- Plastics, Polymers & Resins

- Polyurethane Elastomers Market

Polyurethane Elastomers Market Size, Share, and Growth Forecast, 2026 - 2033

Polyurethane Elastomers Market by Product Type (Thermoplastic Polyurethane, Thermoset/Cast Polyurethane, Others), Application (Furniture, Automotive & Transportation, Others), Process, End-use Industry, and Regional Analysis for 2026 - 2033

Polyurethane Elastomers Market Size and Trends Analysis

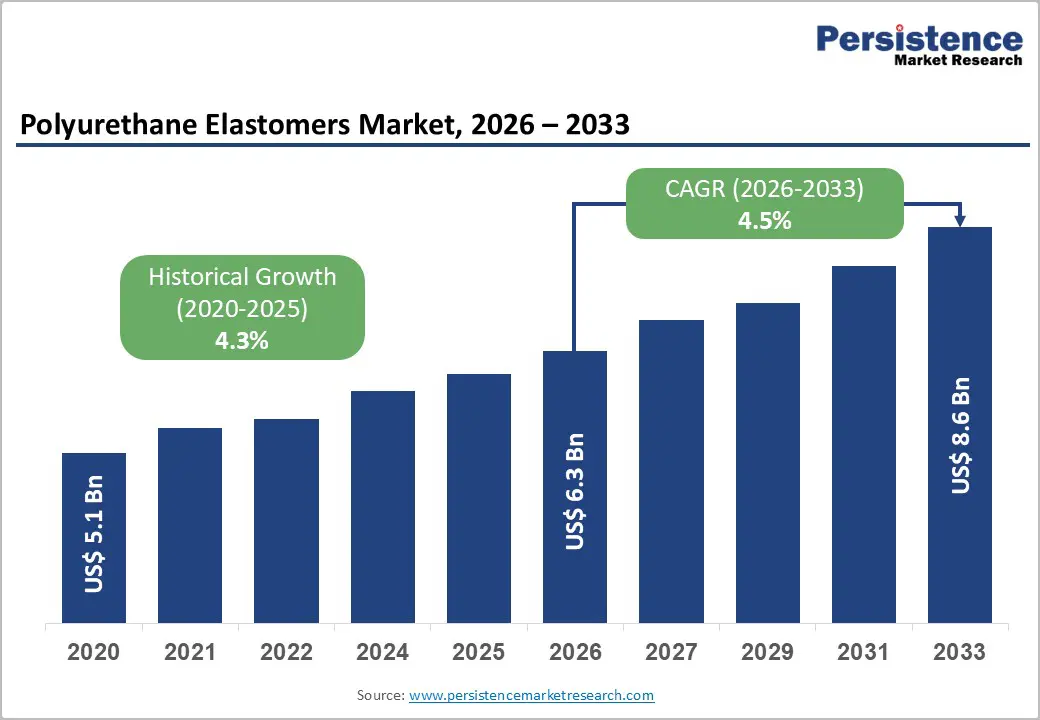

The global polyurethane elastomers market size is likely to be valued at US$6.3 billion in 2026 and is expected to reach US$8.6 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033, driven by increasing demand for lightweight, durable, and high-performance materials across automotive, construction, and consumer applications.

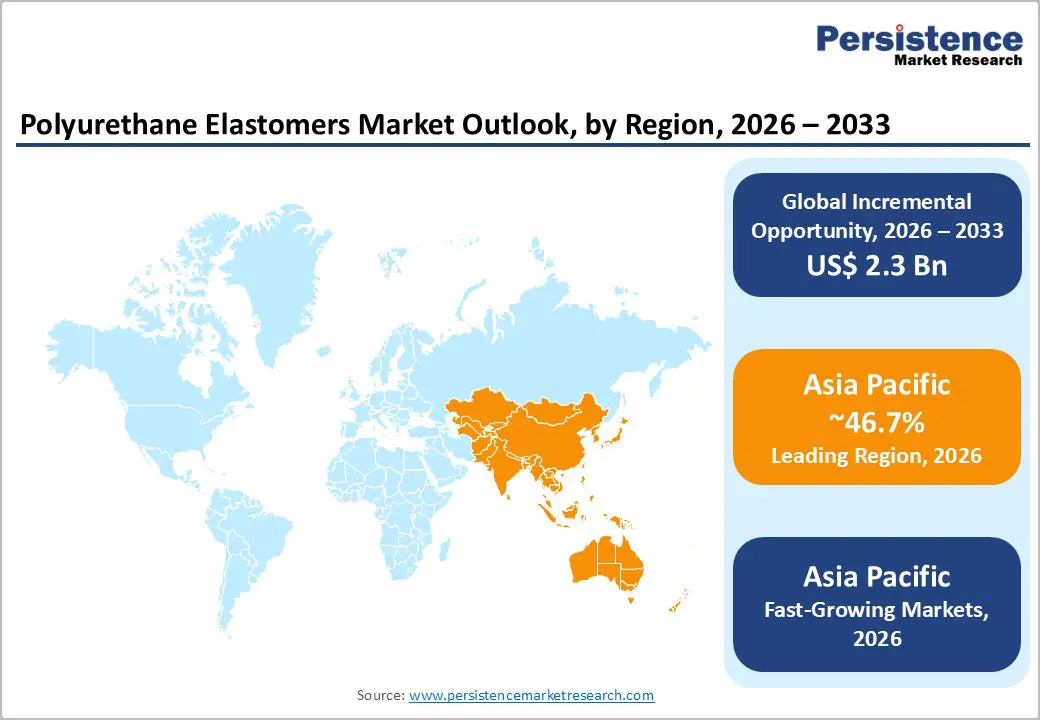

Asia Pacific dominates the global landscape, supported by strong manufacturing output and infrastructure growth. Sustainability-driven reformulation and stricter regulatory compliance are also accelerating the transition toward traceable, low-emission polyurethane elastomer solutions.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to account for approximately 46.7% of the market share, driven by strong manufacturing capabilities, automotive production, and infrastructure expansion across China, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid industrialization, rising EV adoption, and increasing investments in construction and consumer goods sectors, resulting in a higher growth rate compared to North America and Europe.

- Investment Plans: Leading companies are actively investing in regional production expansion and sustainable solutions, including TPU manufacturing capacity additions, ISCC+ certifications, and recycled polyurethane technologies, particularly in Asia Pacific and Europe to meet regulatory and demand shifts.

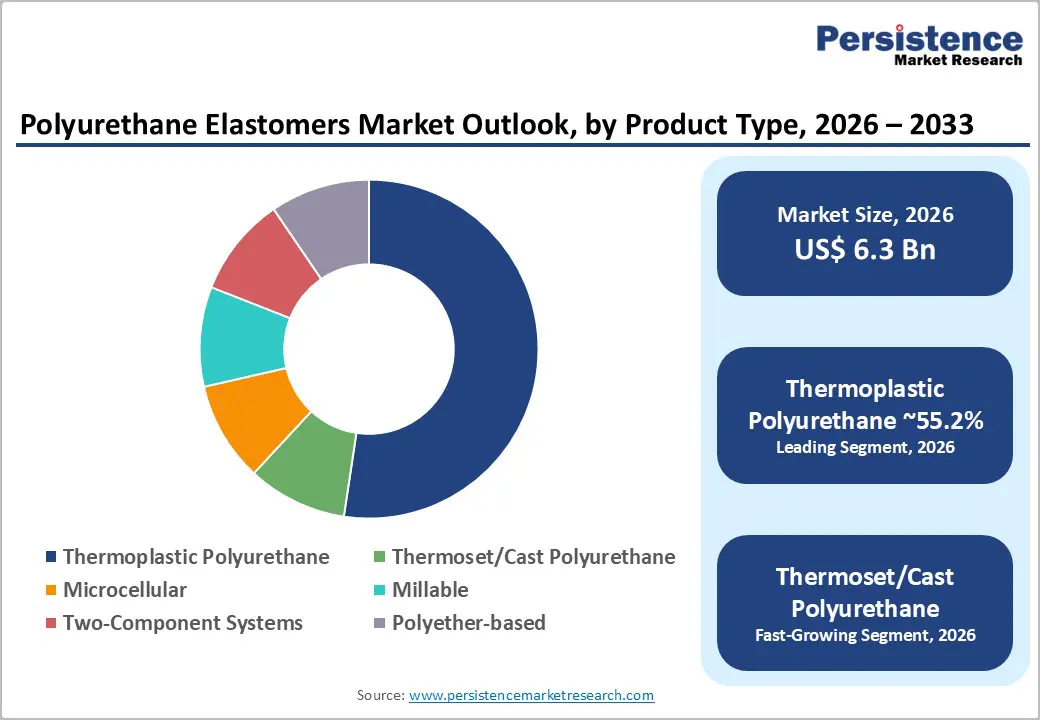

- Dominant Product Type: Thermoplastic polyurethane (TPU) remains the dominant product type, holding an anticipated 55.2% market share, due to its versatility, recyclability, and widespread application across automotive, footwear, and industrial segments.

- Leading Application: The furniture segment leads, accounting for an estimated 31.3% share, driven by high demand for cushioning, seating systems, and ergonomic components in residential and commercial sectors.

| Key Insights | Details |

|---|---|

| Polyurethane Elastomers Market Size (2026E) | US$6.3 Bn |

| Market Value Forecast (2033F) | US$8.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

DRO Analysis

Driver Analysis - Rising Demand for Lightweight and High-Performance Materials in Electric Vehicles (EVs)

The global shift toward electric mobility is significantly increasing the adoption of polyurethane elastomers. EV production continues to scale rapidly, with global sales surpassing 17 million units in 2024. Polyurethane elastomers play a critical role in reducing vehicle weight while maintaining durability and structural integrity. These materials are widely used in seals, bushings, gaskets, and interior components due to their vibration-damping and wear resistance properties. Their ability to enhance energy efficiency and driving range makes them highly relevant for EV platforms. This trend is particularly strong in Asia Pacific and North America, where automakers are prioritizing lightweight materials to meet efficiency and emission targets.

Infrastructure Expansion and Urbanization Driving Construction Demand

Large-scale infrastructure development across emerging economies is fueling demand for polyurethane elastomers in construction applications. Countries such as India are expected to require approximately $840 billion in urban infrastructure investment by 2036, while developing Asia continues to witness sustained capital inflows into transport, housing, and industrial projects. Polyurethane elastomers are extensively used in expansion joints, sealing systems, vibration isolation, and protective coatings for machinery and structures. Their durability and resistance to environmental stress make them suitable for long-term infrastructure applications, ensuring stable demand growth in construction-intensive regions.

Sustainability Regulations and Traceability Requirements Reshaping Product Development

Regulatory frameworks governing chemical safety and environmental impact are becoming increasingly stringent, particularly in Europe. The introduction of mandatory training requirements for handling diisocyanates has elevated compliance standards across the value chain. As a result, manufacturers are focusing on safer processing methods, traceable raw materials, and low-emission formulations. Companies are investing in certifications and recycled-content polyurethane solutions to meet evolving customer expectations. This shift is transforming sustainability from a compliance requirement into a competitive differentiator, influencing procurement decisions across industries.

Restraint Analysis - High Compliance and Operational Costs Associated With Regulatory Requirements

Stringent occupational safety and environmental regulations are increasing the cost of manufacturing and processing polyurethane elastomers. Compliance with handling standards for isocyanates requires structured workforce training, advanced safety systems, and continuous monitoring. These requirements add operational complexity, particularly for small and medium-sized converters. The need for multiple certifications and documentation can also delay project timelines and increase administrative burden, potentially limiting market participation and slowing adoption in cost-sensitive segments.

Volatility in Raw Material Prices and Competition from Alternative Materials

Polyurethane elastomers rely on petrochemical-based feedstocks such as polyols and isocyanates, making them susceptible to fluctuations in crude oil prices and supply chain disruptions. Price volatility can compress profit margins and create uncertainty for manufacturers. At the same time, alternative materials such as thermoplastic elastomers and silicone-based systems are gaining traction due to their recyclability and processing advantages. These substitutes pose a competitive challenge, particularly in applications where cost efficiency and ease of processing are critical decision factors.

Opportunity Analysis - Strong Growth Potential in Asia Pacific Manufacturing Hubs

Asia Pacific presents the most significant growth opportunity for polyurethane elastomer manufacturers. The region accounts for approximately 46.7% of global market share and continues to benefit from rapid industrialization, automotive production, and infrastructure development. China leads in electric vehicle manufacturing, while India and ASEAN countries are emerging as key investment destinations for construction and industrial projects. Local production capabilities, shorter supply chains, and customized product offerings are expected to drive market expansion across the region.

Emergence of Recycled and Sustainable Polyurethane Solutions

The development of recycled-content and bio-based polyurethane elastomers is creating new growth avenues. Manufacturers are increasingly focusing on circular economy principles, including material recovery, recycling technologies, and sustainable feedstocks. These innovations enable companies to meet environmental targets while maintaining product performance. Demand for sustainable materials is particularly strong in automotive, footwear, and consumer goods industries, where brands are under pressure to reduce their carbon footprint and enhance supply chain transparency.

Expansion into High-Value Applications Such As Medical and Electronics

Polyurethane elastomers are gaining traction in specialized applications that require high precision and reliability. In the medical sector, they are used in wound care products, tubing, and device components due to their biocompatibility and flexibility. In electronics, they serve as protective materials for cables, connectors, and sensitive components. These segments offer higher margins compared to traditional applications, as customers prioritize quality, consistency, and regulatory compliance over cost considerations.

Category-wise Analysis

Product Type Insights

Thermoplastic polyurethane (TPU) is expected to dominate the market, accounting for an anticipated 55.2% share of market share in 2026. TPU’s leadership is driven by its versatility, ease of processing, and wide application range across both industrial and consumer segments. It is extensively used in films, fibers, adhesives, footwear, cable jacketing, and automotive components. For instance, TPU is widely utilized in automotive interior skins, protective films, and wire & cable insulation, where flexibility and abrasion resistance are critical.

In consumer markets, it is a preferred material for sports footwear soles and wearable device components due to its durability and aesthetic finish. TPU combines elasticity, chemical resistance, and recyclability, making it compatible with injection molding and extrusion processes, which further strengthens its adoption in high-volume manufacturing environments.

Thermoset/cast polyurethane is likely to be the fastest-growing segment, supported by rising demand for high-performance industrial applications. These materials offer superior mechanical strength, load-bearing capacity, and resistance to extreme temperatures, chemicals, and abrasion. They are widely used in mining conveyor belts, industrial rollers, wheels, and heavy-duty machinery components, where long service life and reliability are essential.

For example, cast polyurethane elastomers are increasingly replacing traditional rubber and metal parts in oil & gas equipment and construction machinery due to their enhanced wear resistance and lower maintenance requirements. While other product types, such as microcellular, millable, and polyether-based elastomers, serve niche applications, including insulation panels and specialty seals, thermoset polyurethane, continues to gain traction due to its customization capabilities and superior performance in demanding environments.

Application Insights

Furniture represents the leading application segment, accounting for an anticipated 31.3% market share in 2026, driven by widespread use in cushioning and ergonomic components. Polyurethane elastomers are commonly used in sofas, office chairs, mattresses, armrests, and modular seating systems, where comfort and durability are key requirements.

For example, high-resilience polyurethane elastomers are widely adopted in ergonomic office furniture and premium bedding products, providing long-term shape retention and load-bearing support. The material’s ability to withstand repeated compression without deformation makes it ideal for both residential and commercial furniture applications. This segment benefits from consistent demand supported by urbanization, rising disposable incomes, and growth in the real estate and hospitality sectors.

Automotive & transportation is the fastest-growing application segment, driven by EV adoption and lightweighting trends. Polyurethane elastomers are increasingly used in vehicle seating systems, suspension bushings, seals, gaskets, NVH (noise, vibration, and harshness) components, and protective coatings. For instance, in electric vehicles, TPU-based components are utilized in battery insulation, cable protection, and interior trims to enhance safety and efficiency.

Automakers are leveraging these materials to reduce vehicle weight, improve energy efficiency, and enhance passenger comfort. The shift toward electric mobility, coupled with advancements in modular seating and lightweight structural components, is expected to further accelerate demand for polyurethane elastomers in this segment.

Regional Insights

North America Polyurethane Elastomers Market Trends - High-Performance Polyurethane Elastomers Driven by Automotive Innovation and Regulatory Compliance

North America represents a mature yet innovation-driven market for polyurethane elastomers, with the U.S. leading in technological advancements and application development. The region benefits from a strong industrial base, advanced manufacturing capabilities, and a well-established automotive sector. Demand is primarily driven by high-performance applications in automotive, construction, medical, and industrial sectors.

For instance, companies such as Dow Inc. and Huntsman Corporation continue to expand their advanced polyurethane portfolios, focusing on lightweight materials and energy-efficient solutions for automotive and building applications. This reinforces North America’s position as a hub for high-value, performance-oriented elastomer usage rather than volume-driven consumption.

The U.S. market emphasizes quality, compliance, and application-specific solutions. Polyurethane elastomers are widely used in lightweight automotive components, insulation systems, and precision industrial parts. A notable example is The Lubrizol Corporation, which has expanded its ESTANE TPU solutions for electric vehicle cable protection and industrial films, aligning with the region’s focus on EV infrastructure and advanced manufacturing. Avient Corporation has also strengthened its specialty polymer offerings for medical and consumer applications, reflecting the growing demand for customized, high-performance materials. These developments highlight how innovation and application engineering are central to market growth in North America.

Regulatory standards in North America focus on occupational safety and environmental protection, influencing material selection and processing methods. While compliance requirements increase operational costs, they also promote the adoption of high-quality and sustainable materials. Companies are responding with safer formulations and improved processing technologies. Investment opportunities in the region are centered on EV components, advanced insulation materials, and specialized industrial applications, particularly where durability and regulatory compliance are critical purchasing factors.

Europe Polyurethane Elastomers Market Trends - Sustainable and Circular Polyurethane Elastomers Led by Strict Regulations and Advanced R&D

Europe is characterized by stringent regulatory frameworks and a strong emphasis on sustainability and innovation. Germany serves as the regional hub for chemical manufacturing and automotive production, while countries such as the U.K., France, and Spain contribute to downstream demand. Major players such as BASF SE, Covestro AG, and LANXESS AG play a pivotal role in shaping the regional polyurethane elastomers landscape through continuous R&D and product innovation. Their strong presence supports Europe’s leadership in high-performance and specialty-grade elastomers.

The European market is driven by automotive electrification, industrial automation, and circular economy initiatives. Polyurethane elastomers are widely used in lightweight vehicle components, sealing systems, and high-performance industrial applications. A key example is Covestro AG advancing circular polyurethane solutions, including the use of alternative raw materials and recycling technologies aimed at reducing carbon emissions. Similarly, BASF SE has introduced recycled-content TPU and is actively investing in chemical recycling processes for polyurethane materials. These initiatives directly influence procurement decisions, as OEMs increasingly prioritize sustainable and traceable materials.

Sustainability is a defining factor in the European market, supported by strict regulatory requirements related to chemical safety and environmental impact. Companies are investing in advanced recycling technologies, bio-based feedstocks, and low-emission production processes. For example, Huntsman Corporation has achieved ISCC+ certification for its TPU production facilities in Germany, enabling the supply of certified sustainable materials. These developments strengthen Europe’s position as a premium market focused on innovation, compliance, and environmental responsibility, while creating opportunities for high-value applications and differentiated product offerings.

Asia Pacific Polyurethane Elastomers Market Trends - Large-Scale Production and Rapid Demand Growth in Polyurethane Elastomers across Industrial Sectors

Asia Pacific is the leading and fastest-growing region, accounting for approximately 46.7% of the market share. The region’s dominance is driven by rapid industrialization, strong manufacturing capabilities, and growing demand across automotive, construction, and consumer goods sectors. Countries, such as China and India, are central to this growth, supported by large-scale infrastructure investments and expanding industrial output.

Regional leaders, including Wanhua Chemical Group, have significantly expanded polyurethane production capacity, strengthening local supply chains and reducing reliance on imports. China remains the largest market in the region, supported by its extensive manufacturing base and leadership in electric vehicle production. Domestic players such as Wanhua Chemical Group continue to invest in integrated polyurethane production facilities, enabling cost-efficient and large-scale output.

Global companies such as BASF SE have also expanded TPU production in Shanghai, including food-contact and high-performance grades, to better serve regional demand. India is emerging as a key growth market due to infrastructure development and urbanization, while Japan, led by companies such as Mitsui Chemicals and INOAC Corporation, contributes advanced material technologies and high-quality manufacturing standards.

The region benefits from cost advantages, large-scale production, and increasing domestic demand across multiple end-use industries. ASEAN countries are gaining importance as alternative manufacturing hubs, attracting investments from global supply chains seeking diversification. For example, Japanese manufacturers have been expanding production footprints in Southeast Asia to support automotive and electronics industries. As sustainability becomes a priority, companies are also focusing on developing eco-friendly polyurethane elastomers, including recycled and low-emission variants. These developments are positioning Asia Pacific not only as the largest market but also as a rapidly evolving center for innovation, localization, and sustainable manufacturing.

Competitive Landscape

The global polyurethane elastomers market is moderately fragmented, with a mix of global chemical companies and regional manufacturers. Leading players hold significant market positions through advanced product portfolios, strong distribution networks, and continuous innovation. A large number of smaller players operate in niche segments, contributing to competitive diversity. Market competition is driven by product performance, pricing, and the ability to meet regulatory and sustainability requirements.

Key players are focusing on innovation, sustainability, and geographic expansion. Companies are investing in advanced materials, recycled-content solutions, and localized production to enhance competitiveness. Strategic partnerships, certification programs, and application-specific product development are emerging as critical differentiators in the market.

Key Industry Developments:

- In April 2025, BASF SE announced that its Shanghai facility was qualified to produce Elastollan® food-contact (FC) grade thermoplastic polyurethane (TPU) under Good Manufacturing Practices (GMP), enabling faster delivery of high-performance materials for medical, food-processing, and industrial applications in Asia Pacific. This development strengthens BASF’s regional supply capabilities and aligns with increasing regulatory requirements for safety and traceability.

Companies Covered in Polyurethane Elastomers Market

- BASF SE

- Covestro AG

- Huntsman Corporation

- Dow Inc.

- The Lubrizol Corporation

- Wanhua Chemical Group

- Mitsui Chemicals

- Tosoh Corporation

- LANXESS AG

- Trelleborg AB

- Avient Corporation

- INOAC Corporation

- Coim Group

- Recticel NV/SA

- Era Polymers Pty Ltd

- Notedome Limited

Frequently Asked Questions

The global polyurethane elastomers market is estimated to be valued at US$6.3 billion in 2026.

The polyurethane elastomers market is projected to reach US$8.6 billion by 2033.

Key trends include increasing adoption of lightweight materials in electric vehicles, rising demand for sustainable and recycled polyurethane solutions, and expanding applications in high-performance industrial and medical segments.

Thermoplastic Polyurethane (TPU) is the leading segment, holding an estimated 55.2% market share, driven by its versatility and wide application range across industries.

The polyurethane elastomers market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

Some of the major players include BASF SE, Covestro AG, Huntsman Corporation, Dow Inc., and Wanhua Chemical Group.