- Electric Mobility

- Electric Vehicle Plastics Market

Electric Vehicle Plastics Market Size, Share, and Growth Forecast 2026 - 2033

Electric Vehicle Plastics Market by Polymer Type (Polypropylene (PP), Polyurethane (PU), Polyamide (PA/Nylon), Polyvinyl Chloride (PVC), Acrylonitrile Butadiene Styrene (ABS), Polycarbonate (PC), Polybutylene Terephthalate (PBT), Polyethylene (PE), Others), Vehicle Type (Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), Hybrid Electric Vehicles (HEV), Fuel Cell Electric Vehicles (FCEV)), Components (Steering & Dashboards, Car Upholstery, Bumper, Door Assembly, Exterior & Interior Trim, Connector and Cables, Battery, Lighting, Electric Wiring, Others), Application, and Regional Analysis, 2026 - 2033

Electric Vehicle Plastics Market Size and Trend Analysis

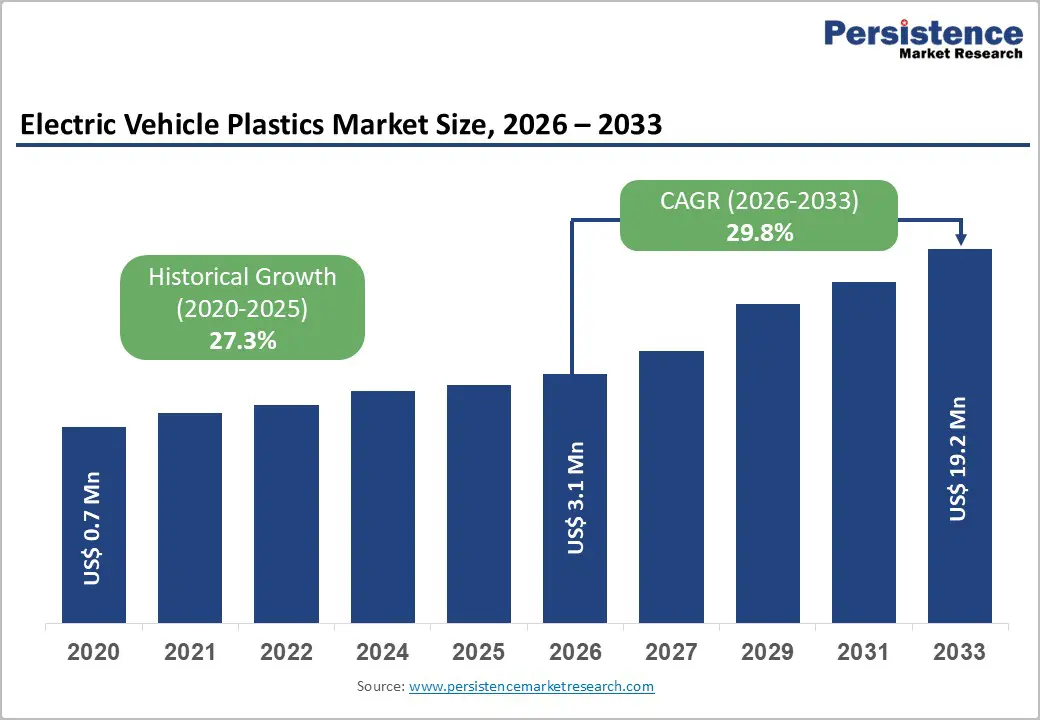

The global Electric Vehicle Plastics market size is expected to be valued at US$ 3.1 Billion in 2026 and projected to reach US$ 19.2 Billion by 2033, growing at an exceptional CAGR of 29.8% between 2026 and 2033.

Explosive growth in global electric vehicle adoption, accelerating EV platform proliferation, and the critical role of engineering plastics in enabling vehicle lightweighting, battery thermal management, and high-voltage electrical insulation are the principal forces driving this extraordinary market trajectory. According to the International Energy Agency (IEA), global EV sales surpassed 14 million units in 2023, representing over 18% of all new car sales globally, and EV stocks on the road are projected to reach 240 million by 2030. Each battery electric vehicle incorporates between 150–200 kg of engineering plastics, significantly more than equivalent internal combustion engine vehicles, across battery housings, thermal management systems, high-voltage connectors, interior panels, and structural components. Ambitious EV sales mandates across the European Union, United States, and China are reinforcing long-run demand certainty for advanced polymer suppliers to the EV supply chain.

Key Industry Highlights:

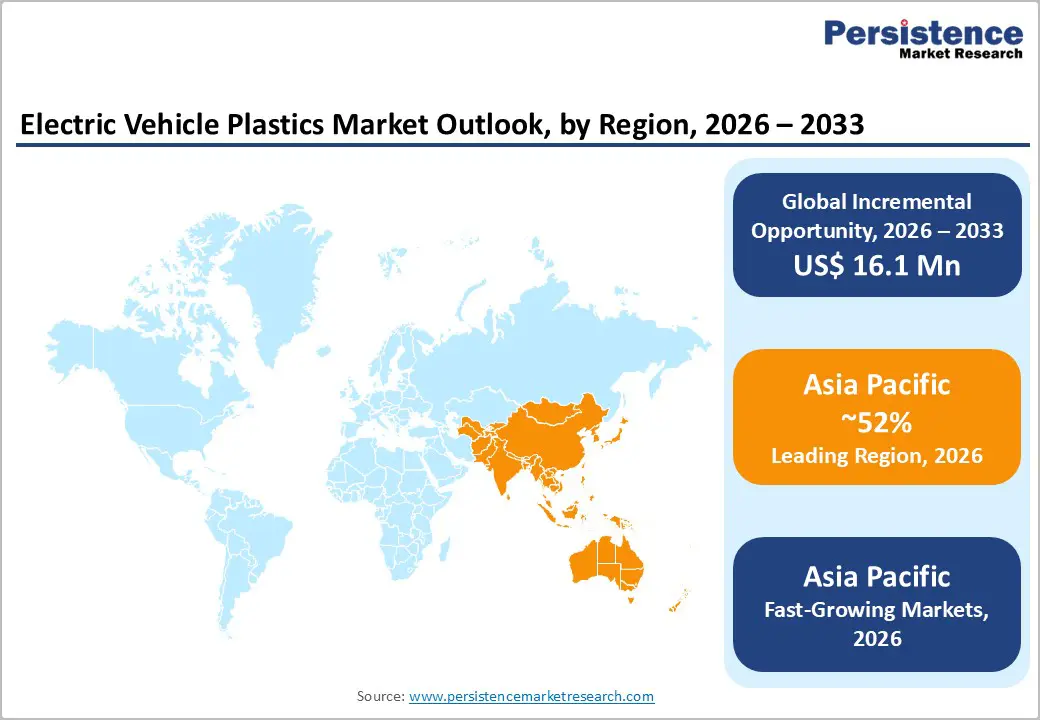

- Leading Region: Asia Pacific commands approximately 52% of global EV Plastics market revenue in 2025, anchored by China's production of over 9.6 million NEVs in 2023 per CAAM data, with India and Japan driving accelerating regional sub-market growth.

- Fastest Growing Region: India is the fastest growing EV plastics sub-market, projected to expand at over 35% CAGR through 2033, driven by PLI automotive incentives, FAME II EV subsidies, and localization of EV production by Tata Motors and Mahindra Electric.

- Dominant Segment: BEVs command approximately 58% of EV Plastics market share in 2025, incorporating 150–200 kg of engineering plastics per vehicle across battery housings, high-voltage connectors, thermal management systems, and interior structures, significantly exceeding ICE vehicle plastic content.

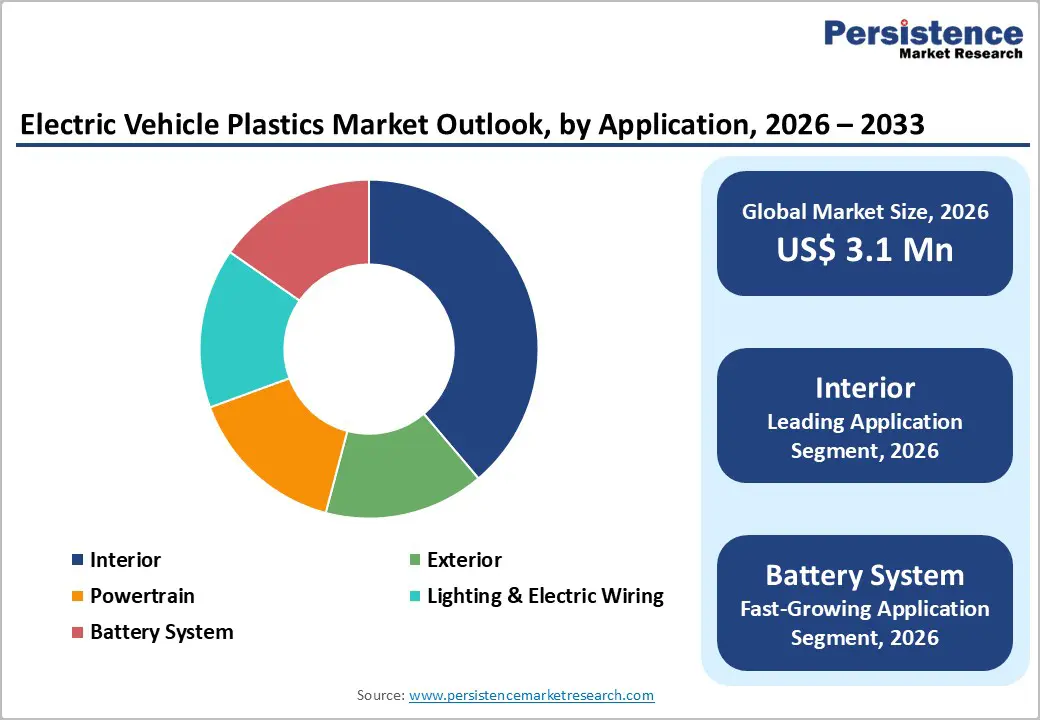

- Fastest Growing Segment: The Battery System application is the fastest growing category, as CTP and CTB battery architectures deployed by Tesla, BYD, and CATL require polymer-intensive structural integration systems replacing conventional aluminum module frameworks.

- Key Market Opportunity: The automotive transition to 800V EV platforms, projected to cover over 40% of new BEV launches by 2027 per IEA, is creating premium demand for high-voltage dielectric specialty polymers from Covestro, LANXESS, and EMS-Chemie.

| Key Insights | Details |

|---|---|

|

Electric Vehicle Plastics Market Size (2026E) |

US$ 3.1 Billion |

|

Market Value Forecast (2033F) |

US$ 19.2 Billion |

|

Projected Growth CAGR (2026–2033) |

29.8% |

|

Historical Market Growth (2020–2025) |

27.3% CAGR |

Market Dynamics

Drivers - Unprecedented Global EV Adoption Driven by Government Policy Mandates and Emission Regulations

Stringent government emission targets and direct EV adoption mandates are the foundational macro-driver for EV plastics demand. The European Union's regulation mandating zero CO2 emissions from new passenger cars by 2035 effectively requires all new vehicle sales to be electric from that date. The U.S. EPA's vehicle emission standards finalized in March 2024 project that EVs will account for 56% of new light-duty vehicle sales by 2032. China's New Energy Vehicle (NEV) dual credit policy already drove NEV penetration to 31% of domestic auto sales in 2023 according to the China Association of Automobile Manufacturers (CAAM). These binding policy frameworks create a compounding demand trajectory for EV-specific engineering plastics across all major vehicle production markets, underpinning the market's exceptional forecast CAGR.

EV Lightweighting Imperative Driving Engineering Plastics Content Per Vehicle

Reducing vehicle weight is a critical strategy for maximizing EV driving range, every 100 kg reduction in vehicle mass improves range by approximately 10–15% according to the European Automobile Manufacturers' Association (ACEA). Engineering plastics are the primary material enabling this lightweighting, replacing metals across structural panels, battery enclosures, seat frames, and powertrain housings at 30–60% weight savings per component. The average plastic content in a BEV is approximately 20% higher than an equivalent ICE vehicle due to the addition of battery thermal management housings, high-voltage connector systems, and EV-specific interior applications. BASF SE reports that its Ultramid (PA) engineering plastics are increasingly specified for EV battery module frames and cooling channel applications, displacing traditional aluminum assemblies and providing both weight and processing cost advantages.

Restraints - High Performance Specification Requirements Increasing Polymer Development Costs

EV applications impose demanding performance requirements on engineering plastics far exceeding those of conventional automotive applications. Battery system components require plastics that maintain structural integrity at operating temperatures between -40°C and +130°C, withstand high-voltage dielectric stresses up to 800V in next-generation platforms, and comply with UL 94 V-0 flame retardancy standards. Developing, testing, and qualifying new polymer grades to these specifications requires multi-year R&D cycles and substantial capital investment, creating barriers to market entry for smaller specialty polymer producers and extending the time-to-revenue for new product platforms.

Supply Chain Concentration Risks in Critical Polymer Precursor Materials

Several high-performance engineering plastics critical for EV applications, including Polyphenylene Sulfide (PPS) and specialty Polyamide 12 (PA12), depend on geographically concentrated precursor chemical supply chains. The 2021 Evonik Marl plant explosion caused a global PA12 shortage that disrupted automotive production across Europe and North America for several months, highlighting supply chain fragility. As EV production scales exponentially, single-source dependency risks for critical polymer precursors could create supply disruptions and cost volatility that impact OEM production schedules and polymer price stability.

Opportunities - Next-Generation Battery System Plastics for High-Voltage 800V EV Architectures

The automotive industry's rapid transition to 800-volt electrical architectures in next-generation BEV platforms is creating a high-value specialty polymer opportunity. Vehicles including the Hyundai Ioniq 6, Porsche Taycan, and Kia EV6 already employ 800V systems enabling ultra-fast charging at rates exceeding 350 kW. These architectures demand plastic components with enhanced dielectric strength, tracking resistance (CTI), and dimensional stability under high thermal and electrical cycling stresses. Covestro AG and LANXESS have both developed dedicated high-voltage connector and busbar polymer grades targeting the 800V platform opportunity. The IEA projects that EV models with 800V architecture will represent over 40% of new BEV launches by 2027, creating a rapidly expanding addressable market for premium engineered dielectric polymers.

Structural Battery Integration and Cell-to-Pack Plastics Innovation

The emerging cell-to-pack (CTP) and cell-to-body (CTB) battery integration architectures, pioneered by Tesla, BYD, and CATL, are creating transformative new opportunities for structural engineering plastics in battery enclosure, thermal management, and module separation applications. CTP architectures eliminate conventional battery module frameworks, requiring new polymer systems that simultaneously provide structural load-bearing capability, thermal conductivity, flame retardancy, and electrical insulation within the same component. BASF SE's Ultramid Structure and Celanese Corp.'s Fortron PPS grades are specifically positioned for CTP structural applications. With CTP-based EVs projected to account for over 50% of new BEV production by 2028 according to BloombergNEF, this architecture shift represents a landmark growth opportunity for advanced polymer innovators in the EV plastics value chain.

Category-wise Analysis

Polymer Type Insights

Polypropylene (PP) is the leading polymer type in the global EV plastics market, commanding approximately 22% of total market share in 2025. PP's dominance reflects its versatility across a broad range of EV interior, exterior, and underbody applications, from door panels and instrument panels to wheel arch liners and battery tray structural elements. PP offers an excellent balance of stiffness, impact resistance, chemical resistance, and processability at competitive cost, making it the highest-volume polymer in automotive manufacturing overall. Long glass fiber reinforced PP (LGF-PP) grades are increasingly specified for structural EV applications requiring higher rigidity. LyondellBasell and SABIC are leading suppliers of automotive PP compounds targeting EV OEMs. Polyamide (PA/Nylon) is the fastest growing polymer type, driven by its critical role in high-temperature battery housings, high-voltage connectors, and thermal management components demanding superior heat resistance and chemical stability.

Vehicle Type Analysis

Battery Electric Vehicles (BEVs) represent the dominant vehicle type segment in the global EV plastics market, accounting for approximately 58% of total market share in 2025. BEVs incorporate the highest plastics content per vehicle among all EV architectures, driven by the complexity of their battery management systems, high-voltage electrical architectures, and the absence of an internal combustion engine powertrain enabling novel cabin and floor structure designs that utilize engineering plastics. According to the IEA, BEV sales reached 9.7 million units in 2023, representing the fastest-growing vehicle category globally. The BEV segment's share of total EV plastics revenue will continue to expand as pure-electric platforms from Tesla, BYD, Volkswagen, and General Motors ramp to mass production volumes. Fuel Cell Electric Vehicles (FCEVs) are the fastest growing vehicle segment given their emerging commercial scaling.

Components Insights

The Battery component segment is the leading category in EV plastics by components, representing approximately 28% of total revenue share in 2025. Battery system plastics encompass cell holders, module frames, pack enclosures, thermal management manifolds, busbars insulation, and compression pads, all requiring engineered polymer grades with precisely calibrated thermal, mechanical, dielectric, and flame retardancy properties. The global EV battery market, with installed capacity exceeding 750 GWh in 2023 according to the International Energy Agency, is a direct multiplier for battery plastics demand. Each 1 GWh of battery production requires substantial volumes of PA, PBT, PC, and PPS polymer components. Connectors and Cables is the fastest growing component segment, driven by the increasing electrical content per EV with 800V architectures requiring more high-performance connector insulation materials.

Application Insights

Interior application is the leading segment in the global EV plastics market, accounting for approximately 32% of total revenue share in 2025. EV interiors rely extensively on engineering plastics for instrument panels, center consoles, door trims, seat structures, headliners, and floor systems, applications where plastics deliver both functional performance and aesthetic design freedom unavailable with metal alternatives. EV OEMs are also investing in premium sustainable interior material systems, driving demand for bio-based and recycled content engineering plastics meeting automotive tactile and aesthetic standards. Covestro AG's polycarbonate blends and BASF's Ultramid polyamide grades are extensively specified in EV interior structural components across major OEMs. The Battery System application is the fastest growing segment, with plastics consumption per EV battery growing exponentially as cell-to-pack architectures replace modular assemblies with polymer-intensive structural integration designs.

Regional Insights

North America Electric Vehicle Plastics Market Trends and Insights

North America is the second largest regional market for EV plastics, propelled by the rapid scaling of domestic EV manufacturing capacity catalyzed by the U.S. Inflation Reduction Act (IRA)'s clean vehicle tax credits and domestic content requirements. The IRA's US$ 7,500 EV consumer tax credit, contingent on domestic battery material sourcing thresholds, is accelerating North American EV and battery supply chain localization, directly stimulating demand for domestically supplied engineering plastics. Tesla's Gigafactory Texas, GM's Ultium platform plants, and Ford's BlueOval City investments collectively represent over US$ 40 billion in EV manufacturing capacity additions, each requiring regional polymer supply chains.

The U.S. plastics innovation ecosystem, anchored by BASF SE, DuPont, and Celanese Corp. regional technical centers, is rapidly developing EV-specific polymer grades for battery systems, high-voltage connectors, and thermal management applications. The U.S. EPA vehicle emission standards finalized in 2024 projecting 56% EV sales penetration by 2032, provide strong policy certainty for long-term engineering plastics investment decisions by both OEMs and Tier 1 automotive suppliers across the North American supply chain.

Europe Electric Vehicle Plastics Market Trends and Insights

Europe is the most regulatory-driven EV plastics market globally, shaped by the EU's 2035 zero-emission new car mandate and the European Green Deal framework requiring deep automotive sector decarbonization. Germany leads regional EV plastics demand as the continent's largest vehicle manufacturing nation, with Volkswagen Group, BMW Group, and Mercedes-Benz collectively producing millions of BEV and PHEV units annually on dedicated EV platforms requiring engineering plastics across battery, interior, exterior, and powertrain applications. BASF SE (Germany), Covestro AG (Germany), and LANXESS (Germany) serve as the European OEM supply chain's core engineering polymer providers.

France's Renault Group and Stellantis are scaling affordable BEV platforms using cost-optimized engineering plastic systems, while the United Kingdom's ZEV Mandate requiring 80% zero-emission new car sales by 2030 is accelerating domestic EV adoption timelines. Spain's automotive sector, with Volkswagen and SEAT/CUPRA expanding EV production, is driving regional plastics demand growth. The EU End-of-Life Vehicles (ELV) Regulation revision requiring mandatory recycled plastic content in new vehicles is also creating demand for recycled-content engineering polymer grades from SABIC and LyondellBasell.

Asia Pacific Electric Vehicle Plastics Market Trends and Insights

Asia Pacific is the leading regional market for EV plastics, commanding approximately 52% of global revenue share in 2025, driven by China's overwhelming dominance as both the world's largest EV production and consumption market. China produced over 9.6 million NEVs in 2023 according to the China Association of Automobile Manufacturers (CAAM), accounting for approximately 60% of global EV output. Domestic EV champions BYD, SAIC, and NIO are consuming enormous polymer volumes, with LG Chem, Sumitomo Chemicals, and Asahi Kasei expanding Asian production capacity to serve surging demand.

India is the fastest growing sub-regional EV plastics market, projected to expand at over 35% CAGR through 2033, supported by the Indian government's PLI scheme for Automobile and Auto Components and FAME II subsidies incentivizing EV adoption. Tata Motors and Mahindra Electric are localizing EV production, creating Indian supply chain opportunities for engineering polymer producers. Japan's Toyota, Honda, and Nissan are accelerating BEV platform launches, driving domestic engineering plastics demand. Asahi Kasei and Mitsubishi Engineering Plastics Corp. are well-positioned to capture Japan's growing EV plastics demand through their established OEM relationships.

Competitive Landscape

The global electric vehicle plastics market demonstrates a moderately consolidated structure, led by large specialty polymer manufacturers with diversified engineering plastics portfolios tailored for electric mobility applications. These companies benefit from strong research and development capabilities, established relationships with automotive OEMs, and the ability to supply high-performance polymers that meet stringent requirements for thermal stability, electrical insulation, flame retardancy, and lightweight structural performance.

Competition in the market is largely driven by innovation in advanced engineering polymers and the ability to secure long-term material qualifications with electric vehicle manufacturers and battery producers. Companies increasingly focus on collaborative product development with automotive suppliers to design integrated polymer solutions for battery systems, connectors, and structural components. Strategic priorities also include expanding production capacities near emerging EV manufacturing hubs and gigafactories to ensure reliable supply chains. Additionally, manufacturers are investing in sustainable polymer solutions, including recyclable and low-carbon materials, to align with evolving circular economy regulations and sustainability commitments across the automotive industry.

Key Developments:

- December 2025: Honda Motor Co. adopted DURABIO™, a bio-based engineering plastic developed by Mitsubishi Chemical, for the instrument panels of its N-ONE e: mini electric vehicle, offering high transparency, improved durability, and reduced VOC emissions while eliminating coating processes during manufacturing.

- January 2026: BASF SE reported extended service-life predictions for its Ultramid polyamide used in electric vehicle components, with testing indicating durability exceeding 100,000 hours, supporting higher reliability requirements for EV pumps, valves, and under-hood systems.

Companies Covered in Electric Vehicle Plastics Market

- BASF SE

- SABIC (Saudi Basic Industries Corporation)

- LyondellBasell Industries Holdings B.V.

- Evonik Industries AG

- Covestro AG

- DuPont de Nemours, Inc.

- Sumitomo Chemical Co., Ltd.

- LG Chem

- Asahi Kasei Corporation

- LANXESS AG

- INEOS Group

- Celanese Corporation

- AGC Chemicals

- EMS-Chemie Holding AG

- Mitsubishi Engineering-Plastics Corporation

- Solvay S.A.

- Toray Industries, Inc.

- Teijin Limited

Frequently Asked Questions

The global Electric Vehicle Plastics market is expected to reach US$ 3.1 Billion in 2026 and is projected to grow to US$ 19.2 Billion by 2033 at a CAGR of 29.8% during 2026-2033.

The electric vehicle plastics market is driven by rapid EV adoption, the need for vehicle lightweighting, increasing battery system polymer use, and strong global policies promoting electric mobility.

Asia Pacific leads the global Electric Vehicle Plastics market, supported by large EV production volumes in China and expanding EV manufacturing in Japan, South Korea, and India.

The key opportunity lies in advanced engineering plastics for high-voltage EV systems and next-generation battery architectures such as cell-to-pack designs.

Key companies include BASF SE, Covestro AG, SABIC, DuPont, LANXESS AG, LyondellBasell, LG Chem, Asahi Kasei, Evonik Industries, Celanese Corp., and EMS-Chemie Holding.