades, with Asia emerging as the primary growth region and India accounting for a major share of global output. This growth drives demand for packaging formats that ensure product safety, extended shelf life, and efficient distribution. Aseptic processing technologies further enhance the value proposition of gable top cartons by enabling storage without refrigeration. As dairy consumption diversifies into flavored milk, cream, and fortified beverages, cartons remain a preferred solution due to their ability to maintain product integrity and reduce spoilage.

Regulatory Push toward Sustainable and Recyclable Packaging

Global regulatory frameworks are increasingly targeting packaging waste reduction and circular economy implementation. Policies focused on recyclability, material reduction, and carbon footprint minimization are accelerating the adoption of fiber-based packaging formats. Gable top cartons, which are primarily paper-based, align well with these regulatory expectations. Investments in recycling infrastructure and material innovation are strengthening the sustainability profile of cartons. This regulatory environment is encouraging manufacturers to transition away from plastic-intensive formats, positioning gable top cartons as a compliant and future-ready packaging solution.

Rising Consumer Preference for Convenience and Premium Packaging

Changing consumer lifestyles are driving demand for packaging that offers portability, resealability, and ease of use. The growth of RTD beverages, functional drinks, and premium dairy products is expanding the application scope of gable top cartons. Closure innovations such as screw caps and flip caps enhance usability, making cartons suitable for both single-serve and multi-use formats. Premiumization trends are also influencing packaging design, with brands focusing on aesthetics, ergonomic features, and sustainability messaging. This shift is increasing the value contribution of packaging in product differentiation and brand positioning.

Restraint Analysis - Higher Production and Conversion Costs Compared to Alternative Packaging

Gable top cartons require specialized materials, barrier coatings, and compatible filling equipment, resulting in higher production and conversion costs compared to plastic bottles or flexible packaging. The need for integrated systems, including machinery, materials, and technical support, creates entry barriers for smaller manufacturers. These cost considerations can limit adoption in price-sensitive markets and low-margin product categories, where alternative packaging formats offer lower upfront investment and operational simplicity.

Dependence on Recycling Infrastructure and Regional Capabilities

Although gable top cartons are recyclable, their actual recycling performance depends heavily on local collection, sorting, and processing infrastructure. In regions with underdeveloped waste management systems, cartons may not be effectively recovered, reducing their environmental advantage. This creates a gap between sustainability claims and real-world outcomes. For manufacturers and brands, this limitation introduces compliance risks and reputational challenges, particularly in markets with evolving environmental regulations.

Opportunity Analysis - Strong Growth Potential in Asia Pacific Markets

Asia Pacific represents the most significant growth opportunity, supported by rapid urbanization, rising disposable incomes, and expanding dairy and beverage industries. The region’s leadership position, with a 36.8% market share, reflects its strong production base and consumption trends. Increasing investments in food processing, packaging infrastructure, and cold chain logistics are further accelerating demand. Local manufacturing capabilities and cost advantages enable scalable production, making the region highly attractive for capacity expansion and strategic partnerships.

Expansion into Non-Dairy Beverages and Plant-Based Segments

The application of gable top cartons is expanding beyond traditional dairy into juices, plant-based beverages, and ready-to-drink (RTD) products, reflecting a broader shift in consumer consumption patterns. These categories benefit from the cartons’ ability to provide extended shelf life, strong barrier protection, and premium shelf presentation, which are essential for maintaining product quality and brand appeal. The rising popularity of plant-based milk alternatives, cold-pressed juices, functional drinks, and fortified beverages is further accelerating this transition. Manufacturers are increasingly leveraging carton packaging to position these products as natural, sustainable, and high-quality offerings, particularly in urban and health-conscious consumer segments.

Development of Low-Carbon and Eco-Friendly Packaging Solutions

Sustainability-driven innovation is creating significant opportunities in low-carbon, fiber-rich, and plastic-reduced packaging formats. Advances in barrier technologies, bio-based coatings, and lightweight material engineering are enabling cartons to deliver high performance while minimizing environmental impact. Companies are focusing on increasing the share of renewable raw materials, improving recyclability, and reducing overall material intensity across packaging structures. In parallel, efforts to integrate tethered caps, fiber-based closures, and fully recyclable components are reshaping product design. These innovations are aligned with evolving regulatory requirements and corporate sustainability commitments, including carbon reduction targets and circular economy goals.

Category-wise Analysis

Capacity Insights

The 250-500 ml segment is anticipated to retain its leadership position, accounting for approximately 40.9% market share in 2026, and is expected to maintain a dominant share through the forecast period. This segment is widely used for single-serve applications in dairy, flavored milk, and small-format beverages. Its dominance is driven by high consumption frequency, affordability, and convenience, particularly among urban consumers and younger demographics. The size aligns well with on-the-go consumption, school meal programs, and portion-controlled packaging, making it a staple across supermarkets, convenience stores, and institutional channels. From a practical standpoint, major dairy brands and beverage companies continue to rely on this format for daily consumption products such as fresh milk, chocolate milk, and fruit juices.

For example, single-serve milk cartons distributed in school nutrition programs and quick-service outlets predominantly fall within this range. The format also supports high turnover rates and efficient shelf stocking, reinforcing its commercial viability across both developed and emerging markets.

The 500-750 ml segment is anticipated to be the fastest-growing capacity range over the forecast period, driven by increasing demand for mid-sized, shareable packaging formats. This segment caters to consumers seeking better value per unit while maintaining portability and convenience. It is gaining traction in RTD beverages, functional drinks, flavored milk, and premium dairy products. Growth in this segment reflects evolving consumption patterns, where products are often consumed across multiple occasions rather than in a single sitting.

The availability of resealable closures such as screw caps and flip caps enhances usability, making these packs suitable for both individual and small-family consumption. For instance, RTD coffee brands and premium juice manufacturers are increasingly adopting this format to balance premium positioning with practical usability, particularly in urban retail environments. The segment also benefits from rising demand in e-commerce grocery channels, where slightly larger pack sizes offer logistical and pricing advantages.

Application Insights

The food & beverages segment is anticipated to maintain its dominant position, accounting for approximately 44.7% of the market share in 2026, primarily driven by milk and fresh liquid products. The segment benefits from consistent global demand for dairy consumption and the widespread adoption of cartons in liquid food packaging. Gable top cartons are extensively used for fresh milk, cream, buttermilk, and liquid food products, where hygiene, product protection, and shelf-life extension are critical.

Their ability to provide lightweight, tamper-evident, and food-safe packaging makes them a preferred choice for both manufacturers and consumers. For example, leading dairy cooperatives and private-label brands across North America and Europe rely heavily on gable top cartons for daily milk distribution. In emerging markets, the format is increasingly used for fortified milk and value-added dairy products, supporting nutritional programs and expanding consumer access to packaged food.

The juices segment is anticipated to be the fastest-growing application category, supported by rising consumption of plant-based beverages, functional drinks, and ready-to-drink (RTD) juices. Gable top cartons offer strong advantages in preserving flavor, nutritional value, and product freshness, while also supporting premium branding and shelf differentiation. This growth is closely linked to increasing health awareness and demand for natural, organic, and minimally processed beverages.

For instance, cold-pressed juice brands and plant-based drink manufacturers are increasingly adopting carton packaging to communicate sustainability and product quality. The format also enables ambient storage and extended shelf life, which is particularly valuable in regions with limited cold chain infrastructure. As a result, juice manufacturers are leveraging gable top cartons to expand into new markets while maintaining product integrity and reducing distribution costs.

Regional Insights

North America Gable Top Liquid Cartons Market Trends - Innovation-Driven Demand with Localized Manufacturing Expansion

North America represents a mature yet innovation-driven market for gable top liquid cartons, supported by a well-established dairy industry, advanced food processing infrastructure, and strong consumer demand for convenience packaging. The U.S. leads regional demand, driven by high consumption of fluid milk, plant-based beverages, juices, and RTD drinks. Large dairy processors and beverage brands continue to rely on gable top cartons for fresh milk distribution and private-label retail products, reinforcing stable baseline demand.

Regulatory frameworks across the region emphasize food safety, recyclability, and extended producer responsibility (EPR), encouraging a gradual shift toward fiber-based packaging formats. This has translated into tangible investments. For instance, Elopak’s establishment of its first U.S. manufacturing facility in Arkansas (2025) reflects growing demand for localized carton production and reduced supply chain dependency. Similarly, major retailers and dairy brands in the U.S. are increasingly adopting paper-based cartons for private-label milk and organic beverages, aligning with sustainability commitments.

Companies such as Pactiv Evergreen (now part of Novolex) continue to supply gable top cartons for mainstream dairy applications, ensuring continuity in large-scale distribution. Innovation in closure systems, lightweight materials, and recycling technologies is becoming a key differentiator. Industry collaborations to improve carton recovery rates, especially through material recovery facility (MRF) upgrades, are strengthening the recycling ecosystem. As a result, investment opportunities are concentrated in premium packaging formats, low-carbon materials, and domestic manufacturing expansion, positioning North America as a stable yet evolving market.

Europe Gable Top Liquid Cartons Market Trends - Regulation-Led Sustainability and Circular Packaging Leadership

Europe is characterized by a highly regulated and sustainability-driven packaging landscape, where environmental compliance plays a central role in shaping market dynamics. Stringent regulations aimed at reducing packaging waste and promoting circular economy practices are accelerating the adoption of recyclable, fiber-based carton solutions. Gable top cartons align well with these objectives due to their high paper content and compatibility with existing recycling systems.

Key markets such as Germany, the U.K., France, and Spain demonstrate strong demand for sustainable packaging, supported by high consumer awareness and well-developed recycling infrastructure. This has led to increased investment and innovation across the value chain. For example, Tetra Pak’s 2025 investment in advanced sorting technologies in the UK is aimed at improving carton recovery rates and recycling efficiency. Similarly, European board producers like Stora Enso and Billerud are actively developing low-carbon liquid packaging boards, enabling converters to meet stricter environmental standards.

Brands across Europe are also increasingly shifting toward carton-based packaging for organic milk, plant-based drinks, and premium juices, leveraging sustainability as a key differentiator. Retailers are also playing a role by prioritizing eco-labeled and recyclable packaging formats in private-label offerings. Innovation efforts are focused on material reduction, barrier optimization, and fully renewable packaging structures, reinforcing Europe’s leadership in sustainable packaging development. While growth rates remain moderate compared to emerging regions, Europe continues to serve as a benchmark for regulatory compliance and sustainability innovation.

Asia Pacific Gable Top Liquid Cartons Market Trends - High-Growth Market Driven by Dairy Expansion and Urbanization

Asia Pacific is expected to be the largest and fastest-growing region, accounting for 36.8% of the market share in 2026, and is expected to maintain its leadership position throughout the forecast period. Growth is driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing consumption of packaged dairy and beverages.

China, India, Japan, and Southeast Asian countries are key contributors, each with distinct growth dynamics. India’s position as the world’s largest milk producer continues to drive strong demand for liquid packaging, particularly in organized dairy distribution. Companies such as UFlex (ASEPTO) have expanded aseptic carton manufacturing capacity in India to cater to rising demand from dairy and juice brands. In China, advancements in food processing and aseptic packaging technologies are supporting large-scale production of shelf-stable milk and beverages, with domestic and international brands increasingly adopting carton formats.

Regional expansion strategies by global players are also shaping the market. For instance, SIG’s continued expansion into high-growth Asian markets, including India and Southeast Asia, highlights the region’s importance for long-term volume growth. Similarly, multinational beverage brands are introducing RTD tea, flavored milk, and plant-based drinks in carton formats, particularly in urban retail channels. In Southeast Asia, countries like Thailand and Indonesia are witnessing rising adoption of carton packaging for juices and coconut-based beverages, driven by export demand and shelf-life advantages.

The region offers strong opportunities in localized production, cost optimization, and product customization, supported by favorable manufacturing economics. Increasing investments in packaging infrastructure, combined with rising consumer preference for affordable, convenient, and sustainable packaging, position Asia Pacific as the primary growth engine for the global gable top liquid cartons market.

Competitive Landscape

The global gable top liquid cartons market is moderately concentrated, with a few global players dominating the upper tier and a fragmented base of regional manufacturers. Leading companies compete on technology, product quality, sustainability, and global reach. The presence of integrated supply chains and strong distribution networks provides competitive advantages to established players, while regional firms focus on cost competitiveness and localized solutions.

Key players are focusing on innovation, sustainability, and geographic expansion. Strategies include developing advanced materials, enhancing recycling capabilities, and expanding production capacity in high-growth regions. Companies are also adopting integrated business models that combine packaging materials, filling technology, and after-sales services to strengthen market positioning.

Key Industry Developments

- In December 2025, Elopak ASA announced a strategic partnership with Blue Ocean Closures, securing exclusive global rights to market fiber-based caps for gable top cartons, aiming to reduce plastic usage and strengthen its sustainable packaging portfolio.

Companies Covered in Gable Top Liquid Cartons Market

- Tetra Pak

- Elopak ASA

- SIG Group AG

- Greatview Aseptic Packaging

- Pactiv Evergreen Inc.

- UFlex Ltd.

- Ecolean AB

- Stora Enso Oyj

- Billerud AB

- Metsä Board Corporation

- Nippon Paper Industries Co., Ltd.

- Smurfit Westrock plc

- Mondi Group

- International Paper Company

- DS Smith plc

- Huhtamaki Oyj

Frequently Asked Questions

The gable top liquid cartons market is estimated to be valued at US$5.1 billion in 2026.

The global gable top liquid cartons market is projected to reach US$7.4 billion by 2033.

Key trends include growing demand for sustainable packaging, rising adoption of aseptic cartons, increasing use of resealable closures, and expansion into RTD and plant-based beverage segments.

The 250-500 ml capacity segment leads the market, accounting for 40.9% of market share, due to its high usage in single-serve dairy and beverage products.

The gable top liquid cartons market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Major players include Tetra Pak, Elopak ASA, SIG Group AG, Stora Enso, and UFlex Ltd.