- Aerospace & Defense

- MRO Distribution Market

MRO Distribution Market Size, Share, and Growth Forecast 2026 - 2033

MRO Distribution Market by Product Type (Engine Material & Components, Airframe & Component Spares, Hardware & Connectors, Cabin & Interior Components, Others), Sourcing Type (OEM New Parts, USM, PMA), Distribution Type (Traditional Distribution, E-Commerce & Marketplaces, Pooling/Exchange Programs, Vendor-Managed Inventory, PBH/Material-by-the-Hour), Platform, End-user, and Regional Analysis for 2026 - 2033

MRO Distribution Market Size and Trend Analysis

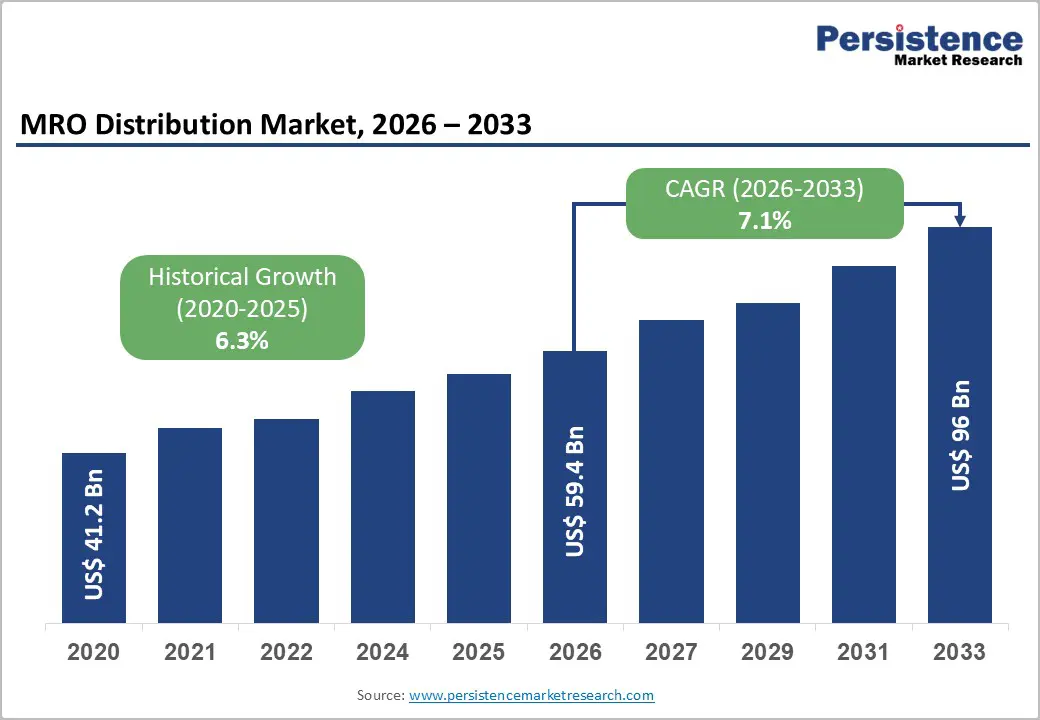

The global MRO distribution market size is expected to reach US$ 59.4 billion in 2026 and US$ 96.0 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033. This sustained growth trajectory is driven by the convergence of an aging global commercial aircraft fleet, record-high air passenger traffic, and rising aircraft-on-ground (AOG) pressures that demand faster aftermarket services.

Simultaneously, rising OEM production backlogs, supply chain disruptions, and an increase in airline fleet age are extending MRO cycles, compelling operators to rely more heavily on third-party MRO distributors for reliable, certified parts sourcing.

Key Market Highlights

- Aging Fleet Demand: Rising aircraft age, averaging 13.4 years in 2025, increases maintenance cycles, spare parts replacement, and distribution demand, especially for narrow-body fleets like Boeing 737NG and Airbus A320.

- Passenger Traffic Surge: Global air passengers reached 4.9 billion in 2024, exceeding 5 billion in 2025, significantly increasing flight hours, component wear, and demand for MRO parts distribution.

- Supply Chain Constraints: Around 78% aerospace suppliers face shortages, with component lead times reaching 12-18 months, increasing costs, disrupting inventory planning, and raising aircraft-on-ground operational risks.

- USM Growth Opportunity: Used Serviceable Material segment projected fastest growth at over 7.3% CAGR, driven by aircraft retirements and demand for cost-effective, traceable alternatives to OEM components.

- Engine Segment Dominance: Engine components dominate with approximately 38% market share, supported by high-value maintenance needs and engine overhauls, which contribute 40.7% of total MRO demand.

- Digital Distribution Rise: E-commerce and digital marketplaces are expected to grow at a CAGR above 6.6%, enhancing real-time inventory visibility, predictive maintenance integration, and faster procurement efficiency across global supply chains.

- North America Leadership: North America dominates with strong MRO infrastructure, a large fleet base, and the U.S. market valued at US$ 26.4 billion in 2026, supported by FAA-regulated repair networks.

- Asia Pacific Expansion: Asia Pacific holds around 30.8% share and is the fastest-growing region, driven by fleet expansion, rising passenger traffic, and increasing MRO investments across China, India, and ASEAN markets.

Market Dynamics

Drivers - Aging Commercial Fleet and Extended Aircraft Life Cycles Fueling Parts Demand

The global commercial aircraft fleet is experiencing an unprecedented rise in average age, creating a structural tailwind for the MRO distribution market. According to Oliver Wyman, the average age of the global commercial fleet reached 13.4 years in 2025, up from 12.1 years in 2024, driven largely by OEM production shortfalls. With over 17,000 jets in unfilled order backlogs (estimated to take 14 years to clear at current production rates), airlines are operating current fleets longer, increasing maintenance cycles, component replacements, and demand for spare parts distribution.

This dynamic underscores the criticality of maintaining supply chain efficiency, as operators seek to secure high-availability parts for aging narrow-body aircraft such as the Boeing 737NG and Airbus A320ceo families. The engine overhaul segment alone accounted for approximately 40.7% of the aerospace & defense MRO market in 2024, underscoring the depth of component sourcing demand from distributors and aftermarket service providers.

Record Air Passenger Traffic and Fleet Expansion Accelerating MRO Activity

Surging global air travel demand is a fundamental driver of expansion in the MRO distribution market. The International Air Transport Association (IATA) reported that global air passenger numbers reached an all-time high of 4.9 billion in 2024 and are expected to surpass 5 billion in 2025. This unrelenting growth in flight cycles and block hours directly translates into higher maintenance frequencies and accelerated component wear, driving demand across the aerospace repair & operations logistics ecosystem.

Commercial aircraft are accumulating flight hours at an accelerated pace to compensate for constrained fleet availability, with global annual flight hours projected to exceed 112 million by 2035. Rising utilization increases line-replacement unit (LRU) consumption, boosts demand for expendable and rotable parts, and compels airlines and independent MROs to diversify their sourcing relationships across OEM-certified distributors, USM brokers, and PMA suppliers to maintain operational readiness.

Restraints - Supply Chain Disruptions and Extended OEM Lead Times

Global supply chain instability continues to constrain MRO distribution operations. The National Association of Manufacturers found that 78% of aerospace suppliers were confronting raw material shortages as of 2024. Lead times for titanium castings and nickel-alloy forgings used in engine hot sections extended to 12-18 months in 2025, double pre-pandemic levels. Additionally, tariffs reinstated in 2024 have added 25% to the cost of imported aerospace components, placing disproportionate strain on smaller distributors lacking bulk-purchasing capabilities. These disruptions impair inventory management and parts availability planning, ultimately increasing AOG risk for operators.

Shortage of Skilled Aviation Maintenance Technicians

A deepening global shortage of certified aviation maintenance technicians (AMTs) poses a significant structural restraint on the MRO distribution market. Industry projections from Boeing and Airbus indicate a need for over 600,000 additional MRO technicians globally over the next two decades to support fleet growth. This workforce gap not only limits the throughput capacity of MRO facilities, constraining demand for parts distribution, but also inflates labor costs for certified repair stations. The resulting turnaround time delays (engine overhaul turnaround widening to 120-150 days by 2026) force operators into costly spare-engine leasing, indirectly compressing the industrial procurement budgets available for parts sourcing.

Opportunities - E-Commerce and Digital Platform Transformation of MRO Parts Distribution

The digitalization of MRO parts procurement represents one of the most compelling near-term opportunities for distributors willing to invest in digital infrastructure. In April 2025, Satair (an Airbus Services company) expanded its e-commerce platform Satair Market by adding 5 million Airbus proprietary part numbers and associated services, creating a true one-stop shop combining OEM parts, used serviceable material (USM), and surplus parts from third-party sellers. This move reflects the broader industry transition toward digital-first aftermarket services that consolidate inventory management, reduce AOG response times, and enable real-time transparency into parts availability.

According to Satair, 56% of MRO leaders are already prioritizing predictive maintenance solutions, with IoT sensors reducing unplanned removals by up to 15%. Distributors that develop AI-driven demand forecasting, automated reorder systems, and seamless API integration with airline and MRO ERP platforms will secure sustained competitive advantages across the evolving aerospace maintenance supply chain.

Rising USM Adoption as a Cost-Effective Sourcing Opportunity

The accelerating adoption of Used Serviceable Material (USM) presents a significant revenue opportunity for MRO distributors. As airlines and operators seek cost-effective, traceable alternatives to high-priced OEM new parts, particularly for mature platforms, the USM segment is expected to register the highest CAGR of 7.30% through the forecast period. The increasing retirement of mid-generation aircraft, including the Boeing 777, Airbus A330, Boeing 737NG, and Airbus A320ceo, is generating a growing supply of high-quality USM parts.

Satair formalized a tripartite Memorandum of Understanding in 2024 with Airbus Chengdu Lifecycle Services and Hangrun Technology for end-of-life aircraft dismantling and USM distribution, signaling the strategic mainstreaming of USM as a core distribution channel. Distributors that build traceability documentation capabilities, EASA and FAA-compliant USM handling protocols, and digital part provenance tools will be well-positioned to capture growing demand across the industrial procurement landscape.

Category-wise Analysis

Product Type Insights - Engine Components Driving High-Value MRO Distribution Demand

Engine material & components represent the dominant segment within the MRO Distribution market by product type, accounting for approximately 38% of total market revenue. This leadership is driven by the criticality of aircraft engines, which are the most expensive and technically complex subsystems and require frequent inspection, overhaul, and component replacement. The engine overhaul segment alone accounted for approximately 40.7% of the broader aerospace MRO market in 2024. Distributors supporting this segment, including those aligned with CFM International, GE Aerospace, and Pratt & Whitney, benefit from long-term service agreements (LTSAs) and power-by-the-hour contracts that ensure predictable demand.

With thousands of LEAP engines under multi-year service agreements, the engine materials distribution ecosystem is highly stable and recurring. At the same time, Cabin & Interior Components are emerging as the fastest-growing product segment, projected to expand at a CAGR of over 6.8%. This growth is supported by rising airline investments in passenger experience upgrades, premium seating retrofits, and cabin modernization programs, particularly across long-haul and high-density routes, creating new distribution demand streams.

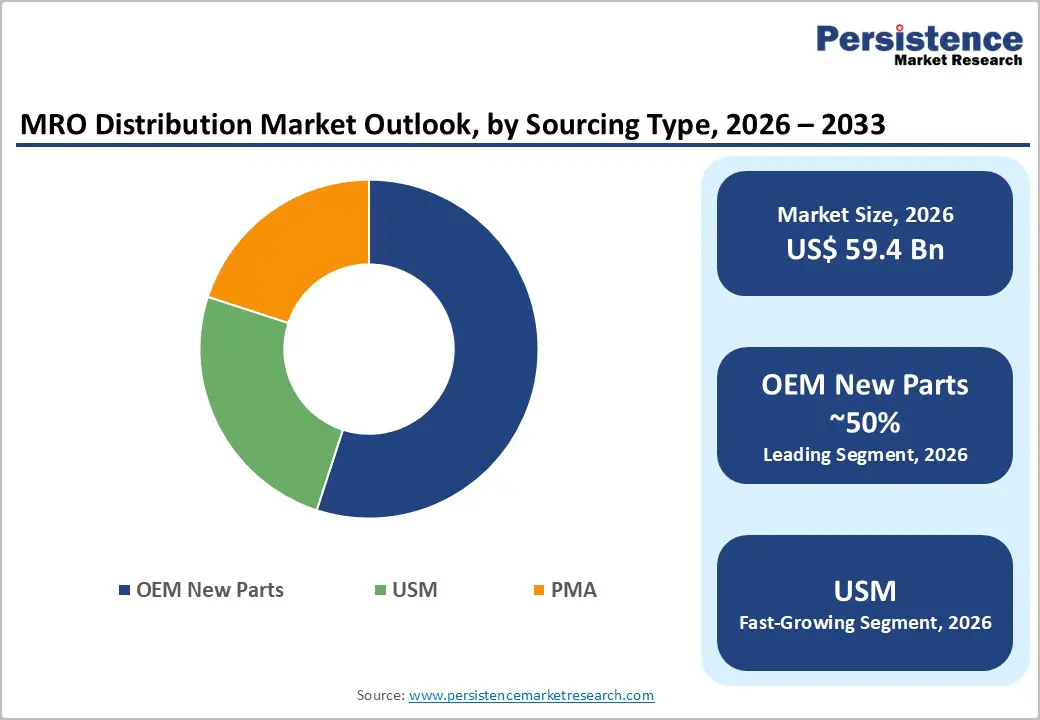

Sourcing Type Insights - OEM Dominance with Rising Cost-Efficient Sourcing Alternatives

OEM New Parts remain the dominant sourcing segment in the global MRO Distribution market, holding approximately 50% of market share. Airlines and operators strongly prefer OEM-certified components for safety-critical systems due to assured compatibility, regulatory compliance, and warranty protection aligned with global aviation standards. Leading OEM-linked distributors such as Satair and Boeing Distribution Services play a crucial role in maintaining supply chain integrity and reliability. This preference is further reinforced by OEM strategies focused on aftermarket capture through integrated service agreements and proprietary parts ecosystems.

Used Serviceable Material (USM) remains the fastest-growing sourcing segment, projected to expand at a CAGR of over 7.3%. This growth is fueled by increasing aircraft retirements, particularly older narrow-body fleets, and the rising need for cost-effective maintenance solutions among airlines seeking to optimize operational expenditures without compromising safety.

Distribution Type Insights - Legacy Distribution Strength with Rapid Digital Transformation

Traditional distribution remains the leading segment by distribution type in the MRO distribution market, accounting for approximately 45% of market revenue. This dominance reflects the aviation industry's reliance on certified supply chains where traceability, documentation, and regulatory compliance are essential. Established distributors maintain a competitive advantage through global warehousing networks, OEM certifications, and 24/7 Aircraft-on-Ground (AOG) support, ensuring operational continuity for airlines. These relationship-driven supply models remain indispensable for delivering mission-critical parts.

Conversely, e-commerce & marketplaces are emerging as the fastest-growing segment, expected to grow at a CAGR of over 6.6%. Digital procurement platforms are transforming the industry by enabling real-time inventory visibility, faster sourcing decisions, and streamlined transactions. Platforms developed by players such as Satair are accelerating adoption, reflecting a broader shift toward digitization and efficiency in aviation supply chain management.

Platform Insights - Narrow-Body Fleet Expansion Sustaining MRO Demand Growth

Narrow-body Jets dominate the platform segment, accounting for approximately 48% of the MRO distribution market by revenue. This is primarily due to the extensive global deployment and high utilization rates of aircraft families such as the Boeing 737 and Airbus A320 family, which serve as the backbone of short-haul and domestic aviation networks. Aging fleets, particularly in North America and Europe, continue to generate strong demand for replacement parts and maintenance services.

Airlines extending aircraft service life beyond 20-25 years are further intensifying demand for rotable and expendable components across the distribution ecosystem.

In parallel, Wide-body Jets are the fastest-growing platform segment, projected to grow at a CAGR of over 6.7%. This growth is driven by the recovery of international air travel, increasing long-haul connectivity, and rising demand for fleet modernization, all of which are boosting maintenance requirements and associated parts distribution.

End-user Insights - Independent MRO Leadership with OEM Service Expansion Momentum

Independent MROs represent the dominant end-user segment in the global MRO Distribution market, accounting for approximately 40% of total revenue. These organizations rely heavily on third-party distributors because they lack direct OEM supply agreements, making them key customers in the aftermarket ecosystem. Their ability to service multiple aircraft platforms at competitive costs makes them attractive to airlines, particularly low-cost carriers seeking flexible maintenance solutions. The increasing outsourcing of maintenance activities, accounting for nearly half of total MRO spending among major airlines, continues to expand the addressable market for independent providers.

OEM-Affiliated MROs are the fastest-growing segment, expected to grow at a CAGR of over 7.1%. OEMs are actively expanding their aftermarket presence through integrated service offerings, digital maintenance platforms, and long-term service agreements, strengthening their position across the value chain and intensifying competition within the MRO distribution landscape.

Regional Insights

North America MRO Distribution Trends

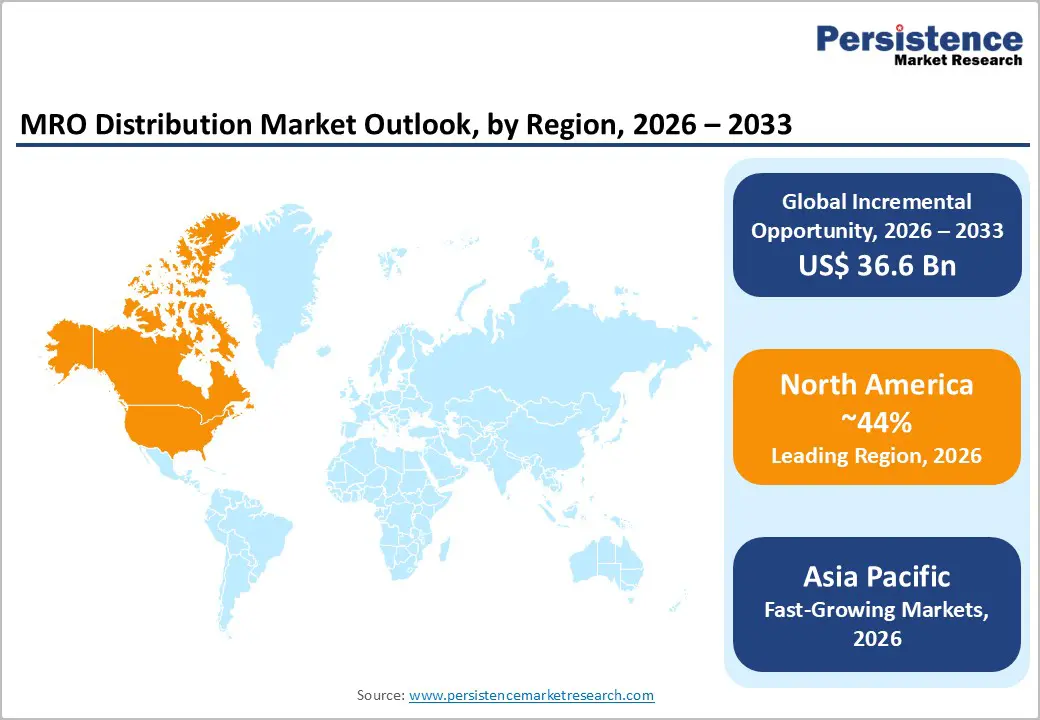

North America is the leading region in the global MRO Distribution market, underpinned by the world's largest commercial and military aircraft fleet, a highly developed MRO infrastructure, and a deep ecosystem of authorized OEM distributors and independent parts brokers. The FAA regulates over 5,000 certificated repair stations across the United States, forming the regulatory backbone for parts sourcing and distribution activity. The U.S. aerospace MRO market was valued at approximately US$ 26.4 Billion in 2026. Key distribution hubs in Atlanta, Dallas, and Chicago serve major airline maintenance supply chain networks.

The region's innovation ecosystem is driving rapid adoption of digital inventory management and predictive parts procurement tools. AAR Corp. which achieved record sales of US$ 2.8 Billion in fiscal year 2025 expanded its new parts Distribution segment with 32% organic growth. The company's acquisition of American Distributors Holding (ADI) in September 2025 and HAECO Americas in November 2025 further solidifies North America's position as the epicenter of MRO distribution consolidation. Regulatory frameworks under FAA Part 145 and FAA Part 21 continue to shape high-quality PMA and OEM parts distribution standards across the region.

Europe MRO Distribution Trends

Europe represents the second-largest MRO distribution region, anchored by the strong aerospace manufacturing and MRO ecosystems of Germany, the United Kingdom, France, and Spain. Germany hosts globally significant MRO distributors and OEM-affiliated service organizations, including Lufthansa Technik AG and Satair's Hamburg distribution hub. The European Union Aviation Safety Agency (EASA) provides the overarching regulatory framework governing parts certification, airworthiness documentation, and distributor approvals across member states driving harmonization that facilitates cross-border parts logistics. The UK, home to AJW Group and historically a global center for USM trading, continues to play a pivotal role in the region's parts distribution ecosystem.

Spain and France contribute significantly through their major MRO facility networks and airline-affiliated maintenance divisions. Air France-KLM Engineering & Maintenance is one of Europe's largest component MRO providers, operating a robust internal supply chain that interfaces with multiple distribution partners. EASA Part 145 approval requirements for repair stations and the REACH regulation governing aerospace chemicals are increasingly influencing distributor product compliance strategies across Europe. Satair's AutoStore automated warehouse system in Hamburg reinforces the region's digital transformation of inventory management, ensuring faster order fulfillment and improved parts availability for MRO operators across the continent.

Asia Pacific MRO Distribution Trends

Asia Pacific is the fastest-growing region in the global MRO Distribution market, driven by rapid fleet expansion, rising air passenger volumes, and increasing investment in domestic MRO capabilities across China, Japan, India, and ASEAN markets. The region accounted for approximately 30.8% of the global aerospace and defense MRO market in 2024. China's rapidly expanding narrow-body fleet, primarily Airbus A320neo and Boeing 737 MAX variants is generating significant aftermarket parts demand. Satair's tripartite USM cooperation agreement with Airbus Chengdu and Guangzhou Hangrun Technology (2024) exemplifies the deepening integration of global distribution networks into the Chinese aerospace maintenance supply chain.

India is emerging as a strategic MRO hub, with the government's Civil Aviation Ministry targeting self-sufficiency in aerospace maintenance to reduce the estimated US$2 billion annual MRO expenditure currently directed overseas. The ASEAN region, particularly Singapore, Thailand, and Malaysia, is attracting large-scale MRO investment backed by bilateral aviation agreements and favorable FDI policies. Satair inaugurated its Singapore AutoStore robotic warehouse in 2025 to serve fast-growing customer demand in Asia Pacific. Japan's well-regulated aviation market, with a large and aging fleet, sustains consistent demand for certified OEM parts distribution and components for its narrow-body and wide-body aircraft operators.

Competitive Landscape

The global MRO distribution market is moderately consolidated, dominated by a blend of OEM-backed distributors and large independent aftermarket specialists competing on reliability, geographic reach, and digital platform capabilities. Key players including Satair (Airbus), AAR Corp., HEICO Aerospace, and Proponent command significant market positions through exclusive OEM distribution agreements and multi-platform service capabilities. Competition increasingly centers on digital enablement, real-time inventory visibility, and e-commerce platforms rather than warehouse size alone.

Strategic acquisitions, long-term service agreements (LTSAs), and vendor-managed inventory (VMI) models are reshaping competitive dynamics, while PMA and USM specialists attract cost-sensitive operators seeking alternatives to full-price OEM parts.

Key Developments:

- In November 2025, AAR Corp. acquired HAECO Americas for approximately US$ 1+ billion (corrected estimate), adding two major heavy maintenance facilities in North Carolina and Florida. The deal also included over US$ 850 million in long-term maintenance contracts, significantly strengthening AAR’s North American MRO and distribution footprint.

- In September 2025, AAR Corp. acquired American Distributors Holding Co. for US$ 146 million, expanding its new parts distribution capabilities. This acquisition enhanced AAR’s OEM product portfolio and broadened its customer base across both commercial aviation and defense aerospace segments.

- In April 2025, Satair, a part of Airbus, expanded its Satair Market digital platform by integrating approximately 5 million Airbus proprietary part numbers. This development created a more comprehensive e-commerce ecosystem, enabling global MRO providers and airlines to source OEM parts, USM, and surplus inventory through a unified digital interface.

Companies Covered in MRO Distribution Market

- AAR Corp.

- AerFin

- AJW Group

- Avtrade

- Boeing

- GA Telesis

- HEICO Aerospace

- Kellstrom Aerospace

- Proponent

- Satair

- Wesco Aircraft/Incora

Frequently Asked Questions

The global MRO Distribution market is valued at US$ 59.4 billion in 2026 and is projected to reach US$ 96 Billion by 2033, growing at a CAGR of 7.1% during the forecast period. Historically, the market grew at a CAGR of 6.3% between 2020 and 2025, supported by fleet expansion, increased aircraft utilization, and rising aftermarket services demand across commercial and defense aviation sectors globally.

The primary growth drivers include a rapidly aging global commercial aircraft fleet with average fleet age rising to 13.4 years in 2025 (per Oliver Wyman) combined with record-high air passenger traffic of 4.9 billion in 2024, as reported by IATA. Extended aircraft life cycles, rising flight hours, OEM production backlogs exceeding 17,000 unfilled orders, and escalating AOG pressures are collectively compelling operators to rely on diversified maintenance supply chain distribution networks.

OEM New Parts is the leading sourcing segment, commanding approximately 50% of the global MRO Distribution market. Airlines and MROs prefer OEM-certified parts for safety-critical systems to ensure regulatory compliance with FAA and EASA airworthiness standards and maintain warranty protection on new-generation platforms. USM is the fastest-growing sourcing segment, projected at a CAGR of 7.30%, as accelerating fleet retirements create a growing supply of cost-effective certified used parts.

North America is the leading region in the global MRO Distribution market, supported by the world's largest commercial and military aircraft fleet, a highly developed network of FAA-certificated repair stations, and dominant distribution players such as AAR Corp. (with fiscal year 2025 revenue of US$ 2.8 Billion) and Boeing Distribution Services. The region holds approximately 33% of global market share, with Asia Pacific emerging as the fastest-growing geography.

The most significant near-term opportunity lies in the digitalization of MRO parts procurement via e-commerce and AI-driven inventory management platforms. Satair Market's addition of 5 million Airbus part numbers in April 2025 demonstrates this trajectory. Simultaneously, the rising adoption of USM is projected at a CAGR of 7.30%, and the rapid growth of the Asia Pacific MRO infrastructure offers substantial long-term revenue opportunities for distributors that combine digital traceability, global logistics networks, and regulatory compliance expertise.

Key players in the global MRO Distribution market include Satair (Airbus), AAR Corp., HEICO Aerospace, Proponent, Boeing Distribution Services (Aviall), Wesco Aircraft/Incora, AJW Group, AerFin, GA Telesis, Kellstrom Aerospace, and Avtrade. These companies compete through OEM distribution exclusivity, digital platform investment, USM capabilities, and global logistics networks.