- Aerospace & Defense

- Military Personal Protective Equipment Market

Military Personal Protective Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Military Personal Protective Equipment Market by Product Type (Body Armor, Advanced Combat Helmets, Others), Branch (Army, Naval/Maritime Forces, Others), Technology, Function, and Regional Analysis for 2026 - 2033

Military Personal Protective Equipment Market Size and Trends Analysis

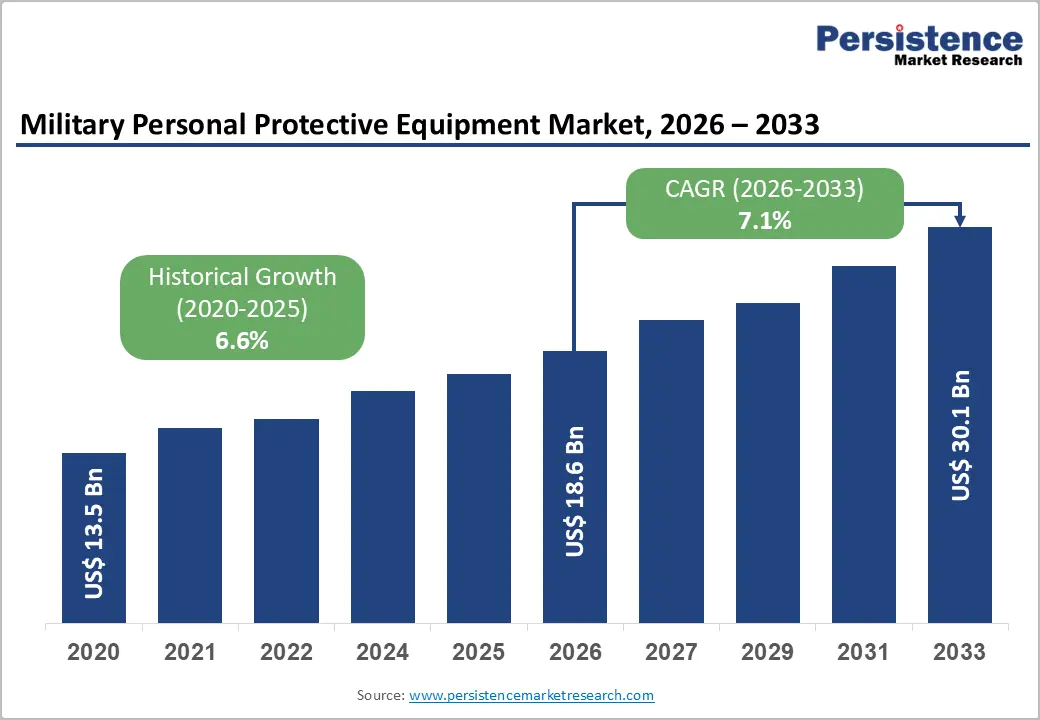

The global military personal protective equipment market size is likely to be valued at US$18.6 billion in 2026 and is expected to reach US$30.1 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by rising global defense expenditures, increasing modernization of armed forces, and growing demand for lightweight, mission-specific protection systems.

Governments across North America, Europe, and Asia Pacific are prioritizing investments in advanced soldier protection programs to improve operational survivability and combat readiness. Procurement strategies are increasingly focused on modular armor systems, integrated communications compatibility, and multi-threat protection capabilities.

Key Industry Highlights:

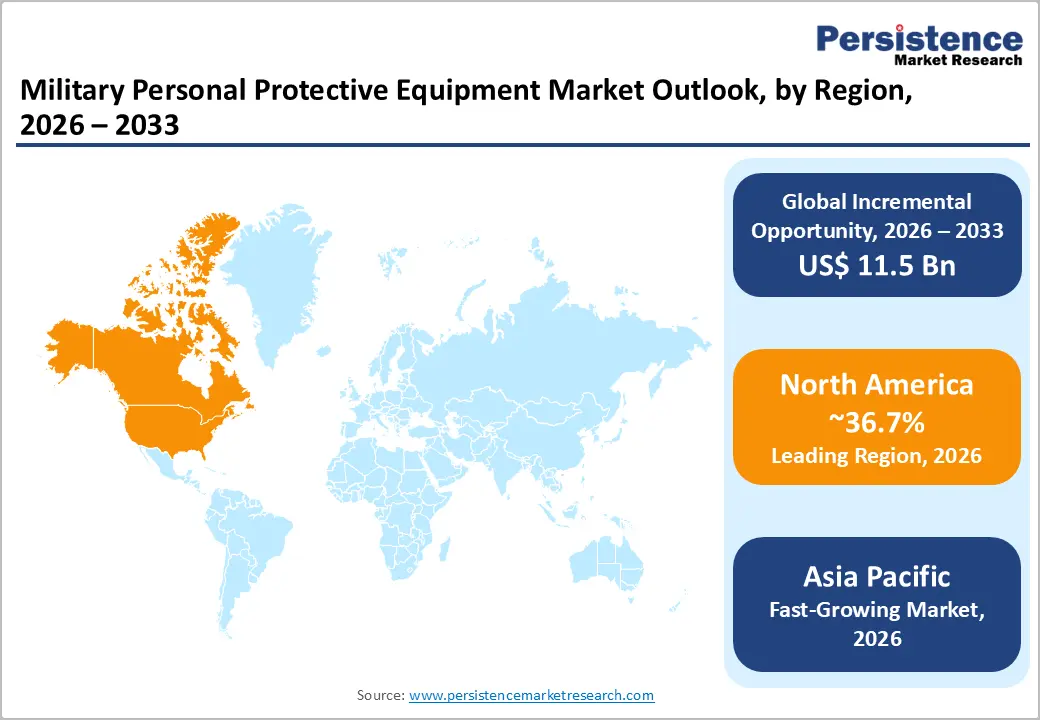

- Leading Region: North America is anticipated to account for approximately 36.7% of the market share in 2026, supported by high defense expenditure, advanced soldier modernization programs, and strong procurement infrastructure led by the U.S.

- Fastest-growing Region: Asia Pacific is projected to register the fastest growth, due to the rising defense budgets, indigenous manufacturing initiatives, and large-scale modernization programs across China, India, Japan, and ASEAN countries.

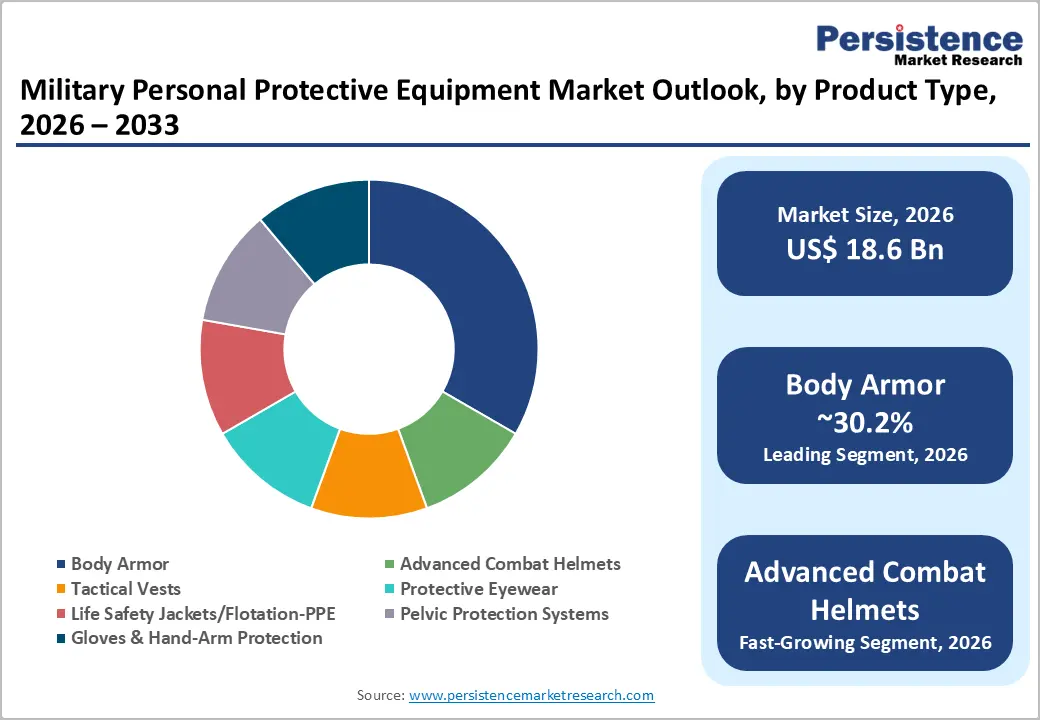

- Dominant Product Type: Body armor is anticipated to lead, accounting for approximately 30.2% of the market share in 2026, driven by recurring replacement cycles, modular armor adoption, and increasing demand for lightweight ballistic protection systems.

- Leading Branch: The army segment is expected to dominate the market with approximately 55.4% share in 2026, supported by large troop volumes, continuous infantry modernization initiatives, and sustained procurement demand for ballistic helmets, tactical armor.

DRO Analysis

Driver - Elevated Defense Spending and Military Modernization Programs Are Sustaining Long-Term Procurement Demand

Rising global military expenditure continues to support consistent procurement of body armor, advanced helmets, respiratory protection systems, and integrated soldier modernization platforms. Governments are allocating larger portions of defense budgets toward troop survivability and next-generation combat preparedness. Defense modernization initiatives in the U.S, China, India, Japan, and NATO member countries are creating long-term procurement cycles for protective equipment across infantry, naval, and special operations units.

Military PPE procurement differs from conventional defense purchases as equipment requires recurring replacement, periodic upgrades, and requalification throughout operational service life. Increasing deployment of troops in asymmetric warfare, border-security operations, and high-risk tactical environments is also reinforcing demand for ballistic-resistant and multi-hazard protective systems. This trend is especially visible in the body armor and advanced combat helmet categories, where procurement contracts are increasingly structured as multi-year modernization programs. The sustained increase in defense budgets creates strong long-term visibility for manufacturers operating across armor, communications-compatible helmets, and integrated soldier systems.

Expanding Threat Complexity Is Increasing Demand for Multi-Hazard Protection Systems

Modern military operations increasingly involve exposure to ballistic threats, blast impacts, chemical hazards, thermal risks, and electronic warfare environments. As a result, military organizations are broadening procurement requirements beyond conventional ballistic armor toward integrated PPE ecosystems capable of addressing multiple operational risks simultaneously.

CBRN preparedness has become a major procurement priority among NATO countries and several Asia-Pacific defense organizations due to evolving geopolitical tensions and hybrid warfare strategies. Soldiers operating in complex combat zones require lightweight systems capable of balancing mobility with enhanced protection. This operational requirement is accelerating demand for integrated protective clothing, respirators, thermal-resistant fabrics, gloves, eye protection systems, and smart wearable equipment.

Defense agencies are also prioritizing interoperability between protective systems and battlefield technologies such as communications devices, night-vision systems, and situational-awareness tools. Consequently, manufacturers capable of developing modular and multifunctional PPE solutions are gaining competitive advantages across military modernization programs.

Restraint - Lengthy Qualification Procedures and High Compliance Costs Limit Market Accessibility

Military PPE products must undergo rigorous ballistic, flame-resistance, fragmentation, environmental, and interoperability testing before receiving procurement approval from defense agencies. Certification standards vary across countries and procurement authorities, increasing qualification complexity for suppliers operating internationally. The product approval process involves extensive laboratory validation, operational field testing, and recurring compliance assessments, all of which significantly increase development costs and time-to-market. Smaller manufacturers often face challenges related to limited testing infrastructure, constrained capital resources, and extended procurement timelines.

These qualification barriers can delay the commercialization of innovative materials and next-generation protective technologies. Program concentration risk is another challenge, as defense suppliers may depend heavily on a limited number of long-term government contracts. Any procurement delay, budget revision, or certification failure can materially affect revenue realization and operational planning for manufacturers.

Opportunity - Asia-Pacific Localization Initiatives Are Creating Significant Manufacturing Opportunities

Asia-Pacific represents the fastest-growing regional market due to increasing defense modernization initiatives and rising emphasis on domestic military manufacturing capabilities. Governments across China, India, Japan, South Korea, and ASEAN countries are strengthening indigenous defense production ecosystems to reduce dependence on foreign suppliers and improve supply-chain security. This localization trend is creating substantial opportunities for regional PPE manufacturers, joint ventures, and technology-transfer partnerships. Domestic procurement preferences are particularly strong in categories such as ballistic armor, advanced helmets, tactical protection systems, and specialized naval protection equipment.

Companies capable of establishing regional manufacturing facilities, local certification capabilities, and sovereign production partnerships are expected to benefit from expanding procurement programs. The opportunity extends beyond product supply into lifecycle services, including maintenance, replacement, and integrated soldier-system upgrades.

Lightweight Materials and Smart Protection Technologies Are Driving Product Innovation

Defense organizations are increasingly focused on reducing soldier load burden without compromising ballistic or environmental protection. This trend is accelerating the adoption of ultra-high-molecular-weight polyethylene (UHMWPE), advanced aramid fibers, carbon composites, and smart sensor-integrated textiles.

Manufacturers are investing heavily in lightweight armor systems that improve mobility, endurance, and operational flexibility in extended combat environments. Advanced helmet systems are now incorporating communication interfaces, situational-awareness sensors, impact-monitoring technologies, and night-vision compatibility.

The growing integration of wearable electronics into protective equipment is creating opportunities for suppliers specializing in smart textiles, biometric monitoring, and connected soldier platforms. As militaries transition toward network-centric warfare environments, integrated protective systems capable of combining survivability with battlefield connectivity are expected to witness strong procurement demand.

Category-wise Analysis

Product Type Insights

Body armor is anticipated to account for approximately 30.2% of the market share in 2026, making it the leading product segment. Strong procurement demand from infantry forces, border-security units, and special operations teams continues to support segment dominance. Countries such as the U.S., India, and China are prioritizing modernization of soldier survivability systems, driving large-scale adoption of lightweight ballistic vests and modular armor carriers.

The market is shifting toward ergonomic and scalable armor systems that improve mobility and reduce combat fatigue during extended missions. Manufacturers, including Point Blank Enterprises and Safariland, are focusing on modular plate carriers and advanced ceramic insert technologies compatible with tactical communications and load-bearing systems. Recurring replacement cycles for ballistic plates and soft armor materials, combined with stricter ballistic standards, continue to strengthen long-term demand across the segment.

Advanced combat helmets are anticipated to witness the fastest growth during the forecast period due to rising demand for integrated battlefield connectivity and lightweight ballistic protection. Defense organizations are increasingly procuring helmet systems capable of supporting communications devices, night-vision equipment, augmented-reality interfaces, and hearing-protection technologies.

Manufacturers such as Team Wendy, Gentex Corporation, and MSA Safety are developing next-generation helmets with lightweight composite structures and modular accessory compatibility to improve soldier mobility and situational awareness. Demand remains particularly strong among special forces and rapid-response tactical units operating in high-intensity combat environments. The growing adoption of sensor-enabled helmet systems and smart battlefield integration technologies is expected to significantly accelerate segment growth over the forecast period.

Branch

The army segment is anticipated to hold approximately 55.4% of the market share in 2026, maintaining its position as the largest branch-level consumer. Ground forces operate across the broadest range of combat scenarios and face continuous exposure to ballistic, blast, environmental, and CBRN threats, resulting in substantial demand for advanced protective equipment.

Armies require extensive PPE inventories, including body armor, combat helmets, tactical eyewear, gloves, and flame-resistant apparel. Programs such as the U.S. Army Soldier Protection System and India’s infantry modernization initiatives continue to drive procurement of integrated soldier-survivability platforms. High troop volumes, recurring replacement requirements, and long-term modernization contracts are expected to sustain segment leadership throughout the forecast period.

Naval and maritime forces are anticipated to register the fastest growth among branch categories due to rising investments in naval modernization, amphibious warfare capabilities, and maritime-security operations. Naval personnel require specialized PPE solutions capable of performing effectively in saltwater, underwater, and confined operational environments.

Demand is increasing for flotation-compatible armor systems, corrosion-resistant protective gear, underwater breathing equipment, and communication-enabled maritime helmets. Countries including China, the U.S., India, and Japan are expanding naval modernization programs to strengthen maritime defense capabilities and secure strategic sea routes. The growing importance of littoral warfare, submarine operations, and special maritime missions is expected to create strong long-term demand for advanced naval PPE systems.

Regional Insights

North America Military Personal Protective Equipment Market Trends

North America is anticipated to account for approximately 36.7% of the market share in 2026, supported by high defense spending, advanced procurement systems, and strong military modernization programs. The region benefits from extensive investments in soldier survivability technologies, integrated battlefield systems, and advanced ballistic protection materials.

U.S. Military Personal Protective Equipment Market Trends

The U.S. remains the dominant contributor to the North American market due to its large defense budget and continuous investment in soldier modernization initiatives. Programs such as the Soldier Protection System (SPS) and Integrated Visual Augmentation System (IVAS) are accelerating procurement of lightweight body armor, advanced combat helmets, tactical eyewear, and integrated communication-enabled PPE.

The country also hosts several major manufacturers specializing in ballistic armor, advanced materials, and tactical protection systems. Growing investments in smart helmets, wearable battlefield sensors, and CBRN protection equipment continue to strengthen market demand. Recurring replacement cycles for ballistic vests and helmets further support long-term procurement opportunities.

Canada Military Personal Protective Equipment Market Trends

Canada is steadily expanding investments in military modernization and tactical readiness enhancement programs. The Canadian Armed Forces are increasing procurement of advanced body armor systems, flame-resistant combat apparel, and protective headgear to improve operational safety during domestic and international missions. The country is also emphasizing interoperability with NATO standards, which is encouraging the adoption of advanced protective technologies compatible with multinational operations. Increased focus on Arctic operations and harsh-environment combat readiness is supporting demand for thermal-resistant and climate-adaptive PPE systems.

Europe Military Personal Protective Equipment Market Trends

Europe represents a strategically important market driven by rising defense budgets, regional security concerns, and increasing interoperability requirements among allied defense organizations. The region is witnessing growing investments in advanced soldier-protection systems, CBRN preparedness, and next-generation tactical equipment.

Germany Military Personal Protective Equipment Market Trends

Germany remains one of the leading European markets due to increasing investments in defense modernization and NATO readiness programs. The country is prioritizing procurement of lightweight ballistic armor, advanced helmets, and integrated soldier systems to enhance troop survivability and combat effectiveness.

German defense manufacturers are also focusing on advanced composite materials, smart textiles, and modular tactical protection technologies. Rising defense allocations and military restructuring initiatives are expected to support long-term PPE procurement growth.

U.K. Military Personal Protective Equipment Market Trends

The U.K. continues to strengthen its military modernization efforts through investments in advanced body armor, tactical communications-compatible helmets, and multi-threat protective equipment. British defense programs increasingly emphasize rapid-deployment readiness, special operations modernization, and CBRN preparedness.

The country also maintains a strong domestic defense manufacturing ecosystem specializing in respiratory protection systems, ballistic materials, and tactical survivability equipment. Ongoing investments in integrated battlefield technologies are expected to drive steady market demand.

France Military Personal Protective Equipment Market Trends

France is expanding investments in future soldier modernization initiatives focused on mobility, operational efficiency, and battlefield integration. Procurement demand remains strong for advanced combat helmets, lightweight armor systems, and wearable communication-integrated PPE platforms. The country’s emphasis on expeditionary operations and international defense cooperation is also supporting the adoption of interoperable protective systems designed for multinational military missions.

Asia Pacific Military Personal Protective Equipment Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market, driven by rapid military modernization, increasing defense expenditure, and expanding indigenous manufacturing capabilities. Countries across the region are heavily investing in advanced soldier-protection systems and localized defense production.

China Military Personal Protective Equipment Market Trends

China represents one of the largest military PPE markets in Asia Pacific due to extensive investments in military modernization and integrated combat readiness programs. The country is increasing procurement of advanced ballistic armor, tactical helmets, smart soldier systems, and maritime protection equipment. Domestic defense manufacturers are rapidly expanding capabilities in lightweight composites, advanced ceramics, and communication-integrated protective systems. Naval modernization and border-security initiatives continue to support strong market demand.

India Military Personal Protective Equipment Market Trends

India is emerging as a major regional manufacturing and procurement hub due to strong government support for indigenous defense production. Rising investments in soldier modernization programs are accelerating the adoption of ballistic helmets, lightweight body armor, tactical eyewear, and CBRN protection equipment. Programs supporting domestic procurement and local manufacturing partnerships are creating significant opportunities for regional PPE suppliers. Border-security requirements and modernization of infantry forces continue to strengthen long-term demand.

Japan Military Personal Protective Equipment Market Trends

Japan is expanding investments in defense preparedness and advanced combat readiness initiatives amid evolving regional security concerns. The country is increasingly procuring lightweight ballistic armor, integrated communication-enabled helmets, and maritime survival systems for naval and rapid-response forces. Japan’s focus on advanced materials research and wearable defense technologies is also supporting innovation across smart protective equipment and high-performance tactical systems.

Competitive Landscape

The global military personal protective equipment market is moderately fragmented and program-driven, with competition centered around technological capability, qualification compliance, manufacturing scale, and defense procurement relationships. Global material suppliers, armor manufacturers, helmet specialists, and integrated defense-system providers compete across different product categories and regional procurement frameworks.

Leading companies are prioritizing lightweight material innovation, modular system integration, and geographic expansion through local manufacturing partnerships. Competitive differentiation increasingly depends on certification capabilities, long-term procurement relationships, and the ability to develop integrated soldier-protection ecosystems that combine survivability, mobility, and battlefield connectivity.

Key Industry Developments;

- In January 2025, DuPont and Point Blank Enterprises announced an exclusive partnership to expand the deployment of Kevlar® EXO™ body armor systems, aiming to deliver lighter and more flexible ballistic protection solutions for military and law enforcement personnel.

- In April 2025, DuPont and Point Blank Enterprises introduced the Elite EXO™ next-generation soft armor platform utilizing Kevlar® EXO™ technology, designed to improve mobility, flexibility, and ballistic protection for tactical personnel.

Companies Covered in Military Personal Protective Equipment Market

- DuPont

- Honeywell International Inc.

- Avon Protection plc

- Gentex Corporation

- MSA Safety Incorporated

- Point Blank Enterprises, Inc.

- Safariland Group

- Team Wendy

- MKU Limited

- BAE Systems plc

- Elbit Systems Ltd.

- Morgan Advanced Materials plc

- ArmorSource LLC

- Revision Military Ltd.

- Rheinmetall AG

- 3M Company

Frequently Asked Questions

The global military personal protective equipment market is anticipated to be valued at US$18.6 billion in 2026.

The military personal protective equipment market is projected to reach approximately US$30.1 billion by 2033.

The military personal protective equipment market is expected to grow at a CAGR of 7.1% between 2026 and 2033.

Key trends include increasing adoption of modular body armor, rising demand for lightweight UHMWPE-based protective systems, integration of smart wearable technologies, growth in advanced combat helmets, and expanding procurement of CBRN protection equipment.

Body armor is anticipated to remain the leading product segment, accounting for approximately 30.2% of the market share in 2026, due to continuous procurement demand across infantry and tactical forces.

Major players include DuPont, Honeywell International Inc., Avon Protection plc, Gentex Corporation, and Point Blank Enterprises, Inc.