- Hardware & Software IT Services

- Finite Element Analysis Market

Finite Element Analysis Market Size, Share, and Growth Forecast 2026 - 2033

Finite Element Analysis Market by Deployment (On Premises, On Cloud), Component (Software, Services), Enterprise Size (Large Enterprises, SMEs), Application (Structural Analysis, Thermal Analysis), and Regional Analysis 2026 - 2033

Finite Element Analysis Market Size and Trends Analysis

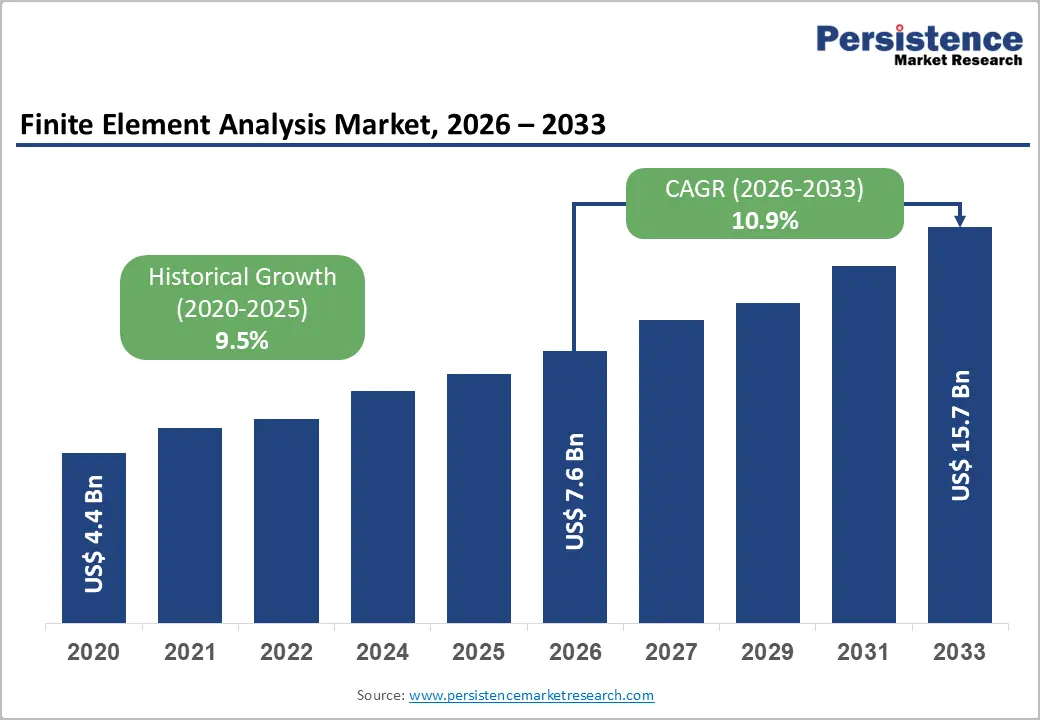

The global finite element analysis market size is likely to be valued at US$7.6 billion in 2026 and is projected to reach US$15.7 billion by 2033, growing at a CAGR of 10.9% during the forecast period from 2026 to 2033, driven by the increasing adoption of virtual prototyping across the automotive and aerospace industries, where manufacturers are focusing on lightweight design optimization and compliance with stringent regulatory standards.

The market is also undergoing a notable transformation as artificial intelligence (AI) and machine learning (ML) are integrated into simulation processes, enabling faster design validation, improved predictive capabilities, and more efficient engineering workflows. In addition, the growing use of lightweight materials in electric vehicles (EVs) and aerospace components is accelerating demand for advanced structural, thermal, and multiphysics analysis solutions to ensure performance reliability, safety, and regulatory compliance.

Key Industry Highlights:

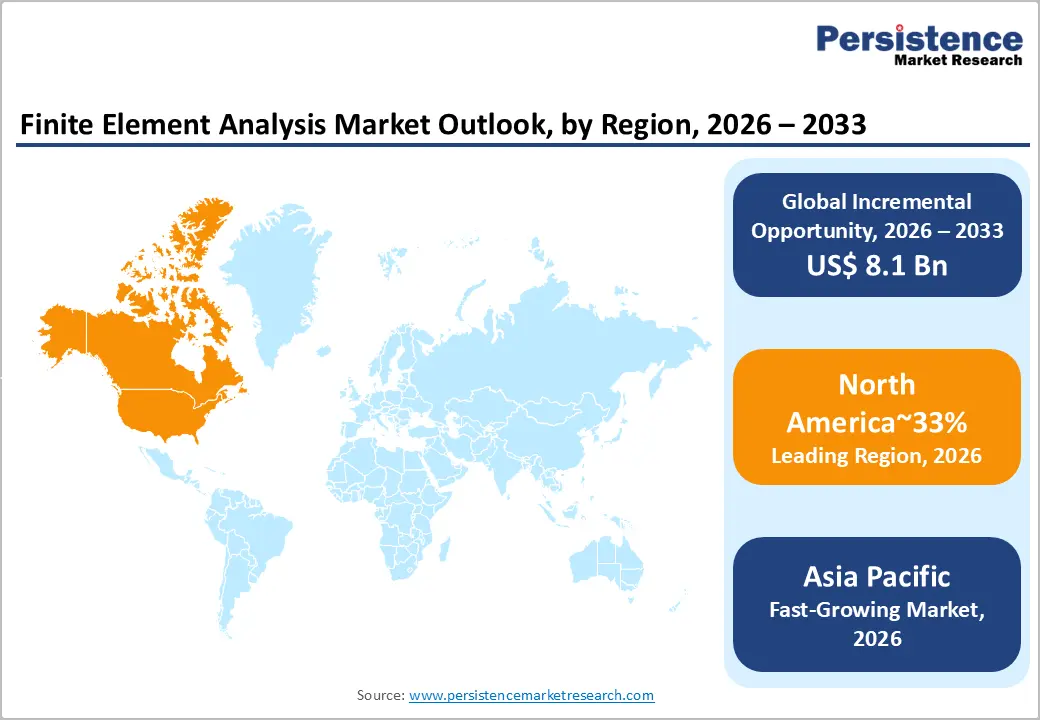

- Leading Region: North America is projected to lead due to intensive R&D investments in the aerospace, defense, and semiconductor sectors, accounting for approximately 33% share in 2026, supported by advanced software adoption, digital twin integration, and a mature innovation ecosystem.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to rapid industrialization, electric vehicle manufacturing expansion, government-backed digital manufacturing initiatives, and rising adoption of simulation tools among SMEs.

- Leading Deployment Type: On-cloud deployment is projected to dominate for simplicity, scalability, adoption, and functional use across engineering enterprises, holding approximately 40% share in 2026.

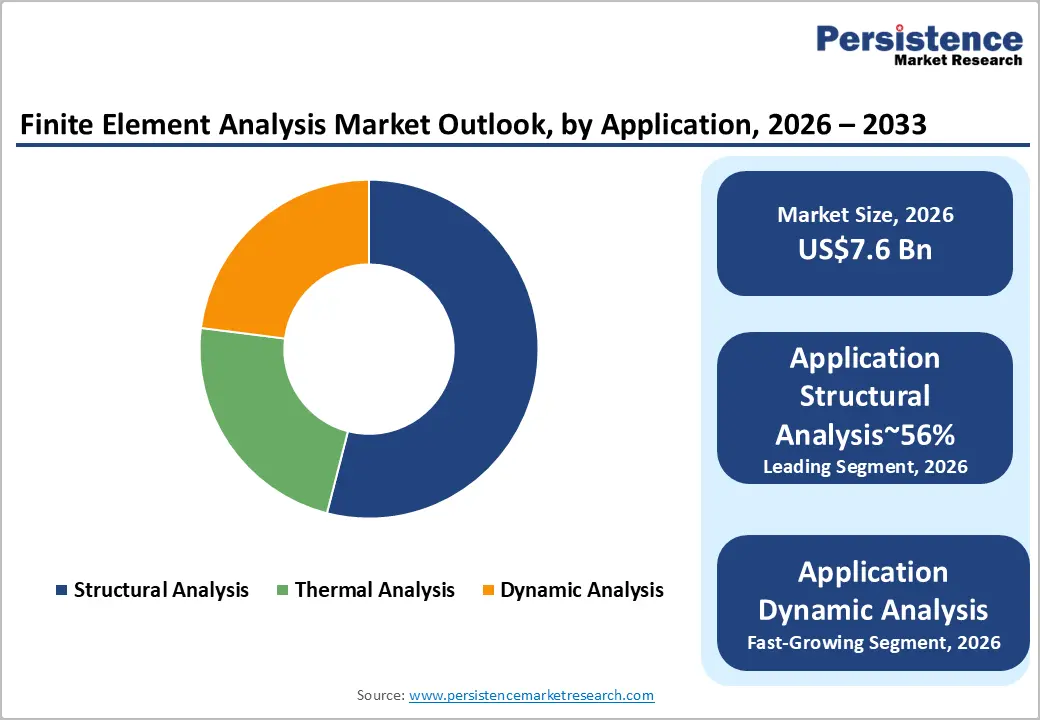

- Leading Application: Structural analysis is expected to lead accounting with approximately 56% share through infrastructure, civil, and industrial engineering adoption, throughput, accuracy, and high-value design applications.

- Key Opportunity: AI-driven simulation and digital twin deployment present a major opportunity. Integration of machine learning into simulation workflows supports faster design iteration and opens new demand across electric mobility and Asia-centric manufacturing expansion. In January 2024, ANSYS launched Ansys 2024 R1 with enhanced AI-driven simulation capabilities. This update improves predictive accuracy and reduces design iteration time, enhancing engineering efficiency on complex projects.

| Key Insights | Details |

|---|---|

|

Finite Element Analysis Market Size (2026E) |

US$7.6 Bn |

|

Market Value Forecast (2033F) |

US$15.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Integration of AI-Driven Simulation and Generative Design as a Structural Growth Driver

The integration of artificial intelligence into finite element analysis platforms is redefining how simulation is applied across engineering workflows, positioning it as a primary growth driver for the FEA market. AI-enabled solvers increasingly leverage historical simulation datasets to predict outcomes, prioritize critical parameters, and reduce computational intensity in complex multiphysics environments. This shifts FEA from a specialist-led, time-intensive process toward a more accessible and iterative design capability that can be used earlier in product development cycles. Generative design further amplifies this impact by enabling engineers to define functional constraints and performance objectives, while the software autonomously generates optimized geometries.

Parallel advances in cloud computing and high-performance simulation infrastructure reinforce this driver by enabling scalable access to advanced FEA tools across distributed engineering teams. The integration of AI and machine learning into meshing, parameter optimization, and validation workflows aligns with regulatory acceptance of virtual testing frameworks, particularly in the aerospace and defense sectors. As simulation becomes embedded within digital certification and compliance strategies, FEA evolves from a design support function into a core decision-making system, sustaining long-term market expansion driven by innovation velocity rather than incremental efficiency gains.

Skills Gap and Operational Complexity as a Structural Market Restraint

The adoption of advanced FEA platforms remains structurally constrained by the high level of technical expertise required to deploy and interpret simulations accurately. Effective use of FEA demands strong proficiency in applied physics, numerical methods, boundary condition modeling, and mesh optimization, skills that are unevenly distributed across engineering teams. This complexity slows implementation timelines, as organizations must align software deployment with workforce upskilling, internal validation protocols, and cross-functional coordination between design, testing, and compliance teams. In cloud-based environments, added concerns around data governance and cybersecurity further complicate onboarding, particularly for regulated industries such as aerospace and defense.

The persistent shortage of qualified simulation specialists amplifies this restraint by limiting the depth of utilization after software acquisition. Many enterprises face a mismatch between licensed FEA capacity and actual productive use, resulting in unrealized efficiency gains and extended ROI horizons. These constraints collectively translate into delayed project timelines and cautious expansion of simulation workloads, moderating overall market growth despite strong technological progress. As a result, skills availability and operational complexity remain material brakes on broader FEA penetration, especially outside large, simulation-mature organizations.

AI and Cloud Convergence as a High-Impact Growth Catalyst

The convergence of artificial intelligence with cloud-based FEA platforms is reshaping how simulation is adopted, scaled, and monetized across industries. AI-enhanced solvers and ML-assisted workflows materially reduce simulation turnaround times by learning from historical datasets, enabling faster convergence in complex multiphysics environments and supporting digital twin development across product lifecycles. Cloud deployment removes traditional infrastructure constraints, allowing organizations to elastically scale compute resources while shifting simulation spend toward subscription-based operating models. This combination is particularly transformative for small and mid-sized enterprises, enabling them to access advanced FEA capabilities without large upfront hardware investments or specialized in-house infrastructure.

AI-driven automation in meshing, parameter optimization, and scenario exploration lowers skill barriers and increases simulation throughput, aligning well with the development of electric mobility, smart manufacturing, and high-iteration design cycles. As enterprises increasingly integrate simulation into continuous engineering workflows rather than discrete validation steps, AI-enabled cloud FEA positions itself as a foundational layer for scalable, data-driven product development, supporting sustained market expansion across both mature and high-growth regions.

Category-wise Analysis

Deployment Type Insights

On-premises deployment is expected to lead, accounting for approximately 60% of the market share in 2026, supported by its entrenched role in data-sensitive engineering environments across the aerospace, defense, and automotive industries. Large enterprises with established high-performance computing infrastructure prioritize on-premises systems to maintain strict control over proprietary simulation models, reduce latency, and ensure secure management of intellectual property. The segment continues to benefit from the reliability and throughput required for large-scale multiphysics simulations used in product development and validation cycles. Vendors such as Ansys, Siemens, and Dassault Systèmes strengthen enterprise deployments through platforms including Ansys Fluent, Simcenter STAR-CCM+, and SIMULIA, embedding advanced automation and AI-assisted solvers to sustain long-term workflow integration within established engineering environments.

Cloud deployment is expected to be the fastest-growing segment, driven by increasing demand for scalable computing resources and flexible collaboration across distributed engineering teams. Cloud-based SaaS architectures enable organizations to access high-performance simulation environments without the capital investment associated with dedicated HPC infrastructure. This shift is being accelerated by advances in elastic computing, remote workflow orchestration, and browser-based simulation platforms that significantly lower entry barriers for smaller design teams. Providers such as Autodesk, Siemens, and Rescale are expanding their cloud-native offerings, including Autodesk CFD Cloud, Simcenter Cloud HPC, and Rescale’s simulation platform, to support distributed product development. As interoperability, AI-driven optimization, and digital engineering ecosystems mature, cloud deployments are positioned to capture accelerating adoption across modern simulation workflows.

Application Insights

Structural analysis is expected to lead the market, accounting for approximately 54% share in 2026, supported by its foundational role in validating durability, fatigue resistance, and load-bearing performance across engineering workflows. Adoption remains deeply embedded within automotive crash simulation, civil infrastructure stress testing, and aerospace fuselage design, where precise load and deformation modeling are essential before physical prototyping. Enterprises prioritize structural simulation for its ability to reduce development cycles while ensuring compliance with rigorous safety and reliability standards. Vendors such as Ansys, Siemens, and Dassault Systèmes reinforce this segment through platforms such as Ansys Mechanical, Simcenter 3D, and Abaqus, integrating automation, nonlinear solver capabilities, and multiphysics coupling to sustain high-volume simulation environments and long-established engineering validation workflows.

Thermal analysis is expected to be the fastest-growing segment, driven by escalating thermal management challenges across next-generation electronics and electrified mobility platforms. Increasing power density in EV battery systems, high-performance computing hardware, and 5G infrastructure has intensified the need for precise heat transfer modeling and cooling optimization. Advanced simulation capabilities now allow engineers to evaluate conduction, convection, and radiation effects simultaneously, improving design accuracy and reducing overheating risks in compact systems. Technology providers such as Ansys, Altair Engineering, and COMSOL are expanding thermal simulation toolsets within multiphysics environments to address complex electro-thermal interactions. As digital prototyping, AI-assisted optimization, and high-fidelity electronics modeling advance, the adoption of thermal analysis is accelerating across modern product design ecosystems.

Regional Insights

North America Finite Element Analysis Market Trends

North America, with an estimated 33% share in 2026, is expected to be the leading regional market. This position is underpinned by intensive R&D investment in aerospace, defense, and semiconductor sectors and is expected to be the leading market region. The region benefits from a mature innovation ecosystem, where high-fidelity simulation is integral to engineering, product certification, and rapid prototyping. Market behavior emphasizes the adoption of advanced software platforms and integration with digital twin and cloud-based simulation workflows.

The U.S. anchors regional leadership, hosting major FEA providers such as Ansys and Altair. Strong collaboration with aerospace and defense contractors, including NASA and Lockheed Martin, drives continuous demand for precision modeling. Coupled with regulatory frameworks that favor virtual testing and simulation-based certification, the U.S. ensures sustained adoption of cutting-edge FEA technologies, securing North America’s position as the global hub for advanced engineering simulation.

Asia Pacific Finite Element Analysis Market Trends

Asia Pacific is expected to be the fastest-growing regional market. The region is projected to witness accelerated adoption as China, India, and Japan expand their manufacturing, automotive, and infrastructure sectors. Growth is estimated to be driven by China’s ambitious electric vehicle programs, high-speed rail projects, and industrial automation initiatives, all of which require high-fidelity structural, thermal, and fluid dynamic simulations. India is forecasted to strengthen its position as a global engineering services hub, with increasing investments in simulation centers of excellence, advanced engineering training, and software deployment across multiple industries. Japan’s mature automotive and electronics sectors are projected to drive ongoing demand for precision simulation solutions to enhance product quality, reliability, and energy efficiency.

China is expected to lead regional adoption by leveraging government-backed smart manufacturing initiatives, digitalization incentives, and robust industrial infrastructure. The proliferation of advanced manufacturing and construction projects across the region is forecasted to generate substantial opportunities for FEA software vendors and service providers. Regulatory support, technology localization, and skill development initiatives are expected to reinforce Asia Pacific’s rapid market expansion.

Asia Pacific Finite Element Analysis Market Trends

Asia Pacific is expected to represent the fastest-growing regional market. The region is projected to witness accelerated adoption as China, India, and Japan expand their manufacturing, automotive, and infrastructure sectors. Growth is estimated to be driven by China’s ambitious electric vehicle programs, high-speed rail projects, and industrial automation initiatives, all of which require high-fidelity structural, thermal, and fluid dynamic simulations. India is forecasted to strengthen its position as a global engineering services hub, with increasing investments in simulation centers of excellence, advanced engineering training, and software deployment across multiple industries. Japan’s mature automotive and electronics sectors are projected to drive ongoing demand for precision simulation solutions to enhance product quality, reliability, and energy efficiency.

China is expected to lead regional adoption by leveraging government-backed smart manufacturing initiatives, digitalization incentives, and robust industrial infrastructure. The proliferation of advanced manufacturing and construction projects across the region is forecasted to generate substantial opportunities for FEA software vendors and service providers. Regulatory support, technology localization, and skill development initiatives are expected to reinforce Asia Pacific’s rapid market expansion.

Europe Finite Element Analysis Market Trends

Europe is projected to be the second-largest regional market. Adoption is expected to be sustained as the automotive and industrial manufacturing sectors continue to integrate simulation-led design for efficiency and compliance. Investment in virtual testing and Industry 4.0 technologies is estimated to accelerate, supporting digital twin initiatives, IoT integration, and precision engineering workflows.

Germany is projected to lead the region, hosting major automotive manufacturers and engineering firms, driving demand for crash safety and emissions optimization simulations. Regulatory frameworks, including Euro 7 emissions standards, are expected to continue driving design optimization, promoting advanced FEA adoption. Europe is forecasted to remain a hub for high-quality engineering simulation solutions throughout the projection period, with continued focus on compliance, energy efficiency, and manufacturing process digitalization.

Competitive Analysis

The global finite element analysis market is moderately consolidated, with the top five players, ANSYS, Dassault Systèmes, Siemens, Autodesk, and Altair, holding approximately 55–60% of the total market share. ANSYS leads the market, followed by Dassault and Siemens, leveraging comprehensive multiphysics platforms and strong enterprise adoption. The remaining share is fragmented among niche specialists such as COMSOL, focusing on civil, geotechnical, or domain-specific simulations. Competitive positioning emphasizes AI integration, cloud-enabled workflows, and end-to-end platform capabilities that unify CAD, CAE, and PLM functions.

Business strategies focus on platformization, AI-enabled solvers, cloud partnerships with hyperscalers, consumption-based licensing, and regional expansion, particularly in Asia, with trends toward subscription models, digital twins, and integrated multiphysics solutions driving differentiation. In September 2024, Altair partnered with LG Electronics for AI-powered FEA in consumer products. This collaboration accelerates product development cycles, improving durability testing and market responsiveness.

Key Industry Developments:

- In June 2025, Siemens expanded the Simcenter portfolio with AI-enhanced fatigue analysis, improving predictive maintenance in manufacturing and potentially reducing downtime by 20–30%.

- In November 2024, Hexagon (MSC Software) launched MSC Nastran 2024.2 with quantum-inspired optimizations, improving computational efficiency for large-scale simulations and supporting high-performance computing in defense.

- In July 2024, Dassault Systèmes released Abaqus 2024 with enhanced nonlinear analysis capabilities, strengthening material modeling for sustainable designs and helping industries such as energy meet regulatory requirements.

- In May 2024, Autodesk acquired Wonderdyn to strengthen Fusion 360’s FEA capabilities with cloud-based simulation tools, expanding access for SMEs and enabling more collaborative design with lower hardware dependence.

Companies Covered in Finite Element Analysis Market

- ANSYS Inc.

- Dassault Systèmes

- Siemens Digital Industries

- Altair Engineering

- Hexagon AB (MSC Software)

- Autodesk Inc.

- COMSOL AB

- ESI Group

- PTC Inc.

- Bentley Systems

- Synopsys Inc.

- SimScale GmbH

- Dlubal Software

- NEi Software

- Convergent Science

- Dlubal Software

Frequently Asked Questions

The global finite element analysis market is projected to be valued at US$7.6 billion in 2026 and is expected to reach US$15.7 billion by 2033, reflecting rising reliance on advanced simulation tools across engineering-intensive industries.

Adoption is accelerating due to increasing regulatory and design complexity, rising need to reduce physical prototyping costs, and growing use of high-fidelity simulation in aerospace, automotive, energy, electronics, and defense manufacturing workflows.

The finite element analysis market is expected to grow at a CAGR of 10.9% between 2026 and 2033, supported by cloud-based deployment, AI-driven simulation, and digital twin integration.

The fastest growth opportunities are emerging in Asia Pacific, driven by rapid industrialization, electric vehicle manufacturing expansion, government-backed digital manufacturing initiatives, and rising adoption of simulation tools among SMEs.

Key players include ANSYS Inc., Dassault Systèmes, Siemens Digital Industries Software, Altair Engineering, Hexagon AB (MSC Software), Autodesk Inc., COMSOL AB, ESI Group, PTC Inc., Bentley Systems, Synopsys Inc., SimScale GmbH, Dlubal Software, and Convergent Science.