- Plastics, Polymers & Resins

- Chloroprene Rubber Market

Chloroprene Rubber Market Size, Share, and Growth Forecast 2026 - 2033

Chloroprene Rubber Market by Production Method (Acetylene Method, Butadiene Method), Grade (Linear Grade, Cross-linked Grade, Sulfur-Modified Grade, Crystallization-Resistant Grade, Others), Application (Coatings & Adhesives, Wires & Cables, Hoses & Tubes, Industrial Rubber Products, Others), Industry (Automotive, Construction, Electrical & Electronics, Textile, Furniture, Oil & Gas, Others), and Regional Analysis, 2026 - 2033

Chloroprene Rubber Market Size and Trend Analysis

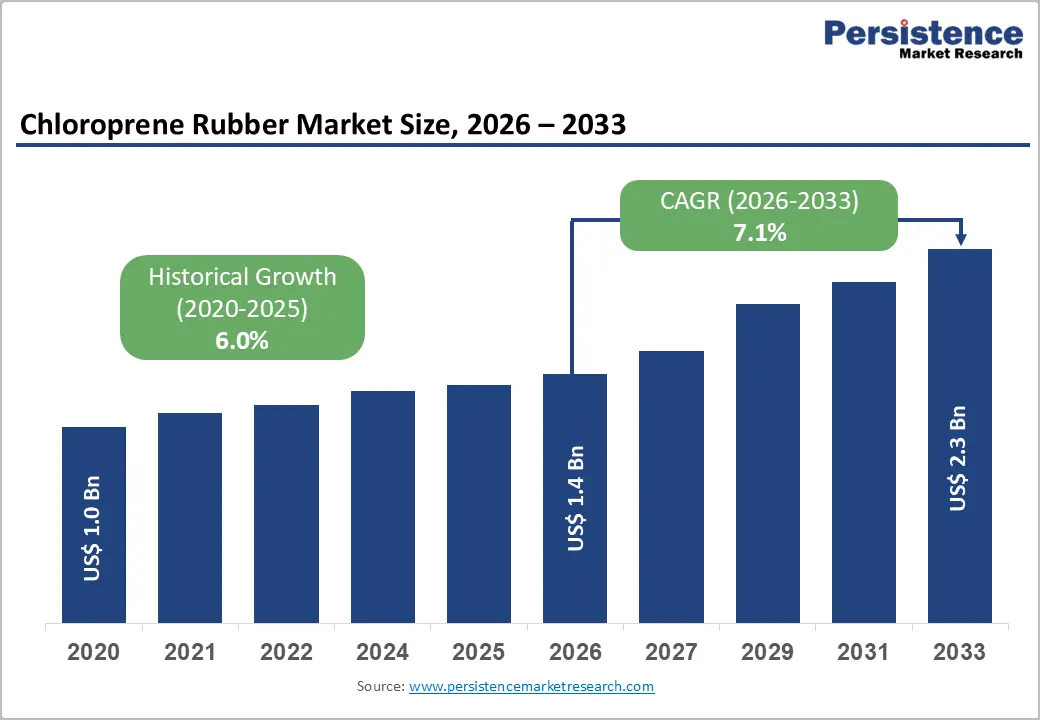

The global chloroprene rubber market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

Growth is driven by rising demand across the automotive and construction industries, where durability and resistance to oil, heat, ozone, and weathering are critical. Increasing global vehicle production and expanding infrastructure investments, particularly in the Asia Pacific, are strengthening consumption. Chloroprene rubber is widely used in hoses, belts, seals, adhesives, and coatings. Additionally, its performance in harsh environments and industrial applications continues to support steady market expansion globally.

Key Industry Highlights:

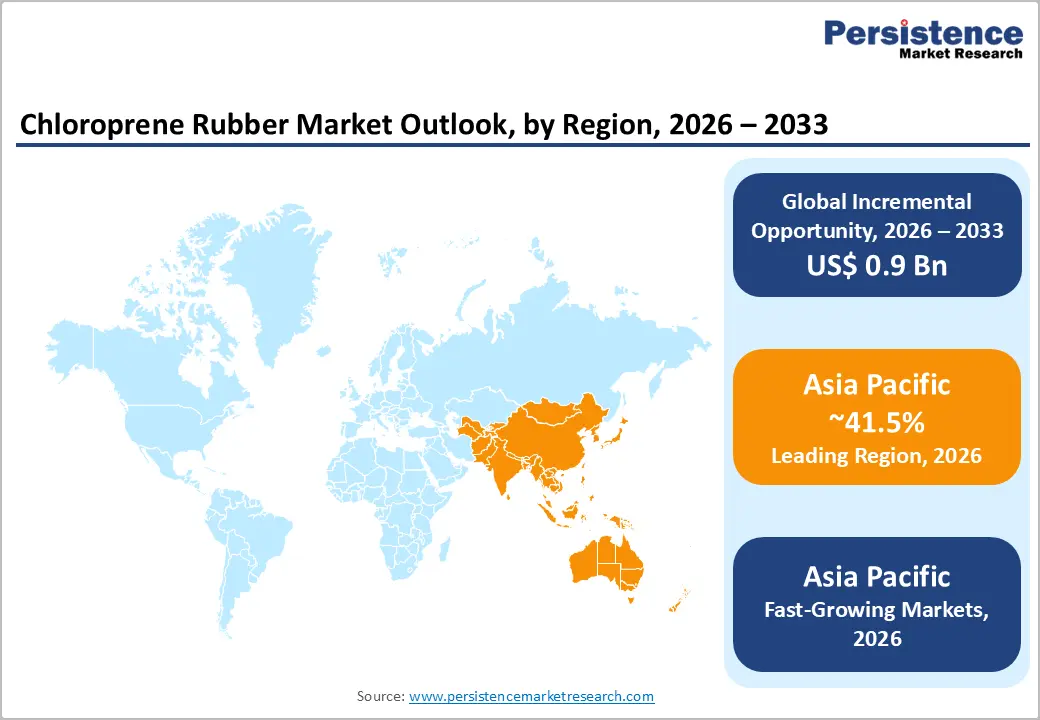

- Leading Region: Asia Pacific dominates the chloroprene rubber market with 41.5% share, supported by large-scale automotive production and infrastructure growth.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, supported by rapid industrialization, urbanization, and expanding manufacturing base.

- Leading Category: Automotive Industry leads with 45% share, due to high usage in hoses, belts, seals, and vibration-damping components.

- Leading Production Method: The butadiene method holds a 65% share, supported by cost efficiency and strong availability of petrochemical feedstocks.

- Key Market Opportunity: Growth in sustainable and bio-based chloroprene rubber for EVs, green tires, and eco-certified construction materials.

Market Dynamics

Drivers - Strong Automotive Production Growth Driving Chloroprene Rubber Demand Globally

The automotive industry is a primary driver of demand for chloroprene rubber, as the material offers superior oil resistance, low-temperature flexibility, and excellent mechanical strength. Global vehicle production stood at roughly 91.5 million units in 2023, according to OICA, with continued growth in both internal combustion and electric vehicles (EVs), driving demand for hoses, belts, seals, and vibration-damping components.

In this context, chloroprene rubber components such as fuel and coolant hoses, timing belts, and gaskets benefit from the polymer’s ability to withstand repeated bending, vibration, and exposure to engine oils. Studies indicate reliable performance above 100°C, while the EV transition, supported by policies such as the US Inflation Reduction Act, is expanding the use of high-voltage cable insulation and battery seals.

Rapid Infrastructure Expansion Increasing Demand for High-Performance Elastomers

Large-scale infrastructure and construction projects create sustained demand for chloroprene rubber in waterproofing membranes, adhesives, bridge bearing pads, and expansion joints. The Asian Development Bank estimates that developing Asian economies will require around US$ 94 trillion in infrastructure investment by 2040, driven by transport, urban development, and industrial expansion across emerging markets.

Many of these projects are located in regions with high humidity, heavy rainfall, or seismic activity, where chloroprene rubber’s resistance to UV radiation, ozone, and fatigue ensures durability. In India, the National Infrastructure Pipeline targets about US$ 1.4 trillion in investment through 2025, supporting the adoption of sealing systems, while engineering bodies emphasize elastomeric components in reducing structural stress.

Restraints - Stringent Environmental Regulations Increasing Compliance Costs and Limiting Growth

Environmental and health regulations related to chloroprene manufacturing and emissions pose a key restraint on the market. The US Environmental Protection Agency has classified chloroprene as a “likely carcinogen” and mandates reductions of up to 90% in emissions at certain facilities. Similarly, frameworks such as EU REACH impose strict limits on VOCs and hazardous monomers, thereby increasing compliance requirements for manufacturers.

These regulations significantly increase capital and operating costs as producers invest in emission-control technologies, closed-loop systems, and safer formulations. Industry estimates suggest compliance-related investments can increase production costs by 15-20%, discouraging smaller players and accelerating market consolidation. Additionally, regulatory pressure encourages end users, particularly in Europe and North America, to shift toward alternative elastomers or bio-based materials.

Volatile Raw Material Prices and Supply Chain Disruptions Impacting Market Stability

Feedstock prices for acetylene and butadiene, essential for chloroprene rubber production, are highly sensitive to fluctuations in crude oil and petrochemical markets. According to the International Energy Agency, crude oil prices surged by around 30% in 2022, significantly increasing input costs. Butadiene prices have also exceeded US$ 2,000 per ton in certain periods, putting pressure on margins across the value chain.

In addition, geopolitical disruptions such as the Russia-Ukraine conflict, along with refinery outages and logistics delays, have impacted supply chains across Europe and Asia. These uncertainties lead to extended lead times and procurement challenges, prompting end users to diversify sourcing strategies or adopt alternative materials, thereby slowing the pace of chloroprene rubber adoption.

Opportunities - Rising Electric Vehicle Adoption and Green Tire Innovations Driving Demand

The growth of electric vehicles (EVs) and the push for low-rolling-resistance, fuel-efficient tires present a major opportunity for chloroprene rubber. The International Energy Agency projects that the global EV fleet could reach about 230 million by 2030, supported by fuel-efficiency regulations and incentives, which are encouraging tire manufacturers to develop advanced rubber compounds.

In this environment, companies like Michelin are investing in green tire technologies that reduce rolling resistance by up to 30% while maintaining durability and safety. Chloroprene rubber is increasingly used in tire sidewalls, EV battery housings, charging connectors, and high-voltage cable insulation, where its thermal stability, weather resistance, and fire-retardant properties support long-term performance.

Advancements in Sustainable and Bio-Based Chloroprene Rubber Materials

Sustainability-driven innovation is creating opportunities for bio-based and low-impact chloroprene rubber alternatives. Initiatives such as the European Green Deal, targeting a 55% reduction in greenhouse gas emissions by 2030, are accelerating research into renewable feedstocks and circular production processes across the chemical industry.

In Japan, the Ministry of Economy, Trade and Industry is supporting projects to reduce fossil-derived content in synthetic rubbers by over 20% by 2030. Pilot studies show that bio-based chloroprene variants can match conventional performance while reducing carbon footprints, making them attractive to sectors prioritizing certifications such as LEED and sustainable procurement practices.

Category-wise Analysis

Production Method Insights

The butadiene method is the leading production route for chloroprene rubber, accounting for approximately 65% of the market share in 2025. This dominance is driven by the widespread availability of butadiene, with global production exceeding 15 million tons annually, ensuring a stable and cost-effective feedstock. Integrated petrochemical complexes, particularly in the Asia Pacific, enable large-scale production supporting automotive, construction, and industrial applications.

In contrast, the acetylene method is emerging as a niche yet increasingly relevant route, driven by advances in process efficiency and specialty applications. While traditionally limited by high energy intensity, ongoing innovations are improving its viability for high-purity and performance-specific chloroprene grades, particularly in applications requiring controlled polymer structures and enhanced material properties.

Grade Insights

Among grades, sulfur-modified grade leads the market, capturing about 40% of the share in 2025 due to its superior vulcanization behavior, adhesion to substrates, and heat aging resistance. It is widely adopted in automotive components such as hoses and timing belts, where durability under dynamic stress is essential. Its compatibility with existing processing systems further supports its large-scale industrial adoption.

Crystallization-resistant grade is gaining traction as the fastest-growing segment, driven by increasing demand for flexibility at low temperatures and improved performance in dynamic environments. This grade is particularly suited for applications exposed to extreme climatic conditions, including specialized automotive and industrial uses where resistance to stiffening and cracking enhances long-term reliability.

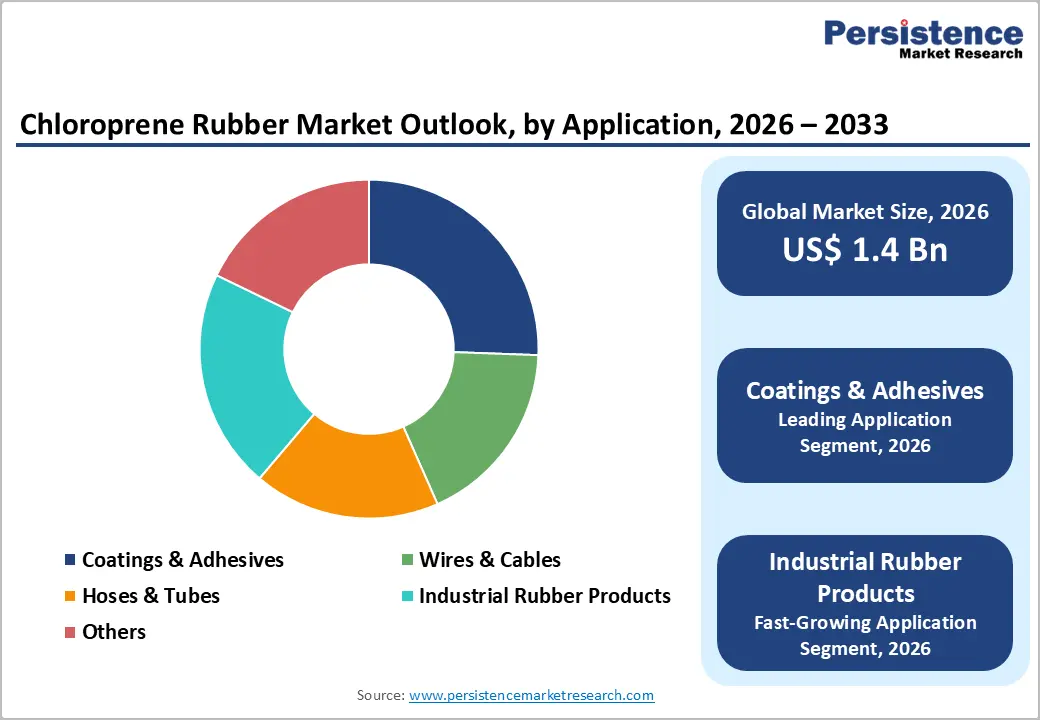

Application Insights

Coatings & adhesives represent the leading application segment, accounting for approximately 35% of the market share in 2025. Chloroprene rubber-based adhesives offer strong bonding to metals, concrete, and textiles while maintaining flexibility over a wide temperature range. Their durability under thermal and mechanical stress makes them widely used in construction, waterproofing systems, and industrial bonding applications.

Industrial rubber products are emerging as the fastest-growing application segment, driven by rising demand for durable elastomeric components across manufacturing and heavy industries. Increasing use in machinery parts, conveyor systems, and protective equipment is expanding adoption, supported by the material’s resistance to abrasion, chemicals, and environmental stress in demanding operational conditions.

Industry Insights

The automotive industry is the dominant end-use segment, accounting for about 45% of the market share in 2025, driven by the extensive use of chloroprene rubber in hoses, belts, seals, gaskets, and vibration-control components. High vehicle production levels, especially in the Asia Pacific, and increasing complexity in engine systems continue to drive demand for durable, heat- and oil-resistant elastomers.

The electrical & electronics sector is emerging as the fastest-growing industry, supported by increasing demand for insulation materials and components in advanced electronic systems. The expansion of EVs, renewable energy systems, and high-voltage infrastructure is driving the adoption of chloroprene rubber for cable insulation, connectors, and protective components that require thermal stability and fire resistance.

Regional Insights

North America Chloroprene Rubber Market Trends and Insights

North America holds a significant share of approximately 28.3% in the chloroprene rubber market, led by the United States’ strong automotive and industrial base. The region benefits from high vehicle production of around 17 million units annually, supporting demand for hoses, belts, and seals. Strict regulations from the US Environmental Protection Agency requiring up to 90% emission reductions have driven investments in cleaner technologies.

These regulatory upgrades have enhanced process efficiency and product quality, positioning North America as a premium market. Innovation hubs such as Detroit and Silicon Valley are advancing EV-specific elastomer applications, while safety frameworks from Underwriters Laboratories influence material standards, encouraging adoption of high-performance, low-emission chloroprene rubber in advanced automotive and electrical systems.

Europe Chloroprene Rubber Market Trends and Insights

Europe represents a mature market driven by strong automotive exports and advanced manufacturing, particularly in Germany. The German Association of the Automotive Industry highlights significant automotive output, supporting demand for high-performance elastomers in drivetrain and under-hood components. The region operates under strict regulatory frameworks, such as EU REACH, that ensure uniform safety and environmental standards.

Europe is expected to grow at a 5.5% CAGR, supported by circular-economy initiatives and sustainability targets. Policies promoting recycling and material recovery are encouraging innovation in recyclable elastomer blends. This focus on durability, compliance, and environmental performance continues to drive demand for advanced chloroprene rubber grades across industrial and automotive applications.

Asia Pacific Chloroprene Rubber Market Trends and Insights

Asia Pacific dominates the global market, accounting for approximately 41.5%, driven by rapid industrialization and strong manufacturing capabilities. China leads regional production with large-scale petrochemical complexes, while Japan supplies high-performance specialty grades. Expanding automotive production in India and Southeast Asia further supports rising demand for chloroprene rubber in components such as hoses, belts, and seals.

The region also benefits from supportive government policies, such as China's “Made in China 2025” and India’s production-linked incentive schemes, which strengthen domestic manufacturing. Growing infrastructure development and cost-efficient production hubs across ASEAN countries are accelerating adoption, positioning the Asia Pacific as the primary growth engine for chloroprene rubber demand over the forecast period.

Competitive Landscape

The chloroprene rubber market is relatively consolidated, with a small group of vertically integrated manufacturers controlling a major portion of global production capacity. This concentration enables strong control over supply chains, pricing, and technological advancements. Companies are actively expanding capacities, particularly in Asia Pacific, to cater to rising demand from automotive, construction, and industrial sectors.

Competition is increasingly driven by innovation, with investments focused on low-emission grades, sustainable feedstocks, and advanced processing technologies. Key differentiators include scale, technical expertise, and global distribution capabilities. Additionally, long-term contracts, collaborative product development with end users, and growing emphasis on sustainability certifications are shaping the competitive dynamics.

Key Developments:

- In March 2025, LANXESS expanded its production capacity in the United States by approximately 20% for low-emission chloroprene rubber grades. The expansion is aimed at meeting stricter EPA emission standards and supporting growing demand from the automotive and construction sectors in North America.

- In July 2024, Tosoh Corporation launched a new crystallization-resistant chloroprene rubber grade tailored for electric vehicle applications. The grade is designed for use in high-voltage cable insulation and battery-related seals, where thermal stability and long-term flexibility are critical.

- In November 2023, Denka Company Limited invested approximately ¥10 billion (about US$70 million) to upgrade its chloroprene rubber production facility in Japan. The project focused on improving energy efficiency, reducing VOC emissions, and enhancing output quality for export-oriented automotive and industrial customers.

Companies Covered in Chloroprene Rubber Market

- Denka Company Limited

- LANXESS AG

- DuPont

- Dow Chemical Company

- Tosoh Corporation

- Asahi Kasei Corporation

- ARLANXEO

- Resonac Holdings Corporation

- Shanxi Synthetic Rubber Group Co., Ltd.

- Chongqing Longevity Salt and Chemical Co., Ltd.

- Nairit Plant CJSC

- SEDO Chemicals Neoprene GmbH

- Zenith Industrial Rubber Products Pvt. Ltd.

- Qingdao Nova Rubber Co., Ltd.

- Versalis S.p.A.

Frequently Asked Questions

The global chloroprene rubber market is expected to be valued at US$ 1.4 billion in 2026, based on current demand trends and expansion in automotive and construction sectors.

The rapid growth of automotive production, which reached about 91.5 million vehicles globally in 2023, is a major driver, as each vehicle requires multiple chloroprene rubber components such as hoses, belts, and seals.

Asia Pacific leads the chloroprene rubber market, with an estimated 41.5% share in 2025, powered by large-scale manufacturing in China, India, and ASEAN countries.

A key opportunity is the development of sustainable and bio-based chloroprene rubber grades for green tires, electric vehicles, and eco-certified construction projects, where low-carbon and recyclable materials are increasingly preferred.

Leading companies include LANXESS, DuPont, Tosoh Corporation, Denka Company Limited, Showa Denko, and Nippon Zeon, along with major petrochemical groups such as PetroChina and Sinopec.