- Energy & Utilities

- Energy Storage for Unmanned Aerial Vehicle Market

Energy Storage for Unmanned Aerial Vehicle Market size, share, trends, growth, regional forecasts 2026 - 2033

Energy Storage for Unmanned Aerial Vehicle Market by Product Type (Battery Systems, Fuel Cell Systems), Endurance (Medium Altitude Long Endurance, High Altitude Long Endurance, Tactical UAVs, Small / Mini UAVs), Capacity (Up to 10 kWh, 11–50 kWh, 51–100 kWh, Above 100 kWh), End-user (Government & Defense Agencies, Commercial Enterprises, Industrial Operators), and Region Analysis for 2026 - 2033

Energy Storage for Unmanned Aerial Vehicle Market Trends and Analysis

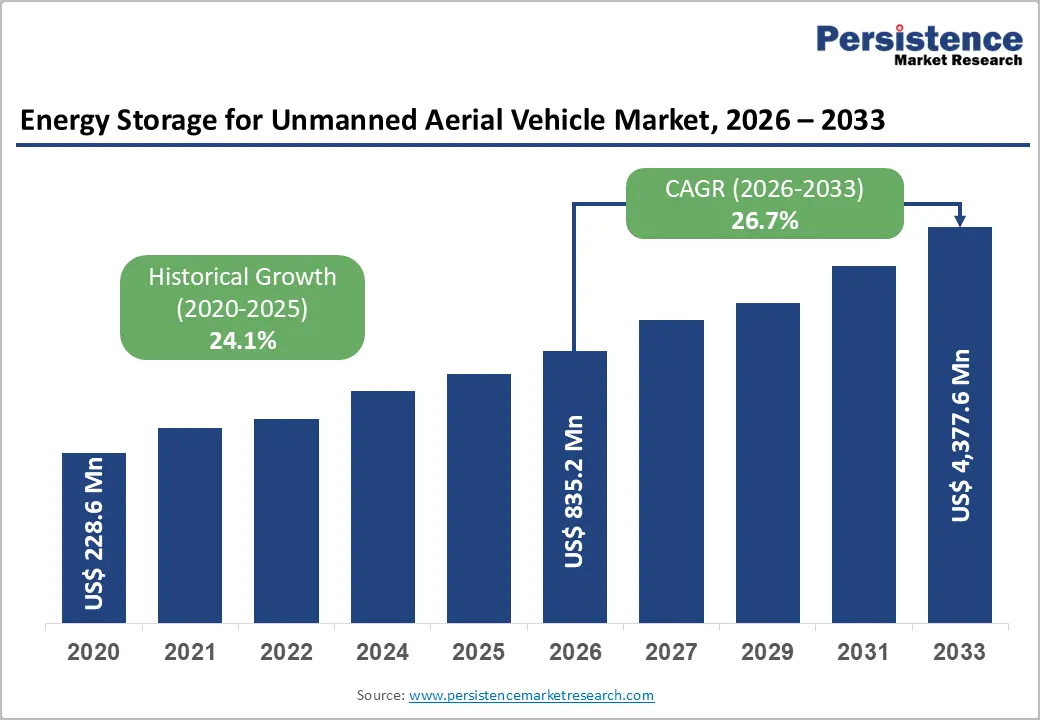

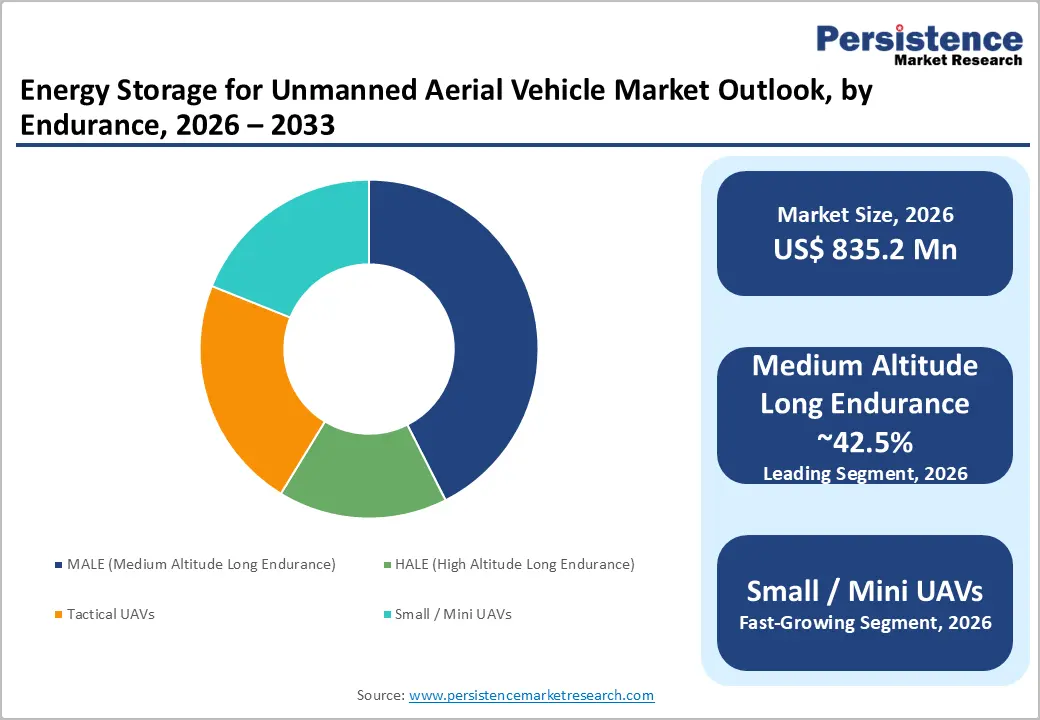

The global Energy Storage for Unmanned Aerial Vehicle Market size is projected at US$ 835.2 Mn in 2026 and is projected to reach US$ 4,377.6 Mn by 2033, growing at a CAGR of 26.7% between 2026 and 2033.

Accelerating defense UAV procurement programs, commercial drone adoption across logistics and agriculture, and breakthrough advances in high-energy-density lithium-sulfur and zinc-air battery chemistries are the primary growth catalysts. Rising demand for extended flight endurance in MALE and HALE platforms is driving investment in both battery and hydrogen fuel cell systems. Energy-as-a-Service models and battery swapping infrastructure are creating new recurring revenue streams for energy storage providers through 2033.

Key Industry Highlights:

- Leading Product Type: Battery Systems command 92.8% share; Fuel Cell Systems grow fastest at 29.9% CAGR, driven by defense MALE platform endurance requirements exceeding 2.8 kWh per mission.

- Top Endurance Segment: MALE UAVs lead at 42.5% share; Small/Mini UAVs grow fastest at 28.7% CAGR, driven by exponential commercial delivery and agricultural drone fleet deployment globally.

- Dominant End-user: Government & Defense Agencies lead at 53.1% share; Commercial Enterprises grow fastest at 30.1% CAGR, driven by Amazon, Wing, and Zipline drone delivery network scaling.

- Regional Performance: North America dominates at 41.8% share with the U.S. at US$ 301.8 Mn; Asia Pacific grows fastest at 30.0% CAGR with China at US$ 99.2 Mn and India at ~US$ 18.9 Mn.

- Strategic Developments: Ballard Power Systems' hydrogen fuel cell weight-reduction program (2024) and Intelligent Energy's NATO defense UAV fuel-cell integration are accelerating the commercialization of next-generation energy systems.

Market Dynamics Analysis

Drivers - Defense UAV Modernization and Sovereign Procurement Programs

Global defense spending on UAV platforms, and specifically long-endurance ISR (Intelligence, Surveillance, and Reconnaissance) and combat UAV systems requiring high-performance energy storage, represents the market's most structurally reliable demand driver. The U.S. Department of Defense's UAV procurement budget exceeded US$ 2.6 billion in fiscal year 2024 (DoD Budget Justification), with energy storage system upgrades for MALE and HALE platforms identified as critical capability enhancement priorities. NATO member nations collectively increased UAV-related defense expenditure by 17% in 2023–2024, per the NATO Defense Expenditure Report.

Israel's Ministry of Defense, South Korea's Defense Acquisition Program Administration, and India's Defense Research and Development Organization (DRDO) are each running active MALE UAV energy system procurement programs requiring domestically validated high-cycle lithium-ion and emerging fuel cell solutions. The U.S. Air Force's Golden Horde program and the U.S. Army's Future Vertical Lift initiative are both embedding advanced energy storage specifications into platform requirements. These sustained government procurement pipelines create multi-year energy storage supply contracts that provide UAV energy system manufacturers with the revenue certainty essential for advanced-chemistry R&D investment.

Commercial Drone Proliferation Across Logistics, Agriculture, and Inspection Applications

Commercial UAV adoption is generating a high-volume, rapidly expanding demand base for lightweight, high-cycle-life battery systems spanning last-mile delivery, precision agriculture, infrastructure inspection, and emergency response applications. The Federal Aviation Administration (FAA) registered over 855,000 commercial drones in the United States as of 2024, with commercial drone operations growing at a 24% annual rate. Amazon Prime Air, Wing (Alphabet), and Zipline are actively scaling drone delivery networks that require high-density battery systems capable of supporting 60–90-minute flight cycles with rapid recharge.

India's DGCA (Directorate General of Civil Aviation) Drone Rules 2021 and the EU's U-Space regulatory framework are progressively enabling commercial drone operations at scale, unlocking agricultural, inspection, and logistics UAV markets across 40+ countries, collectively representing hundreds of millions of annual flight operations by 2030. The global commercial UAV market exceeded US$ 36 billion in 2025 (Cognitive Market Research), with energy storage representing 15–18% of total platform cost. This structural linkage means commercial UAV fleet expansion directly multiplies energy storage procurement demand across battery replacement, fleet scaling, and next-generation platform upgrade cycles.

Restraints - Aviation Certification and Airworthiness Compliance Barriers for Advanced Energy Systems

UAV energy storage systems, particularly hydrogen fuel cells and next-generation lithium-sulfur or solid-state batteries, face extensive aviation certification requirements from the FAA, EASA, and equivalent national airworthiness authorities before commercial and defense deployment is permissible. EASA's Special Condition for VTOL aircraft and FAA's Part 135 certification pathway for commercial UAV operations impose energy system safety validation timelines of 18–36 months per platform configuration.

These certification cycles constrain the pace at which new battery chemistries and hydrogen fuel cell systems can transition from laboratory validation to certified commercial deployment, creating competitive disadvantages for innovators against established lithium-ion incumbents with existing type approvals.

Hydrogen Infrastructure Deficit Constraining Fuel Cell UAV Deployment Scale

Despite hydrogen fuel cells' superior energy density advantage, offering 3–5x longer endurance than equivalent-weight lithium-ion batteries at energy demands exceeding 2.8 kWh per mission (ScienceDirect, 2024), the absence of adequate hydrogen refueling infrastructure at operational UAV deployment sites structurally limits fuel cell system commercialization outside controlled military and test facility environments.

The Hydrogen Council estimates that only 12% of major commercial logistics and agricultural operation zones globally have hydrogen supply infrastructure accessible within operational radius, creating a critical deployment bottleneck that battery-swapping and fast-charging infrastructure, already available at 60%+ of drone operation sites, does not face.

Opportunities - Energy-as-a-Service (EaaS) and Battery Swapping Infrastructure for Commercial Drone Fleets

The structural shift toward drone delivery and autonomous inspection networks operating at high daily flight cycle frequencies, where battery recharging time creates operational throughput bottlenecks, is creating significant commercial opportunities for Energy-as-a-Service platforms that provide battery swapping stations, subscription-based energy management, and predictive battery health monitoring. DJI's Agras agricultural drone battery swap systems and Wing's charging infrastructure deployments are early commercial validations of this model, with the EaaS UAV addressable market projected to grow from negligible revenue in 2023 to over US$ 800 Mn by 2030.

Rapid recharge infrastructure networks, enabling 5–10 minute battery exchanges versus 45–90 minute conventional charging, unlock higher UAV utilization rates that directly improve fleet operator economics. For energy storage manufacturers and infrastructure providers, EaaS creates high-margin recurring revenue streams, replacing one-time battery sales with subscription contracts tied to flight hours and cycle guarantees. This business model convergence, combining hardware, software, and energy services, represents a structural market evolution that rewards vertically integrated UAV energy ecosystem players capable of deploying battery networks across logistics corridors and agricultural districts at commercial scale.

Next-Generation Battery Chemistry Commercialization for Extended Endurance Platforms

Lithium-sulfur (Li-S) and zinc-air battery chemistries, offering theoretical energy densities of 400–650 Wh/kg versus 150–250 Wh/kg for current lithium-ion systems, are approaching commercial readiness for UAV applications, with Oxis Energy and Zeta Energy advancing Li-S prototypes targeting 2026–2028 commercial availability. A doubling of specific energy density directly translates into either doubled flight endurance at equivalent weight or equivalent endurance at half the battery weight, transforming mission capability profiles for surveillance, agricultural, and logistics UAV platforms.

DARPA's advanced energy storage programs and the EU Horizon Europe research consortium's battery innovation initiatives are co-funding Li-S and solid-state battery UAV validation projects with defense and commercial partners.

For energy storage manufacturers positioned in this technology transition, the opportunity is to capture premium pricing on next-generation systems while simultaneously expanding the addressable MALE and HALE platform specifications that currently require hydrogen fuel cells due to lithium-ion's endurance limitations. The next-generation UAV battery chemistry addressable market is estimated at US$ 1.2–1.8 Bn by 2030, representing a high-value growth vector above the commodity battery replacement market.

Category-wise Analysis

Product Type Insights

Battery Systems lead the product type segment with a commanding 92.8% market share in 2026. Their dominance reflects the unmatched commercial maturity, cost accessibility, regulatory certification availability, and manufacturing scale of lithium-ion battery technology across both defense and commercial UAV platforms globally. Battery systems offer superior power density for dynamic maneuver and rapid throttle response, critical for multirotor and tactical UAV platforms, while benefiting from a global supply chain infrastructure that enables rapid procurement, field replacement, and maintenance.

Fuel Cell Systems, while offering superior energy density for extended endurance missions, remain constrained by limitations in hydrogen infrastructure, higher system weight, and incomplete airworthiness certification across most operational environments. Battery dominance will persist, though fuel cell share is projected to grow meaningfully in MALE/HALE defense applications.

Fuel cell systems are the fastest-growing product type, with a remarkable CAGR of 29.9% by 2033. Hydrogen fuel cells' 3–5x endurance advantage over lithium-ion at energy demands exceeding 2.8 kWh per mission, combined with defense MALE platform procurement programs requiring multi-hour ISR flight capability, are accelerating deployment.

Endurance Insights

MALE (Medium Altitude Long Endurance) UAVs lead the endurance segment with a 42.5% market share in 2026. MALE platforms, including the General Atomics MQ-9 Reaper, IAI Heron, and DRDO Rustom II, command the highest per-unit energy storage system values, driven by 12–40+ hour mission endurance requirements that demand large-capacity, high-cycle-life battery or hybrid fuel cell configurations. Defense procurement agencies across the U.S., Europe, Israel, and India specify MALE platforms as primary ISR and strike assets, sustaining consistent high-value energy storage procurement pipelines. While the Small/Mini UAV segment is growing rapidly, MALEs' per-platform energy system value ensures revenue leadership through 2033.

Small/Mini UAVs are the fastest-growing endurance segment, with a 28.7% CAGR through 2033. Exponential commercial drone adoption for delivery, agricultural monitoring, and inspection, combined with declining platform costs enabling mass deployment, is driving high-volume lightweight battery system procurement at an accelerating pace.

Capacity Insights

Up to 10 kWh leads the capacity segment with a 38.6% share in 2026. This capacity range serves the largest volume segment, small and mini commercial UAVs used for delivery, photography, agricultural sensing, and inspection, where lightweight compact battery packs enabling 20–60 minute flight endurance are the standard specification. The sub-10 kWh segment benefits from the widest availability of lithium-ion cells, the lowest per-kWh system costs, and the broadest FAA/EASA certification coverage.

Medium and large-capacity segments serve tactical and MALE platforms with higher per-unit value but lower volume. The 11–50 kWh segment is growing fastest, progressively narrowing the revenue gap with sub-10 kWh as medium UAV commercial applications scale.

11–50 kWh-capacity systems are the fastest-growing segment, with a 28.9% CAGR through 2033. Medium-capacity UAV applications, including agricultural spraying drones, cargo UAVs, and tactical military platforms, are scaling rapidly, requiring mid-range battery systems that bridge the gap between small commercial and large defense platform requirements.

End-user Insights

Government & defense agencies lead the end-user segment with a 53.1% market share in 2026. Defense agencies represent the highest per-unit value energy storage procurement segment, specifying advanced battery and fuel cell systems for MALE, HALE, and tactical UAV platforms with mission-critical endurance, reliability, and environmental survivability requirements that command premium pricing. U.S. DoD, NATO member defense ministries, and Asia Pacific sovereign defense programs sustain consistent multi-year procurement pipelines. While Commercial Enterprises represent the fastest-growing segment by volume, Government & Defense's combination of high unit values, long-term framework contracts, and classified technology programs ensures revenue leadership through 2033.

Commercial Enterprises is the fastest-growing end-user segment, with a 30.1% CAGR through 2033. E-commerce drone delivery scaling by Amazon and Wing, precision agriculture adoption, and infrastructure inspection fleet expansion are driving exponential commercial UAV energy storage procurement volume across multiple industries globally.

Regional Market Insights

North America Energy Storage for Unmanned Aerial Vehicle Market Share

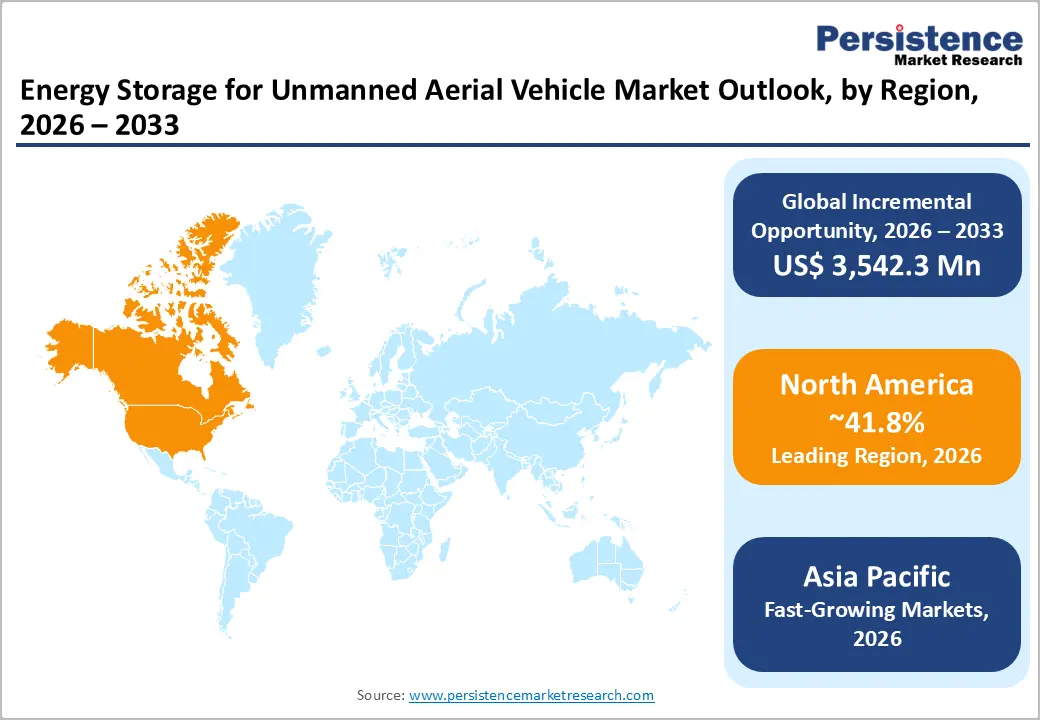

North America holds the dominant regional position with 41.8% share of the global Energy Storage for UAV Market in 2025, with the U.S. market estimated at ~US$ 301.8 Mn, anchored by world-leading defense UAV procurement programs, FAA commercial drone regulatory framework, and a deep technology innovation ecosystem.

U.S. Energy Storage for UAV Market:

The U.S. DoD's UAV procurement budget exceeding US$ 2.6 Bn in fiscal 2024, combined with DARPA's advanced energy storage R&D programs and the U.S. Air Force's long-endurance UAV platform investments, sustains the world's largest defense UAV energy storage demand base.

Commercial momentum is building through Amazon Prime Air's drone delivery network expansion and FAA Part 135 certification, enabling commercial operations at scale. Canada contributes to the defense and resource sector UAV energy storage demand. North America's growth is driven by defense MALE/HALE platform energy system upgrades, commercial drone fleet scaling and next-generation battery-chemistry commercialization programs funded by DARPA and DoE.

Europe Energy Storage for Unmanned Aerial Vehicle Market Share

Europe accounts for a considerable share of the global energy storage for unmanned aerial vehicle market in 2025, growing at a 25.1% CAGR through 2033, with Germany's market estimated at ~US$ 223.1 Mn, anchored by defense procurement, EU UAV regulatory harmonization, and deep aerospace manufacturing capabilities.

Germany Energy Storage for UAV Market: Innovation

Germany's position as Europe's largest defense spender and home to Airbus Defense & Space, developing the Eurodrone MALE platform requiring advanced energy storage systems, makes it the regional technology and revenue anchor. The EU's U-Space regulation framework, implemented from January 2023, enables commercial drone operations across all member states, creating a unified market for commercial energy storage demand. France contributes Thales and Dassault defense UAV energy system procurement, while the U.K.'s BVLOS (Beyond Visual Line of Sight) drone trials across logistics corridors are generating commercial energy storage validation demand. Europe's growth is anchored by Eurodrone MALE energy storage procurement, EU U-Space commercial drone enablement, and hydrogen fuel cell UAV R&D through Horizon Europe programs.

Asia Pacific Energy Storage for Unmanned Aerial Vehicle Market Insights

Asia Pacific is the fastest-growing region at 30.0% CAGR through 2033, driven by China's dominant UAV manufacturing ecosystem, India's rapidly scaling defense and commercial drone programs, and ASEAN's accelerating agricultural and logistics drone adoption.

China & India Energy Storage for UAV Market

China holds an estimated US$ 99.2 Mn market in 2026, anchored by DJI's global commercial drone manufacturing leadership, CASC and AVIC's defense UAV programs, and domestic lithium-ion cell manufacturing scale providing structural cost advantages. India, estimated at ~US$ 18.9 Mn, is growing at an accelerating pace driven by DRDO's Rustom MALE UAV program, PLI scheme-backed domestic drone manufacturing, and the DGCA drone regulations enabling commercial agricultural and logistics operations.

Japan is contributing to precision agriculture UAV energy storage demand through ACSL and Yamaha deployments, while ASEAN markets, particularly Indonesia and Vietnam, are experiencing rapid commercial drone fleet expansion. Asia Pacific's manufacturing cost advantages, government UAV production incentives, and expanding commercial drone ecosystems make it the most strategically dynamic region for energy storage growth through 2033.

Competitive Landscape

The global energy storage for UAV Market is highly fragmented, with leading players, Sion Power, Ballard Power Systems, Intelligent Energy, EaglePicher, and Kokam, collectively holding approximately 35% of global defense and commercial revenue in 2025. Regional battery manufacturers in China, led by CATL and EVE Energy's UAV-specific battery divisions, command significant commercial volume share. Key differentiators include energy density benchmarks, certification status, and weight-to-capacity ratios.

Technology leadership in next-generation chemistries (lithium-sulfur, solid-state), hydrogen fuel cell system miniaturization, geographic expansion into Asia Pacific defense procurement channels, and Energy-as-a-Service platform development define the dominant competitive strategy themes shaping the UAV energy storage market through 2033.

Key Developments:

- In November 2024, Ballard Power Systems expanded its hydrogen PEM fuel cell program for MALE defense UAV platforms, advancing lightweight stack designs targeting 40% weight reduction versus previous generation systems to extend ISR mission endurance beyond 20 hours at competitive payload fractions.

- In April 2024, SFC Energy AG expanded its EFOY hydrogen fuel cell distribution network across Asia Pacific UAV markets, targeting agricultural and infrastructure inspection commercial operators in Japan, South Korea, and Australia, investing in regional service and maintenance infrastructure to support in-field fuel cell system operations.

Global Energy Storage for Unmanned Aerial Vehicle Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 228.6 Mn |

|

Current Market Value (2026) |

US$ 835.2 Mn |

|

Projected Market Value (2033) |

US$ 4,377.6 Mn |

|

CAGR (2026–2033) |

26.7% |

|

Leading Region |

North America |

|

Dominant End-user |

Government & Defense Agencies – 53.1% Share |

|

Top-ranking Product Type |

Battery Systems – 92.8% Share |

|

Incremental Opportunity |

US$ 3,542.3 Mn |

Companies Covered in Energy Storage for Unmanned Aerial Vehicle Market

- Sion Power Corporation

- Ballard Power Systems Inc.

- Intelligent Energy Limited

- EaglePicher Technologies LLC

- Kokam Co. Ltd.

- Ultralife Corporation

- Electra.aero

- SFC Energy AG

- Cella Energy Ltd.

- Grepow Battery Co. Ltd.

- CATL

- Inventus Power

- Tadiran Batteries

- Texas Instruments

- H3 Dynamics Holdings

Frequently Asked Questions

The energy storage for unmanned aerial vehicle market is likely to be valued at US$ 835.2 Mn in 2026, projected to reach US$ 4,377.6 Mn by 2033.

Defense UAV modernization procurement programs and commercial drone proliferation across delivery, agriculture, and inspection applications, requiring extended flight endurance, are the primary growth drivers.

The market is projected to grow at a CAGR of 26.7% from 2026 to 2033.

Energy-as-a-Service battery swapping infrastructure for commercial drone fleets and next-generation lithium-sulfur battery chemistry commercialization for extended endurance platforms represent the most actionable near-term opportunities.

Sion Power, Ballard Power Systems, Intelligent Energy, EaglePicher, Kokam, Ultralife, SFC Energy AG, Grepow, CATL, and H3 Dynamics are the leading global participants.