- Electric Mobility

- Electric Vehicle Battery Swapping Market

Electric Vehicle Battery Swapping Market Size, Share, and Growth Forecast 2026 - 2033

Electric Vehicle Battery Swapping Market by Service Type (Subscription Model, Pay-per-Use Model), by Vehicle Type (Two-Wheeler, Three-Wheeler, Passenger Cars (Four-Wheeler), Commercial Vehicles), Station Type (Automated, Manual), and Regional Analysis, 2026 - 2033

Electric Vehicle Battery Swapping Market Size and Trend Analysis

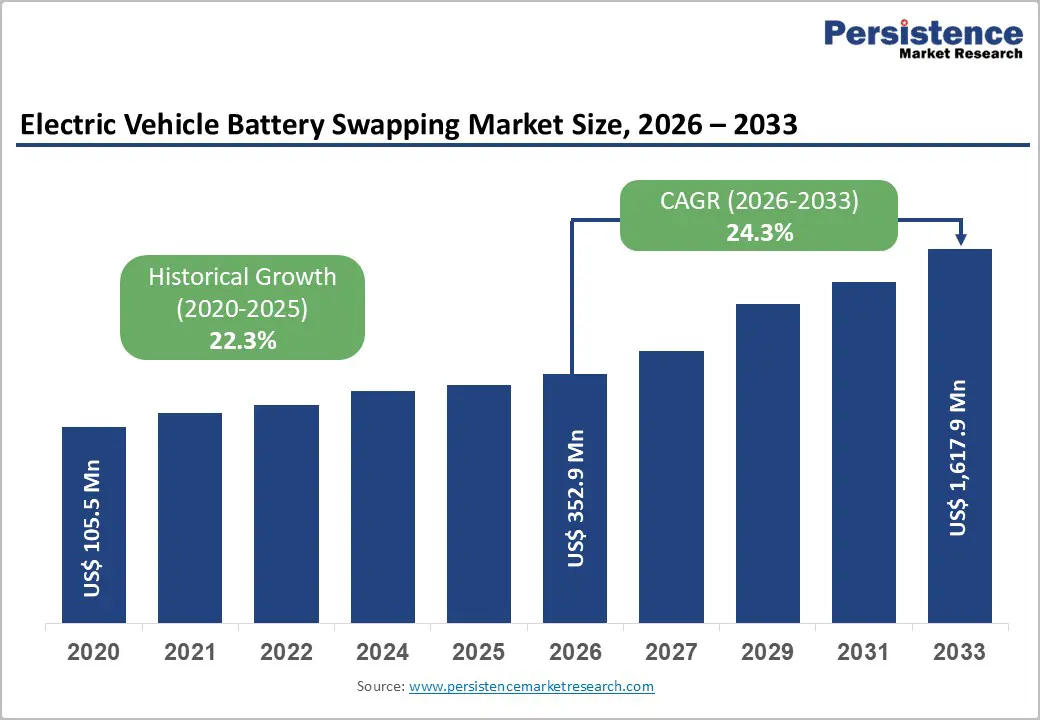

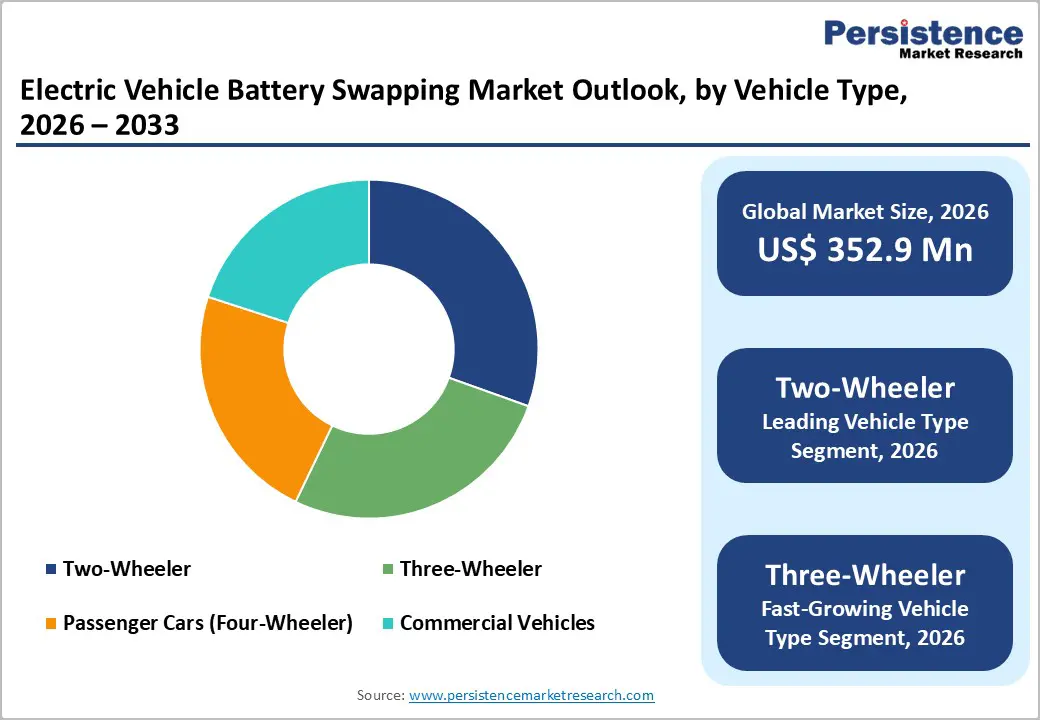

The global Electric Vehicle Battery Swapping Market size is expected to be valued at US$ 352.9 million in 2026 and projected to reach US$ 1,617.9 million by 2033, growing at a CAGR of 24.3% between 2026 and 2033.

Rapid adoption of electric vehicles, coupled with government mandates for zero-emission transport, is driving demand for efficient battery solutions. Swapping infrastructure reduces refueling times to under five minutes compared to conventional charging, minimizing vehicle downtime by up to 70%. With over 14 million EVs expected globally by 2024, battery swapping is becoming critical for fleets and shared mobility, addressing range anxiety and operational efficiency.

Key Industry Highlights:

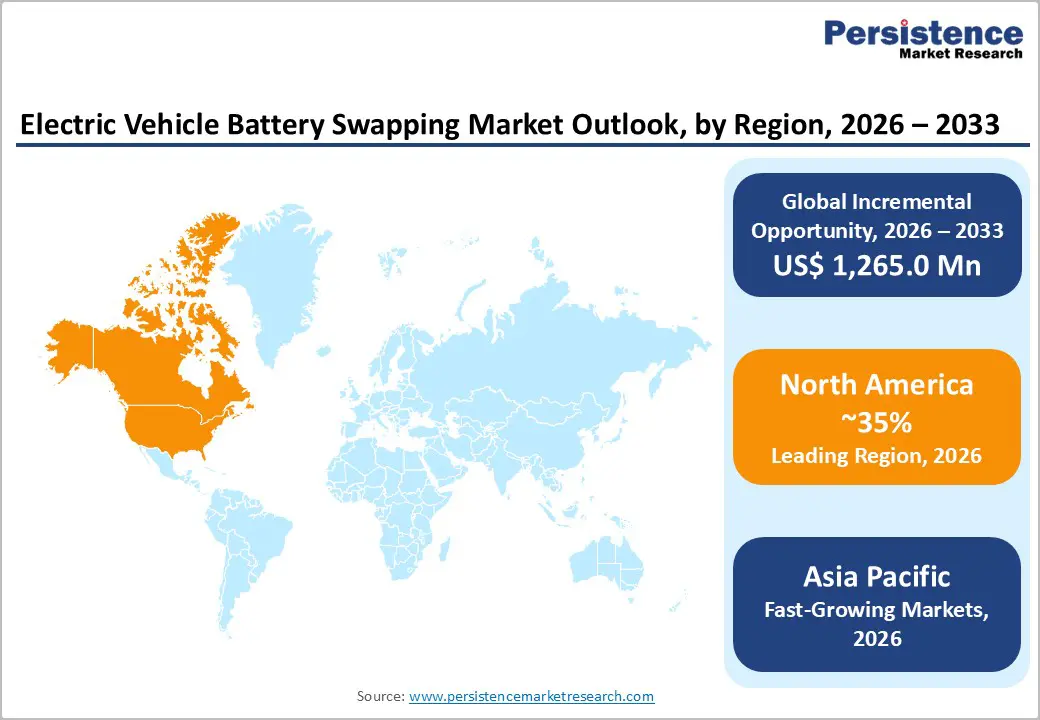

- Leading Region: North America leads with 35% share in 2025, supported by government funding, pilot programs, and advanced fleet deployments.

- Fastest-Growing Region: Asia Pacific grows fastest at 28% CAGR, fueled by two- and three-wheeler adoption and expanding infrastructure.

- Leading Service Type Category: Pay-per-Use dominates the service segment with a 56% share, preferred for flexibility and minimal upfront fees.

- Leading Vehicle Type Category: Two-wheelers lead vehicle adoption with 45% share, driven by urban fleet demand and high operational efficiency.

- Key Market Opportunity: Commercial fleets present major growth potential, with initiatives targeting 50% electrification, enabling rapid swapping adoption and reduced downtime.

| Key Insights | Details |

|---|---|

|

Electric Vehicle Battery Swapping Size (2026E) |

US$ 352.9 million |

|

Market Value Forecast (2033F) |

US$ 1,617.9 million |

|

Projected Growth CAGR(2026-2033) |

24.3% |

|

Historical Market Growth (2020-2025) |

22.3% |

DRO Analysis

Drivers - Rapid EV Adoption Boosting Demand for Battery Swapping

Global electric vehicle adoption is accelerating, with over 14 million EVs on roads by 2024, creating a pressing need for fast and reliable refueling solutions. Battery swapping reduces charging times to under five minutes compared to traditional 60-minute charging, minimizing downtime and improving fleet efficiency.

In Asia, two-wheelers dominate urban mobility, and compact swapping systems have demonstrated up to 95% operational efficiency in pilot programs. With EVs projected to reach 250 million by 2030, the demand for swapping stations is expected to grow significantly, supporting fleets, shared mobility, and high-usage commercial operations while addressing range anxiety effectively.

Government Policies and Incentives Driving Battery Swapping Growth

Supportive government mandates and incentives are accelerating the adoption of battery swapping infrastructure. China requires swap-compatible fleets, resulting in over 10,000 operational stations, while India targets 30% e-two-wheeler penetration by 2030, providing financial support to operators.

Europe’s Alternative Fuels Infrastructure Regulation reduces upfront costs for networks by roughly 40%, lowering capital barriers and encouraging investment. These policies cut operator expenses, enable faster deployment, and have historically driven substantial market expansion, positioning battery swapping as a key solution for sustainable urban mobility and large-scale fleet electrification.

Restraints - High Initial Infrastructure Costs Limiting Market Expansion

Battery swapping stations require substantial capital investment, with individual setups costing between US$ 500,000 and US$ 1 million. Pilot programs have highlighted these high upfront costs as a significant barrier for new operators. Additionally, only a small fraction of electric vehicles around 10% are swap-ready, and retrofitting existing vehicles adds an extra 20–30% to expenses, slowing the overall adoption of swapping infrastructure.

These high initial costs make network expansion challenging, especially in emerging markets with limited financing options. Operators must balance return on investment with operational efficiency, which can delay large-scale deployment. This restraint continues to limit the speed at which battery swapping networks can scale globally despite growing EV adoption.

Battery Standardization Gaps Hindering Efficient Deployment

The lack of standardization across EV batteries poses another major challenge for the swapping market. With over 50 different battery formats in use, interoperability issues create roughly 25% inefficiencies in station operations. Divergent regulations and design standards, particularly in regions like Europe, slow down the rollout of uniform swapping networks and complicate infrastructure planning.

These gaps require operators to either maintain multiple battery types or retrofit vehicles to fit specific stations, increasing operational costs and limiting scalability. Until industry-wide standardization improves, deployment speed and cost-effectiveness will remain key constraints on market growth.

Opportunities - Rapid Two-Wheeler and Three-Wheeler Growth Creating Swapping Opportunities

Asia Pacific’s electric two- and three-wheeler segment dominates with over 60% market share, driven by rising urban mobility needs. In India, e-two-wheeler sales jumped 148% year-on-year to reach 1 million units, highlighting strong adoption. Battery swapping reduces operational costs by up to 40%, while pilot programs by companies like Gogoro and Sun Mobility have already served over 25,000 users, proving scalability and efficiency.

Government initiatives such as India’s FAME-III scheme further amplify demand by incentivizing EV adoption and supporting infrastructure expansion. The growing population of compact EVs presents a lucrative opportunity for operators to deploy dedicated swapping networks, especially in high-density urban centers where downtime reduction and operational efficiency are critical.

Commercial Fleet Electrification Driving Battery Swapping Market Expansion

Electrification of commercial fleets presents significant growth potential for battery swapping networks. China’s Green Freight initiative targets 50% electric truck penetration by 2030, while the US funds pilots worth US$50 million to reduce vehicle downtime by up to 90%, demonstrating strong policy support for fleets.

Companies like Voltera and Ample have demonstrated swapping solutions for long-haul logistics, proving operational viability. As fleet operators seek to maintain high utilization while transitioning to electric vehicles, battery swapping offers faster refueling and predictable performance, creating substantial opportunities in urban delivery, intercity transport, and logistics sectors worldwide.

Category-wise Analysis

Service Type Insights

The pay-per-use model dominates the service type segment with a 56% share in 2025, favored for its flexibility and zero upfront fees. Urban individual users prefer this model for convenience and cost-effectiveness, contributing most of the revenue in city deployments. Subscription services remain significant for fleets, offering predictable monthly costs, integrated battery management, and operational reliability across multiple vehicles.

Subscription models are the fastest-growing segment, driven by fleet adoption in logistics, delivery, and ride-sharing services. Predictable expenses, reduced downtime, and easier battery lifecycle management make subscription attractive for large-scale operations. Operators can efficiently scale their networks while ensuring high vehicle availability and service continuity, especially for commercial and shared mobility use cases.

Vehicle Type Insights

Two-wheelers lead the vehicle type segment with a 45% share, driven by Asia Pacific urban fleets. India’s VAHAN database records over 2 million electric two-wheeler registrations, and pilots like Zypp report 95% uptime using swapping stations. Compact stations, costing roughly 40% less than four-wheeler stations, support high adoption rates and enable efficient city deployment, particularly for short-distance commuting and last-mile delivery.

Three-wheelers and passenger cars are the fastest-growing categories, supported by delivery fleets, ride-hailing, and urban shared mobility programs. Swapping reduces downtime and operational costs for these vehicles, allowing operators to scale fleets efficiently. Growing adoption in densely populated cities highlights the potential for expanded swapping infrastructure to serve multiple vehicle types.

Station Type Insights

Automated stations hold a 60% market share, driven by high throughput, reliability, and robotics-based error-free operations. Gogoro stations, for example, handle up to 300 swaps per day per site with 98% accuracy. IoT integration enables real-time monitoring, predictive maintenance, and scalable network operations, making automated stations ideal for commercial fleets and high-usage urban deployments.

Manual stations are the fastest-growing segment, favored in emerging markets and smaller cities due to lower upfront costs and easier setup. These stations allow flexible expansion where full automation is not feasible, enabling operators to test markets, expand coverage, and support EV adoption without heavy initial investment, particularly for low-density or suburban areas.

Regional Insights

North America Electric Vehicle Battery Swapping Market Trends

North America holds a 35% share of the global EV battery swapping market, driven by strong government funding and pilot programs. The US DOE’s Bipartisan Infrastructure Law allocates US$5 billion through NEVI for EV infrastructure, while California and Texas benefit from US$50 million in CEC-funded truck pilot programs. Companies like Ample and Voltera have reduced truck downtime to just 10 minutes, improving fleet efficiency and operational reliability.

Silicon Valley serves as an innovation hub, pushing modular swapping technologies and automation solutions. The combination of government support, private innovation, and a growing commercial EV fleet positions North America as a key leader in swapping network deployment, particularly for high-utilization fleets and long-haul logistics operations.

Europe Electric Vehicle Battery Swapping Market Trends

Europe is experiencing steady adoption of battery swapping infrastructure, with Germany leading through NIO’s support for DIN battery standards and 59 operational stations. The Alternative Fuels Infrastructure Regulation (AFIR) mandates 1 million swap points, while France’s ADEME initiatives show 20% fleet success, and Spain aligns ports with the Fit for 55 program. The region is projected to grow at a 28% CAGR through 2033, driven by emissions regulations and fleet electrification.

Emerging standardization and government incentives are accelerating network expansion, particularly for urban fleets and public transport operators. Modular designs and interoperable stations are enabling scalable deployment across multiple countries, ensuring consistent performance while reducing investment barriers and operational downtime for commercial fleets.

Asia Pacific Electric Vehicle Battery Swapping Market Trends

Asia Pacific is the fastest-growing region with a 28% CAGR, driven by China, India, Japan, and ASEAN countries. China has over 10,000 stations through collaborations like CATL-NIO, while India’s Ola and Hero plans target 10,000 stations by 2025, guided by Ministry regulations. Japan’s Gogoro model and ASEAN’s manufacturing advantages reduce logistics costs by up to 50%, supporting rapid fleet adoption.

Two and three-wheelers dominate urban transport, and high population density increases swapping demand. Government incentives, robust EV adoption, and local manufacturing capabilities create a favorable environment for network expansion, positioning Asia Pacific as the global leader in high-volume, cost-efficient, and scalable battery swapping infrastructure.

Competitive Landscape

The global battery swapping market is highly fragmented, with numerous players competing to offer innovative and efficient solutions. Key strategies focus on Battery-as-a-Service models and AI-enabled automation to reduce swap times to under three minutes. Operators differentiate themselves through interoperability across multiple vehicle types and the integration of hybrid stations combining manual and automated processes, enhancing flexibility and coverage.

Emerging trends emphasize serving commercial fleets and shared mobility networks, where uptime and predictability are critical. Additionally, the adoption of second-life batteries for swapping networks is gaining traction, lowering costs and supporting sustainability while extending battery lifecycle management across the ecosystem.

Key Developments:

- In June 2025, NIO launched its 1,000th battery swapping station in China, achieving 25 million swaps, reflecting rapid infrastructure expansion and strong adoption among urban fleets and shared mobility users.

- In August 2024, Sun Mobility partnered with Veera to enable heavy electric vehicle battery swaps in under three minutes, advancing high-capacity swapping technology and minimizing downtime for commercial and logistics fleets.

- In February 2025, NIO contributed to establishing the DIN battery swapping standard in Germany, promoting interoperability, regulatory alignment, and standardized deployment of battery swapping networks across European markets.

Companies Covered in Electric Vehicle Battery Swapping Market

- NIO Inc.

- Gogoro Inc.

- Ample Inc.

- SUN Mobility

- China Tower Corporation

- BYD Co. Ltd.

- Contemporary Amperex Technology Co. Limited (CATL)

- KYMCO (Kwang Yang Motor Co.)

- Honda Motor Co., Ltd.

- Panasonic Corporation

- Battery Smart

- Swobbee GmbH

- Ampersand

- Oyika Pte Ltd.

- Lithion Power Pvt. Ltd.

Frequently Asked Questions

The market is valued at US$ 352.9 million in 2026, projected to reach US$ 1,617.9 million by 2033 at 24.3% CAGR.

Rapid EV adoption with 14 million units globally by 2024 and <5-minute swap times compared to conventional charging drive demand.

North America leads with 35% share in 2025, supported by government programs, pilot fleets, and advanced swapping infrastructure.

Commercial fleets and two-/three-wheelers offer growth potential, with 50% electrification targets and operational cost savings up to 40%.

Key companies include NIO, CATL, Gogoro, Ample, and Sun Mobility.