- Plastics, Polymers & Resins

- Filler Masterbatch Market

Filler Masterbatch Market Size, Share, and Growth Forecast, 2026 - 2033

Filler Masterbatch Market by Filler Type (Calcium Carbonate, Talc, Others), Carrier Polymer (Polyethylene, Polypropylene, Others), Application, End-use Industry, and Regional Analysis for 2026 - 2033

Filler Masterbatch Market Size and Trends Analysis

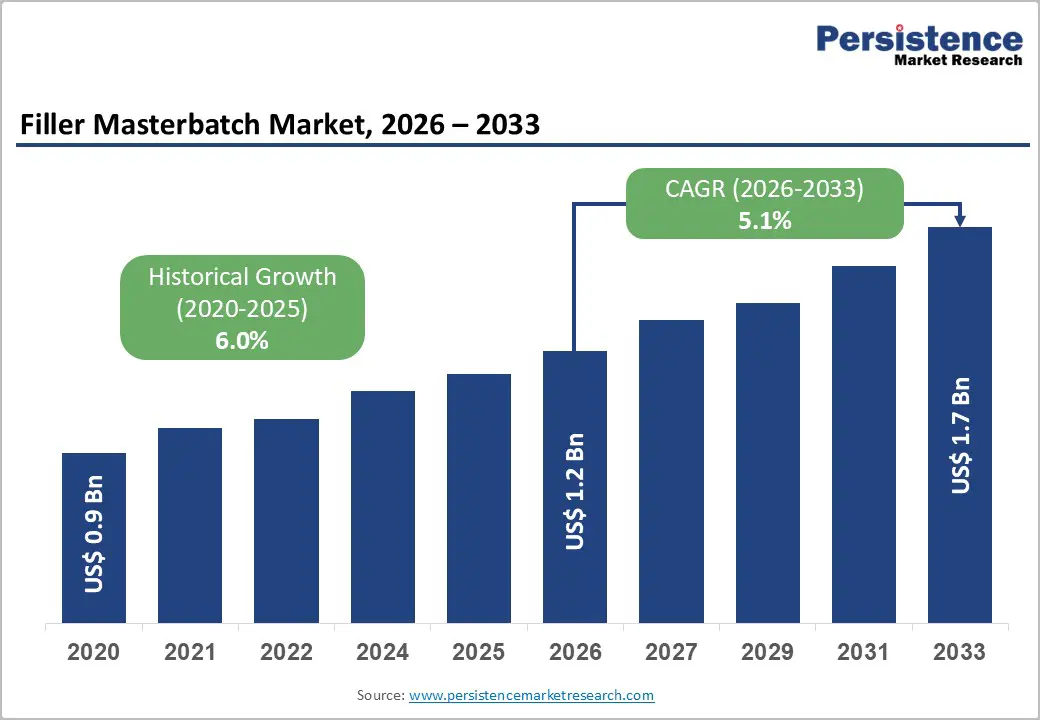

The global filler masterbatch market size is likely to be valued at US$1.2 billion in 2026 and is expected to reach US$1.7 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033, driven by cost optimization in plastic processing, increasing demand from the packaging sector, and the need to enhance material performance, such as stiffness and dimensional stability.

Growth is further supported by rising urbanization and infrastructure development, particularly in emerging economies. Regulatory shifts toward recyclable and sustainable materials are also influencing formulation strategies and supplier competitiveness.

Key Industry Highlights:

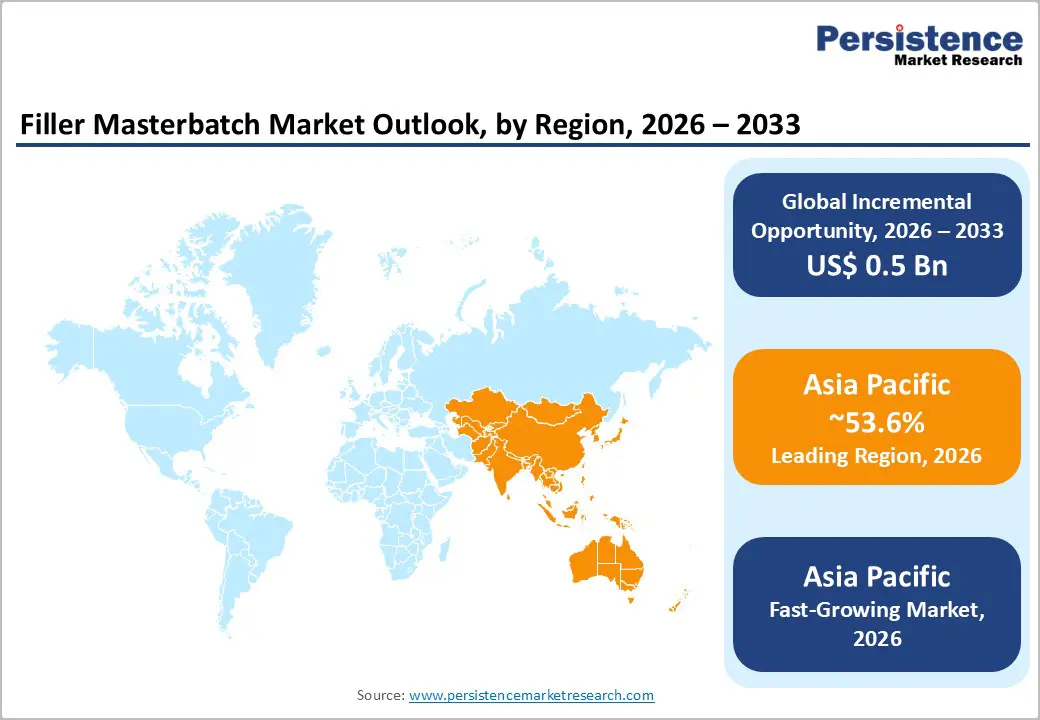

- Leading Region: Asia Pacific is projected to account for 53.6% of the market share, supported by strong manufacturing capabilities and high demand from the packaging and construction sectors.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by rapid urbanization, infrastructure expansion, and increasing consumption of plastic products across China, India, and Southeast Asia.

- Investment Plans: Market participants are focusing on capacity expansions, sustainable product development, and regional manufacturing investments, particularly in Asia Pacific and North America, to support recyclable and high-performance masterbatch solutions.

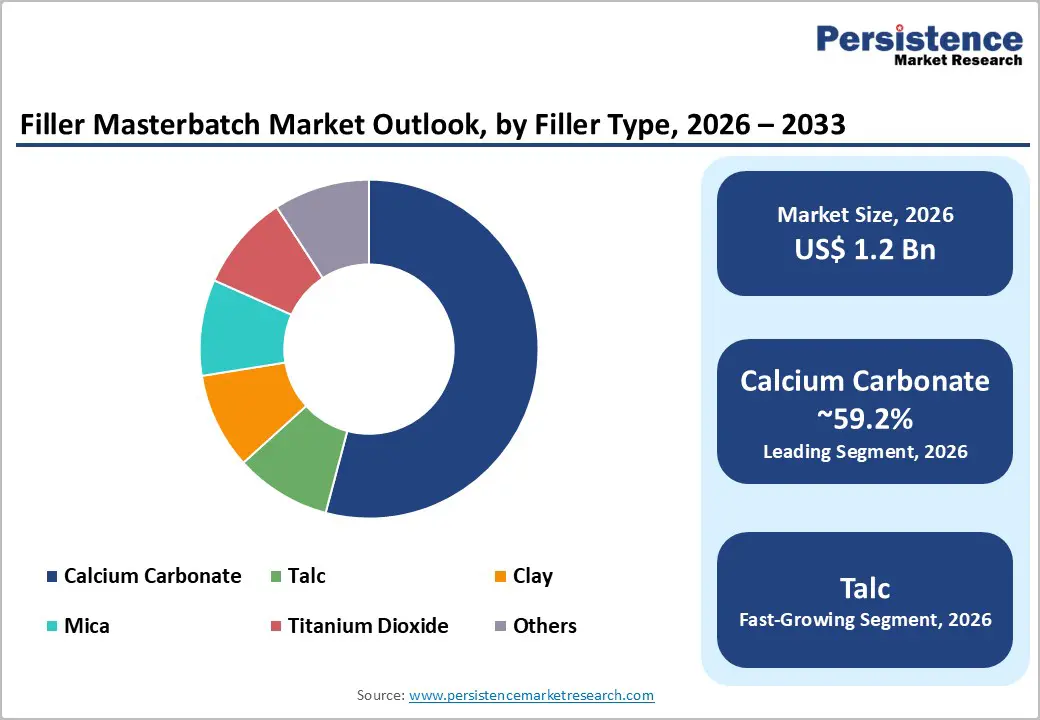

- Dominant Filler Type: Calcium carbonate remains the dominant filler type, holding an anticipated 59.2% market share, due to its cost efficiency, wide availability, and strong application across packaging and injection molding.

- Leading Carrier Polymer: Polyethylene leads the carrier polymer segment with an anticipated 54.2% market share, driven by its extensive use in flexible packaging, films, and extrusion applications.

| Key Insights | Details |

|---|---|

| Filler Masterbatch Market Size (2026E) | US$1.2 Bn |

| Market Value Forecast (2033F) | US$1.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

DRO Analysis

Driver Analysis - Packaging-led Plastics Consumption and Cost Optimization

Packaging remains the largest demand center for plastics, directly supporting filler masterbatch consumption due to its ability to reduce raw material costs while maintaining functional performance. Packaging accounts for approximately 31% of global plastics usage, followed by construction at 17% and transportation at 12%. In high-volume applications such as flexible packaging, rigid containers, and industrial films, manufacturers prioritize cost efficiency without compromising production speed. Filler masterbatch enables reduced polymer usage while maintaining acceptable mechanical properties, making it essential for converters operating in price-sensitive markets. The widespread use of calcium carbonate-based masterbatches reinforces this trend. The market impact is sustained baseline demand across packaging supply chains, even during periods of economic fluctuation.

Urbanization, Industrialization, and Asia Pacific Manufacturing Expansion

Rapid urbanization and industrialization are increasing plastic consumption across construction, consumer goods, and infrastructure applications. Currently, about 55% of the global population lives in urban areas, with projections indicating an increase to 68% by 2050. This transition is particularly significant in Asia Pacific, where large-scale infrastructure development and manufacturing expansion are driving demand for plastic-based products such as pipes, films, and molded components. The region’s strong manufacturing ecosystem enables localized production, reduced logistics costs, and efficient supply chains. As a result, Asia Pacific has emerged as both the largest producer and consumer of filler masterbatch, reinforcing its strategic importance in global market dynamics.

Regulatory Pressure Driving Demand for Sustainable and Compliant Formulations

Evolving environmental regulations and sustainability mandates are reshaping material selection in the plastics industry. Policies focused on waste reduction, recyclability, and extended producer responsibility are influencing the adoption of filler masterbatch solutions that support lightweighting and recyclability. Regulations targeting packaging waste and food-contact materials are particularly impactful, requiring improved traceability and compliance. Manufacturers are increasingly developing formulations compatible with recycled polymers and bio-based materials. This regulatory landscape is shifting competition from purely price-based dynamics to performance- and compliance-driven differentiation, favoring companies with strong technical and regulatory capabilities.

Restraint Analysis - Price Sensitivity and Performance Trade-offs

Filler masterbatch operates within a highly price-sensitive segment of the plastics value chain, which limits pricing flexibility and compresses margins. Fluctuations in raw material costs, including polymers and mineral fillers, can significantly impact profitability. High filler loading levels can also lead to trade-offs in mechanical properties such as impact resistance, transparency, and surface finish. These limitations restrict usage in premium or high-performance applications, particularly in thin films and aesthetic products. As a result, manufacturers must balance cost savings with performance requirements, increasing the need for advanced formulation expertise and quality control.

Regulatory Fragmentation and Compliance Costs

Diverse regulatory frameworks across regions create complexity for manufacturers supplying global markets. Compliance requirements related to food safety, recyclability, and environmental impact vary significantly between regions, necessitating multiple certifications and testing protocols. This increases operational costs, extends product development timelines, and raises barriers for smaller players. The need for traceability and consistent quality further adds to production complexity. Consequently, regulatory fragmentation favors established companies with strong compliance infrastructure and global operational capabilities.

Opportunity Analysis - Growth in the Recycled and Circular Plastics Economy

The transition toward a circular economy presents a significant opportunity for filler masterbatch manufacturers. Increasing demand for recycled-content plastics requires solutions that maintain processability and mechanical performance despite variability in recycled feedstock. Filler masterbatch can enhance the quality and consistency of recycled polymers while reducing overall material costs. This is particularly relevant in packaging, where sustainability targets are becoming mandatory. Companies that develop formulations compatible with recycled and bio-based polymers are well-positioned to capture emerging demand and strengthen long-term customer relationships.

Expansion in Films, Sheets, and Construction Applications

Demand for films and sheets is growing due to increased consumption in packaging, agriculture, and industrial applications. Lightweighting trends and material efficiency initiatives are driving the adoption of filler masterbatch in these segments. At the same time, construction activity in emerging economies is increasing demand for plastic-based materials such as pipes, insulation, and geomembranes. These applications require cost-effective and durable materials, making filler masterbatch an attractive solution. This dual demand from packaging and construction creates strong growth potential, particularly in high-volume markets.

High-Compliance and Value-Added Applications

There is increasing demand for filler masterbatch solutions in regulated industries such as food packaging and consumer goods. These applications require strict compliance with safety standards, traceability, and consistent performance. Manufacturers are investing in advanced formulations that combine cost efficiency with regulatory compliance and enhanced functionality, such as improved barrier properties and extended shelf life. This shift toward value-added products provides opportunities for differentiation and higher margins, particularly for companies with strong research and development capabilities.

Category-wise Analysis

Filler Type Insights

Calcium carbonate is expected to dominate, holding 59.2% market share in 2026, due to its cost-effectiveness, wide availability, and versatility across a broad range of applications. It is extensively used in packaging films, injection-molded containers, and extrusion products such as pipes and sheets, where reducing raw material cost remains a critical priority. Its ability to enhance stiffness, improve dimensional stability, and maintain process efficiency without significantly compromising mechanical performance makes it highly suitable for high-volume manufacturing.

In practical applications, calcium carbonate-based masterbatches are widely used in polyethylene film production for grocery bags and industrial liners, as well as in injection-molded household products such as buckets, crates, and storage containers. Its compatibility with multiple carrier polymers, including polyethylene and polypropylene, further strengthens its adoption. The segment’s dominance is reinforced by a well-established global supply chain and consistent demand from the packaging and construction industries, where cost-performance optimization is essential.

Talc is emerging as the fastest-growing filler type due to its superior performance characteristics, including enhanced heat resistance, rigidity, and dimensional stability. Unlike calcium carbonate, talc offers improved thermal performance, making it particularly suitable for applications that require higher structural integrity under stress or elevated temperatures.

This filler is increasingly used in automotive interior components such as dashboards and panels, where stiffness and heat resistance are critical, as well as in rigid packaging applications like caps and closures. It is also gaining traction in appliance housings and industrial parts, where dimensional precision is required. As manufacturers continue to prioritize lightweight, durable, and high-performance materials, talc-based masterbatches are becoming a preferred solution. The shift toward engineering-grade plastics and performance-driven applications is expected to sustain strong growth for this segment.

Carrier Polymer Insights

Polyethylene leads the carrier polymer segment, anticipated to hold 54.2% market share in 2026, due to its widespread use in packaging and film-based applications. Its excellent processability, flexibility, and compatibility with a wide range of fillers make it the preferred carrier for filler masterbatch formulations. The dominance of polyethylene is closely tied to the global demand for flexible packaging, which requires materials that are both cost-effective and capable of high-speed processing.

Common use cases include blown films for food packaging, stretch films, and agricultural films, where polyethylene-based filler masterbatch helps reduce material consumption while maintaining film strength and uniformity. It is also used in extrusion applications such as pipes and sheets, where consistent dispersion and process stability are essential. The extensive adoption of polyethylene across industries ensures steady demand and supports large-scale production efficiencies for masterbatch manufacturers.

Polypropylene is expected to be the fastest-growing carrier polymer, driven by its increasing use in rigid packaging, automotive components, and consumer goods. It offers a balanced combination of strength, heat resistance, and lightweight properties, making it suitable for applications that require higher mechanical performance compared to polyethylene.

Polypropylene-based filler masterbatch is widely used in injection-molded products such as food containers, caps, automotive trims, and battery casings, where rigidity and dimensional stability are critical. It is also gaining adoption in nonwoven fabrics and structural components, particularly in automotive and industrial sectors. The ongoing shift toward lightweight materials and the replacement of more expensive engineering plastics are accelerating the use of polypropylene. As demand for durable and cost-efficient materials grows, this segment is expected to witness strong and sustained expansion.

Regional Insights

North America Filler Masterbatch Market Trends - Innovation-Driven, High-Performance & Regulatory-Compliant Masterbatch Market

North America represents a mature and innovation-driven market for filler masterbatch, characterized by advanced manufacturing capabilities and stringent regulatory standards. The U.S. leads the region, supported by a strong plastics processing industry and high demand from packaging, healthcare, and infrastructure sectors. Regulatory frameworks emphasize sustainability, recyclability, and material safety, encouraging the development of high-performance and compliant formulations.

For instance, companies such as Avient Corporation and Ampacet Corporation have expanded their portfolios of recyclable and food-contact-compliant masterbatches, aligning with increasing demand from brand owners focused on sustainable packaging. The region’s growth is driven by increasing adoption of recycled plastics, technological advancements in compounding processes, and rising demand for specialty applications.

Companies such as Cabot Corporation have introduced advanced black masterbatches for infrastructure applications such as pressure pipes, improving durability and UV resistance. Americhem Inc. has also invested in color and additive solutions tailored for medical and healthcare applications, where regulatory compliance and consistency are critical. These developments reflect a broader shift toward high-value, application-specific formulations rather than commodity products.

North America also benefits from a well-developed supply chain and robust infrastructure, facilitating efficient production and distribution. However, growth remains moderate compared to emerging regions due to market maturity. Strategic opportunities are concentrated in high-performance segments such as food packaging, medical devices, and advanced industrial components. The increasing collaboration between material suppliers and converters is strengthening innovation ecosystems and enabling faster commercialization of sustainable solutions.

Europe Filler Masterbatch Market Trends - Sustainability-Led, Regulation-Intensive & Circular Economy Focused Market

Europe is a regulation-driven market with a strong focus on sustainability and environmental compliance. Countries such as Germany, the U.K., France, and Spain play a significant role in regional demand, supported by advanced manufacturing and packaging industries. The implementation of stringent regulations related to packaging waste and recyclability is actively shaping material selection and accelerating innovation in filler masterbatch formulations. Companies like Gabriel-Chemie Group have expanded their sustainable product lines, focusing on recyclable and environmentally compliant masterbatches to meet evolving regulatory standards.

The region is witnessing increased demand for sustainable solutions, including recyclable and bio-based materials. For example, Clariant has introduced PFAS-free polymer processing aids and additive solutions, supporting cleaner production processes and regulatory alignment. Similarly, Sukano AG has developed additive masterbatches for PET and biodegradable polymers, targeting circular packaging applications. These innovations are enabling converters to reduce environmental impact while maintaining product performance.

Europe’s market growth is also influenced by the automotive and construction sectors, which require high-performance materials with specific mechanical properties. The use of talc-based masterbatches in automotive interiors and structural components is increasing as manufacturers seek lightweight and durable materials. While regulatory complexity presents operational challenges, it also creates opportunities for companies with strong compliance and R&D capabilities. As a result, Europe continues to lead in premium, high-specification, and sustainability-driven filler masterbatch solutions.

Asia Pacific Filler Masterbatch Market Trends - High-Volume, Cost-Efficient & Rapidly Expanding Manufacturing Hub

Asia Pacific is projected to dominate the global filler masterbatch market, accounting for 53.6% of market share, and is also the fastest-growing region. China leads the market due to its extensive manufacturing base and high consumption of plastics across packaging, construction, and industrial sectors. India is emerging as a high-growth market, supported by rapid urbanization, infrastructure development, and increasing demand for consumer goods. Regional players such as Plastiblends India Ltd. have expanded production capacity and product portfolios to cater to rising domestic and export demand, particularly in packaging and agriculture applications.

The region’s competitive advantage lies in its cost-effective production capabilities, availability of raw materials, and strong export-oriented manufacturing ecosystem. Companies like Plastika Kritis have strengthened their presence in Asia through expanded distribution networks and localized offerings, particularly in agricultural films and packaging solutions. In China, large-scale investments in polymer processing and infrastructure have further increased demand for cost-efficient filler masterbatch in pipes, sheets, and industrial components.

Countries in Southeast Asia, including Vietnam, Indonesia, and Thailand, are experiencing strong growth driven by foreign direct investment in packaging and manufacturing industries. Global suppliers such as LyondellBasell are expanding their footprint in the region through strategic partnerships and product innovations tailored to local demand. Government initiatives supporting industrialization, infrastructure development, and manufacturing exports continue to accelerate market growth.

The expanding middle-class population and rising consumption of packaged goods are further boosting demand for plastic materials and related additives. Asia Pacific’s combination of scale, cost efficiency, and rapid demand growth makes it the most attractive region for investment and expansion. The market is increasingly characterized by high-volume production, competitive pricing, and growing adoption of performance-enhancing formulations, positioning the region as the global hub for filler masterbatch manufacturing and consumption.

Competitive Landscape

The global filler masterbatch market is fragmented with a mix of global and regional players. Leading companies hold a significant share in high-value and regulated applications, while smaller players compete in cost-sensitive segments. The market is characterized by strong competition based on product quality, pricing, and technical capabilities. Companies with advanced formulation expertise and global distribution networks maintain a competitive advantage.

Key players are focusing on product innovation, regulatory compliance, and geographic expansion to strengthen their market position. Investment in research and development, along with localized production capabilities, enables companies to meet evolving customer requirements. Strategic partnerships and customized solutions are increasingly important for maintaining competitiveness in a dynamic market environment.

Key Industry Developments:

- In April 2026, Avient Corporation announced the launch of its Hiformer™ technology for BOPP films, aimed at reducing production complexity while improving film quality, enabling more efficient and cost-effective packaging applications.

- In November 2025, Avient Corporation introduced a non-PFAS low-retention additive (Mevopur™) for polypropylene pipette tips, designed to enhance performance in healthcare plastics while meeting evolving regulatory requirements for safer materials.

Companies Covered in Filler Masterbatch Market

- Avient Corporation

- Ampacet Corporation

- Cabot Corporation

- LyondellBasell

- Plastika Kritis

- Plastiblends India Ltd.

- Tosaf Group

- Americhem Inc.

- Penn Color Inc.

- Hubron International

- Gabriel-Chemie Group

- Sukano AG

- Clariant

- Astra Polymers

- Alok Masterbatches Pvt. Ltd.

- Prayag Polytech Pvt. Ltd.

Frequently Asked Questions

The global filler masterbatch market is estimated to be valued at US$1.2 billion in 2026.

The filler masterbatch market is projected to reach US$1.7 billion by 2033.

Key trends include increasing adoption of recyclable and sustainable masterbatch formulations, rising demand from flexible packaging and infrastructure sectors, and growing use of performance-enhancing fillers such as talc in high-specification applications.

Calcium carbonate is the leading filler type, accounting for an anticipated 59.2% market share, driven by its cost-effectiveness and wide application across plastic processing industries.

The filler masterbatch market is expected to grow at a CAGR of 5.1% between 2026 and 2033.

Some of the major players include Avient Corporation, Ampacet Corporation, Cabot Corporation, LyondellBasell, and Tosaf Group.