- Specialty & Fine Chemicals

- Ethanol Market

Ethanol Market Size, Share, and Growth Forecast 2026 - 2033

Ethanol Market by Product Type (Synthetic Ethanol, Bio-ethanol), Raw Material (Sugar-Based Feedstocks, Starch-Based Feedstocks, Cellulosic Feedstock, Petrochemical Feedstock), Application (Fuel Blending, Solvents, Chemical Intermediate, Disinfectants & Sanitizers, Personal Care & Cosmetics, Food Processing, Others), and Regional Analysis, 2026 - 2033

Ethanol Market Size and Trend Analysis

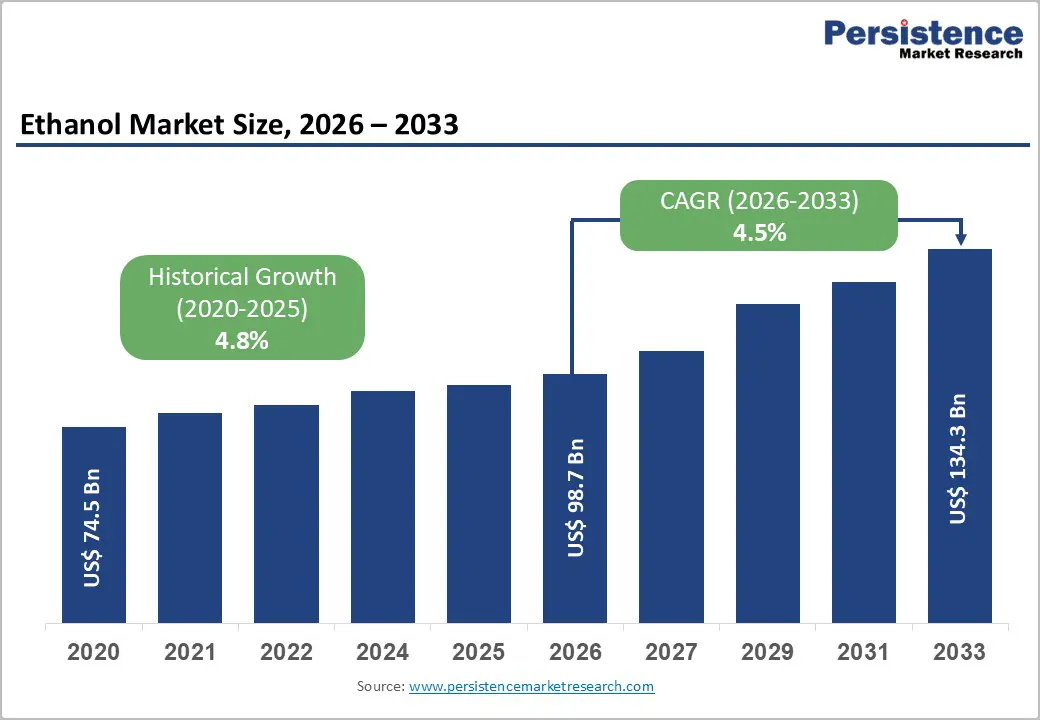

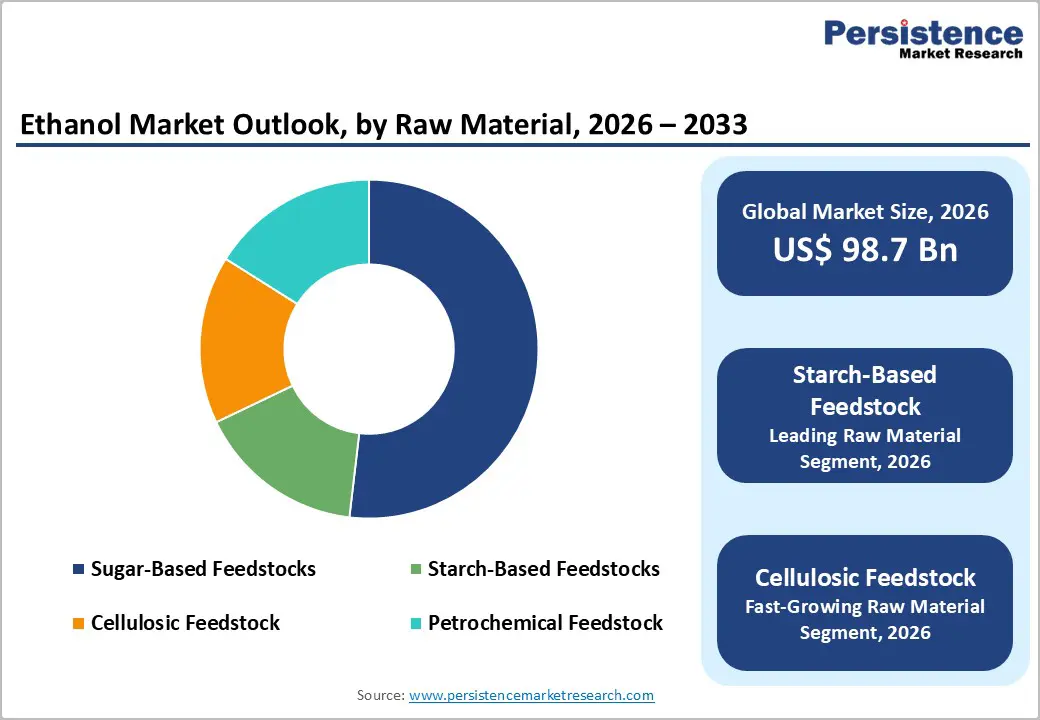

The global Ethanol market size is expected to be valued at US$ 98.7 billion in 2026 and projected to reach US$ 134.3 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033. Biofuel blending mandates, expanding industrial solvent applications, and surging demand for bio-based chemical intermediates are collectively propelling the global ethanol market forward.

The accelerating global energy transition, underscored by government-mandated renewable fuel standards in the United States, Brazil, the European Union, and India, is the primary demand engine, with fuel-grade ethanol blending programs absorbing the majority of global output. Simultaneously, robust demand from the pharmaceutical, personal care, and food processing industries, alongside growing interest in second-generation cellulosic ethanol as a low-carbon fuel extender, is diversifying the demand base and providing market resilience amid fluctuating fossil fuel prices.

Key Industry Highlights:

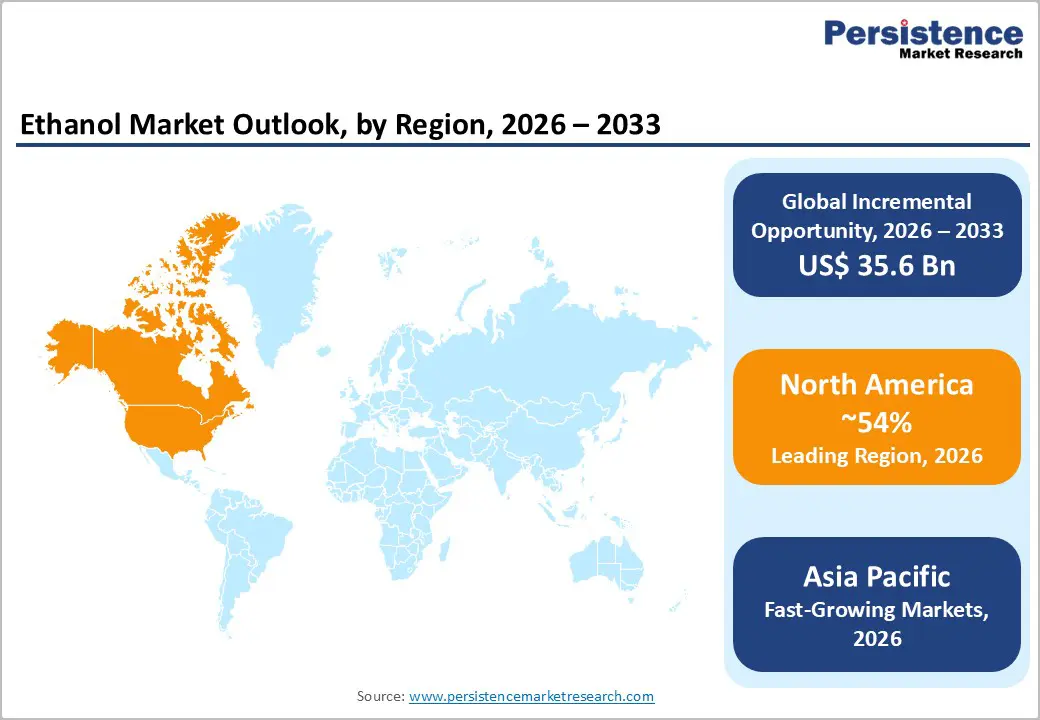

- Leading Region: North America leads the global ethanol market with approximately 54% of production share in 2025, underpinned by the U.S. RFS mandate, vast corn-based bioethanol infrastructure, and world-class producers such as POET LLC, ADM, and Valero Energy Corporation.

- Fastest Growing Region: Asia Pacific is the fastest growing region at approximately 6.1% CAGR (2026–2033), driven by India's E20 blending mandate, China's national E10 policy, and rapid capacity expansion in ASEAN economies, reducing fossil fuel import dependence through biofuel programs.

- Dominant Application: Fuel Blending dominates the Application category with approximately 74% market share in 2025, anchored by government-mandated ethanol blending in gasoline across the U.S., Brazil, the EU, India, and China, collectively consuming the vast majority of global bio-ethanol output annually.

- Fastest Growing Feedstock Category: Cellulosic Feedstock is the fastest growing raw material segment, driven by U.S. DOE investment, IRA cellulosic biofuel tax credits, and Raízen's world-scale 2G sugarcane bagasse ethanol operations in Brazil, offering 80–90% lifecycle GHG reductions versus gasoline.

- Key Opportunity: The key market opportunity is the Sustainable Aviation Fuel (SAF) via the Alcohol-to-Jet (ATJ) pathway, driven by ICAO's CORSIA scheme, EU ReFuelEU Aviation mandates, and the U.S. IRA SAF tax credit, expected to create a structurally large new premium demand channel for advanced bio-ethanol through 2033 and beyond.

| Key Insights | Details |

|---|---|

|

Ethanol Market Size (2026E) |

US$ 98.7 Billion |

|

Market Value Forecast (2033F) |

US$ 134.3 Billion |

|

Projected Growth CAGR (2026–2033) |

4.5% |

|

Historical Market Growth (2020–2025) |

4.8% |

Market Dynamics

Drivers - Expanding Global Biofuel Blending Mandates and Renewable Fuel Standards

Mandatory biofuel blending policies remain the dominant structural demand driver for ethanol globally, with governments across major economies enforcing ethanol content requirements in transportation fuels to reduce greenhouse gas (GHG) emissions and fossil fuel dependence. The U.S. Renewable Fuel Standard (RFS), administered by the U.S. Environmental Protection Agency (EPA), mandated approximately 15 billion gallons of conventional ethanol blending in 2023, while Brazil's RenovaBio program and E27 mandate, requiring 27% anhydrous ethanol in gasoline, make it the world's most advanced ethanol economy, per the Brazilian National Agency of Petroleum, Natural Gas and Biofuels (ANP). The European Union's Renewable Energy Directive (RED III), which targets 42.5% renewable energy in transport by 2030, further compels ethanol demand expansion. India's Ethanol Blending Programme (EBP), targeting 20% ethanol blending by 2025–26, has driven domestic production investments exceeding INR 41,000 crore according to the Ministry of Petroleum and Natural Gas, reinforcing sustained long-term demand growth across the Asia Pacific corridor.

Rising Pharmaceutical, Personal Care, and Industrial Solvent Applications

Beyond fuel blending, the pharmaceutical and personal care industries represent the fastest-growing non-fuel demand vectors for high-purity ethanol. The COVID-19 pandemic-driven surge in hand sanitizer use permanently elevated baseline ethanol consumption in the healthcare and institutional disinfectant segment; the World Health Organization (WHO) recommends 60–80% ethanol-based formulations as the gold standard for hand hygiene. Industrial solvent applications, spanning coatings, adhesives, inks, and extraction processes, also register consistent demand, driven by tightening volatile organic compound (VOC) emission regulations under U.S. EPA and EU REACH frameworks that favor ethanol over petroleum-based solvents. The global pharmaceutical industry's expansion, with the International Federation of Pharmaceutical Manufacturers and Associations (IFPMA) documenting continued R&D expenditure growth, is steadily increasing consumption of pharmaceutical-grade ethanol in API synthesis, extraction, and excipient applications, providing a premium-priced, high-margin demand channel for quality ethanol producers.

Restraints - Food vs. Fuel Feedstock Competition and Price Volatility

The dominant starch- and sugar-based ethanol production pathways create direct competition with food and feed commodity markets, exposing producers to significant cost volatility and reputational risk. According to the Food and Agriculture Organization (FAO), the FAO Food Price Index surged to an all-time high in March 2022, intensifying political criticism of crop-based biofuel mandates. Corn and sugarcane, the two primary ethanol feedstocks in the U.S. and Brazil, respectively, are traded commodities subject to weather, geopolitical, and logistics shocks, causing unpredictable margin compression for ethanol producers during periods of feedstock inflation. This structural tension between food security and the continuity of biofuel policy represents a persistent risk to investor confidence and policy stability across major ethanol-producing markets.

Infrastructure Constraints for High-Blend Ethanol Distribution

The wider adoption of higher ethanol blends, such as E15, E85, and E100, is materially constrained by existing transportation fuel distribution infrastructure, including pipelines, storage tanks, and retail dispensing equipment that are incompatible with or require costly retrofitting for high-ethanol blends. In the United States, the U.S. Energy Information Administration (EIA) reports that E85 is available at fewer than 5,000 retail stations out of approximately 145,000 total fuel outlets, illustrating the distribution bottleneck. Corrosion of legacy pipeline infrastructure and fuel system components in older vehicles further limits consumer uptake, restraining blending volumes above E10 in most markets and capping near-term demand growth from the fuel blending segment.

Opportunities - Second-Generation Cellulosic Ethanol Commercialization

Cellulosic ethanol, derived from non-food agricultural residues, dedicated energy crops, and forestry waste, represents the most transformative long-term opportunity for the ethanol industry, offering lifecycle GHG emission reductions of 80–90% compared to gasoline, per the U.S. Department of Energy (DOE) Argonne National Laboratory. The U.S. EPA grants cellulosic ethanol a D3 Renewable Identification Number (RIN) with a higher value than conventional corn ethanol, providing a policy premium that incentivizes investment. POET LLC and DuPont have demonstrated commercial-scale cellulosic production, while Raízen S.A. operates the world's largest second-generation ethanol facility in Brazil, processing sugarcane bagasse. The U.S. DOE's Bioenergy Technologies Office (BETO) has committed over US$ 300 million to advanced biofuel demonstration projects since 2021. As technology costs decline and policy support strengthens under frameworks such as the U.S. Inflation Reduction Act (IRA) and cellulosic biofuel tax credits, this segment is poised to significantly expand the ethanol market's addressable volume and margin profile beyond the forecast horizon.

Sustainable Aviation Fuel (SAF) and Ethanol-to-Jet Pathway

The emerging Sustainable Aviation Fuel (SAF) market is creating a compelling new premium demand channel for ethanol through the Alcohol-to-Jet (ATJ) conversion pathway. International aviation's decarbonization imperative, driven by the International Civil Aviation Organization (ICAO)'s net-zero 2050 target under its CORSIA scheme and the European Union's ReFuelEU Aviation regulation mandating 2% SAF blending by 2025, rising to 70% by 2050, is compelling airlines and fuel suppliers to scale alternative jet fuel production. The U.S. IRA provides a US$ 1.25–1.75 per gallon SAF blending tax credit for qualifying low-carbon fuels, with ATJ-pathway ethanol meeting the required 50%+ lifecycle GHG reduction threshold. Valero Energy Corporation and LanzaJet (backed by British Airways and Shell) are actively scaling ATJ facilities. According to the International Air Transport Association (IATA), global SAF demand could reach 450 billion liters annually by 2050, creating a structurally massive new outlet for advanced bio-ethanol producers over the coming decades.

Category-wise Analysis

Product Type Insights

Bio-ethanol is the dominant product type in the global ethanol market, accounting for approximately 88% of total market share in 2025. Bio-ethanol's supremacy is entrenched by global biofuel policy mandates that explicitly require renewable-origin ethanol in transportation fuel blending programs; synthetic ethanol derived from petrochemical ethylene hydration cannot qualify under the U.S. RFS, Brazil's RenovaBio, or the EU's RED III framework. The Renewable Fuels Association (RFA) reported that U.S. ethanol producers alone generated over 15.8 billion gallons of bio-ethanol in 2023, accounting for the majority of the North American supply. Additionally, bio-ethanol carries a significantly lower carbon intensity than synthetic ethanol, making it the preferred input for pharmaceutical, food-grade, and personal care applications that increasingly demand sustainability credentials. Synthetic ethanol retains a niche position in specific industrial chemical synthesis applications where petrochemical-route economics remain competitive.

Raw Material Insights

Starch-Based feedstock, primarily corn in the United States and wheat and cassava in Asia and Europe, represents the leading raw material category, accounting for approximately 52% of global ethanol production in 2025. This dominance reflects the U.S.'s position as the world's largest ethanol producer, where corn-to-ethanol fermentation is a mature, cost-optimized process benefiting from extensive co-product (distillers' grains) revenue streams. According to the U.S. Department of Agriculture (USDA), approximately 38–40% of the U.S. corn crop is consumed by the ethanol industry annually, underscoring the segment's dominance in feedstock volume. Starch-to-ethanol conversion efficiency via enzymatic hydrolysis and yeast fermentation is well-established at an industrial scale, and improvements in enzyme technology by companies including Novozymes A/S and DuPont continue to incrementally improve starch-to-ethanol yields and reduce production costs, reinforcing the segment's market leadership position.

Application Insights

Fuel Blending is the dominant application of ethanol globally, accounting for approximately 74% of total consumption in 2025. The application's commanding share is a direct consequence of government-mandated biofuel policies in the world's largest economies. In the United States, fuel ethanol blended into the gasoline pool at the standard E10 (10% ethanol) rate accounts for the bulk of the ~15 billion gallons of annual consumption. Brazil, uniquely operating an E27 mandatory blend alongside a dedicated hydrous ethanol (E100) fuel for flex-fuel vehicles that account for over 80% of its new-car fleet, according to the National Association of Vehicle Manufacturers (ANFAVEA), is the world's most advanced fuel ethanol economy. India's rapidly scaling blending program (E20 target by 2025) and China's E10 national mandate are further broadening the global consumption base, cementing fuel blending as the decisive demand driver for the ethanol market through the forecast period.

Regional Insights

North America Ethanol Market Trends and Insights

North America is the world's largest ethanol-producing and consuming region, led overwhelmingly by the United States, which accounts for approximately 54% of global ethanol production according to the Renewable Fuels Association (RFA). The U.S. Renewable Fuel Standard (RFS2) remains the cornerstone of domestic demand, mandating multi-billion-gallon annual ethanol volumes blended into the gasoline supply. The U.S. EPA's approval of year-round E15 sales, effective from June 2023, and the U.S. IRA's Second-Generation Biofuel Plant tax credits are catalyzing new investment in cellulosic ethanol. Major producers POET LLC, Archer Daniels Midland Company (ADM), Valero Energy Corporation, and Green Plains Inc. collectively operate the world's most efficient corn-to-ethanol industrial complex, with ongoing carbon capture and sequestration (CCS) investments further reducing the carbon intensity of Midwest ethanol production.

Canada contributes to regional production through wheat and corn-based ethanol under the Canadian Renewable Fuels Regulations, which mandate a 5% average renewable content in gasoline. The region is also at the frontier of the SAF opportunity, with Valero Energy and ADM evaluating or executing Alcohol-to-Jet capacity investments supported by IRA SAF tax credits. The U.S. export market, shipping ethanol primarily to Canada, India, Brazil, and South Korea, further underscores North America's strategic position in the global ethanol trade, with the U.S. Energy Information Administration (EIA) reporting that annual fuel ethanol exports have consistently exceeded 1.5 billion gallons in recent years.

Europe Ethanol Market Trends and Insights

Europe's ethanol market is defined by a progressive regulatory framework focused on decarbonizing transportation, with the EU's Renewable Energy Directive (RED III) and the FuelEU Maritime regulation setting ambitious targets for ethanol-derived fuels. Germany is the largest European consumer, with a well-developed bioethanol supply chain anchored by Südzucker AG and its CropEnergies subsidiary, which operates some of Europe's most efficient wheat- and sugar beet-to-ethanol facilities. France, home to major producer Cristal Union, and Spain maintain active ethanol blending programs, while ePURE (European Renewable Ethanol Association) reports that European bioethanol delivered lifecycle GHG emissions 79% lower than those of fossil gasoline in 2022, strengthening the policy case for continued mandate support.

The United Kingdom, post-Brexit, maintains its E10 mandatory blend standard, in force since September 2021, which underpins stable demand for domestically produced and imported bioethanol. Regulatory harmonization across the EU's REACH framework and the European Chemicals Agency (ECHA) continues to favor bio-based ethanol in solvent and pharmaceutical applications, displacing petroleum-derived alternatives. The ReFuelEU Aviation mandate is creating a nascent SAF demand pull for ethanol-to-jet capacity, with Neste, TotalEnergies, and Repsol among the major energy companies evaluating ATJ investments to supply European aviation's growing SAF obligation through 2033 and beyond.

Asia Pacific Ethanol Market Trends and Insights

Asia Pacific is the fastest-growing ethanol market globally, projected to expand at a CAGR of approximately 6.1% from 2026 to 2033, driven by large-scale blending mandates in India and China, alongside robust industrial and pharmaceutical demand. China, the world's third-largest ethanol producer, operates a national E10 mandate covering all provinces, creating vast corn- and cassava-based ethanol consumption. According to China's National Development and Reform Commission (NDRC), bioethanol is a priority renewable fuel under the national energy transition strategy. Japan's cross-ministry Biofuel Action Plan supports ethanol blending and biojet fuel development, with the Ministry of Economy, Trade and Industry (METI) targeting SAF scale-up for the aviation sector.

India represents the region's most dynamic growth story: the government's Ethanol Blending Programme (EBP) successfully achieved an average blending of 12%+ in 2023–24 petrol, with a binding E20 target by 2025–26, according to the Ministry of Petroleum and Natural Gas. This policy ambition has triggered massive sugar-mill and grain distillery capacity expansion, supported by concessional loans administered through the Department of Food and Public Distribution. ASEAN nations, notably Thailand, Indonesia, and the Philippines, are implementing or expanding ethanol blending programs to reduce fossil fuel import dependence, with Thailand's E20 gasohol program and Indonesia's molasses-based bioethanol roadmap adding significant incremental regional volumes through the forecast period.

Competitive Landscape

The global ethanol market exhibits a moderately consolidated structure, with a limited number of large-scale integrated producers accounting for a substantial share of global output, particularly in North America and Brazil. These players benefit from large processing capacities, strong feedstock supply networks, and established distribution channels. In contrast, the Asian market remains relatively fragmented, characterized by a mix of state-backed enterprises and regional private producers primarily focused on domestic fuel blending programs and industrial alcohol supply.

Competitive differentiation increasingly revolves around feedstock diversification, operational efficiency, and value maximization from co-products such as distillers dried grains with solubles (DDGS). Many producers are investing in carbon intensity reduction through energy efficiency improvements, renewable power usage, and carbon capture integration to align with evolving regulatory frameworks. Additionally, companies are pursuing strategic diversification into second-generation ethanol technologies and sustainable aviation fuel pathways. Long-term offtake agreements with aviation and energy companies, along with expansion into higher-value biochemical and specialty alcohol segments, are emerging as key strategies to stabilize margins and reduce exposure to volatility in fuel ethanol markets.

Key Developments:

- March, 2026: Gayatri Renewable Energy launched a INR 2.6 billion ethanol plant project at the IFFCO Kisan Special Economic Zone in Kovur, Andhra Pradesh, aimed at boosting ethanol blending supply, supporting local grain procurement, and generating around 200 direct jobs and 500–700 indirect employment opportunities.

- January, 2026: LanzaTech Global announced plans to build a next-generation ethanol facility in Uttar Pradesh, India, in partnership with Spray Engineering Devices, utilizing sugarcane bagasse to produce sustainable fuels and chemicals while supporting India’s advanced biofuel initiatives under the PM JI-VAN program.

- January, 2026: Gevo, Inc. secured a new U.S. patent for its Ethanol-to-Olefins (ETO) technology, strengthening its renewable fuel portfolio and enabling ethanol conversion into light olefins for sustainable aviation fuel and chemicals with up to 35% lower capital and operating costs.

Companies Covered in Ethanol Market

- Archer Daniels Midland Company (ADM)

- POET LLC

- Valero Energy Corporation

- Green Plains Inc.

- The Andersons Inc.

- Raízen S.A.

- Copersucar

- Tereos Group

- Louis Dreyfus Company

- Bunge Limited

- Wilmar International

- COFCO Corporation

- China Resources Alcohol Corporation

- Südzucker AG (CropEnergies)

- Cristal Union

- Pacific Ethanol (Alto Ingredients, Inc.)

- Novozymes A/S

- LanzaJet Inc.

Frequently Asked Questions

The global ethanol market is estimated at US$ 98.7 billion in 2026 and is projected to reach US$ 134.3 billion by 2033, driven by biofuel blending mandates and steady demand from pharmaceutical, personal care, food, and industrial solvent applications.

Key demand drivers include government biofuel blending mandates, expanding pharmaceutical and disinfectant applications, and emerging demand from sustainable aviation fuel production via alcohol-to-jet pathways.

North America leads the global ethanol market, primarily due to the United States’ large corn-ethanol production base and strong biofuel blending policies.

A major growth opportunity lies in sustainable aviation fuel production through the alcohol-to-jet conversion pathway and the expansion of second-generation cellulosic ethanol technologies.

Major market participants include POET LLC, Archer Daniels Midland Company, Raízen S.A., Copersucar, Tereos Group, Südzucker AG, COFCO Corporation, and Valero Energy Corporation.