- Electric Mobility

- Electric Tractor Market

Electric Tractor Market Size, Share, and Growth Forecast 2026 - 2033

Electric Tractor Market by Propulsion (Battery Electric Tractors (BEV), Hybrid Electric Tractors, Plug-in Hybrid Electric Tractors), Power Output (Low Power <50 HP, Medium Power 50-100 HP, High Power >100 HP), Drive Type (2-Wheel Drive (2WD), 4-Wheel Drive (4WD)), Application (Agriculture, Utility, Industrial), by Regional Analysis, 2026 - 2033

Electric Tractor Market Size and Trend Analysis

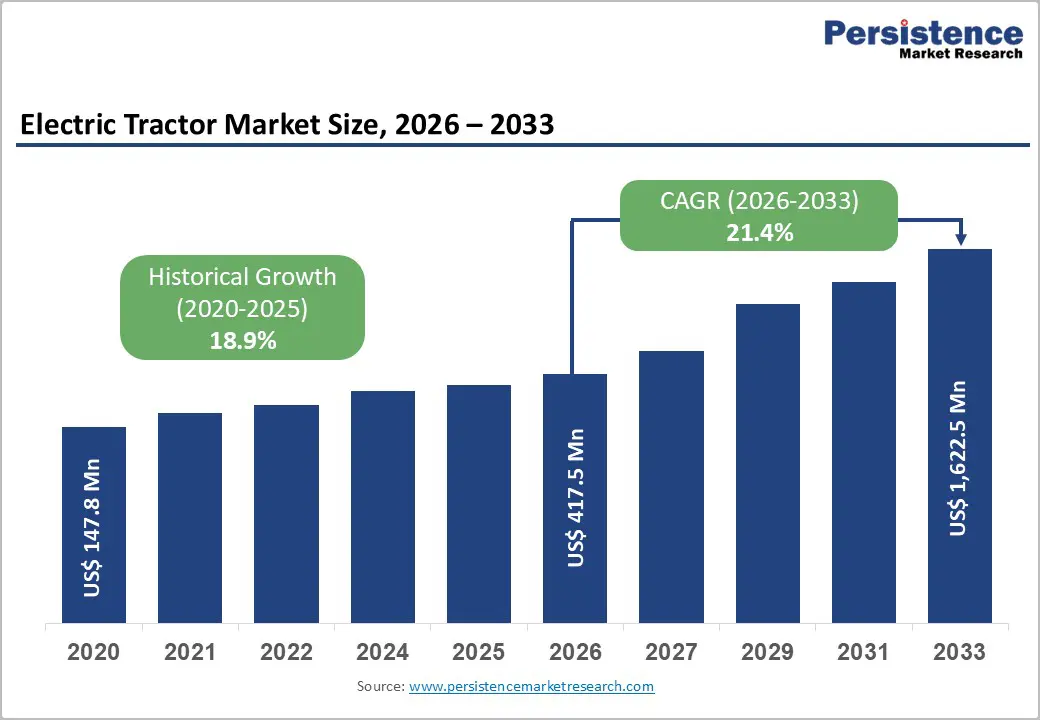

The global electric tractor market size is expected to be valued at US$ 417.5 million in 2026 and projected to reach US$ 1,622.5 million by 2033, growing at a CAGR of 21.4% between 2026 and 2033.

The electric tractor market is experiencing extraordinary growth, fueled by a powerful convergence of tightening emission regulations, advances in lithium-ion battery technology, and escalating government subsidies for sustainable farm mechanization. Over 25 countries now offer financial incentives for electric tractor adoption, while rapid improvements in battery energy density and the declining cost of EV powertrains are making electric tractors cost-competitive with conventional diesel alternatives. The U.S. Department of Agriculture (USDA) reported that agriculture, food, and related industries contributed approximately US$ 1.530 trillion to the U.S. GDP in 2023, reinforcing the strategic importance of mechanization investments and underpinning sustained demand for next-generation electric farm equipment across global markets.

Key Industry Highlights

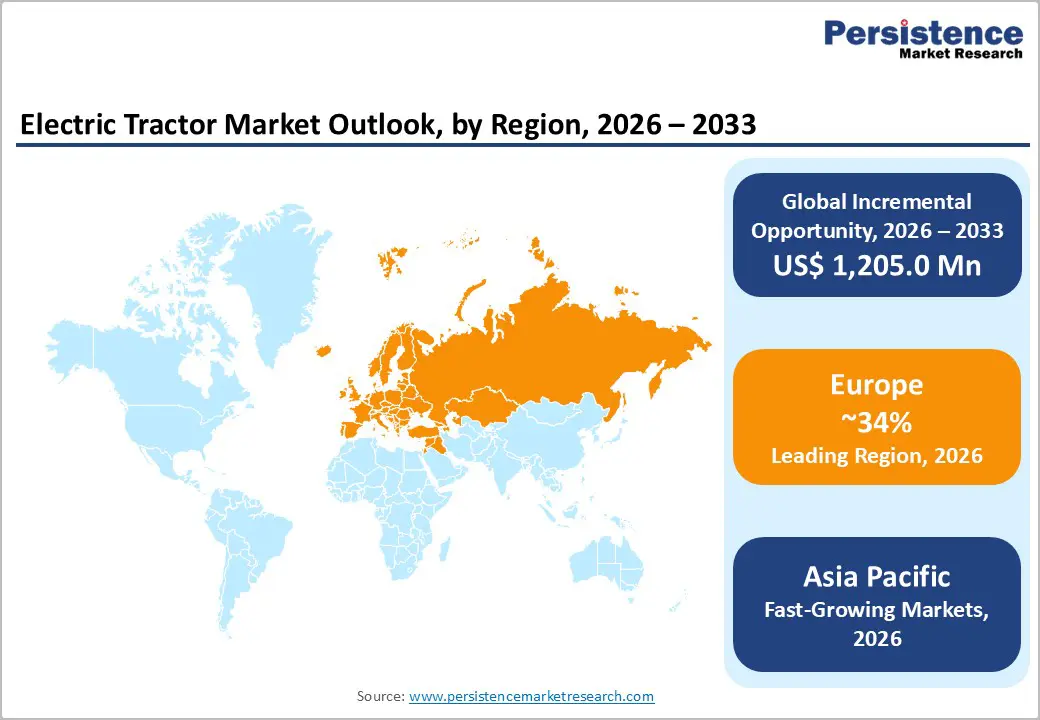

- Leading Region: Europe leads the global Electric Tractor market with approximately 34% market share in 2025, supported by the EU Green Deal, the Farm to Fork Strategy, OEM-led innovation (AGCO's Fendt, CLAAS, CNH Industrial), and comprehensive regulatory mandates targeting a 50% reduction in agricultural emissions by 2030.

- Fastest Growing Region: Asia Pacific is the fastest-growing region in the electric tractor market, driven by India's PM-KUSUM green mechanization scheme, China's 4WD subsidy programs, and a combined base of over 500 million smallholder farms representing significant untapped electrification demand through 2033.

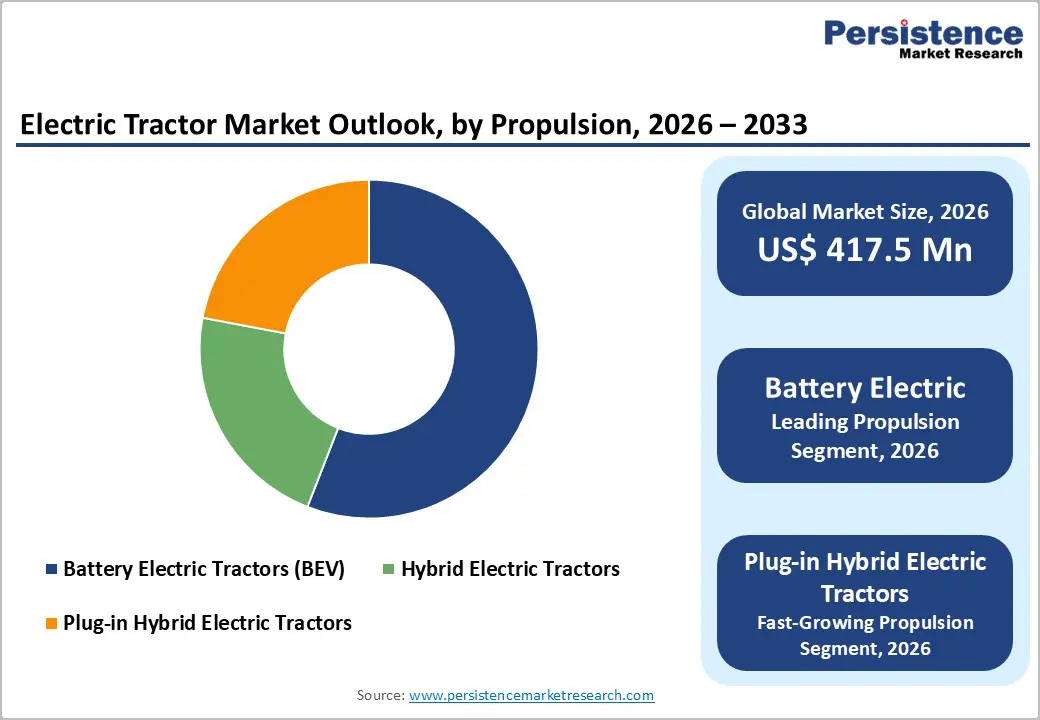

- Dominant Segment: Battery Electric Tractors (BEV) dominate the propulsion segment with approximately 52% market share in 2025, supported by lithium-ion battery dominance (70% of power systems), fast-charge capabilities, and landmark BEV launches from John Deere, Monarch Tractor, and Kubota, accelerating mainstream commercial adoption.

- Fastest-Growing Segment: Plug-in Hybrid Electric Tractors are the fastest-growing propulsion segment, accounting for ~20% of new tractor releases in 2023 - 2025, offering farmers the operational versatility of electric power for light tasks combined with combustion backup for heavy-duty continuous field operations.

- Key Opportunity: The convergence of autonomous AI navigation and BEV propulsion is a key market opportunity, validated by Monarch Tractor's record US$ 133 million Series C in 2024 and John Deere's US$ 20 billion U.S. manufacturing investment, unlocking substantial addressable demand for smart electric farm equipment.

| Key Insights | Details |

|---|---|

| Electric Tractor Market Size (2026E) | US$ 417.5 Million |

| Market Value Forecast (2033F) | US$ 1,622.5 Million |

| Projected Growth CAGR (2026 - 2033) | 21.4% |

| Historical Market Growth (2020 - 2025) | 18.9% |

Market Dynamics

Drivers - Stringent Emission Regulations and Government Incentive Programs Accelerating Electrification

Regulatory pressure from global environmental agencies is one of the most decisive drivers shaping the Electric Tractor market. Agencies, including the U.S. Environmental Protection Agency (EPA), the California Air Resources Board (CARB), and the European Commission, are progressively tightening off-road equipment emission standards, compelling fleet operators and farmers to migrate toward zero-emission alternatives. The EU's Green Deal and the Farm to Fork Strategy mandate a 50% reduction in the use of chemical pesticides and a significant cut in the agricultural carbon footprint by 2030, directly incentivizing the adoption of electric tractors. In the U.S., programs such as the USDA's Environmental Quality Incentives Program (EQIP) and the Clean Vehicle Rebate Project provide direct financial support for farmers transitioning to electric equipment. With over 25 countries now offering subsidies for electric tractor adoption, policy support is driving sustained demand across both developed and emerging agricultural markets.

Advances in Battery Technology and Falling EV Component Costs Boosting Viability

Technological advances in battery systems are rapidly transforming the economic proposition of electric tractors, making them a compelling alternative to diesel-powered tractors. Lithium-ion batteries now account for approximately 70% of power systems deployed in electric tractors, offering higher energy density, longer lifespan, and fast charging. Battery energy density improvements of 5-10% were recorded in new models launched in 2023-2024, and new battery packs can support typical farm workloads ranging from 30 kWh for compact 20-40 HP units to 150 kWh+ for heavy-duty 100+ HP tractors. Charging times on fast chargers have been reduced to as low as 30-120 minutes, addressing a key operational concern. In 2025, John Deere announced a partnership with a battery technology firm to co-develop modular battery systems targeting a 20% reduction in battery costs, a development that signals the broader industry trajectory toward cost parity with conventional tractors.

Restraints - High Upfront Purchase Cost and Limited Rural Charging Infrastructure

Despite improving battery economics, the acquisition cost of electric tractors remains significantly higher than comparable diesel models, with premium prices creating adoption barriers, especially for smallholder farmers and low-income agricultural economies. In many developing regions, access to stable grid electricity and dedicated charging infrastructure is severely limited. While more than 100 rural farm sites across Europe and Asia deployed high-capacity DC chargers in 2024, this represents a fraction of the global agricultural land base. The challenge of charging availability in remote areas remains a critical operational constraint, limiting the viability of electric tractors outside well-connected farming clusters.

Limited High-Power Models and Field Endurance Concerns for Large-Scale Operations

Electric tractors have made significant inroads in the compact and medium-power segments but continue to face technical limitations in high-horsepower applications critical to large-scale commercial farming. Heavy-duty field operations such as deep tillage, bulk hauling, and large-scale planting demand sustained high torque outputs that current battery systems struggle to maintain across full working days. Only approximately 40% of the planned electric tractor units are heavy-duty models, with the majority in light-to-medium-duty classes. This limits addressable market penetration in regions such as the U.S. Midwest and South America, where high-horsepower tractors above 100 HP dominate agricultural operations.

Opportunities - Precision Agriculture Integration and Autonomous Electric Tractor Adoption

The convergence of electrification and autonomous precision agriculture represents one of the most transformative opportunities in the Electric Tractor market. Approximately 25% of electric tractor prototypes unveiled in 2024 featured semi-autonomous plowing or AI-guided navigation capabilities, reflecting the accelerating integration of smart technologies. Monarch Tractor's driver-optional MK-V, the first all-electric autonomous tractor from the Foxconn assembly line in Lordstown, Ohio, exemplifies this trajectory. In July 2024, Monarch Tractor raised a record-breaking US$ 133 million in a Series C funding round, the largest in the history of agricultural robotics, validating strong investor confidence. GPS receivers in autonomous agricultural equipment now achieve positional accuracy up to two centimeters, enabling precision field management that reduces inputs and maximizes crop yields. With 90% of new electric tractors supporting telematics and IoT farm management platforms, the market is well-positioned to capitalize on the growing demand for data-driven, sustainable farming solutions.

Asia Pacific Smallholder Modernization and Government-Driven Green Mechanization Programs

Asia Pacific holds one of the most substantial long-term growth opportunities for Electric Tractor market participants, driven by massive smallholder modernization programs, government-funded green mechanization schemes, and a dense agricultural base that demands affordable, clean-energy farm equipment. India's tractor mechanization rate currently stands at approximately 40-45%, well behind China's 57% and the United States' 95%, as highlighted by the OECD's Agricultural Policy Monitoring and Evaluation 2024 report, indicating substantial untapped demand. India's PM-KUSUM scheme and government subsidies on agricultural electric tractors are accelerating adoption. In November 2025, Mahindra & Mahindra, the world's largest tractor manufacturer by volume, launched electric mini-tractors under the PM-KUSUM scheme, partnering with Tata Power for solar charging networks. China's new subsidy schemes prioritize smart 4WD tractors, creating an opportunity for high-power and premium electric tractor manufacturers to penetrate this rapidly evolving market.

Category-wise Analysis

Propulsion Insights

Battery Electric Tractors (BEV) represent the leading propulsion segment in the Electric Tractor market, accounting for approximately 52% of total market share in 2025. BEVs dominate because they offer zero direct emissions, significantly lower operating costs compared to diesel, and are most compatible with the growing network of on-farm charging infrastructure. Lithium-ion battery systems power approximately 70% of deployed electric tractors globally, offering fast charging, durability, and higher energy density. New BEV models from John Deere (inaugural series launched in February 2025), Kubota, and Monarch Tractor are reinforcing BEV's leadership. Plug-in Hybrid Electric Tractors are the fastest-growing propulsion segment, attracting farmers who need versatility across heavy tasks while maintaining access to electric power for lighter field work, with approximately 20% of new tractor releases between 2023 and 2025 being plug-in hybrid models.

Power Output Insights

The medium-power (50-100 HP) segment is the leading power output category in the Electric Tractor market, accounting for approximately 45% of total market share in 2025. Medium-power tractors occupy the versatility sweet spot for a broad range of agricultural operations, including soil preparation, planting, and crop care, making them suitable for both mid-sized farms and diversified smallholder operations across Asia Pacific, Europe, and North America. This class also aligns most closely with current battery technology capabilities, where 51-100 kWh battery packs enable adequate field endurance for standard working days. The 40-100 HP class offered mainstream versatility and accounted for approximately 47% of the broader tractor market in 2024. The High Power (>100 HP) segment is the fastest-growing, driven by demand from large commercial farms seeking electric alternatives for heavy-duty operations.

Drive Type Analysis

4-Wheel Drive (4WD) is the leading drive type in the Electric Tractor market, representing approximately 58% of total market share in 2025. The dominance of 4WD stems from its superior traction, enhanced pulling capability, and ability to navigate challenging terrain, including wet, muddy, and uneven farmland, conditions that are common across the majority of global agricultural regions. China's new government subsidy schemes explicitly prioritize smart 4WD tractors to drive productivity gains, further reinforcing demand. John Deere's 4WD 9RX electric series and CNH Industrial's 4WD platforms reflect OEM strategy aligned to this demand. The integration of precision agriculture systems, including GPS-guided navigation that achieves accuracy up to two centimeters, is more widely deployed on 4WD models, making them increasingly preferred by technology-forward farming operations seeking both performance and digital farm management capabilities.

Application Insights

Agriculture is the dominant application segment in the Electric Tractor market, accounting for approximately 68% of total market share in 2025. The sector's leadership is backed by the fundamental and ever-growing need for mechanized farm equipment to perform critical operations, including plowing, tilling, sowing, hauling, and harvesting. The USDA confirmed that farm output alone contributed US$ 203.5 billion to U.S. GDP in 2023, underscoring the scale of demand for agricultural mechanization. Asia Pacific, home to over 500 million small farms, represents the world's most prolific agricultural tractor market. With agriculture accounting for 89.38% of total tractor application demand globally in 2024, the segment's electrical transition has an outsized impact on market growth. The Utility segment is the fastest-growing application, driven by expanding urban logistics, airport ground handling, and global construction electrification programs.

Regional Insights

North America Electric Tractor Market Trends and Insights

North America holds the second-largest share in the global Electric Tractor market, supported by a strong innovation ecosystem, proactive regulatory frameworks, and high-profile commercial deployments. The U.S. tractor market was sized at approximately 217,200 units in 2024 with the electric segment growing at a CAGR of 15.98% between 2024 and 2029. Emission mandates from the EPA and CARB, alongside the USDA's EQIP program and Clean Vehicle Rebate Project, are accelerating farmer adoption of electric tractors, particularly in California's extensive specialty crop regions.

Innovation is a defining characteristic of the North American market. Monarch Tractor debuted its driver-optional MK-V at Oregon Wine Country in March 2024, while Solectrac sells three fully electric tractor models ranging from 25 HP to 70 HP across 85 dealer locations nationwide. In early 2024, AGCO strengthened its U.S. presence by launching Fendt electric tractors, complemented by its Fuse Smart Farming precision technology platform. John Deere's commitment of US$ 20 billion in May 2025 to expand U.S. manufacturing capabilities signals long-term confidence in domestic electric tractor production.

Europe Electric Tractor Market Trends and Insights

Europe is the leading region in the global Electric Tractor market, driven by the most comprehensive regulatory framework for agricultural sustainability and the highest concentration of OEM electric tractor development programs. The EU's Green Deal and Farm to Fork Strategy mandate a 50% reduction in pesticide use and sharp cuts in agricultural carbon emissions by 2030. Germany's leadership in precision agriculture technology and France's proximity to the Airbus Group's advanced manufacturing hub create a fertile environment for electric tractor R&D. France's national agricultural sector is projected to grow at a 4.0% CAGR through 2035, while Germany is projected to grow at 4.5% in the forecast period.

In November 2023, TAFE (Tractors and Farm Equipment Ltd.) introduced the E30 compact electric tractor at Agritechnica in Hannover, Germany, powered by a lithium-ion battery with a two-speed transmission. A European consortium unveiled 100 solar charging stations across agricultural clusters in 2025. Spain's and the UK's expanding organic farming sectors are increasingly receptive to zero-emission tractor solutions. In September 2024, SuperPanther GmbH and Steyr Automotive GmbH launched the eTopas 600 electric tractor at IAA Transportation, targeting the 'Net-Zero' roadmap and reinforcing Europe's position as the leading hub for electric tractor innovation.

Asia Pacific Electric Tractor Market Trends and Insights

Asia Pacific is the fastest-growing region in the Electric Tractor market, driven by large-scale agriculture, accelerating government-sponsored mechanization programs, and growing domestic EV manufacturing capabilities. The region is home to over 500 million small farms and holds approximately 35% of global prototype and pilot electric tractor deployments. China's government subsidy schemes now explicitly prioritize smart 4WD electric tractors, while India's PM-KUSUM scheme and direct agricultural electrification subsidies are driving adoption among smallholder farmers. In November 2025, Mahindra & Mahindra launched electric mini-tractors in partnership with Tata Power for solar charging, and presented them at Agrovision 2025 in Nagpur, with the Union Cabinet Ministers in attendance.

India's tractor mechanization rate of 40-45% compared to China's 57% and the U.S.'s 95% highlights vast untapped potential, according to the OECD's Agricultural Policy Monitoring and Evaluation 2024. Kubota is scaling drone-integrated sprayers across Southeast Asia, while John Deere deployed 5,000 autonomous tractor units in Chinese and Indian farmlands following its CES 2025 unveiling. In 2024, Mahindra inaugurated a pilot deployment of 50 electric tractors in Gujarat to test performance across varied soil and climate conditions, demonstrating the region's commitment to large-scale electric agriculture.

Competitive Landscape

The global Electric Tractor market exhibits a moderately fragmented structure, characterized by the presence of established agricultural equipment manufacturers alongside emerging electric mobility startups. While a few large OEMs hold a notable share of ongoing electrification projects, the competitive environment remains dynamic due to rapid technological innovation and new entrants focusing on specialized electric platforms. Companies are increasingly differentiating through advanced battery management systems, precision telematics integration, and digital farm connectivity solutions designed to enhance operational efficiency and equipment performance.

Strategically, market participants are prioritizing partnerships with battery technology providers and software developers to accelerate product development and improve energy efficiency. Investments in R&D are rising across the sector as manufacturers focus on extending battery range, improving charging infrastructure compatibility, and enabling autonomous capabilities. In addition, companies are experimenting with alternative ownership models such as equipment leasing, fleet-based deployment, and subscription-driven farm management services. These approaches aim to lower upfront costs for farmers while supporting broader adoption of electric agricultural machinery in both developed and emerging agricultural markets.

Key Developments

- November, 2025: Montra Electric launched the E-27 electric tractor in India at a starting price of INR 10.75 lakh, featuring a 27 HP PMSM motor, 22.37 kWh LFP battery, and availability across 17 dealerships, showcased at the EIMA Agrimach India 2025 farm mechanization exhibition.

- November, 2025: Tractors and Farm Equipment Limited unveiled the EVX75 electric-hybrid tractor and introduced the Terra Vista vision-based guidance system at Agritechnica 2025 in Germany, highlighting its push into precision agriculture and sustainable farm mechanization technologies.

- January, 2026: John Deere unveiled a fully electric 130-hp E-Power tractor prototype at the Grüne Woche 2026 exhibition in Berlin, featuring modular batteries from Kreisel Electric and a fast-charging system, with limited market launch planned for 2027.

Companies Covered in Electric Tractor Market

- AGCO Corporation

- AutoNxt Automation

- CLAAS KGaA mbH

- CNH Industrial N.V.

- John Deere (Deere & Company)

- Kubota Corporation

- Mahindra and Mahindra Ltd.

- Monarch Tractor

- Solectrac Inc.

- Farm Trac (Escorts Kubota Limited)

- Cellestial E-Mobility

- Sabi Agri

- Agro Tractors SpA

- Proxecto

- Tadus GmbH

- Yanmar Co., Ltd.

- Sonalika International Tractors Ltd.

- TAFE (Tractors and Farm Equipment Ltd.)

- Fendt (AGCO Brand)

Frequently Asked Questions

The global Electric Tractor market is estimated to reach US$ 417.5 million in 2026, supported by growing zero-emission equipment mandates, government subsidy programs, and advances in lithium-ion battery technology.

Key demand drivers include stringent emission regulations, government incentives, declining EV component costs, advancements in lithium-ion batteries, and increasing adoption of precision and autonomous farming technologies.

Europe leads the Electric Tractor market, accounting for around 34% of global share, driven by strong decarbonization policies, advanced agricultural mechanization, and the presence of major tractor OEMs.

The major growth opportunity lies in autonomous electric tractors and agricultural mechanization programs in Asia Pacific, particularly in countries such as India and China supported by government initiatives.

Key players include Deere & Company, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, CLAAS, Monarch Tractor, Solectrac, Cellestial E‑Mobility, and AutoNxt Automation.