- Plastics, Polymers & Resins

- Polyamide Resins Market

Polyamide Resins Market Size, Share, and Growth Forecast 2026 - 2033

Polyamide Resins Market by Product Type (Dimer Acid-Based (DAB) Polyamide Resins, Polyamide-epichlorohydrin Resins), Product Form (Pellets / Granules, Liquids, Powders), Industry (Automotive, Electrical & Electronics, Inks, Paints & Coatings, Textile & Fibers, Packaging, Aerospace, Chemicals, Consumer Goods, Others), and Regional Analysis for 2026 - 2033

Polyamide Resins Market Size and Trend Analysis

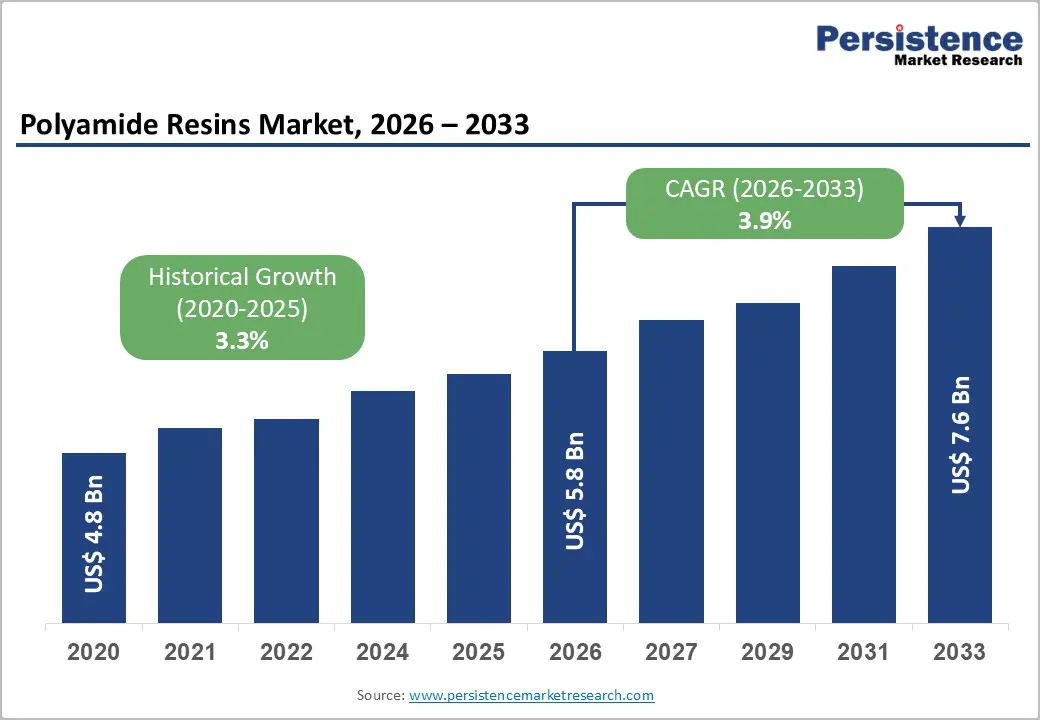

The global polyamide resins market size is likely to be valued at US$ 5.8 billion in 2026 and is projected to reach US$ 7.6 billion by 2033, growing at a CAGR of 3.9% between 2026 and 2033.

The market is propelled by escalating demand from the inks, paints, and coatings industry, where polyamide resins function as high-performance adhesion promoters and binders, alongside increasing polymer adoption in automotive lightweighting programs and flexible packaging. Tightening environmental standards enforced by regulators such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) are further steering innovation toward low-VOC and bio-derived resin platforms, broadening the addressable market for next-generation formulations.

Key Industry Highlights:

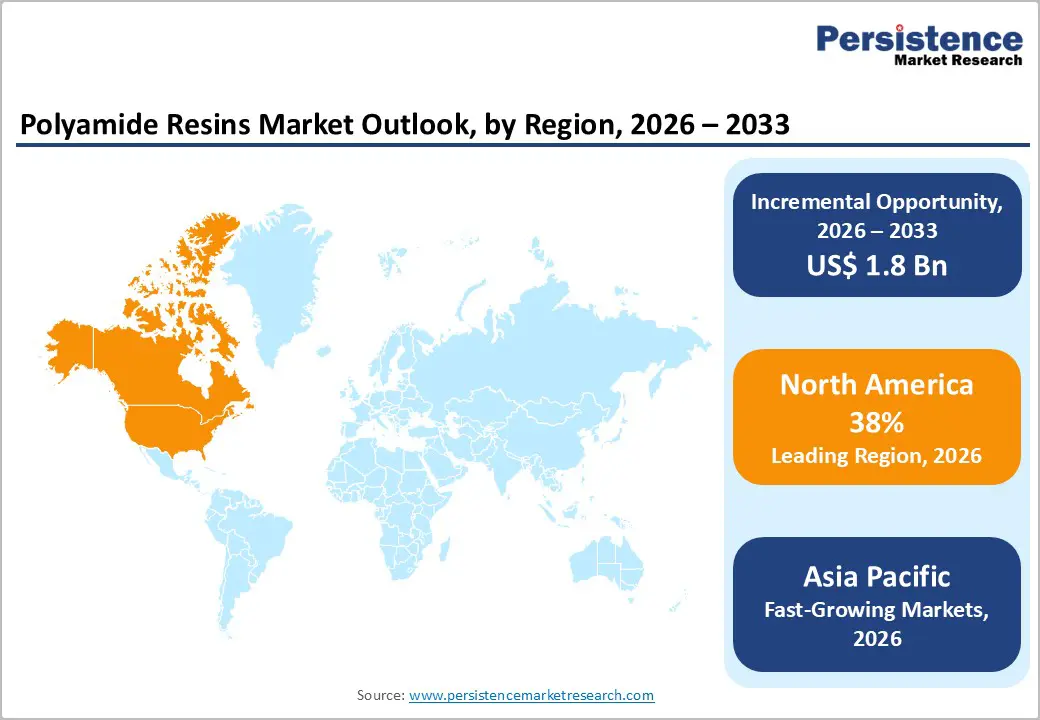

- Leading Region: North America leads the global polyamide resins market with approximately 35% of total revenue share, anchored by a strong automotive OEM supply chain, well-established specialty coatings industry, and regulatory-driven innovation in low-VOC and sustainable resin systems across the United States.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, powered by China's aggressive EV policy framework, India's PLI-driven manufacturing expansion, and surging demand from ASEAN-based flexible packaging and consumer goods manufacturers.

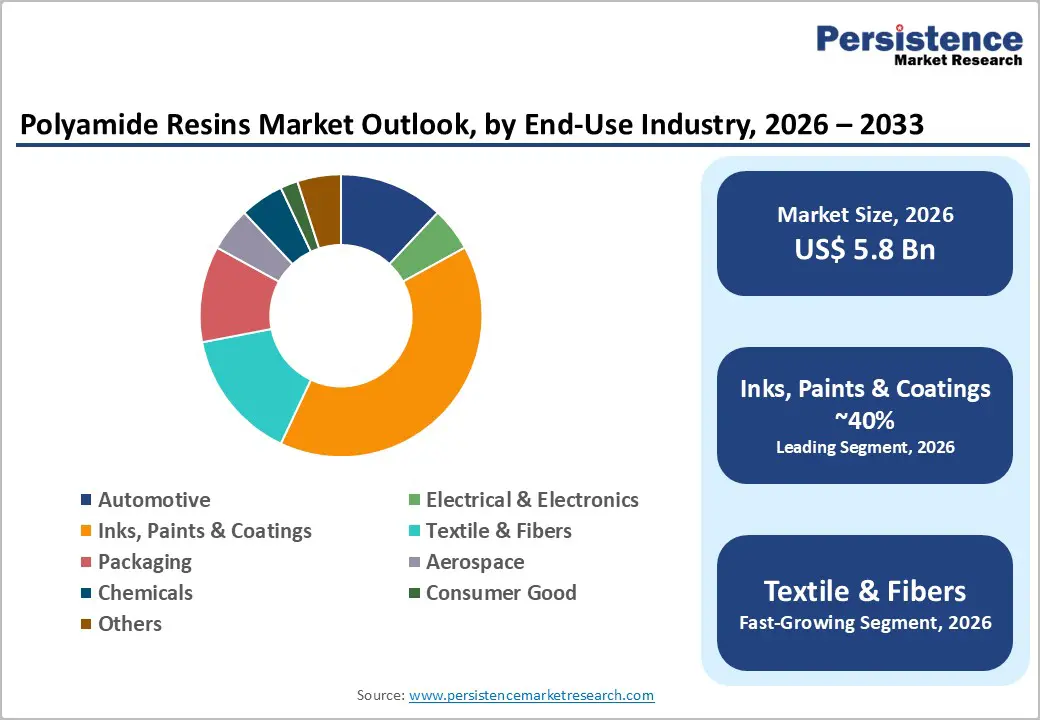

- Dominant Segment: The Inks, Paints & Coatings end-use segment accounts for approximately 40% of global revenue, driven by the extensive use of polyamide resins as adhesion promoters, binders, and rheology modifiers in industrial, packaging, and decorative coating formulations.

- Fastest Growing Segment: Bio-based and sustainable polyamide resin formulations represent the fastest-growing innovation segment, supported by European Green Deal mandates, corporate ESG procurement policies, and growing commercial viability of plant-derived dimer acid feedstocks.

- Key Opportunity: The global EV sector, with approximately 17 million units sold in 2024 per IEA data, creates a high-value demand corridor for UL-certified, thermally stable polyamide resin grades engineered for EV battery housings, high-voltage connectors, and thermal management components.

| Key Insights | Details |

|---|---|

| Polyamide Resins Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 7.6 Bn |

| Projected Growth CAGR (2026 - 2033) | 3.9% |

| Historical Market Growth (2020-2025) | 3.3% |

DRO Analysis

Drivers - Surging Demand from Automotive Lightweighting and Component Manufacturing

The automotive sector remains one of the most consequential demand drivers for polyamide resins, driven by sustained industry-wide efforts to reduce vehicle weight and meet increasingly stringent fuel-economy and emissions standards. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production has consistently exceeded 90 million units annually over the past few years. Polyamide resins are integral to a broad array of automotive components, including air intake manifolds, brake fluid reservoirs, cooling fans, gearbox components, wire and cable jacketing, and valve covers.

Notably, nearly one-third of the approximately 30,000 components in a modern vehicle are manufactured from plastics, with polyamides among the most widely specified engineering thermoplastics. The accelerating global transition to battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs), driven by government policy and the International Energy Agency's (IEA) net-zero targets, is amplifying demand for heat-resistant, dimensionally stable polyamide resin grades for EV powertrain and thermal management systems.

Robust Expansion of the Global Inks, Paints, and Coatings Industry

The global paints and coatings industry constitutes a structural demand anchor for polyamide resins, which are valued as functional binders, rheology modifiers, and film formers across decorative, protective, and functional coating categories. According to the American Coatings Association (ACA), the U.S. coatings industry generates over US$ 30 billion in annual shipments, encompassing architectural, industrial maintenance, and special-purpose applications.

Dimer Acid-Based (DAB) polyamide resins are particularly critical in printing inks, especially flexographic and gravure ink formulations, where they deliver fast-drying performance, superior gloss, and excellent pigment compatibility on flexible packaging substrates. The global surge in e-commerce-driven packaging volumes, combined with increasing brand-owner investment in premium print quality and barrier coatings, is expected to generate sustained demand growth for polyamide resin grades serving the inks and coatings space over the forecast horizon.

Restraints - Feedstock Price Volatility and Raw Material Supply Uncertainty

The manufacture of polyamide resins depends on petrochemical feedstocks, including dimer fatty acids, caprolactam, dicarboxylic acids, and epichlorohydrin, all of which are subject to crude oil price fluctuations and upstream supply disruptions. The U.S. Energy Information Administration (EIA) has consistently highlighted the structural volatility of global crude oil benchmarks, which cascades directly into feedstock cost inflation for resin producers.

Sharp and prolonged increases in raw material costs compress profit margins across the polyamide resins value chain, particularly for small and mid-tier manufacturers with limited hedging capacity or long-term supply agreements. This pricing uncertainty deters new capacity investments, delays R&D commercialization timelines, and undermines procurement planning for downstream formulators, collectively acting as a meaningful drag on overall market growth.

Regulatory Scrutiny on Chlorinated Byproducts in Polyamide-Epichlorohydrin Resins

Polyamide-epichlorohydrin resins, extensively used as wet-strength agents in paper and tissue manufacturing, face growing regulatory pressure related to chlorinated organic byproducts, specifically 1,3-dichloro-2-propanol (1,3-DCP) and 3-chloro-1,2-propanediol (3-MCPD), generated during their synthesis and use in food-contact paper grades. The European Food Safety Authority (EFSA) and the European Chemicals Agency (ECHA) have established restrictive thresholds for these compounds in food packaging materials, imposing significant reformulation and compliance costs on producers.

Failure to comply risks market access restrictions within the European Union, product recalls, and reputational harm. These escalating compliance demands are constraining growth in the polyamide-epichlorohydrin resin segment, particularly in food-grade and beverage-related paper packaging applications.

Opportunities - Bio-Based Polyamide Resins as a Sustainability-Driven Growth Frontier

The global transition toward sustainable chemistry is generating a transformational growth opportunity for polyamide resin manufacturers investing in bio-derived feedstock platforms. Renewable raw materials such as vegetable fatty acids, castor oil derivatives, and plant-based dicarboxylic acids are increasingly viable alternatives to petroleum-based precursors, enabling manufacturers to reduce carbon footprint without compromising resin performance.

Bio-derived polyamide resins are attracting strong policy support under frameworks including the European Green Deal, the EU Chemicals Strategy for Sustainability, and corporate ESG (Environmental, Social, and Governance) procurement mandates from global brand owners in coatings, packaging, and textiles.

The bio-polyamide segment is projected to expand at a notably strong double-digit CAGR through 2030, reflecting the depth of market interest. Companies that achieve commercially viable, performance-equivalent bio-based polyamide resin grades, particularly those that meet REACH compliance requirements, are well positioned to capture premium pricing and long-term supply contracts from sustainability-committed customers in Europe and North America.

Electric Vehicle Component Manufacturing: A High-Growth Demand Corridor

The rapid global proliferation of electric vehicles is creating a structural demand opportunity for polyamide resin suppliers capable of delivering high-performance, engineering-grade polymer solutions for EV-specific applications. EV battery housings, thermal management modules, high-voltage electrical connectors, and lightweight structural components all require resins that offer high-temperature resistance (above 150°C), dimensional stability, and superior electrical insulation.

According to the International Energy Agency (IEA), global electric vehicle sales reached approximately 17 million units in 2024, representing nearly 20% of all new car registrations globally. With the European Union mandating zero-emission vehicle standards by 2035, and major markets in China and the United States implementing aggressive EV adoption incentives, the compounding demand for polymer-intensive EV components will be substantial. Polyamide resin manufacturers holding UL (Underwriters Laboratories) flame-retardant certifications and EV application development expertise are uniquely positioned to exploit this high-value demand corridor.

Category-wise Analysis

Product Type Insights

Dimer Acid-Based (DAB) Polyamide Resins dominate the product type category, commanding approximately 65% of total global polyamide resins market revenue. The segment's preeminence is rooted in the exceptional performance versatility of DAB resins, which are synthesized from dimerized fatty acids and engineered to deliver outstanding flexibility, strong adhesion to metals, plastics, and composites, and superior resistance to water, chemicals, and corrosion. These characteristics make DAB polyamide resins the resin of choice in solvent-borne and waterborne coatings, high-performance adhesives, printing inks, and industrial sealants.

Approximately 35% of manufacturers in the coatings and adhesives sector are reported to be actively transitioning to DAB-based resin systems due to their favorable low-VOC profile and regulatory alignment. Their molecular architecture, allowing customizable melting point, hardness, and compatibility, ensures formulation flexibility across diverse application requirements, underpinning sustained market leadership through 2033.

Product Form Insights

The Liquids segment leads the polyamide resins market by product form, accounting for approximately 39% of total market revenue. Liquid polyamide resins offer critical formulation advantages in coatings, printing inks, and adhesive applications, where uniform substrate penetration, rapid viscosity integration, and strong adhesion film formation are essential quality parameters. Their high compatibility with both solvent-borne and water-borne binder systems allows formulators to achieve consistent gloss, smooth finish, and robust barrier performance on flexible packaging films, metal surfaces, and plastic substrates.

The operational efficiency of liquid resins, encompassing reduced processing temperatures, faster mixing cycles, and minimal handling complexity, makes them highly attractive to large-scale manufacturers in the inks and coatings industries. Manufacturing facilities have increasingly adopted liquid resin systems to streamline continuous production workflows and minimize material waste.

Industry Insights

Inks, Paints & Coatings stands as the dominant Industry segment, contributing approximately 40% of total global polyamide resins market revenue. The segment's leadership reflects the indispensable role of polyamide resins as high-function binders, adhesion promoters, and rheology modifiers across a broad spectrum of decorative, protective, and functional coating formulations. In printing inks, particularly flexographic and gravure applications serving the flexible packaging industry, polyamide resins deliver fast drying, superior pigment wetting, and excellent gloss development on film substrates.

The American Coatings Association (ACA) recognizes protective coatings as a critical enabler of corrosion prevention across infrastructure, automotive, and industrial maintenance sectors, sustaining robust demand for high-performance resin additives. Accelerating growth in consumer goods packaging, pharmaceutical labeling, and e-commerce-driven secondary packaging applications further consolidates this segment's leading position.

Regional Analysis

North America Polyamide Resins Trends & Insights

North America represents the largest regional market for polyamide resins, holding approximately 35% of global market revenue. The United States anchors regional demand, underpinned by a well-developed manufacturing base across automotive components, specialty industrial coatings, and flexible packaging. The U.S. EPA's National Emissions Standards for Hazardous Air Pollutants (NESHAP) and regulations under the Toxic Substances Control Act (TSCA) continue to drive demand for low-VOC resin reformulations, incentivizing product innovation among domestic polyamide resin manufacturers.

The region's robust innovation ecosystem, supported by university research programs and initiatives funded through the U.S. Department of Energy (DOE), is accelerating the development of sustainable and bio-derived polyamide resin chemistries. The presence of major end-use industrial consumers, including leading Tier 1 automotive suppliers, specialty coatings manufacturers, and consumer electronics OEMs, ensures a consistent high-value procurement pipeline for engineered polyamide resin grades. The U.S. automotive sector's accelerated shift to EV platforms, supported by the Inflation Reduction Act (IRA) incentives, is expected to further elevate demand for flame-retardant and thermally stable polyamide resin systems in North America.

Europe Polyamide Resins Trends & Insights

Europe is a mature yet innovation-oriented market for polyamide resins, with Germany, France, the United Kingdom, and Spain forming the core demand base. Germany's position as Europe's largest automotive manufacturer, producing over 4 million passenger vehicles annually, sustains significant consumption of engineering polyamide resins in underhood, powertrain, and lightweight structural applications. The European Union's REACH regulation and the evolving EU Chemicals Strategy for Sustainability continue to shape formulation priorities, compelling manufacturers to transition to safer and environmentally compliant resin platforms.

France and the U.K. represent established markets for specialty printing inks and high-performance industrial coatings, where polyamide resins are specified for their superior durability and formulation compatibility. Spain's construction and industrial maintenance coatings sectors add incremental regional demand. The European Green Deal, targeting climate neutrality by 2050, is structurally redirecting polymer procurement toward bio-based, recyclable, and low-carbon materials. European companies are progressively increasing regulatory compliance expenditures while co-investing in green chemistry platforms with academic institutions under Horizon Europe research programs, reinforcing Europe's role as a global center for sustainable polyamide resin innovation.

Asia Pacific Polyamide Resins Trends & Insights

Asia Pacific is the fastest-growing regional market for polyamide resins, propelled by rapid industrialization, expanding middle-class consumer demand, and a highly competitive and integrated manufacturing ecosystem. China dominates regional consumption, supported by its massive automotive OEM base, electronics manufacturing sector, and expanding industrial coatings industry. National policy directives from China's Ministry of Industry and Information Technology (MIIT) supporting EV adoption and green manufacturing are creating structural demand for high-performance polymer materials, including specialty polyamide resin grades. The China DAB polyamide resin segment is projected to grow at a particularly strong CAGR, fueled by rapid expansion in domestic packaging and export-oriented printing inks production.

Japan and South Korea contribute specialized demand for high-purity engineering-grade polyamide resins serving precision electronics, semiconductor packaging, and advanced composite applications. India is emerging as a high-growth sub-market, driven by the government's Make in India initiative and Production Linked Incentive (PLI) schemes in chemicals, electronics manufacturing, and automotive components. ASEAN nations, notably Vietnam, Thailand, and Indonesia, are rapidly consolidating their positions as manufacturing hubs for flexible packaging, textiles, and consumer goods, adding meaningful momentum to regional polyamide resin demand growth through 2033.

Competitive Landscape

The global polyamide resins market exhibits a moderately fragmented competitive structure, featuring a mix of large multinational specialty chemical companies and agile regional producers. Market leaders including Solvay SA, Mitsubishi Chemical Group, and Toyobo Co., Ltd. sustain competitive advantage through diversified product portfolios, global application development networks, and continuous R&D investment in performance enhancement and sustainable chemistry. Strategic differentiation is pursued through proprietary bio-based resin platforms, customized formulation services, and technical application support.

Mid-tier and regional players, particularly those based in China and India, compete primarily on production cost efficiency and supply agility. Emerging industry trends include cross-border strategic partnerships for green chemistry co-development, capacity expansion in Asia Pacific, and backward integration into fatty acid and dimer acid feedstock supply chains to mitigate raw material cost volatility.

Key Developments:

- In January 2025, Solvay SA advanced its specialty polymer sustainability agenda, with its 2025 Annual Integrated Report confirming strategic progress in reducing carbon footprint across its polyamide and specialty resin manufacturing operations in Europe and North America.

- In March 2024, Mitsubishi Chemical Group presented advanced diamine-based resin hardener solutions, including MXDA and 1,3-BAC series, at CHINACOAT 2024 in China, reinforcing its technical positioning in high-performance epoxy and polyamide coatings chemistries for Asia Pacific markets.

- In January 2022, Solvay SA launched the Omnix® ReCycle high-performance polyamide family, incorporating a minimum of 33% recycled content (70% PIR/PCR), targeting consumer appliances, lightweight automotive components, and packaging applications with a combined performance and sustainability profile.

Companies Covered in Polyamide Resins Market

- Solvay SA

- Toyobo Co., Ltd.

- Mitsubishi Chemical Group

- The Dow Chemical Company

- Merck KGaA

- Arizona Chemical Company

- Ensinger GmbH

- Thomas Swan & Co. Ltd.

- MPD Industries Pvt. Ltd.

- RI Chemical Corporation

- Gabriel Performance Products

- Anqing Hongyu Chemical Co., Ltd.

- Jinan Tongfa Resin Co., Ltd.

- Cytech Coatings Pvt. Ltd.

- RITEKS

Frequently Asked Questions

The global Polyamide Resins market is estimated to be valued at US$ 5.8 Bn in 2026 and is projected to reach US$ 7.6 Bn by 2033, growing at a CAGR of 3.9% during the forecast period, underpinned by sustained demand from coatings, automotive, and flexible packaging end-use sectors.

The principal demand drivers include the growing adoption of lightweight engineering polymers in automotive component manufacturing, a sector producing over 90 million vehicles annually globally, and the expanding global paints and coatings industry, where polyamide resins are essential as binders, adhesion promoters, and rheology modifiers for industrial and packaging applications.

The Inks, Paints & Coatings segment leads the Industry category, accounting for approximately 40% of global Polyamide Resins market revenue, driven by the critical role these resins play in flexographic printing inks, industrial protective coatings, and decorative architectural coating formulations.

North America leads the global Polyamide Resins market, capturing approximately 35% of total revenue, supported by a robust automotive OEM and Tier 1 supplier base, significant specialty coatings industry, and regulatory standards from the U.S. EPA and TSCA driving demand for advanced low-VOC resin formulations.

The most significant emerging opportunity lies in electric vehicle component manufacturing. With global EV sales reaching approximately 17 million units in 2024 per IEA data, polyamide resin manufacturers developing thermally stable, UL-certified flame-retardant polymer grades for EV battery systems, connectors, and thermal management modules stand to access a rapidly expanding, premium-value demand stream.

The global Polyamide Resins market is served by prominent players including Solvay SA, Toyobo Co., Ltd., Mitsubishi Chemical Group, The Dow Chemical Company, Merck KGaA, Arizona Chemical Company (Kraton Corporation), Ensinger GmbH, Gabriel Performance Products, RI Chemical Corporation, MPD Industries Pvt. Ltd., Anqing Hongyu Chemical Co., Ltd., Jinan Tongfa Resin Co., Ltd., Cytech Coatings Pvt. Ltd., and RITEKS, among others.