- Processed Food

- Europe Frozen Food Market

Europe Frozen Food Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Europe Frozen Food Market by Product Type (Fruits & Vegetables, Dairy Products, Ready Meals, Meat & Seafood, Bakery & Confectionery, Snacks & Appetizers), by Flavor (Raw, Half Cooked, Ready to Eat), by Distribution Channel (B2B, B2C), by Regional Analysis, 2026 -2033

Europe Frozen Food Market Share and Trends Analysis

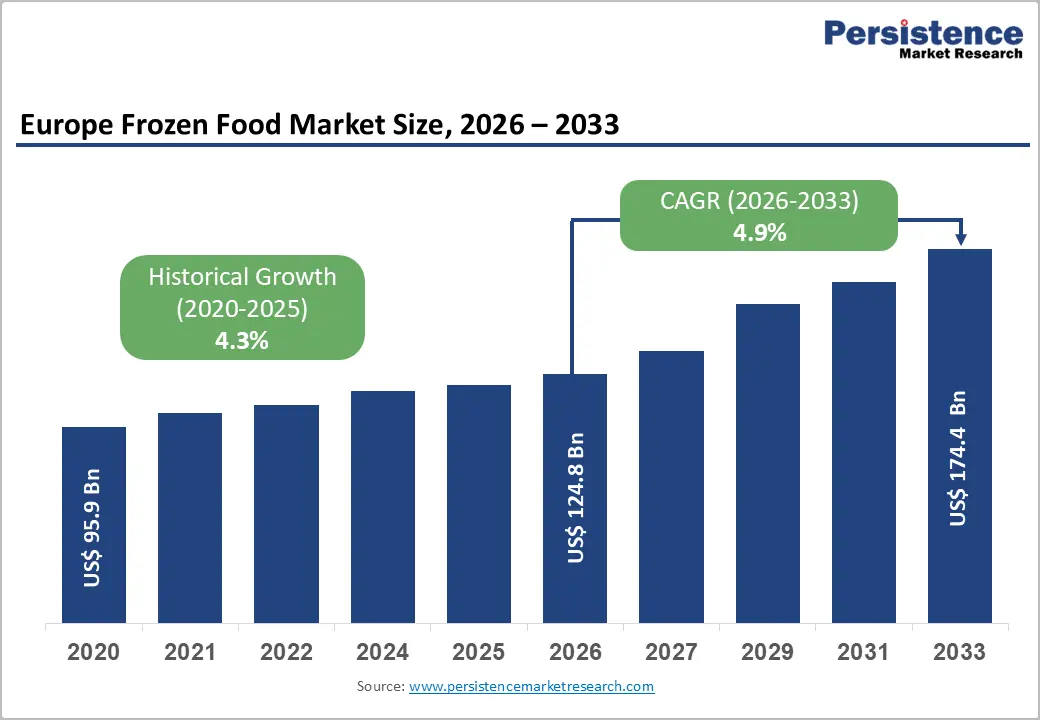

The Europe frozen food market size is estimated to grow from US$ 124.8 billion in 2026 to US$ 174.4 billion, projected to record a CAGR of 4.9% during the forecast period from 2026 to 2033.

Europe’s frozen food market is evolving rapidly as convenience, affordability, and premium meal experiences reshape consumer purchasing behavior. Busy urban lifestyles, rising demand for quick meal preparation, and growing acceptance of frozen nutrition are strengthening category expansion across households and foodservice channels. Consumers are increasingly seeking frozen products that combine convenience with clean-label ingredients, authentic regional flavors, and healthier nutritional profiles. Manufacturers are responding through innovation in ready-to-eat meals, plant-based recipes, organic frozen foods, and sustainable packaging solutions.

Key Industry Highlights:

- Leading Country: Germany, holding approximately 22% share in the Europe Frozen Food Market, driven by strong demand for premium frozen meals, convenient cooking solutions, and clean-label frozen products.

- Fastest-Growing Product Nature Segment: Ready to Eat Frozen Food, projected to grow at a CAGR of 6.9% during the forecast period, supported by rising demand for quick meal solutions and convenient home dining options.

- Leading Product Type Segment: Fruits & Vegetables, accounting for approximately 24% market share as of 2025, driven by increasing consumer preference for nutritious, convenient, and longer-lasting frozen produce products.

- Growth Indicators: Convenience-driven lifestyles, increasing workforce participation, and rising preference for time-saving meal solutions are accelerating demand for frozen ready meals across Europe.

- Consumer Trends: Consumers are increasingly preferring clean-label frozen foods, plant-based ready meals, organic frozen products, regional cuisine-inspired recipes, and healthier frozen alternatives with reduced preservatives and improved nutritional profiles.

- Opportunities: Expanding regional cuisine-inspired frozen food portfolios is creating strong opportunities for product differentiation, premium positioning, and broader consumer engagement across European markets.

Market Dynamics

Driver: Convenience-driven lifestyles accelerate demand for frozen ready meals

Fast-moving urban routines and changing household eating habits are significantly boosting demand for frozen ready meals across Europe. Consumers increasingly prefer quick meal solutions that reduce cooking time while offering consistent taste, portion control, and extended shelf life. Frozen pizzas, pasta dishes, ready-to-cook meat products, soups, and microwaveable meals are gaining popularity among working professionals, students, and smaller households seeking convenient food options.

Advancements in freezing technologies are also improving product texture, freshness retention, and nutritional quality, strengthening consumer acceptance across multiple demographics.

Growing participation of women in the workforce and increasing reliance on convenience-oriented grocery shopping are further accelerating market growth. Retailers are expanding frozen food sections with premium, organic, plant-based, and regional cuisine-inspired offerings to attract broader consumer groups. Rising demand for home dining, online grocery delivery, and value-focused meal solutions is also encouraging manufacturers to diversify frozen ready meal portfolios across European markets.

Restraint: Perceived Nutritional Inferiority Compared to Fresh Food Alternatives

Freshness perception continues to challenge growth in the Europe frozen food market as many consumers associate frozen products with lower nutritional quality compared to fresh alternatives. Concerns regarding preservatives, sodium content, texture changes, and nutrient degradation during freezing and reheating processes are influencing purchasing decisions among health-conscious consumers. Frozen ready meals and processed frozen products are often viewed as less wholesome, particularly by consumers prioritizing clean-label diets and minimally processed foods. This perception is limiting wider adoption across certain demographic groups despite advancements in freezing technologies.

Growing preference for fresh produce, locally sourced ingredients, and homemade meal preparation is further restraining frozen food consumption across several European markets. Consumer skepticism surrounding ingredient transparency and product quality is encouraging manufacturers to invest in cleaner formulations, organic offerings, and nutritional labeling improvements to strengthen confidence and improve category perception.

Opportunity: Regional cuisine-based frozen offerings differentiating product portfolios

Authentic regional flavors are creating strong growth opportunities in the Europe frozen food market as consumers increasingly seek convenient meals inspired by traditional cuisines. Frozen food manufacturers are expanding portfolios with region-specific dishes such as Italian pasta, Spanish paella, German specialties, Nordic seafood meals, and Mediterranean-inspired recipes to attract diverse consumer preferences. These offerings provide cultural familiarity, premium positioning, and restaurant-style experiences while maintaining the convenience benefits of frozen products.

Demand for globally inspired and locally authentic frozen meals is rising among younger consumers, working professionals, and households seeking variety in everyday dining.

Food companies are also leveraging regional cuisine-based innovation to strengthen brand differentiation and increase shelf visibility in competitive retail environments. Premium ingredients, artisanal recipes, clean-label formulations, and traditional cooking styles are helping manufacturers create higher-value frozen meal categories. Growing tourism influence and multicultural eating habits are further supporting demand for regional frozen food offerings across Europe.

Category-wise Analysis

By Nature Insights

Ready-to-eat frozen food is expected to show promising growth of CAGR 6.9% during the forecast period, driven by rising demand for convenient meal solutions among busy urban consumers. Increasing work commitments, changing household structures, and growing preference for time-saving food options are accelerating the consumption of frozen ready meals across European countries. Products such as frozen pasta dishes, pizzas, rice meals, soups, and microwaveable snacks are gaining popularity due to easy preparation, longer shelf life, and consistent taste quality.

Growth is further supported by expanding premium and health-focused product innovation within the ready-to-eat frozen category. Manufacturers are introducing organic meals, plant-based recipes, regional cuisine-inspired dishes, and clean-label formulations to attract health-conscious consumers seeking convenience without compromising food quality. Expanding online grocery retailing, improving cold chain infrastructure, and increasing home dining preferences are also strengthening market demand across Europe.

By Product Type Insights

Fruits & vegetables are likely to dominate with a 24% share as of 2026, supported by rising consumer preference for convenient, nutritious, and longer-lasting food products across Europe. Frozen fruits and vegetables retain essential vitamins, minerals, texture, and freshness through advanced freezing technologies, making them attractive alternatives to fresh produce. Consumers increasingly prefer frozen berries, peas, spinach, broccoli, mixed vegetables, and tropical fruits for smoothies, ready meals, soups, desserts, and healthy snacks. Their year-round availability and reduced food waste further strengthen demand among households and foodservice operators.

Growing interest in healthy eating, plant-based diets, and convenient meal preparation is accelerating the consumption of frozen produce across regional markets. Retailers are expanding frozen fruit and vegetable portfolios with organic options, steam-ready packaging, and premium product varieties to attract health-conscious consumers. Rising home cooking trends and demand for affordable nutritional ingredients are also reinforcing segment dominance throughout Europe.

Country-wise Insights

Germany Frozen Food Market Trends

Germany is likely to register 22% share in Europe frozen food market in 2026, supported by strong consumer demand for convenient meal solutions, premium frozen products, and ready-to-cook food options. Busy lifestyles, increasing single-person households, and growing preference for time-saving meal preparation are accelerating consumption of frozen pizzas, vegetables, bakery products, seafood, and prepared meals across the country. German consumers are increasingly seeking high-quality frozen foods with clean-label ingredients, reduced preservatives, and improved nutritional profiles.

Advancements in freezing technologies and efficient cold chain infrastructure are further strengthening product quality and market penetration.

Demand for organic frozen foods, plant-based ready meals, and regional cuisine-inspired offerings is also rising steadily across Germany. Retailers and manufacturers are expanding premium frozen portfolios featuring sustainable packaging, healthier formulations, and authentic taste experiences to attract health-conscious and environmentally aware consumers. Growth in online grocery platforms and home dining trends continues to support long-term market expansion.

U.K. Frozen Food Market Trends

U.K. frozen food market is expected to reveal a 5.7% CAGR during forecast period driven by changing eating patterns, rising grocery cost awareness, and increasing preference for longer-lasting food products. Consumers are increasingly purchasing frozen meat products, seafood, bakery items, breakfast foods, and prepared meals to manage food waste and improve household meal planning efficiency. Growing demand for affordable convenience foods among working families and younger consumers is supporting wider adoption across supermarkets and online grocery platforms.

Improved freezing techniques are also enhancing product texture, taste consistency, and storage flexibility across multiple frozen food categories.

Demand for healthier frozen alternatives featuring reduced salt, high protein, and plant-based ingredients is steadily increasing across the U.K. market. Manufacturers are introducing globally inspired recipes, air-fryer-friendly products, and portion-controlled frozen meals to attract modern consumers seeking convenience and dietary flexibility in everyday food consumption.

Competitive Landscape

Europe frozen food market is moderately fragmented, with multinational food companies, private-label brands, and regional manufacturers competing through product innovation, premium positioning, and convenience-focused strategies. Companies are expanding portfolios with ready-to-eat meals, frozen vegetables, plant-based products, seafood, bakery items, and regional cuisine-inspired offerings to attract evolving consumer preferences. Clean-label ingredients, sustainable sourcing, recyclable packaging, and healthier formulations with reduced salt and preservatives are becoming major competitive priorities across European markets.

Manufacturers are increasingly targeting health-conscious and convenience-seeking consumers through online grocery partnerships, digital marketing campaigns, and value-focused product launches. Flavor innovation featuring Mediterranean recipes, Asian-inspired meals, and traditional European dishes is strengthening product differentiation. Investments in cold chain infrastructure, freezing technologies, and sustainable packaging solutions are also enhancing product quality, shelf stability, and operational efficiency across the competitive frozen food landscape in Europe.

Key Industry Developments:

- In December 2025, Hormel Foods Corporation was named to Fast Company’s 2025 Brands That Matter list, recognizing its strong brand purpose and consumer relevance.

- In December 2025, McCain Foods and Cargill expanded their long-standing partnership in India to meet rising demand for frozen potato products, especially French fries.

- In June 2025, Conagra Brands, Inc. debuted over 50 new frozen food products spanning single-serve and multi-serve meals, vegetable side dishes, and gluten-free and plant-based options.

Companies Covered in Europe Frozen Food Market

- Nestlé

- Cargill, Incorporated

- Unilever

- Associated British Foods plc

- Grupo Bimbo

- Tyson Foods, Inc.

- General Mills, Inc.

- Hormel Foods Corporation

- Conagra Brands, Inc.

- Ajinomoto Co., Inc.

- ITC Limited

- McCain Foods Limited

- Del Monte Foods, Inc.

- Others

Frequently Asked Questions

Europe Frozen Food market is projected to be valued at US$ 124.8 Bn in 2026.

Convenience-driven lifestyles accelerate demand for frozen ready meals is driving the Europe Frozen Food market.

The Europe Frozen Food market is poised to witness a CAGR of 4.9% between 2026 and 2033.

Expanding regional cuisine-inspired frozen food offerings is emerging as a key growth opportunity for product differentiation in the Europe Frozen Food market.

Nestlé, Cargill, Incorporated, Unilever, Associated British Foods plc, Grupo Bimbo, Tyson Foods, Inc., and General Mills, Inc.