- Smart Packaging

- Laminated Tube Market

Laminated Tube Market Size, Share, and Growth Forecast 2026 - 2033

Laminated Tube Market by Material (Plastic, Aluminum, Others), Capacity (Below 50 ml, 51 to 100 ml, 101 to 150 ml, Above 150 ml), Application (Personal Care & Cosmetics, Consumer Goods, Pharmaceuticals, Food, Others), and Regional Analysis for 2026 - 2033

Laminated Tube Market Size and Trend Analysis

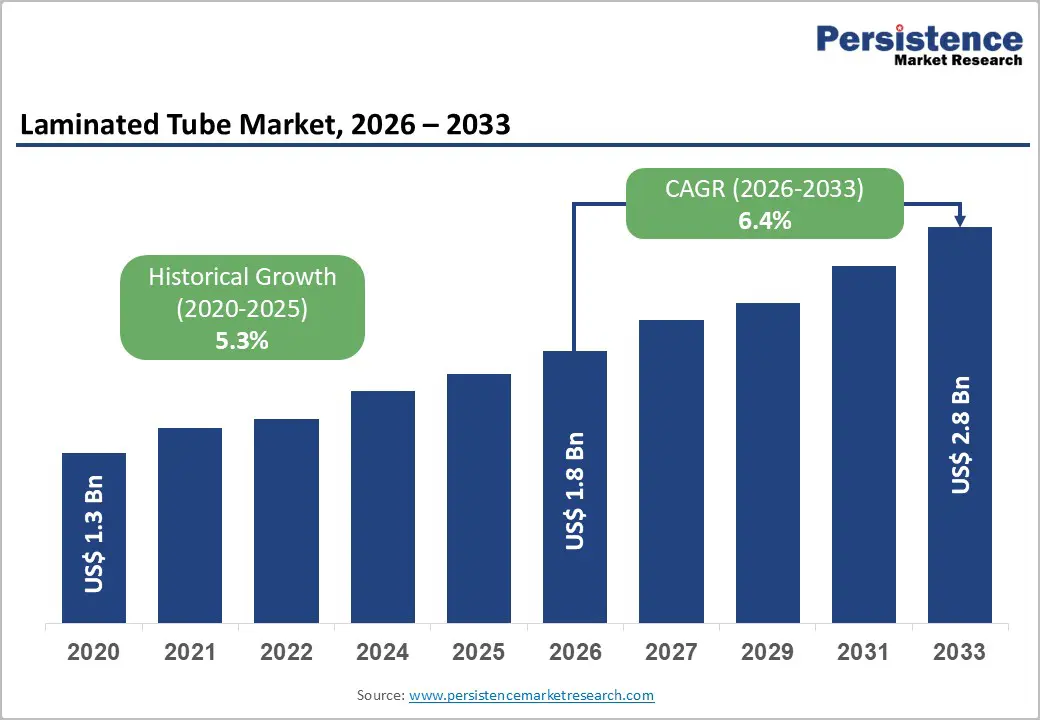

The global laminated tube market is valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 2.8 Bn by 2033, growing at a CAGR of 6.4% between 2026 and 2033. This growth is primarily driven by rising consumer demand for hygienic, barrier-protective packaging across the personal care, pharmaceutical, and food industries.

Laminated tubes constructed from multi-layer structures combining polyethylene, aluminium foil, or EVOH barriers offer superior protection against moisture, oxygen, and UV radiation, making them the preferred packaging format for sensitive formulations.

Key Industry Highlights:

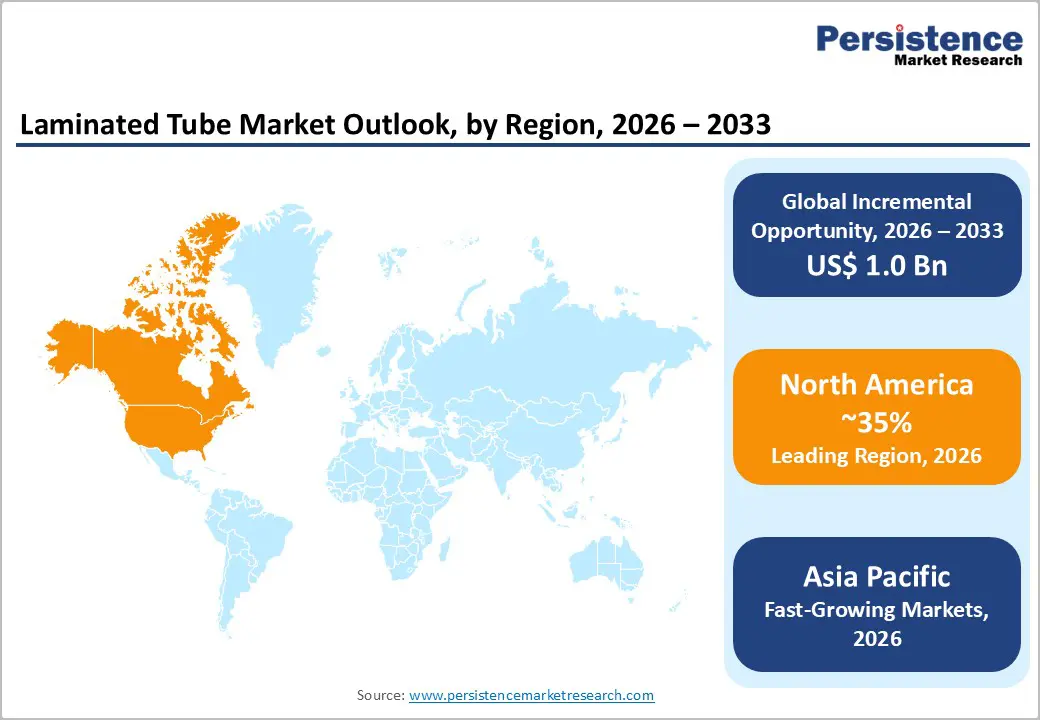

- Leading Region: North America leads the global laminated tube market, driven by strong pharmaceutical and personal care demand, FDA regulatory standards, and accelerating adoption of sustainable, recyclable mono-material tube solutions by major consumer brands.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market, with South Asia projected at a CAGR of 5.8% through 2035, fuelled by rising incomes, K-beauty/C-beauty product launches, and expanding manufacturing infrastructure.

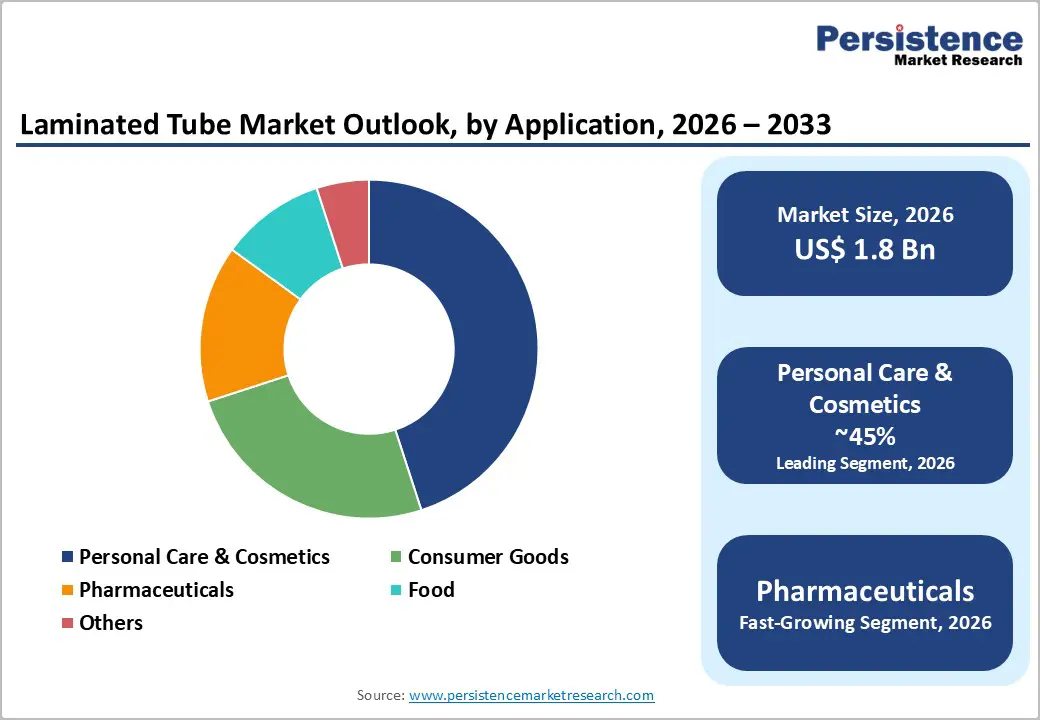

- Dominant Segment: Personal Care & Cosmetics is the leading application segment with approximately 45% market share, driven by global skincare, oral care, and haircare growth and the adoption of premium laminated tube formats by major beauty brands.

- Fastest Growing Segment: The Above 150 ml capacity segment is the fastest growing, expanding at over 5% CAGR, driven by consumer preference for larger value-sized personal care and food products.

- Key Opportunity: The transition to certified recyclable mono-material and PCR-content laminated tubes driven by global sustainability regulations represents the most commercially significant near-term opportunity for market participants.

| Key Insights | Details |

|---|---|

| Laminated Tube Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.4% |

| Historical Market Growth (2020 - 2025) | 5.3% |

DRO Analysis

Drivers - Rising Demand from Personal Care & Cosmetics Industry

The personal care and cosmetics industry represent the single largest demand driver for laminated tubes globally. According to Statista, the global skincare market was valued at approximately US$ 190.27 Bn in 2024 and is projected to reach US$ 235.96 Bn by 2030, reflecting sustained consumer spending on moisturizers, serums, sunscreens, and hair care treatments. These product categories overwhelmingly favour laminated tube packaging due to its squeezable convenience, precise dispensing capability, and barrier properties that prevent formulation degradation.

The personal care segment accounted for approximately 42% of total laminated tube demand in 2023. The surge in e-commerce-driven beauty retail has further amplified this demand, as brands require lightweight, leak-proof, and premium-looking tubes that withstand logistics handling while reinforcing brand identity on digital shelves.

Growing Pharmaceutical Packaging Applications

Laminated tubes are increasingly the packaging solution of choice within the pharmaceutical sector for topical formulations including ointments, creams, and gels. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) impose strict requirements on packaging integrity for pharmaceutical products, which laminated tubes satisfy through multi-layer aluminium barrier laminate (ABL) and plastic barrier laminate (PBL) constructions.

The pharmaceutical packaging application is projected to expand at a CAGR of 7.1% through 2032. The global ageing population, the shift from hospital-based to home care, and expanding access to over-the-counter dermatological products in emerging markets are collectively driving a structural uplift in pharmaceutical tube packaging demand, ensuring sustained and high-quality volume growth for laminated tube manufacturers.

Restraints - Environmental Concerns Over Multi-Layer Laminate Recyclability

A key restraint facing the laminated tube market is the inherent challenge of recycling multi-material laminate structures. Traditional ABL and PBL tubes combine dissimilar materials polyethylene, aluminium foil, and EVOH layers that are difficult to separate in conventional recycling streams.

The European Union's Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging be recyclable by 2030, is creating compliance pressure on manufacturers and brand owners. As regulatory scrutiny intensifies globally, companies that cannot demonstrate credible recyclability pathways risk losing contracts with sustainability-focused consumer brands, effectively constraining the growth trajectory of conventional laminated tube formats.

Raw Material Price Volatility

The laminated tube manufacturing process depends heavily on polyethylene resins, aluminium foil, adhesives, and speciality barrier films. These inputs are subject to significant price volatility linked to crude oil price fluctuations, aluminium market cycles, and global supply chain disruptions.

During 2021 - 2023, polyethylene resin prices experienced sharp increases of over 30-40% owing to supply chain bottlenecks. Such cost escalations directly compress manufacturer margins and can result in price increases being passed to brand owners, limiting tube adoption in cost-sensitive product categories such as food and entry-level consumer goods.

Opportunities - Emergence of Sustainable and Recyclable Mono-Material Tube Solutions

The transition to sustainable packaging presents a significant commercial opportunity for laminated tube manufacturers. Consumer brands committed to ESG targets are actively seeking certified recyclable tube alternatives. Advances in mono-material polyethylene laminate technology, which maintains barrier performance while enabling curb-side recyclability, are opening a new premium product tier.

The Australian Packaging Covenant Organization (APCO) and the ANZPAC Plastics Pact are among regional bodies pushing brand owners toward certified recyclable packaging. In October 2024, Albea Tubes launched local production of its Greenleaf™ recycle-ready laminate in North America, demonstrating robust commercial demand for such solutions.

Rapid Expansion in Asia Pacific Emerging Markets

Asia Pacific and particularly India, Southeast Asia, and China present an exceptional volume-growth opportunity for laminated tube manufacturers. India's fast-moving consumer goods sector, driven by companies such as Patanjali Ayurveda and Dabur, is actively expanding herbal and ayurvedic product ranges in laminated squeeze tube formats. According to Wifag Polytype India, the Indian laminate tube market carries enormous potential, and herbal product launches are meaningfully accelerating laminate tube consumption.

Similarly, South Korea and Japan continue to generate premium K-beauty and J-beauty innovations that require high-quality, customisable laminated tubes. The region as a whole is expected to register the fastest growth CAGR over the forecast period, driven by rising disposable incomes, urbanisation, and expanding modern retail penetration. Manufacturers establishing regional production bases and local supply chains in these markets are positioned for outsized share gains.

Category-wise Analysis

Material Insights

Within the material category, Plastic Barrier Laminate (PBL) tubes represent the leading segment, accounting for approximately 55% of the global laminated tube market. PBL tubes constructed using multi-layer polyethylene structures with EVOH or polyester barrier layers are the preferred material format across the personal care, cosmetics, and oral care segments owing to their squeezability, printability, and capacity to accommodate full-wrap, high-resolution decorative printing.

The growing sustainability imperative is reinforcing PBL's dominance, as mono-material polyethylene constructions enable easier recyclability versus traditional ABL structures. Aluminium Barrier Laminate (ABL) tubes, while commanding a strong ~45% share, are particularly valued in pharmaceutical applications due to superior dead-fold characteristics and tamper evidence, ensuring continued demand across regulated end-use categories.

Capacity Insights

The 51 to 100 ml capacity segment leads the laminated tube market, accounting for approximately 38% of total market share. This capacity range strikes the optimal balance between product economy-of-use and consumer convenience, making it the standard format for oral care (toothpaste), face wash, moisturising creams, and pharmaceutical ointment categories. According to industry data, oral care products that predominantly employ the 50-100 ml capacity account for a substantial share of overall laminated tube consumption globally.

The segment below 50 ml is also significant, driven by rising demand for travel-sized personal care products, dermatological samples, and high-potency pharmaceutical topicals. Meanwhile, the above 150 ml segment is the fastest growing, expanding at a CAGR exceeding 5%, driven by consumer preference for larger-format, value-sized personal care and food products.

Application Insights

The personal care & cosmetics segment dominates the laminated tube market with approximately 45% market share, sustained by robust spending on skincare, haircare, and oral care products worldwide. Laminated tubes are the packaging solution of choice within this segment due to their ability to deliver premium shelf appeal, precise dispensing, and extended product shelf life.

The segment's strength is further underpinned by the rapid growth of the K-beauty, C-beauty, and D2C beauty channels, which require customisable, visually differentiated packaging. The Pharmaceuticals segment follows as the second largest application, driven by expanding topical drug formulation markets globally, with pharmaceutical tube packaging projected to grow at the fastest application-level CAGR of 7.1% through 2033. The Food segment, though smaller in share, is growing driven by demand for squeezable condiments, sauces, and specialty food pastes.

Regional Analysis

North America Laminated Tube Market Trends

North America maintains a leading position in the global laminated tube market, underpinned by a highly mature personal care, pharmaceuticals, and food processing sector. The United States is the dominant national market within the region, with the U.S. tube packaging market projected to reach approximately US$ 3.17 Bn across all tube types by 2033.

Regulatory frameworks, including the FDA requirements for pharmaceutical tube packaging and increasing brand commitments to sustainable packaging, are pushing manufacturers to accelerate investments in recyclable mono-material and PCR-content laminated tube formats. In June 2024, Colgate launched its clear, recyclable PET Elixir toothpaste tube in North America, illustrating the pace of sustainable tube adoption.

Asia Pacific Laminated Tube Market Trends

Asia Pacific is the fastest-growing regional market for laminated tubes, driven by rapid urbanisation, rising disposable incomes, and a booming beauty and personal care industry across China, India, Japan, and South Korea. The region accounted for the largest global market share in 2024, reflecting the outsized scale of its consumer goods manufacturing base. China and India are key drivers of volume growth, with rising youth populations, growing middle-class consumption, and the influence of social media fuelling demand for cosmetics and personal care products packaged in laminated tubes.

In India, companies such as EPL Limited (formerly Essel Propack) headquartered in Mumbai, operate as among the world's largest laminated tube manufacturers, supplying oral care, cosmetics, and pharmaceutical brands globally. Huhtamäki Oyj continues to expand its laminated tube portfolio across India and Southeast Asia.

Europe Laminated Tube Market Trends

Europe represents one of the most regulatory-driven markets for laminated tube packaging, with the European Union's Packaging and Packaging Waste Regulation (PPWR) mandating full recyclability of packaging by 2030. This is reshaping the product strategies of all major laminated tube manufacturers operating in the region. Germany leads European consumption, supported by a large men's grooming market and a premium personal care industry.

Leading European tube manufacturers, including Hoffmann Neopac AG (Switzerland) and Huhtamäki Oyj (Finland), are actively investing in circular packaging solutions. In October 2024, Hoffmann Neopac achieved RecyClass EN 15343 certification for its Hungary facility and launched its Polyfoil Mono-Material tube range, becoming the first European tube maker to earn this certification for traceable recycled content.

Competitive Landscape

The global laminated tube market is moderately consolidated, with the top ten companies collectively accounting for over 50% of global revenue, while no single player commands a market share exceeding 15%. Leading multinational manufacturers including EPL Limited, Albea S.A., and Amcor Plc compete through vertically integrated manufacturing, global distribution networks, and accelerating investments in sustainable packaging R&D.

Key strategic differentiators include proprietary barrier laminate technologies, digital and high-resolution printing capabilities, and sustainability certifications. Emerging business model trends include collaborative co-development agreements with consumer brand owners, subscription-based tube supply contracts, and licensing of recyclable laminate technologies.

Key Developments:

- In August 2025, Uflex introduced anti-counterfeiting holographic film within its multilayer laminate tubes. UFlex has announced that it is integrating its anti-counterfeiting holographic film as a fundamental component of the multi-layer laminate design of tubes. This process goes beyond merely printing a cold foil or label; it involves embedding a brand-specific custom holographic film directly into the structure of the tube, thereby rendering duplication nearly impossible, as the company asserts.

- In October 2024, Berry Global Group, Inc., a global leader in packaging, declared a substantial investment aimed at expanding and improving the company’s tube manufacturing capabilities through the utilization of its newly patented DecoFusion hybrid technology process. This cutting-edge process creates a seamless construction tube that features high-impact, high-resolution graphic decoration, all while preserving a premium rebound and tactile experience.

Companies Covered in Laminated Tube Market

- Amcor Plc

- CCL Industries Inc.

- Huhtamäki Oyj

- Albea S.A.

- EPL Limited

- Alltub SAS

- Hoffmann Neopac AG

- San Ying Packaging (Jiangsu) Co., Ltd

- REGO

- Montebello Packaging Inc.

- STS Pack Holding

Frequently Asked Questions

The global Laminated Tube Market is estimated at US$ 1.8 Bn in 2026 and is projected to reach US$ 2.8 Bn by 2033, expanding at a CAGR of 6.4% during the forecast period 2026-2033.

The primary demand drivers include the rapid expansion of the global personal care and cosmetics industry valued at over US$ 500 Bn accelerating pharmaceutical packaging requirements enforced by regulatory bodies such as the FDA and EMA, growing consumer preference for hygienic and squeezable packaging formats, and brand-owner transitions to sustainable, recyclable laminated tube solutions in response to the EU's PPWR and comparable global regulations.

The Personal Care & Cosmetics segment holds the dominant position in the laminated tube market with approximately 45% market share. This leadership is driven by widespread use of laminated tubes for skincare, oral care, and haircare products, the global expansion of the beauty industry particularly in Asia Pacific and the growing preference for premium, barrier-protective, and customisable packaging formats by leading cosmetics brands.

North America leads the global laminated tube market, driven by a highly developed pharmaceutical and personal care sector, stringent FDA packaging requirements, and the rapid adoption of sustainable recyclable tube formats.

The key players operating in the global laminated tube market include EPL Limited, Albea S.A., Amcor Plc, Huhtamäki Oyj, Hoffmann Neopac AG, CCL Industries Inc., San Ying Packaging (Jiangsu) Co., Ltd, REGO, and STS Pack Holding, among others.