- Bulk Chemicals

- Ethyl Acetate Market

Ethyl Acetate Market Size, Share, and Growth Forecast 2026 - 2033

Ethyl Acetate Market by Application (Paints and Coatings, Inks, Process Solvents), End-user (Artificial Leather, Automotive, Food & Beverage), Distribution Channel (Offline, Online), and Regional Analysis, 2026 - 2033

Ethyl Acetate Market Size and Trends Analysis

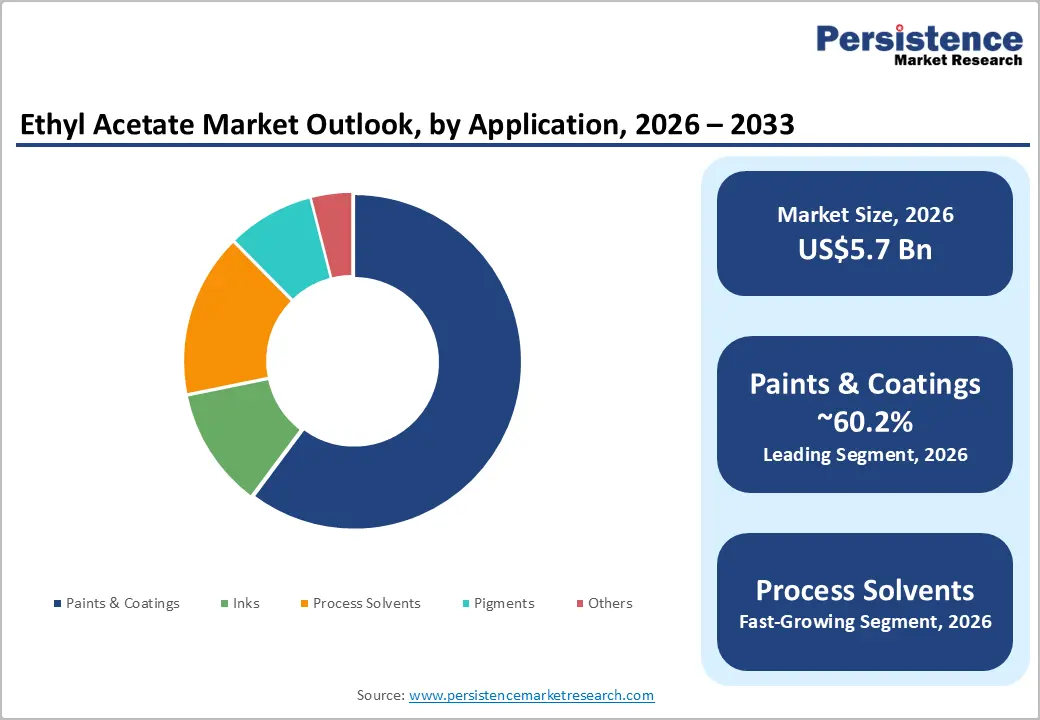

The global ethyl acetate market size is likely to be valued at US$5.7 billion in 2026 and is expected to reach US$9.7 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by rising demand from paints and coatings due to its fast-drying and low-VOC properties.

The market is also benefiting from increasing automotive production, especially electric vehicles that require high-performance coatings and adhesives.

Key Industry Highlights:

- Leading Application: Paints and coatings, approximately 60.2% share in 2026, as ethyl acetate enables fast drying, smooth finishes, and easy compliance with low-VOC norms.

- Dominant End-user: Automotive, nearly 39.6% in 2026, as large-scale vehicle production demands high volumes of coatings, adhesives, and cleaning solvents.

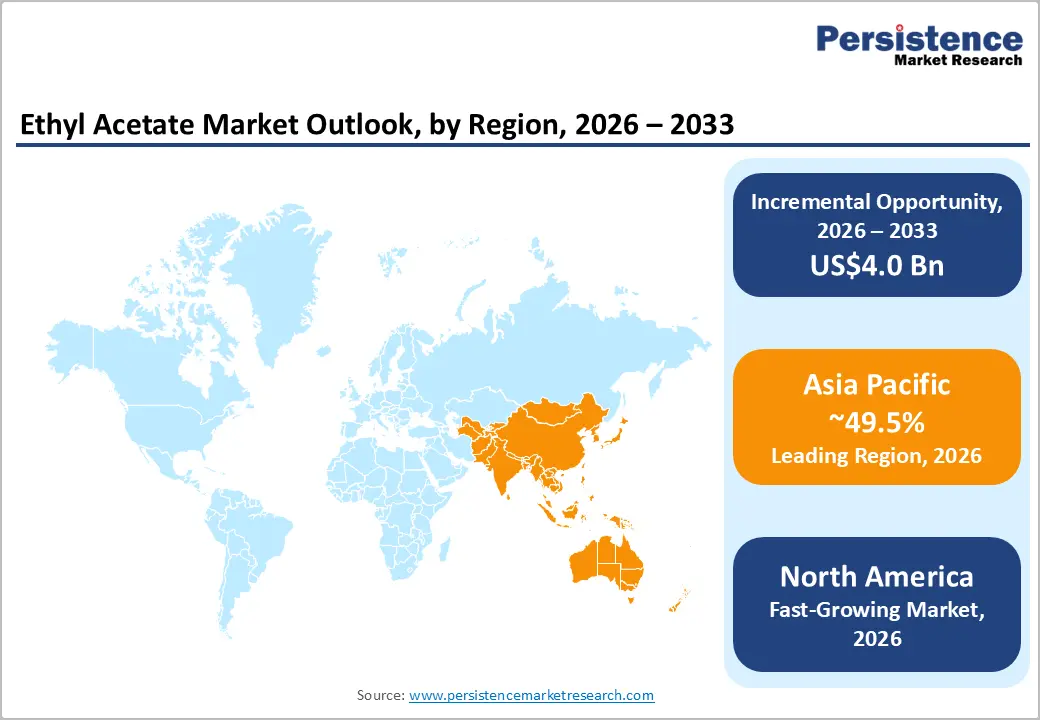

- Leading Region: Asia Pacific, with about 49.5% share in 2026, owing to rising chemical manufacturing capacity in China and India.

- Fast-growing Region: North America, backed by the rising demand for low-toxicity solvents in pharmaceuticals and coatings.

- Sustainability Initiative: Celanese Corporation recently announced the availability of sustainable versions of multiple acetyl chain materials under the ECO-B designation, including ethyl acetate. These products feature mass balance bio-content, where fossil and bio-based feedstocks are mixed in production but accounted for separately through a third-party certified accounting process.

DRO Analysis

Driver - Coatings Industry to Propel Consistent Demand

Ethyl acetate is a go-to solvent in the coatings industry as it breaks down a wide range of resins, including nitrocellulose, Cellulose Acetate Butyrate (CAB), and acrylic resins. At the same time, it allows coatings to dry quickly and evenly. Its fast evaporation rate produces smooth and defect-free films, making it essential for automotive clear coats, wood finishes, and industrial primers.

The shift away from toxic alternatives is gaining more ground. The gradual move from Methyl Ethyl Ketone (MEK) to ethyl acetate in certain coating formulations, boosted by its lower toxicity and stronger regulatory acceptance, is adding incremental demand. Infrastructure spending across India and Southeast Asia is further boosting consumption of architectural and industrial coatings, keeping bulk demand for this solvent resilient.

Pharmaceutical and Personal Care Sectors to Broaden Usage

Ethyl acetate plays a key role in drug manufacturing, not just as an extraction medium but as a reaction solvent and chromatography eluent as well. Its ICH Class 3 designation (low toxic potential) means it carries generous residual solvent limits in finished drug products, making it a preferred choice for API purification. India's generic drug exports surpassed US$50 billion in 2024.

It is hence boosting demand for pharmaceutical-grade ethyl acetate in antibiotic purification, steroid extraction, and tablet-coating processes. The U.S. Food and Drug Administration’s (FDA) regulation 21 CFR 182.60 lists the solvent as Generally Recognized as Safe (GRAS). This validates its use in excipients and taste-masking formulations under cGMP regimes. In personal care, its speedy evaporation and mild odor make it ideal for nail polish removers, base coats, and fragrances, where residue or strong odors are undesirable.

Restraint - Flammability and Vapor Hazards Complicate Safe Handling

Ethyl acetate's high volatility creates serious fire and safety risks throughout its supply chain. With a flash point of -4°C and explosive limits between 2.0% and 11.5%, it is classified under hazard statements H225 (highly flammable liquid and vapor) and carries an NFPA flammability rating of 3. What makes this dangerous is how its vapors behave. The liquid produces vapors that form explosive mixtures with air at normal temperatures. Those vapors can travel a considerable distance to a source of ignition before flashing back.

Its vapor density is 3.04, meaning vapors are heavier than air and tend to accumulate in low-lying areas rather than dispersing upward. Under OSHA regulations, facilities storing or using ethyl acetate must meet stringent ventilation, grounding, and ignition-control requirements. These further raise compliance costs and limit its use in settings without proper infrastructure.

Opportunity - Renewable Ethanol as a Feedstock

Ethyl acetate can be made entirely from bio-derived ethanol and acetic acid, which qualifies it as a 100% bio-based solvent. This is creating a commercial momentum. Viridis Chemical, the only industrial-scale producer of 100% bio-based ethyl acetate in North America, announced in December 2024 that it is relocating its plant to Peoria, Illinois, to co-locate with BioUrja Renewables' corn-based industrial alcohol facility. The company holds ISCC PLUS certification and is a USDA BioPreferred-certified product manufacturer.

Viridis also received the U.S. EPA's 2024 Green Chemistry Challenge Award for this work. The model of pairing ethyl acetate production directly with a renewable ethanol source cuts logistics costs and strengthens the sustainability case. As buyers in coatings, pharma, and personal care require documented low-carbon inputs, bio-ethanol-derived ethyl acetate gives producers a traceable and certifiable product that fossil-based grades simply cannot match.

Mass-Balance Certification to Unleash Sustainable Product Claims

For producers that cannot fully switch to bio-based feedstock, the mass-balance approach provides a practical middle path. Under frameworks such as ISCC PLUS, renewable feedstock is introduced into an existing production process alongside fossil inputs. The resulting bio-based share is allocated to specific product batches through verified bookkeeping without requiring physical segregation. Mass balancing can be implemented in already existing manufacturing processes, making it the method of choice for most ISCC PLUS certified companies. This is already happening with adjacent chemistries.

BASF switched its ethyl acrylate production to bio-based grades using bioethanol as the alcohol source starting Q4 2024. It is now delivering a variant with ISCC PLUS mass-balance certification and a product carbon footprint nearly 30% lower than fossil-based equivalents. A similar approach applied to ethyl acetate would let leading producers meet buyer sustainability requirements without rebuilding production infrastructure. It is anticipated to help in reducing the barrier to entry into the booming bio-solvents segment.

Category-wise Analysis

Application Insights

Paints and coatings are predicted to lead with a share of approximately 60.2% in 2026, as ethyl acetate fits strict regulatory and performance requirements at the same time. The organic compound is widely used as a solvent in coatings because it evaporates quickly and leaves a smooth finish. This is important in automotive paints, wood coatings, and industrial finishes. What makes it more significant today is compliance.

Agencies such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) classify ethyl acetate as a relatively low-toxicity solvent compared to alternatives such as toluene. This helps manufacturers meet VOC emission rules without changing formulations drastically.

Process solvents are estimated to be the fastest-growing segment in the forecast period, as new industries require clean and highly efficient extraction systems. Ethyl acetate is now widely used in pharmaceutical synthesis, lithium battery materials, and specialty chemicals. Its role is expanding as it dissolves a wide range of compounds, but it is still easy to remove after processing. This is important in high-purity manufacturing. The U.S. FDA has listed the organic compound as a Class 3 solvent, meaning low toxic risk. This allows higher permissible residual levels compared to stricter solvents.

End-use Insights

The automotive segment is anticipated to dominate with a share of nearly 39.6% in 2026, as it uses ethyl acetate across multiple layers of manufacturing, not just coatings. The automotive sector uses ethyl acetate in paints, adhesives, printing inks for labels, and interior components. Modern vehicles require multi-layer coatings for corrosion resistance and aesthetics. Each layer uses fast-evaporating solvents such as ethyl acetate to reduce cycle time in paint shops.

Industry data from groups, including the International Organization of Motor Vehicle Manufacturers, shows steady global vehicle production recovery, especially in Asia Pacific. This propels coating and adhesive demand. EV manufacturing is also increasing solvent use.

The food and beverage segment is expected to remain in the second position in 2026, as ethyl acetate is seen as a safe and naturally derived solvent. The organic compound is used in food processing for the decaffeination of coffee and tea, flavor extraction, and packaging inks. What is pushing growth is its natural positioning. It can be produced from bio-ethanol, which fits clean-label trends. The European Food Safety Authority and the Food Safety and Standards Authority of India both allow ethyl acetate as a food-grade extraction solvent in limited amounts. This regulatory acceptance supports its use in large-scale food processing.

Regional Insights

Asia Pacific Ethyl Acetate Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 49.5%, augmented by large-scale infrastructure projects and a booming automotive sector, all of which feed consistent demand for paints, coatings, and adhesives. The region also has a built-in cost edge. It benefits from abundant raw material availability, low production costs, and superior industrial growth. Countries such as China and India are dominating due to their expanding manufacturing sectors and rising export bases.

Regulatory pressure in other parts of the world is also redirecting demand here. Regulatory restrictions on competing aromatic solvents, including toluene and xylene, are pushing formulators toward ethyl acetate, providing structural long-term tailwinds.

China Ethyl Acetate Market Trends

China is the single largest producer and consumer of ethyl acetate in the world, but the picture right now is mixed. On the supply side, total production capacity is projected to reach 4.7 million tons in 2025, with 480,000 tons of new capacity added, thereby intensifying domestic competition. Traditional consumption sectors such as coatings and adhesives are showing insufficient recovery momentum, constrained by deep adjustments in the real estate sector. The brighter spots are in high-value niches. Electronic-grade acetate esters are seeing growth. China-based producers are now moving toward high-end transformation and export-led strategies to offset sluggish domestic offtake.

India Ethyl Acetate Market Trends

India is the fastest-growing market for ethyl acetate in Asia Pacific, with demand being pulled simultaneously from multiple high-growth sectors. The pharmaceutical pull is the most significant driver. The country’s generic drug exports are rising, further boosting demand for pharmaceutical-grade ethyl acetate in antibiotic purification, steroid extraction, and tablet-coating processes. Government-backed construction programs and a surging automotive base are also lifting demand for paints and coatings.

Laxmi Organic Industries, for example, broadened its ethyl acetate production capacity by an additional 70 kilotons per annum in October 2024. This expansion triggered after the company's plant utilization rates reached 90%.

North America Ethyl Acetate Market Trends

North America is the fastest-growing region for ethyl acetate among all geographies, and two factors are driving this. First, the shift away from more toxic solvents is structural. The progressive shift away from methyl ethyl ketone toward ethyl acetate in certain coating formulations is adding incremental demand. Second, the pharmaceutical sector is creating a durable new lane. The U.S. FDA's regulation 21 CFR 182.60 lists ethyl acetate as GRAS, validating its use in excipients and taste-masking formulations under cGMP regimes. ICH Q3C residual-solvent testing keeps removal thresholds tight, sustaining sales of high-purity grades.

U.S. Ethyl Acetate Market Trends

Growth in the U.S. is fostered by vertically integrated producers who control both feedstock and downstream supply. Celanese commissioned a 1.3-million-ton acetic acid unit at Clear Lake, Texas, in 2023, strengthening raw material security for its downstream ester plants. On the capacity side, in October 2025, INEOS USA announced the expansion of its ethyl acetate production capacity in Texas to meet rising demand from coatings, adhesives, and flexible packaging sectors, including process optimization for reduced carbon emissions. In September 2025, Celanese also launched a new bio-based ethyl acetate line from renewable ethanol feedstock.

Europe Ethyl Acetate Market Trends

Europe's market is being transformed by sustainability mandates more than pure volume growth. The EU's VOC regulations and green procurement policies are pushing formulators away from aromatic solvents and toward ethyl acetate. On the production side, the most significant development is the shift toward renewables. For instance, CropEnergies AG began the construction of Europe's first green ethyl acetate production plant in Elsteraue, Germany, in April 2023. It is expected to create around 50 jobs and begin operations by late 2025.

The company partnered with Johnson Matthey to use its proprietary technology for this facility. This is a landmark move, as it establishes a domestically sourced and bio-based supply chain for domestic buyers for the first time.

U.K. Ethyl Acetate Market Trends

The U.K. is functioning primarily as a key producer and exporter rather than a net consumer. This is almost entirely due to INEOS's Salt End facility in Hull. It is the largest single ethyl acetate production unit in Europe. The U.K. has re-emerged as a prominent exporter post-Brexit, supplying markets across Europe and beyond. The INEOS Hull plant receives ethylene feedstock via pipeline from INEOS's Grangemouth complex in Scotland, giving it a raw material cost advantage.

The firm announced a multi-million-pound expansion at the Hull facility, citing rising demand across pharmaceuticals, cosmetics, inks, and flexible packaging. The U.K.'s role as Europe's primary ethyl acetate supplier is further strengthened by Belgium's position as a re-export distribution hub into the broad EU market.

Germany Ethyl Acetate Market Trends

Germany is both a significant consumer of ethyl acetate and the birthplace of Europe's first renewable ethyl acetate plant. The industrial base, including automotive OEMs, specialty coatings, and pharmaceutical manufacturers, maintains consistent demand for high-purity grades. The CropEnergies facility in Elsteraue, Saxony-Anhalt, is set to change Germany's supply dynamic. CropEnergies broke ground on its bio-based ethyl acetate plant on April 5, 2024.

Once operational, this 50,000-ton-per-year plant will reduce the country’s reliance on imports as well as give domestic manufacturers access to a certified and low-carbon solvent grade. It is increasingly important under EU green procurement frameworks and corporate Scope 3 reporting commitments.

Competitive Landscape

The global ethyl acetate market is moderately consolidated, with a small group of integrated chemical giants controlling a significant share of global capacity. Companies such as Celanese Corporation, INEOS Group, and Eastman Chemical Company dominate premium-grade supply as they control upstream acetic acid production and operate integrated acetyl chains. This allows them to manage raw material volatility better than standalone solvent producers and maintain margins even during pricing pressure cycles.

Asia-based producers, especially China’s manufacturers such as Jiangsu Sopo and Jiangmen Handsome Chemical Development, are changing the global competition through large-scale capacity additions and low production costs. These suppliers collectively account for around 73% of global ethyl acetate volume, giving the region key pricing influence in export markets. They benefit from economies of scale, coal-based feedstock economics, and government-backed chemical infrastructure.

Key Industry Developments:

- In May 2026, Laxmi Organic Industries Ltd commissioned its new ethyl acetate plant at manufacturing site-III, located in Maharashtra. Commercial dispatches commenced immediately, marking a key milestone in the company's capacity expansion strategy.

- In June 2025, New Iridium secured US$2.65 million in seed funding to expand its low-carbon platform and build a 50 metric ton pilot facility for producing bio-based acetic acid and ethyl acetate. It is supported by the U.S. Department of Energy, with both products receiving USDA BioPreferred certification for 100% bio-based content.

- In April 2025, CropEnergies AG held the groundbreaking ceremony for Europe's first green ethyl acetate production plant at the Zeitz Chemical and Industrial Park in Elsteraue, Germany. The 50,000-ton-per-year facility uses Johnson Matthey's proprietary technology to produce renewable ethyl acetate from sustainable ethanol.

Companies Covered in Ethyl Acetate Market

- INEOS

- Celanese Corporation

- Eastman Chemical

- Jiangsu Sopo

- Jiangmen Handsome

- Wuxi Baichuan

- Jubilant Life Sciences

- Godavari Biorefineries Ltd.

- Sekab

- KAI CO. LTD.

- IOL Chemicals and Pharmaceuticals

- Others

Frequently Asked Questions

The global ethyl acetate market is projected to be valued at US$5.7 billion in 2026.

The ethyl acetate market is expected to reach US$9.7 billion by 2033.

Key market trends include a shift toward bio-based ethyl acetate and rising demand for high-purity as well as low-VOC solvents.

Automotive is expected to be the leading end-user with a share of nearly 39.6% in 2026, as EV production increases the demand for precision coatings.

The market is expected to grow at a CAGR of 7.9% from 2026 to 2033.

INEOS, Celanese Corporation, Eastman Chemical, and Jiangsu Sopo are a few key market players.