- Pharmaceuticals

- Global Dysmenorrhea Treatment Market

Global Dysmenorrhea Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Dysmenorrhea Treatment Market by Treatment (Hormonal Therapy, NSAIDs , Surgery, Others), Type (Primary Dysmenorrhea, Secondary Dysmenorrhea), Route of Administration (Oral , Injectable , Transdermal , Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, Retail Pharmacy), and Regional Analysis from 2026 to 2033.

Dysmenorrhea Treatment Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

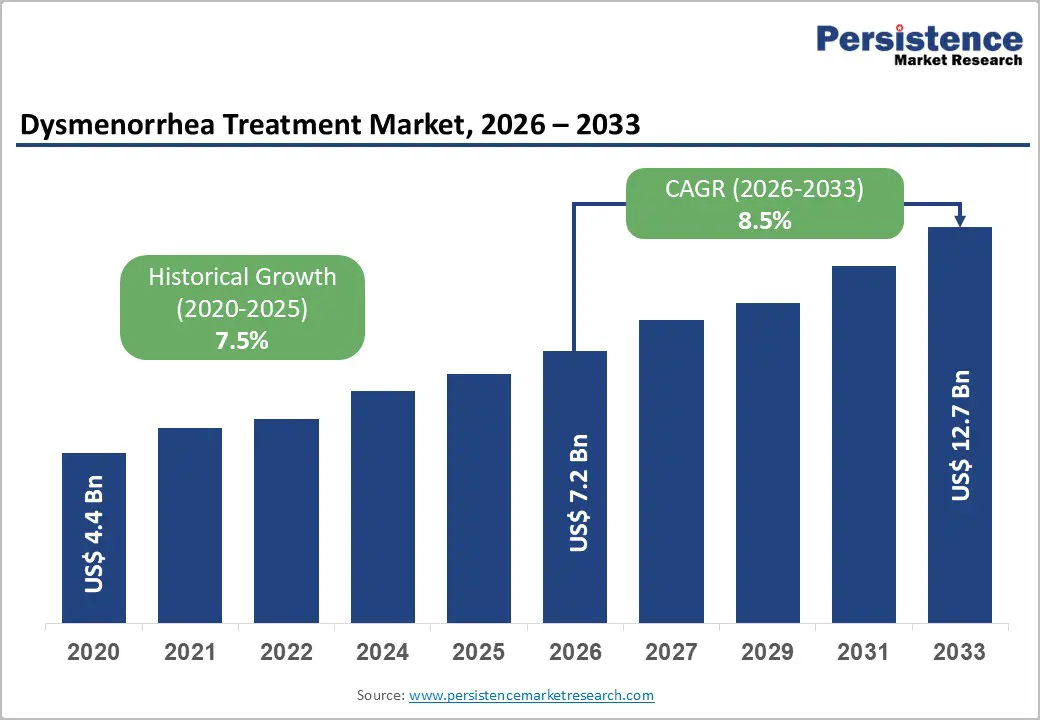

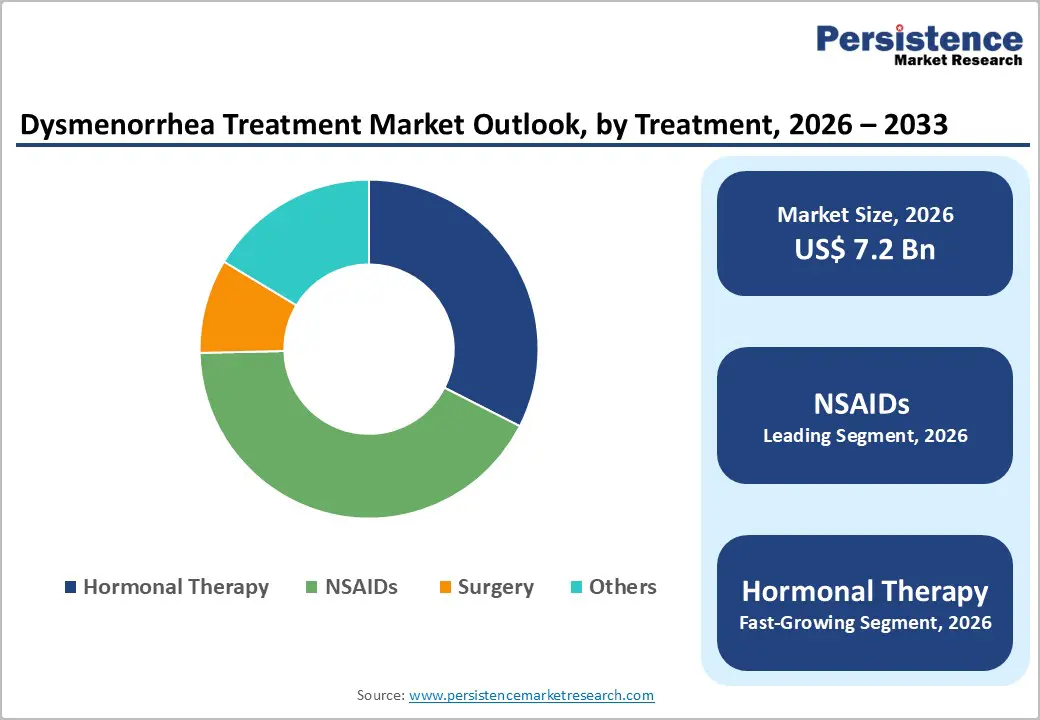

The global dysmenorrhea treatment market is estimated to grow from US$ 7.2 Bn in 2026 to US$ 12.7 Bn by 2033. The market is projected to record a CAGR of 8.5% during the forecast period from 2026 to 2033.

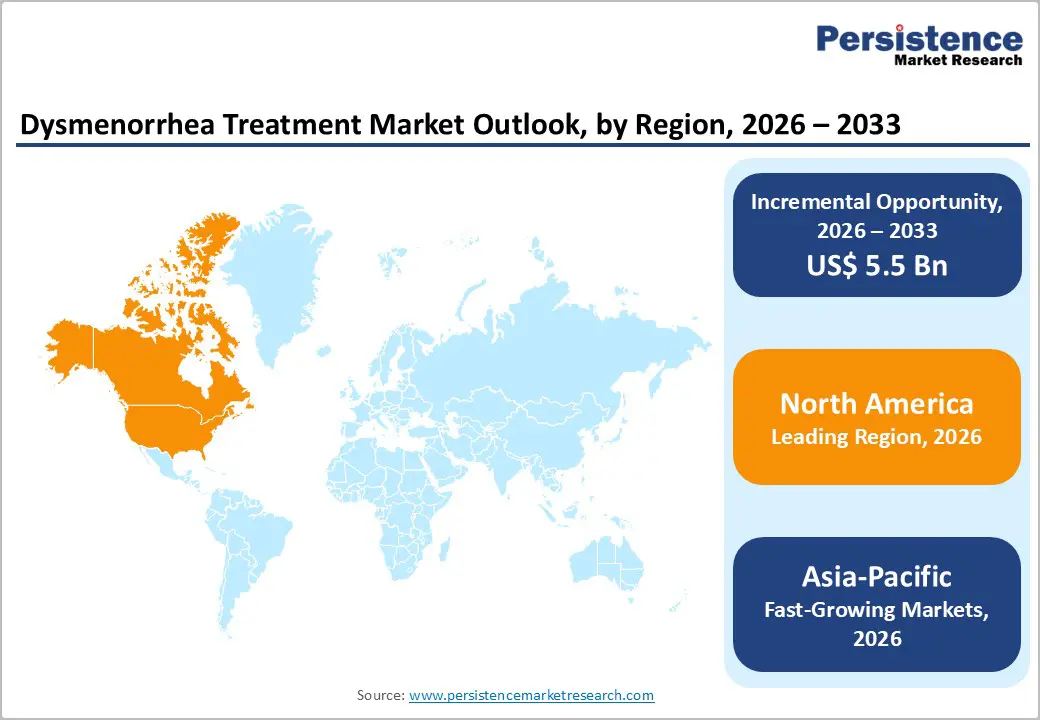

The global dysmenorrhea treatment market is expanding steadily, fueled by increasing awareness, rising prevalence of menstrual disorders, and demand for effective pain management solutions. North America leads due to advanced healthcare systems, strong regulatory support, and high adoption of innovative therapies, while Asia-Pacific grows rapidly, driven by improving healthcare infrastructure, government initiatives, and rising patient awareness.

Key Industry Highlights

- Dominant Segment: NSAIDs (Non-Steroidal Anti-Inflammatory Drugs) account for 42.1% share in dysmenorrhea treatment in 2025, driven by their effectiveness in reducing menstrual pain, safety profile, and ease of use. They work by inhibiting prostaglandin production, providing rapid symptom relief, avoiding surgical intervention, and are widely available as prescription and over-the-counter medications.

- Dominant Region: North America leads the dysmenorrhea treatment market with 38.7% share in 2025, due to advanced healthcare infrastructure, high awareness of menstrual health, strong regulatory frameworks, and early adoption of innovative therapies. Asia-Pacific is the fastest-growing region, supported by rising prevalence of menstrual disorders, expanding healthcare access, and government awareness initiatives.

- Market Drivers: Increasing prevalence of dysmenorrhea, rising awareness of menstrual health, demand for safe and effective pain relief, growth in over-the-counter treatments, and innovation in targeted therapies support market growth.

- Market Opportunity: Key opportunities include development of novel non-hormonal and hormonal therapies, digital pain management solutions, integration with telehealth services, personalized treatment approaches, and expansion into emerging markets with improving women’s healthcare access.

| Key Insights | Details |

|---|---|

|

Global Dysmenorrhea Treatment Market Size (2026E) |

US$ 7.2 Bn |

|

Market Value Forecast (2033F) |

US$ 12.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.5% |

Market Dynamics

Driver: Rising Prevalence of Dysmenorrhea and Menstrual Disorders

Dysmenorrhea is one of the most common gynecological conditions worldwide. A comprehensive meta analysis across 336 global studies found that the pooled prevalence of dysmenorrhea was about 71.3% among women of reproductive age, with primary dysmenorrhea (pain without underlying pathology) at around 73% and secondary dysmenorrhea at 35% in included studies. This condition is particularly prevalent among young adults and university populations, where rates can approach 78.4% due to menstrual pain and related symptoms.

In clinical practice, rates vary regionally but remain consistently high, studies reported prevalence ranges from 45% to over 90% depending on population and age group. In younger cohorts, figures exceed 80%, and even moderate to severe symptoms that disrupt daily activities occur in a significant proportion of women. This high and persistent prevalence underscores the broad base of unmet medical need; many individuals seek effective relief to maintain productivity, quality of life, and social function. As awareness grows and more women seek care rather than dismissing menstrual pain as “normal,” demand for clinically effective therapies increases, driving growth in the dysmenorrhea treatment market.

Restraints: Side Effects Associated with Long Term NSAID and Hormonal Use

Non steroidal anti inflammatory drugs (NSAIDs) are the cornerstone pharmacological therapy for dysmenorrhea due to their effectiveness at reducing prostaglandin mediated uterine pain. However, NSAIDs carry well documented adverse effects that can limit long term use. NSAIDs inhibit cyclooxygenase enzymes that play protective roles in the gastric mucosa and renal circulation, increasing the risk of gastrointestinal irritation, ulcers, bleeding, renal impairment, and cardiovascular events when used chronically, particularly in susceptible populations.

The risk profile is especially relevant for individuals relying on repeated NSAID courses each menstrual cycle over many years. For example, gastrointestinal adverse effects such as dyspepsia occur in 10–20% of users, and significant bleeding or ulceration can occur with higher or prolonged dosing. Additionally, select NSAIDs (e.g., diclofenac) are associated with increased vascular risks, including elevated coronary event rates compared with placebo in some analyses.

Hormonal therapies (e.g., combined oral contraceptives) also pose side effects such as nausea, weight changes, and menstrual irregularities that can deter continuation. Collectively, these safety concerns restrain broader market adoption of first line treatments, drive discontinuation, and fuel demand for safer, well tolerated alternatives.

Opportunity: Development of Novel Non Hormonal Therapies and Targeted Drugs

Emerging non hormonal and non pharmacological therapies present a significant opportunity in the dysmenorrhea treatment landscape, addressing limitations of traditional NSAIDs and hormonal approaches. Scientific evidence increasingly supports various complementary and alternative modalities such as acupuncture, transcutaneous electrical nerve stimulation (TENS), exercise, yoga, and heat therapy for reducing menstrual pain intensity compared with placebo or no treatment.

Acupuncture–related therapies, for example, have shown promising outcomes in large meta analyses involving thousands of participants, demonstrating improvements in pain scores and reductions in prostaglandin levels compared with Western medicine alone, indicating that mechanistic, non drug approaches may effectively modulate pain pathways.

These therapies often carry lower systemic side effect profiles than NSAIDs or hormones and can be integrated into personalized care regimens, expanding treatment options for women who are unresponsive or intolerant to conventional medications. Beyond established CAM approaches, research into novel drug delivery systems, targeted analgesics, and plant based compounds is underway, indicating active clinical pipelines that could yield safer, more effective non hormonal pharmacological solutions in the coming years.

Category-wise Analysis

By Treatment, NSAIDs Dominates the Dysmenorrhea Treatment Market

NSAIDs occupies 42.1% share of the global market in 2025, because they directly target prostaglandin-mediated uterine contractions, providing rapid pain relief. Clinical guidelines from major health authorities recommend NSAIDs as first-line therapy, with effectiveness rates reported between 70–90% for reducing menstrual pain.

Over-the-counter availability, ease of use, and established safety profiles (when used short-term) further enhance adoption. Compared with hormonal therapies, NSAIDs avoid systemic hormonal effects, appealing to a wider patient population, including adolescents and women with contraindications for hormonal contraceptives. The combination of high efficacy, accessibility, and broad patient acceptance positions NSAIDs as the dominant treatment segment in the dysmenorrhea market globally.

By Type, Primary dysmenorrhea dominates due to high prevalence and treatment demand

Primary dysmenorrhea, menstrual pain without underlying pathology, dominates due to its high prevalence among women of reproductive age. Studies indicate that 50–90% of women globally experience primary dysmenorrhea, with moderate-to-severe pain affecting 20–30%, significantly impacting daily activities.

Secondary dysmenorrhea, linked to conditions like endometriosis or fibroids, accounts for only about 10% of cases. Because of the sheer volume of primary cases, demand for treatment is concentrated here, driving product adoption, research, and healthcare resources toward effective symptom management. Awareness campaigns and improved diagnosis also encourage women to seek treatment early, reinforcing primary dysmenorrhea’s dominance in the market.

Regional Insights

North America Dysmenorrhea Treatment Market Trends

North America dominates the dysmenorrhea treatment market with 38.7% share in 2025, due to a combination of high awareness, advanced healthcare infrastructure, and broad treatment access. The region particularly the United States accounts for a significant share of global revenue due to widespread use of NSAIDs, hormonal therapies, and innovative drugs approved by regulatory authorities such as the FDA. Over 31 million women in the U.S. report experiencing menstrual pain annually, highlighting high demand for effective therapies.

Robust pharmaceutical R&D, strong OTC availability, and extensive telemedicine adoption further strengthen market dominance. Additionally, public health initiatives and women’s health advocacy increase diagnosis rates and treatment uptake. High consumer health literacy and insurance coverage for pain management also support sustained market leadership.

Europe Dysmenorrhea Treatment Market Trends

Europe represents a major regional market for dysmenorrhea treatments, supported by robust healthcare systems, proactive public health policies, and strong clinical research activity. Countries such as Germany, France, the UK, and Italy show high adoption of both NSAIDs and advanced therapeutic options, contributing substantially to regional demand.

European regulatory frameworks including the EMA ensure safe, effective treatments and facilitate clinical trials for new therapies. Growing awareness of menstrual health through national campaigns and nonprofit initiatives further drives women to seek care and management for dysmenorrhea. Additionally, preventative healthcare culture and increasing healthcare spending bolster ongoing adoption of both conventional and novel pain management solutions.

Overall, Europe’s combination of accessible care, policy support, and rising patient engagement underpins its importance in the global market.

Asia-Pacific Dysmenorrhea Treatment Market Trends

Asia Pacific is the fastest growing region in the dysmenorrhea treatment market due to its large female population, rising healthcare access, and increasing awareness of menstrual health issues. Countries like China, India, and Japan are expanding healthcare infrastructure and increasing gynecological care availability, propelling higher diagnosis and treatment rates.

The region’s growth is further supported by rapid urbanization, rising disposable income, and expanding telemedicine and online pharmacy use, which improve access to dysmenorrhea therapies. Public health campaigns and educational programs are reducing stigma and encouraging women to seek effective pain management. Moreover, increased spending on women’s health and stronger pharmaceutical penetration contribute to swift market expansion. Asia Pacific’s combination of demographic scale and improving healthcare services drives its position as the fastest expanding dysmenorrhea treatment market globally.

Market Competitive Landscape

The dysmenorrhea treatment market is competitive, led by major players offering NSAIDs, hormonal therapies, and novel non-hormonal options. Key companies focus on R&D, OTC availability, and geographic expansion. Strong presence in North America and Europe, coupled with emerging Asia-Pacific growth, drives innovation and intensifies market rivalry globally.

Key Industry Developments:

- In December 2025, Bayer initiated a Phase III clinical trial, called SUNFLOWER, investigating its Mirena® 52 mg levonorgestrel releasing intrauterine system (LNG IUS) for the treatment of nonatypical endometrial hyperplasia (NAEH) in women.

Companies Covered in Global Dysmenorrhea Treatment Market

- Novartis Pharmaceuticals Corporation

- Merck, Inc.

- Bayer Schering Pharma AG

- Vanita Therapeutics

- Alvogen

- Pfizer, Inc.

- Nua

- Cora

- Roche Laboratories

- Taj Pharmaceuticals, Ltd.

- Sanofi

- Terramedic, Inc.

- Others

Frequently Asked Questions

The global dysmenorrhea treatment market is projected to be valued at US$ 7.2 Bn in 2026.

Rising dysmenorrhea prevalence, growing women’s health awareness, demand for effective therapies, and expanding healthcare access.

The global dysmenorrhea treatment market is poised to witness a CAGR of 8.5% between 2026 and 2033.

Development of non-hormonal therapies, digital health solutions, personalized treatments, telemedicine expansion, and emerging market adoption.

Novartis Pharmaceuticals Corporation, Merck, Inc., Bayer Schering Pharma AG, Vanita Therapeutics, Alvogen, Pfizer, Inc.