- Processed Food

- Frozen Dough Market

Frozen Dough Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Frozen Dough Market by Product Type (Bread, Pizza, Pastry & Croissant, Biscuits & Rolls, Others), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Stores / Bakery Stores, Online Retail / E-commerce, Foodservice Distribution), and Regional Analysis from 2026 to 2033

Frozen Dough Market Share and Trends Analysis

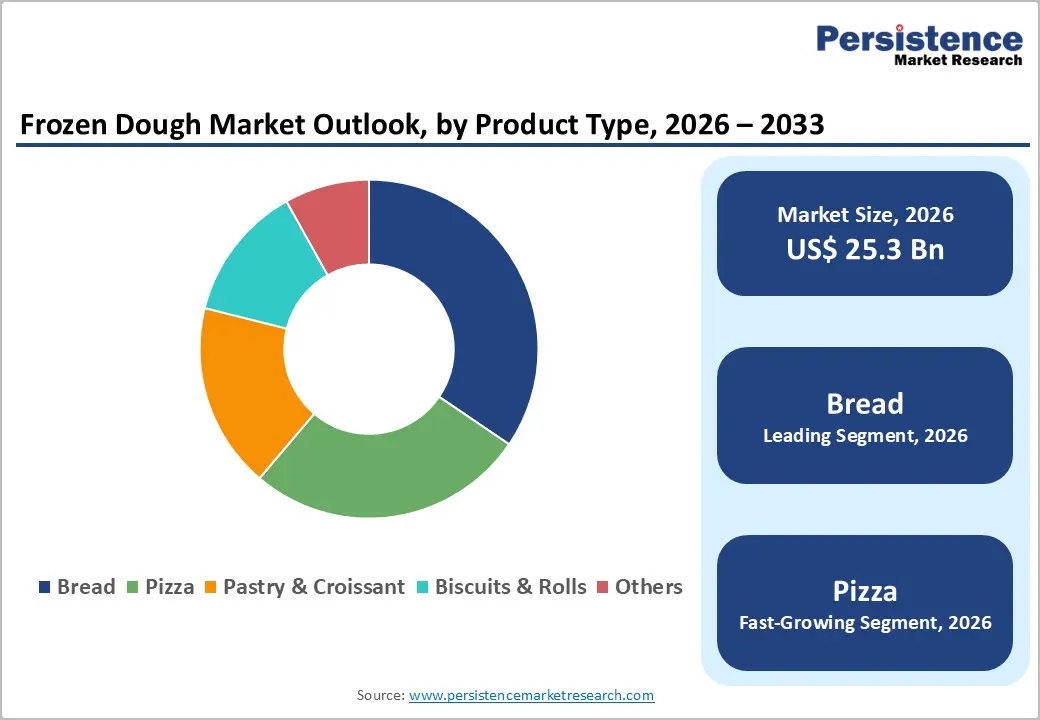

The global frozen dough market is estimated to grow from US$ 25.3 billion in 2026 to US$ 33.3 billion by 2033. The market is projected to record a CAGR of 4.0% during the forecast period from 2026 to 2033.

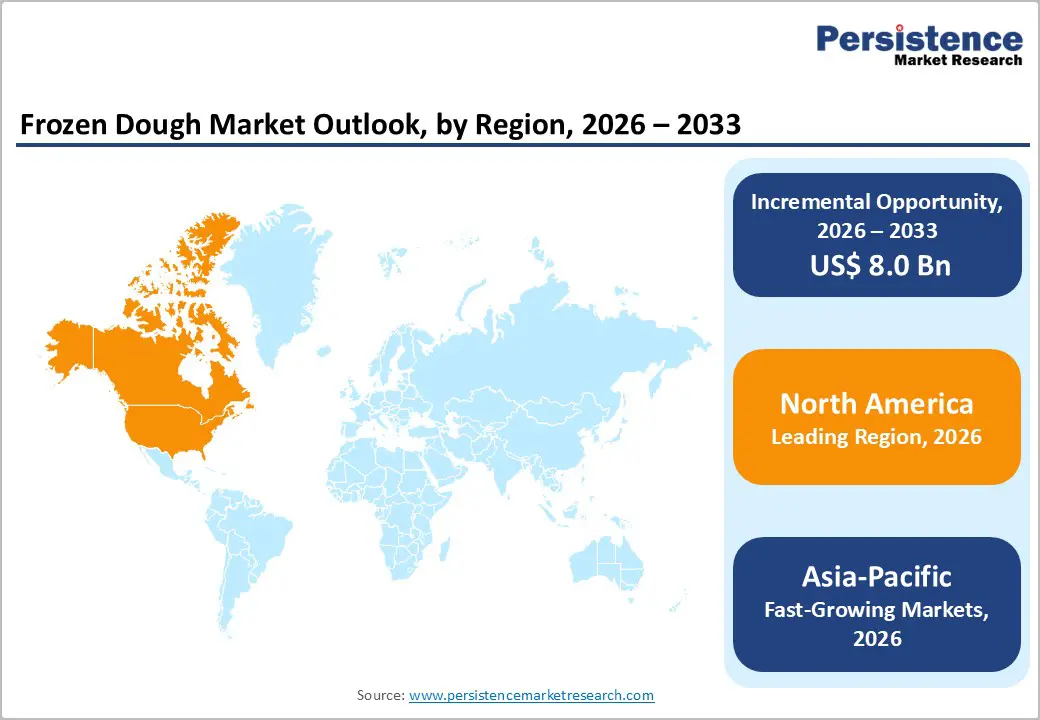

The global frozen dough market is expanding steadily, driven by rising demand for convenient bakery products and time-saving food preparation solutions. Europe leads the market due to strong bakery traditions and widespread consumption of bread and pastries, while Asia-Pacific is the fastest-growing region, supported by urbanization, expanding bakery chains, and increasing adoption of frozen bakery products.

Key Industry Highlights

- Dominant Segment: Bread dough held nearly 34.5% share in 2025, driven by high global consumption of bread products and strong demand from commercial bakeries, foodservice outlets, and retail consumers seeking convenient, ready-to-bake bakery solutions.

- Dominant Region: North America is the leading region in the frozen dough market with 36.2% share in 2025, supported by strong demand for convenience foods, widespread presence of quick-service restaurants, and advanced frozen food distribution infrastructure.

- Growth Indicators: Growth is driven by rising demand for convenient bakery products, expansion of quick-service restaurants and cafés, increasing adoption of frozen bakery solutions by commercial bakeries, and growing consumer preference for ready-to-bake and time-saving food products.

- Opportunity: Opportunities include development of gluten-free, organic, and clean-label frozen dough, expansion in emerging markets, innovation in artisanal and premium bakery products, and increasing demand from foodservice chains and in-store bakery sections of supermarkets.

| Key Insights | Details |

|---|---|

| Global Frozen Dough Market Size (2026E) | US$ 25.3 Bn |

| Market Value Forecast (2033F) | US$ 33.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Dynamics

Driver: Rising Demand for Convenient and Ready-to-Bake Bakery Product

The global shift toward convenient and time-saving food formats has significantly boosted the demand for frozen bakery dough products, including frozen dough for breads, pizzas, and pastries. In the United States, more than 58% of consumers purchased pre-packaged refrigerated or frozen dough at least once monthly, highlighting strong adoption among households seeking quick home meal solutions. Supermarkets and hypermarkets across North America and Europe have expanded shelf space for frozen dough and ready-to-ake bakery items to cater to this trend, reflecting a broad consumption pattern among busy working adults and dual-income families. In Europe, sales of frozen pizza dough increased by 26% in 2023, indicating strong consumer preference for ready-to-bake products that reduce meal preparation time while offering variety and quality at home.

Convenience extends beyond the home to commercial foodservice and quick-service restaurants (QSRs), where frozen dough enables consistent product quality and reduced labor costs. With over 45% of bakery chains in Europe integrating frozen dough to streamline operations, commercial adoption directly supports market growth and reinforces the role of convenience as a key demand driver. Manufacturers are also innovating with diversified frozen dough offerings such as par-baked croissants, sweet rolls, and artisan-style dough, making ready-to-bake dough products more appealing to a wide demographic. This global pattern powered by urban lifestyles, limited kitchen time, and preference for minimal preparation sustains increasing market growth for convenience-oriented frozen dough solutions.

Restraint: High Cold Storage and Transportation Costs

A critical challenge for the frozen dough market is the dependency on efficient cold chain infrastructure, which significantly increases operational and logistics costs. Frozen dough products require temperature-controlled storage and transportation from production facilities to retail outlets and foodservice clients to preserve quality and safety. The global cold storage market integral to frozen food logistics was valued at USD 138.5 billion in 2023, yet energy costs alone including electricity for cold storage can represent up to 30% of total operating expenses for temperature-controlled warehouses. These high costs erode profit margins for frozen dough manufacturers and distributors, particularly in regions with high energy tariffs or less efficient power grids.

In addition to energy expenses, logistics challenges such as temperature variation during transit and inadequate last-mile refrigeration further constrain market expansion. Industry estimates show that logistics costs account for 10-15% of the total cost of frozen food products, with approximately 30% of frozen food spoilage occurring during last-mile delivery due to temperature management issues. These inefficiencies disproportionately affect small and medium enterprises, which often lack capital to invest in advanced refrigerated fleets and cold storage facilities. High capital requirements and fragmented infrastructure in emerging economies also limit frozen dough penetration in rural and underdeveloped areas. Together, these factors underscore how cold chain cost and operational complexity restrain broader market growth by increasing product prices and limiting retailer adoption.

Opportunity: Rising Demand for Gluten-Free and Clean-Label Frozen Dough

Consumer interest in healthier ingredient profiles and dietary inclusivity is creating new opportunities for gluten-free, clean-label, and specialty frozen dough products. Across global frozen bakery categories, demand for alternative dietary products has accelerated: gluten-free frozen baked goods accounted for 18% of product launches in recent years, while plant-based and vegan frozen bakery options grew by nearly 29% in the same timeframe. Additionally, 38% of consumers prefer preservative-free frozen baked goods, reflecting growing prioritization of cleaner ingredient lists and transparency in food packaging. These trends indicate a strong opportunity for frozen dough manufacturers to differentiate offerings with health-centric claims tailored to evolving consumer preferences.

Emerging markets also present a fertile landscape for clean-label frozen dough expansion, as per-capita consumption of frozen bakery products remains relatively low compared to developed regions. In Asia-Pacific, increased cold chain investment has enabled broader product availability, supporting demand for premium and dietary-specific bakery options. Retailers report that products marketed with allergen-free, natural, or clean-label attributes have higher consumer engagement, with consumers increasingly reading ingredient lists before purchase. This presents a strategic opportunity for brands to develop gluten-free, organic, and minimally processed frozen dough formats, which not only meet health trends but also attract segments previously reluctant to buy conventional frozen bakery items. By aligning product development with health and wellness trends, frozen dough manufacturers can capture a broader consumer base and unlock new revenue streams as demand for specialty and clean-label frozen bakery items continues to grow.

Category-wise Analysis

By Product Type

Bread is a staple food consumed globally; according to FAO/UN data, the average per-capita consumption of bread and cereals in Europe and North America exceeds 75-100 kg per year, significantly higher than other bakery categories. Bread accounts for a major share of daily caloric intake in developed regions, driving constant demand. In the U.S., approximately 90% of households buy bread weekly, reflecting high staple usage rather than discretionary bakery items. Frozen bread dough provides consistency, reduced waste, and labor savings for commercial bakeries and foodservice operators, reinforcing its leading share. Bread’s fundamental role in daily diets is essential for sandwiches, breakfast routines, and meals, sustaining its dominance over pizza dough and pastries in frozen formats.

By Distribution Channel

Supermarkets and hypermarkets are the primary retail channels for frozen bakery products due to wide product assortments and extensive cold chain infrastructure. In the U.S., over 82% of frozen foods are purchased through grocery and mass merchandisers, according to USDA food availability data. These retailers invest in dedicated frozen sections with large freezers, ensuring product visibility and preservation. Supermarkets also offer promotional pricing and private-label frozen dough items, increasing consumer trial and repeat purchases. In Europe, retail grocery remains the top channel for frozen foods, accounting for over 70% of volume sales, supported by consumer preference for one-stop shopping convenience. The broad reach of supermarkets helps frozen dough products penetrate both urban and suburban markets more effectively than specialist or online channels.

Regional Insights

North America Frozen Dough Market Trends

North America leads the frozen dough market due to high consumption of bakery products and strong frozen food penetration. U.S. Department of Agriculture (USDA) data shows that Americans consume ~50 kg of bread per person annually, one of the highest global rates, and bakery items remain a staple across age groups. Frozen foods account for over 15% of total retail food sales in the U.S., supported by household freezer ownership exceeding 98%. The region’s established cold chain infrastructure and modern retail networks (supermarkets, mass merchandisers) ensure wide frozen dough availability. Commercial foodservice, including quick-service restaurants purchasing frozen dough for operational efficiency further amplifies demand, solidifying North America’s leading position.

Europe Frozen Dough Market Trends

Europe is critical in the frozen dough market due to a deeply embedded bakery culture and high per-capita bakery consumption. FAO data indicates that European countries like Germany, France, and Belgium have annual per-capita bread consumption of 70-90 kg, reflecting ingrained daily bread consumption. European retailers also report substantial sales of frozen bakery products, with frozen bread and pastry representing a significant share of the frozen foods category. The presence of traditional bakery preferences, such as croissants, artisan breads, and speciality rolls, creates steady demand for frozen dough formats to serve both retail consumers and commercial bakeries. Moreover, Europe’s strong regulatory frameworks for quality and food safety bolster consumer trust in frozen bakery products.

Asia-Pacific Frozen Dough Market Trends

Asia Pacific is the fastest growing region due to rapid urbanization, rising disposable incomes, and shifting dietary patterns. World Bank data shows that urban population in Asia Pacific exceeded 50% in recent years and continues to rise, leading to increased demand for convenient and ready-to-eat foods, including frozen bakery products. China’s retail frozen food sales have grown at double-digit rates annually, driven by expanding supermarket chains and improved cold chain logistics supported by government infrastructure initiatives. Additionally, Western-style bakery products, bread, pizza, and croissants are gaining popularity among younger consumers in India, China, and Southeast Asia. These demographic and consumption shifts propel frozen dough market growth faster than in established Western regions.

Competitive Landscape

The frozen dough market is highly competitive, dominated by global bakery and frozen food companies like ARYZTA, Grupo Bimbo, and Rich Products. These players focus on innovative dough varieties, expanding frozen bakery portfolios, strengthening distribution networks, and introducing premium and specialty products to meet consumer demand and maintain market share.

Key Industry Developments:

- In March 2026, The trend dubbed the “Ozempic effect” significantly influenced bakery product development, with Grupo Bimbo adapting its bread and snacks portfolio to align with changing consumer eating habits driven by increased use of GLP?1 weight?loss drugs like Ozempic.

- In July 2025, Europastry completed the acquisition of a 60% majority stake in Thailand’s Art of Baking, marking a strategic expansion into Southeast Asia. The Spanish frozen dough and bakery products specialist purchased the stake from Minor International Public Co. and Srifa Frozen Food, with both retaining 20% ownership each after the deal.

Companies Covered in Frozen Dough Market

- ARYZTA AG

- Bimbo Bakeries USA (Grupo Bimbo)

- Bridgford Foods Corporation

- Europastry S.A.

- General Mills Inc.

- Grupo Bimbo

- Guttenplan's Frozen Dough Specialists

- Lantmännen Unibake International

- Otis Spunkmeyer (ARYZTA)

- Pillsbury (General Mills)

- Rich Products Corporation

- Others

Frequently Asked Questions

The global frozen dough market is projected to be valued at US$ 25.3 Bn in 2026.

Rising demand for convenient, ready-to-bake bakery products, urbanization, foodservice growth, and frozen food adoption.

The global frozen dough market is poised to witness a CAGR of 4.0% between 2026 and 2033.

Expansion of gluten-free, clean-label, artisanal frozen dough, emerging markets, online retail, and premium bakery products.

ARYZTA AG, Bimbo Bakeries USA (Grupo Bimbo), Bridgford Foods Corporation, Europastry S.A., General Mills Inc., Grupo Bimbo.