- Industrial Goods & Service

- Fireproof Insulation Market

Fireproof Insulation Market Size, Share, and Growth Forecast 2026 - 2033

Fireproof Insulation Market by Material Type (Mineral Wool, Fiberglass, Calcium Silicate, Ceramic Fiber, Perlite, Vermiculite, Other), Product Form (Boards & Panels, Blankets & Rolls, Coatings, Foams, Loose Fill Insulation), Temperature Resistance (Below 500°C, 500°C-1,000°C, Above 1,000°C), Application (Walls & Partitions, Roofs & Ceilings, Floors, Pipes & Ducts, Industrial Equipment), End-Use Industry (Residential Construction, Commercial Construction, Industrial, Oil & Gas, Power Generation, Transportation), by Regional Analysis, 2026 - 2033

Fireproof Insulation Market Size and Trend Analysis

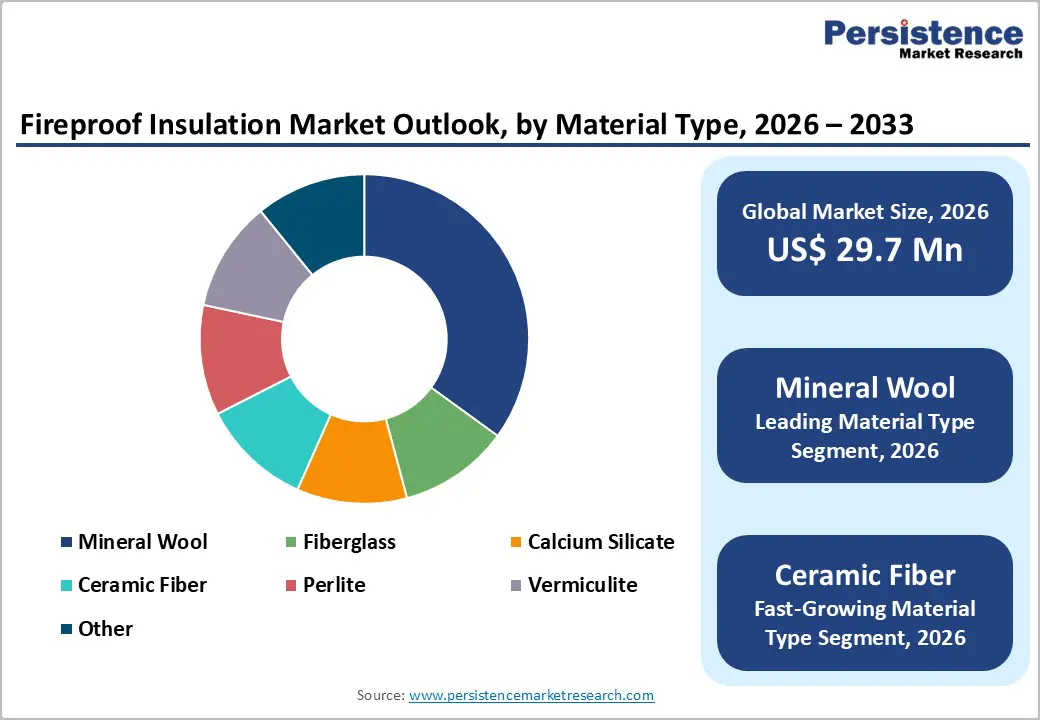

The global fireproof insulation market size is expected to be valued at US$ 29.7 million in 2026 and projected to reach US$ 41.5 million by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The fireproof insulation market is on a sustained growth trajectory, propelled by increasingly stringent global fire safety regulations, accelerating construction activity, and heightened awareness of structural fire risks across commercial and industrial sectors. In the United States, the National Fire Protection Association (NFPA) publishes and enforces building fire safety codes mandating the integration of non-combustible insulation in new construction.

Similarly, the European Union's Construction Products Regulation (EU CPR 305/2011) requires all insulation materials to carry CE marking certifying fire performance classification under EN 13501-1. With global construction investment exceeding US$ 12 trillion annually, demand for certified fireproof insulation for walls, pipes, roofs, and industrial equipment continues to grow steadily, reinforcing the market's consistent expansion.

Key Industry Highlights

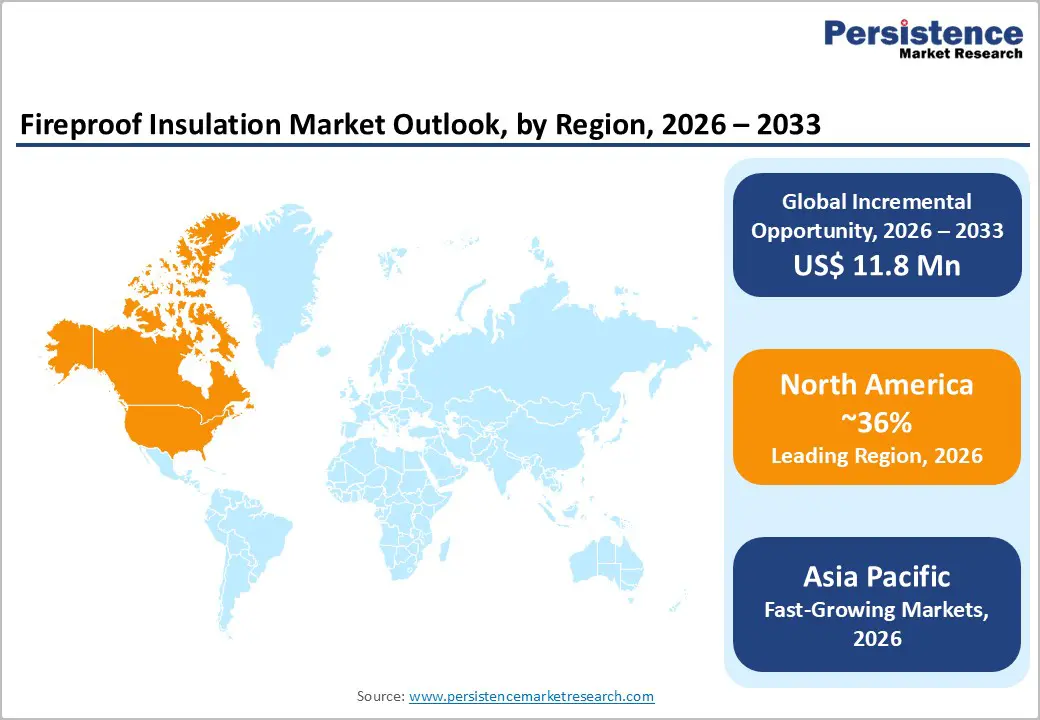

- Leading Region: North America leads the global fireproof insulation market with approximately 36% share in 2025, underpinned by NFPA's 300+ fire codes, the U.S. IBC mandate for fire-rated materials in commercial construction, and the US$ 1.2 trillion IIJA infrastructure spending program driving sustained procurement demand.

- Fastest Growing Region: Asia Pacific is the fastest-growing region in the fireproof insulation market, driven by China's US$ 3.5 trillion annual construction investment, India's Smart Cities Mission, updated national fire codes mandating certified insulation in high-rise projects, and ASEAN industrial expansion accelerating demand through 2033.

- Dominant Segment: Mineral Wool is the dominant material type segment, with approximately 38% market share in 2025, underpinned by its Euroclass A1 non-combustibility under EN 13501-1 and ASTM E136, its melting point exceeding 1,000°C, and its versatile application across residential, commercial, and industrial fire-rated building assemblies globally.

- Fastest Growing Segment: Ceramic Fiber is the fastest-growing material segment in the Fireproof Insulation market, expanding rapidly in high-temperature industrial applications including oil & gas refineries, power plants, and aerospace facilities requiring sustained thermal performance above 1,000°C under continuous operational conditions.

- Key Opportunity: A significant market opportunity lies in dual-certified fire and energy-efficient insulation products, with the USGBC reporting over 108,000 LEED-certified projects globally and the EU EPBD mandating near-zero energy buildings by 2030, creating growing demand for mineral wool and fiberglass solutions meeting both performance criteria.

| Key Insights | Details |

|---|---|

| Fireproof Insulation Market Size (2026E) | US$ 29.7 Million |

| Market Value Forecast (2033F) | US$ 41.5 Million |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics and Market Growth Drivers

Stringent Fire Safety Building Codes and Regulatory Mandates Driving Widespread Adoption

Tightening fire safety regulations across major markets remain the most decisive demand driver for the global fireproof insulation market. In the United States, NFPA 285 governs fire-propagation testing for exterior wall assemblies, effectively mandating non-combustible insulation in mid-rise and high-rise construction. The International Building Code (IBC), adopted in all 50 U.S. states, requires fire-rated insulation for commercial and industrial occupancies. In Europe, Euroclass A1 classification under EN 13501-1 sets the benchmark for complete non-combustibility, with materials such as mineral wool and calcium silicate routinely achieving this top-tier fire rating. A 25% global increase in fire safety code revisions between 2020 and 2024 has accelerated the replacement of legacy insulation with certified fireproof alternatives, driving robust procurement across construction and renovation projects in both developed and developing markets. The UK Building Safety Act 2022, enacted in response to the Grenfell Tower disaster, has fundamentally reshaped specification practices by banning combustible cladding and insulation on all high-rise residential buildings above 18 meters.

Surge in Global Construction Activity and Industrial Infrastructure Investment

Accelerating construction and industrial infrastructure development is driving persistent global demand for fireproof insulation. According to Oxford Economics, global construction output is forecast to reach US$ 15.2 trillion by 2030, with emerging economies in Asia Pacific, the Middle East, and Africa accounting for the majority of incremental growth. The U.S. Infrastructure Investment and Jobs Act (IIJA) of 2021 allocated US$ 1.2 trillion for infrastructure upgrades, a significant portion of which supports fire-safe building systems. In the industrial sector, oil & gas refineries, chemical plants, and power stations are increasingly specifying ceramic fiber and calcium silicate insulation for high-temperature equipment protection. High-rise commercial construction in China, India, UAE, and Southeast Asia is also mandating fireproof insulation under updated national building codes, generating durable, multi-year demand pipelines for market participants.

Market Restraints

Volatility in Raw Material Prices and Supply Chain Disruptions

The fireproof insulation market is significantly exposed to fluctuations in the prices of key raw materials, including silica, basalt rock, calcium silicate, and specialty ceramic fibers. Raw material cost volatility, exacerbated by geopolitical tensions and supply chain disruptions, can increase manufacturing costs by 15-25% during peak periods, compressing margins and disrupting stable product pricing. Currency exchange rate volatility further amplifies procurement challenges for globally sourced inputs. These cost pressures have forced smaller regional manufacturers to reduce output or exit the market, constraining overall supply-side competition and limiting price competitiveness for end users seeking certified fireproof insulation alternatives.

High Initial Cost Premium and Retrofitting Complexity

Fireproof insulation materials command a significant price premium over conventional insulation, with certified mineral wool and ceramic fiber products costing 30-60% more than standard alternatives. This cost differential creates adoption barriers, particularly for price-sensitive residential construction in developing economies and smallholder commercial developers. Retrofitting existing buildings with fire-rated insulation involves substantial material and labor costs, often requiring structural modifications that can increase total project expenditure by 20-40% compared to new-build specifications. These financial hurdles slow market penetration in retrofit-heavy segments, limiting overall adoption rates in older building stocks across North America and Europe.

Market Opportunities

Rapid Growth of Oil & Gas and Power Generation Sectors Driving High-Temperature Insulation Demand

The Oil & Gas and Power Generation industries represent a compelling and fast-expanding opportunity for fireproof insulation manufacturers, particularly for high-temperature products rated above 1,000°C. Global investment in liquefied natural gas (LNG) infrastructure is projected to exceed US$ 120 billion by 2030, according to the International Energy Agency (IEA), and each LNG terminal will require extensive passive fire protection and insulation across piping, storage tanks, and process equipment. The global power generation capacity additions, particularly new gas-fired, nuclear, and hydrogen production plants, are further amplifying demand for ceramic fiber and calcium silicate fireproof insulation products rated above 1,000°C. Promat International (Etex Group) and Morgan Advanced Materials are well positioned to capitalize on this demand with their portfolios of high-temperature passive fire protection solutions, targeting a segment projected to grow at a CAGR above the overall market average between 2026 and 2033.

Green Building Certifications and Energy Efficiency Mandates Creating Dual-Benefit Product Opportunities

The global push for green building certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method) is creating a powerful dual-opportunity for fireproof insulation suppliers. Buildings certified under these frameworks are required to incorporate materials that simultaneously provide fire resistance and superior thermal performance, criteria that mineral wool, fiberglass, and calcium silicate products intrinsically satisfy. The U.S. Green Building Council (USGBC) reports over 108,000 LEED-certified projects globally as of 2024, with the pipeline growing at approximately 8% per year. Kingspan Group and Knauf Insulation are actively aligning product development with LEED and BREEAM specifications. The North American Insulation Manufacturers Association (NAIMA) further reports that fiberglass and mineral wool insulation can reduce heating and cooling energy consumption by up to 40%, making dual-certified products increasingly attractive across both new construction and deep retrofitting projects globally.

Category-wise Insights

Material Type Analysis

Mineral Wool is the leading material type in the fireproof insulation market, commanding approximately 38% of total market share in 2025. Mineral wool, encompassing stone wool (rockwool) and slag wool, earns its market leadership through its inherent non-combustibility, with a melting point exceeding 1,000°C and certification to Euroclass A1 under EN 13501-1 and ASTM E136 in the United States, the highest achievable fire performance classifications globally. Rockwool International A/S alone reported revenues exceeding EUR 3.5 billion in 2024, with fire-rated stone wool accounting for a dominant share. Mineral wool is versatile across residential, commercial, and industrial applications in walls, roofs, pipes, and duct systems, while providing simultaneous thermal and acoustic insulation. Ceramic Fiber is the fastest-growing material segment, driven by escalating demand from industrial high-temperature applications in oil & gas, power generation, and petrochemical processing above 1,000°C.

Product Form Analysis

Boards & Panels represent the leading product form in the fireproof insulation market, capturing approximately 36% of total market share in 2025. Their dominance is rooted in structural versatility; boards and panels can be precisely dimensioned and installed across wall, ceiling, floor, and partition assemblies, making them the preferred specification for architects and fire engineers seeking predictable, code-compliant fire ratings. Calcium silicate boards achieve fire resistance ratings of up to 4 hours under ASTM E119 and EN 1364 testing standards. Promat International (Etex Group) and Morgan Advanced Materials are leading suppliers of certified fireproof boards for industrial and commercial applications. Coatings (intumescent) are the fastest-growing product form, offering application flexibility for retrofitting structural steel and complex geometries where rigid board installation is impractical.

Temperature Resistance Analysis

The 500°C-1,000°C temperature resistance range is the leading segment in the fireproof insulation market, representing approximately 45% of total market share in 2025. This range encompasses the broadest spectrum of commercial and industrial applications, including HVAC ductwork, industrial piping, and high-rise building partitions, making it the most versatile and widely specifiable performance tier. Mineral wool maintains structural integrity at temperatures up to 1,000°C, and fiberglass withstands temperatures up to approximately 540°C without combustion, collectively covering the majority of commercial and mid-temperature industrial use cases. The Above 1,000°C segment is the fastest-growing temperature resistance category, driven by expanding oil & gas refinery construction, aerospace applications, and next-generation high-temperature industrial processes globally.

Application Analysis

Walls & Partitions is the dominant application segment in the fireproof insulation market, accounting for approximately 33% of total market share in 2025. Fire-rated wall and partition assemblies are mandated in commercial and high-rise residential construction across all major regulatory jurisdictions, driven by the International Building Code (IBC) and its global equivalents. Fire compartmentalization standards require that internal walls achieve a minimum 60-minute to 120-minute fire resistance rating, compelling builders to incorporate certified mineral wool, fiberglass, or calcium silicate insulation within partition systems. Modern office towers, hospitals, schools, and residential apartment complexes universally specify fire-rated wall insulation as a structural requirement. Pipes & Ducts is the fastest-growing application segment, driven by oil & gas infrastructure expansion and stricter fire safety standards for mechanical systems globally.

End-Use Industry Analysis

The Industrial end-use segment leads the fireproof insulation market , representing approximately 30% of total market share in 2025. Industrial facilities, including manufacturing plants, refineries, chemical processing plants, and power stations, impose the most demanding fire protection requirements, necessitating high-performance insulation products rated for extreme thermal and mechanical stress. The U.S. Occupational Safety and Health Administration (OSHA) and international equivalents mandate passive fire protection for industrial equipment, piping, and structural steelwork in all process industries. Major oil & gas operators and industrial developers specify calcium silicate and ceramic fiber products for process equipment insulation at temperatures exceeding 500°C. The Oil & Gas segment is the fastest-growing end-use industry, driven by global energy infrastructure investment and stringent passive fire protection specifications across LNG, refining, and upstream facilities.

Regional Insights

North America Fireproof Insulation Market Trends and Insights

North America leads the global fireproof insulation markett with approximately 36% market share in 2025, anchored by the United States' comprehensive regulatory framework, robust construction pipeline, and a mature industrial base demanding passive fire protection solutions. The NFPA publishes over 300 fire safety codes and standards, including NFPA 285 and NFPA 13 for fire sprinkler systems, mandating certified non-combustible insulation across new commercial, industrial, and high-rise residential construction. The U.S. housing market added approximately 1.4 million new housing units in 2024 alone, each requiring code-compliant fire-rated insulation. The U.S. Infrastructure Investment and Jobs Act (IIJA)'s US$ 1.2 trillion spending program further reinforces demand for fireproof insulation in public infrastructure projects including tunnels, transit hubs, and government facilities.

Innovation is a defining strength of the North American market. Owens Corning launched its Pure Safety® high-performance mineral wool insulation in 2024, providing fire protection alongside enhanced air quality and acoustic performance, made with at least 65% recycled content. Johns Manville continues to expand its mineral wool range across commercial and industrial distribution channels. The NAIMA estimates fiberglass and mineral wool fireproof insulation reduces building energy consumption by up to 40%, making them dual-compliant with fire codes and energy efficiency mandates, reinforcing their adoption in the world's most regulatory-intensive building market.

Europe Fireproof Insulation Market Trends and Insights

Europe holds the second-largest share of the global fireproof insulation market , driven by some of the world's most stringent fire performance standards, a mature renovation pipeline, and a deep commitment to sustainable construction. The EU Construction Products Regulation (CPR 305/2011) requires CE marking for all insulation products across member states, with fire performance classified under EN 13501-1. Germany's DIN 4102 building fire safety standards and the UK Building Safety Act 2022, enacted following the Grenfell Tower disaster, have fundamentally reshaped national specification practices, banning combustible insulation on all high-rise residential buildings above 18 meters in height.

France, Spain, and Germany are key markets where aging commercial building stock is being retrofitted with certified mineral wool and fiberglass fireproof insulation. Rockwool International A/S announced a major European capacity expansion investment targeting stone wool production in 2024-2025 to meet growing regional demand. Saint-Gobain ISOVER and Knauf Insulation hold particularly strong positions in the European commercial construction segment. The EU's Energy Performance of Buildings Directive (EPBD) revision mandating near-zero energy new buildings by 2030 further incentivizes the use of dual-performing fire and thermal insulation materials across all European markets.

Asia Pacific Fireproof Insulation Market Trends and Insights

Asia Pacific is the fastest-growing region, projected to register the highest CAGR between 2026 and 2033, propelled by rapid urbanization, high-rise construction growth, and increasingly stringent adoption of national fire safety codes across China, India, Japan, and the ASEAN bloc. China remains the world's largest construction market by volume, with the country investing over US$ 3.5 trillion annually in real estate, infrastructure, and industrial facilities. The China National Standard GB 50045 mandates fire-resistant insulation in high-rise commercial buildings, and updated national building codes now require Euroclass A1 equivalents for facade and partition insulation in high-rise projects.

India's construction sector, driven by the Smart Cities Mission and the PM Gati Shakti National Master Plan, is accelerating industrial and commercial building starts at a pace requiring expanded fireproof insulation specification. Japan's Building Standards Law enforces rigorous fire resistance testing for all classified building occupancies. ASEAN nations, including Vietnam, Indonesia, and Thailand, are progressively adopting ISO 9705 and equivalent fire performance testing requirements for commercial facilities. Kingspan Group and BASF have expanded their Asia Pacific manufacturing and distribution footprints to capture growing regional demand, while local manufacturers benefit from lower production costs and improving technical capabilities.

Competitive Landscape

The global fireproof insulation market exhibits a moderately consolidated structure, with several multinational manufacturers accounting for a substantial share of global supply while regional producers serve price-sensitive and localized construction markets. Large companies maintain competitive advantages through extensive product portfolios that meet internationally recognized fire safety certifications and building standards. Strong distribution networks, established relationships with contractors and construction firms, and technical support capabilities further strengthen their market positioning.

Business strategies across the industry increasingly emphasize product innovation, sustainability, and integrated fire protection solutions. Manufacturers are investing in advanced materials such as bio-soluble fibers, improved mineral wool formulations, and environmentally responsible manufacturing processes to meet evolving regulatory and environmental requirements. Companies are also shifting toward system-based offerings, where insulation products are designed as part of complete fire-rated wall and structural assemblies. Digital tools supporting product certification, building information modeling (BIM), and compliance documentation are becoming important competitive differentiators. Meanwhile, regional suppliers, particularly in Asia Pacific, often compete through cost efficiency, while producers in Europe and North America focus on regulatory compliance, product performance, and sustainability leadership.

Key Developments

- February, 2026: Sprayman announced that its Spraycoat Thermal & Sound Insulation Spray Foam achieved ASTM-E84 Class A fire rating certification, confirming compliance with the highest fire-safety standards while providing strong thermal performance for residential and commercial insulation applications.

- October, 2025: ROCKWOOL introduced its new FirePro fire-stopping product range developed at its global centre of excellence in Birmingham, including coated batt, sealants, collars, and wraps designed to meet upcoming fire-resistance standards and strengthen building safety compliance.

Companies Covered in Fireproof Insulation Market

- Armacell International S.A.

- BASF SE

- Fletcher Insulation

- Huntsman International LLC

- Isover (a division of Saint-Gobain)

- Johns Manville (a Berkshire Hathaway company)

- Kingspan Group plc

- Knauf Insulation GmbH

- Morgan Advanced Materials plc

- Owens Corning

- Rockwool International A/S

- Saint-Gobain ISOVER

- 3M Company (Fire Protection Products Division)

- Unifrax LLC

- Etex Group

Frequently Asked Questions

The global Fireproof Insulation market is estimated to reach US$ 29.7 million in 2026, driven by stricter fire safety regulations and increasing adoption of fire-resistant insulation in construction and industrial sectors.

Key demand drivers include tightening fire safety building codes, growing global construction activity, stricter restrictions on combustible materials, and increasing demand for passive fire protection in industrial infrastructure.

North America leads the Fireproof Insulation market, supported by stringent fire safety standards, widespread adoption of building codes, and strong residential and commercial construction activity.

A key growth opportunity lies in fire-resistant insulation solutions that also meet green building and energy efficiency standards, particularly in new construction and retrofit projects.

Key players include Rockwool International A/S, Owens Corning, Saint-Gobain, Knauf Insulation, Kingspan Group plc, Johns Manville, Promat International, Morgan Advanced Materials plc, and BASF SE.