- Pharmaceuticals

- DPP-IV Inhibitors Market

DPP-IV Inhibitors Market Size, Share, and Growth Forecast, 2026-2033

DPP-IV Inhibitors Market by Drug Type (Sitagliptin, Linagliptin, Teneligliptin, Saxagliptin, Others), Medication Type (Branded Drugs, Generic Drugs, Fixed-Dose Combinations, Others), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Others), and Regional Analysis for 2026-2033

DPP-IV Inhibitors Market Share and Trends Analysis

The global DPP-IV inhibitors market size is likely to be valued at US$ 15.2 billion in 2026, and is projected to reach US$ 18.8 billion by 2033, growing at a CAGR of 6.0% during the forecast period 2026–2033. With clinicians increasingly prescribing oral antidiabetic drugs as first line and second line treatment options in routine glycemic management, this market is poised for steady expansion. Dipeptidyl peptidase 4 (DPP-IV) inhibitors are maintaining strong clinical acceptance due to their glucose dependent mechanism of action, weight neutral profile, and relatively low risk of hypoglycemia.

As healthcare systems are emphasizing long term disease control and patient adherence, these agents are remaining integral to combination therapy strategies. Market stability is further supported by expanding generic availability and broader reimbursement coverage across developed economies. Generic penetration is improving affordability, which is widening patient access in both public and private healthcare settings. Uptake across Asia Pacific is strengthening as diagnosis rates increase and treatment infrastructure advances. Regulatory authorities are continuing to endorse cardiovascular safety data for antidiabetic therapies, which is reinforcing physician confidence and payer support.

Key Industry Highlights

- Dominant Drug Types: Sitagliptin is projected to account for around 39% revenue share in 2026, while teneligliptin is expected to be the fastest-growing molecule through 2033, driven by strong uptake in cost-sensitive Asian markets.

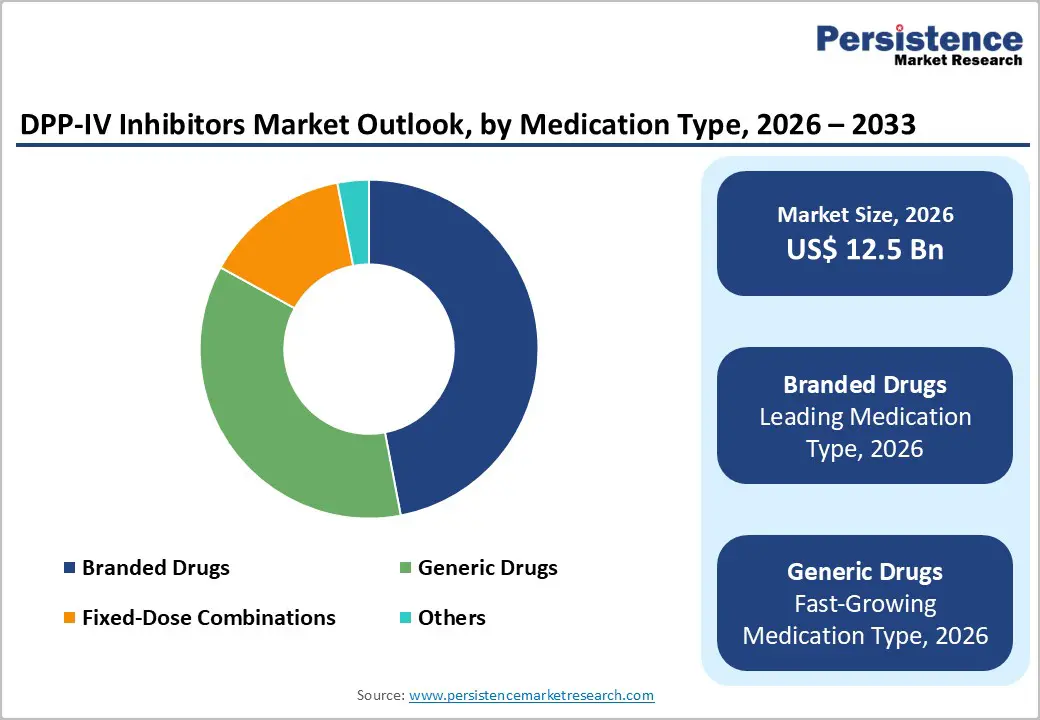

- Leading Medication Types: Branded DPP-IV inhibitors are estimated to account for approximately 47% of market value in 2026, while generic drugs are projected to register a 7.5% CAGR through 2033, driven by patent expirations.

- Distribution Channel Dynamics: Retail pharmacies are expected to hold about 50% revenue share in 2026, whereas online pharmacies are set to grow the fastest through 2033, fueled by e-prescriptions and chronic care home delivery.

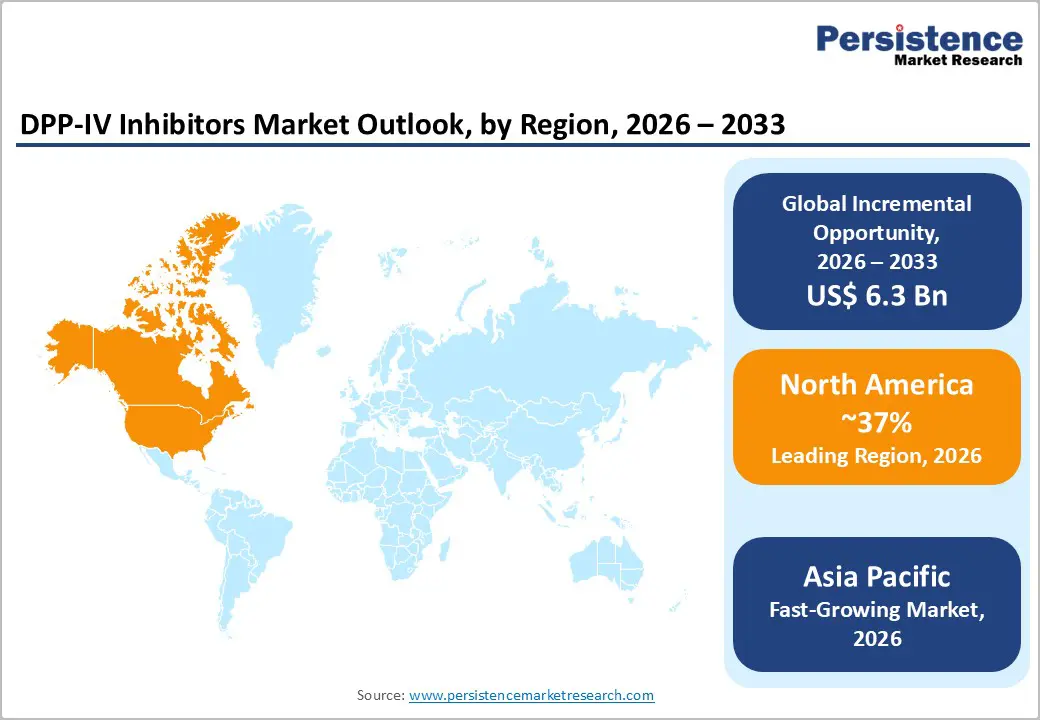

- Regional Leadership: North America is anticipated to lead with an estimated 37% share in 2026, while Asia Pacific is projected to be the fastest-growing market at 8% CAGR during 2026–2033, driven by expanding access to affordable oral therapies.

| Global Market Attributes | Key Insights |

|---|---|

| DPP-IV Inhibitors Market Size (2026E) | US$ 12.5 Bn |

| Market Value Forecast (2033F) | US$ 18.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Type 2 Diabetes and Expanding Patient Base to Benefit the Market

According to the International Diabetes Federation (IDF), more than 530 million adults were living with diabetes globally in 2023, with type 2 diabetes accounting for the vast majority of cases. This disease burden continues to rise due to demographic aging, lifestyle transitions, and increasing obesity rates across both developed and emerging economies. As screening and diagnosis rates improve, a larger patient population is entering long-term treatment pathways. This expansion directly increases demand for chronic glucose-lowering therapies. Oral antidiabetic drugs remain central to early and mid-stage disease management. As a result, sustained prescription volumes are being observed across regions.

Recent industry and policy developments further reinforce this demand outlook. The U.S. Department of Health and Human Services (HHS) announced that linagliptin and sitagliptin–metformin combinations were included among drugs selected for Medicare Part D price negotiations, signaling a policy focus on affordability and access. This move strengthens formulary positioning for DPP-IV inhibitors and supports wider patient reach. Clinically, these therapies are favored when metformin alone is insufficient. Their oral administration, weight-neutral profile, and suitability for combination therapy support continued physician preference, particularly among elderly and multi-comorbidity patient groups.

Generic Availability, Affordability Initiatives, and Favorable Clinical Positioning to Favor Growth

Clinical guidance from leading diabetes associations continues to recognize DPP-IV inhibitors for their low hypoglycemia risk and established safety profile relative to older oral antidiabetic classes. This favorable clinical positioning supports physician confidence and long-term patient adherence, particularly among elderly patients and those with multiple comorbidities. As a result, DPP-IV inhibitors remain widely used as second- or third-line oral therapies in type 2 diabetes management. Their predictable tolerability enables sustained utilization even as newer injectable and combination therapies gain visibility. This stability reinforces their role within standard treatment algorithms.

Government-led reimbursement and access initiatives have further strengthened market uptake. China’s National Healthcare Security Administration (NHSA) expanded reimbursement coverage under the National Reimbursement Drug List (NRDL) to include additional generic DPP-IV inhibitor formulations, following price negotiations aimed at reducing patient costs. This policy move improved affordability and accelerated adoption across public hospitals and retail pharmacies. Alongside ongoing patent expirations in multiple regions, increased generic availability continues to place downward pressure on branded pricing. Collectively, these developments expand treatment access and reinforce generics as core components of national diabetes care strategies.

Intensifying Competition from Newer Antidiabetic Drug Classes to Limit Expansion

Clinical treatment patterns are increasingly shifting toward GLP-1 receptor agonists and SGLT-2 inhibitors, driven by robust cardiovascular and renal outcome data from large-scale clinical trials. These outcomes have directly influenced treatment guidelines, particularly for patients with established cardiovascular risk. As a result, therapy selection is becoming more outcomes-focused rather than centered solely on glycemic control. This shift is gradually reducing the addressable patient pool for DPP-IV inhibitors. The effect is most visible in advanced healthcare systems where guideline adherence is high. Prescribing behavior is increasingly aligned with long-term outcome optimization.

Recent policy and reimbursement developments further reinforce this competitive pressure. The U.S. Department of Health and Human Services and the Centers for Medicare & Medicaid Services advanced Medicare Part D price negotiations targeting high-utilization diabetes therapies, with particular emphasis on GLP-1-based treatments, as widely reported by leading healthcare news outlets. This government focus underscores payer and policy prioritization of newer drug classes with demonstrated outcome benefits. As these therapies become more affordable and accessible, physicians are increasingly reserving DPP-IV inhibitors for narrower patient subsets. This selective positioning constrains long-term revenue expansion despite stable diabetes prevalence and may gradually dampen innovation momentum within the segment.

Sustained Pricing Pressure and Margin Erosion to Temper Market Spirits

The rapid expansion of generic DPP-IV inhibitor formulations continues to drive notable price erosion, particularly across Asia Pacific and Latin America. As multiple manufacturers enter the market, competitive pricing has become the primary purchasing determinant for both public and private buyers. Although treatment volumes remain stable due to chronic disease prevalence, the average selling price per unit continues to decline. This environment compresses margins for both branded and generic producers. Cost leadership and scale efficiencies are therefore becoming essential for sustained participation. Smaller players face increasing profitability challenges.

Recent policy actions have intensified this pressure in regulated markets. The European Union (EU) formally implemented the EU Health Technology Assessment (HTA) Regulation, enabling joint clinical assessments across member states for new and existing therapies, as reported by European Commission briefings and major European news outlets. This framework strengthens payer leverage and further limits premium reimbursement for branded diabetes drugs. In parallel, several Latin American governments expanded centralized procurement and reference pricing mechanisms for chronic disease medicines, according to regional health ministry announcements covered by Reuters. These measures collectively restrict pricing flexibility, directly impacting manufacturer margins and influencing long-term portfolio and investment decisions within the DPP-IV inhibitors market.

Expansion of Diagnosis and Treatment Access in Emerging and Underserved Markets

Emerging economies across Asia Pacific, Latin America, and parts of the Middle East present a significant growth opportunity due to historically low diagnosis-to-treatment ratios for type 2 diabetes. The World Health Organization continues to highlight that a large share of diabetes cases in low- and middle-income countries remains undiagnosed, creating a sizeable latent patient pool. As public health systems prioritize early detection, demand for cost-effective oral therapies is expected to rise. DPP-IV inhibitors, with established safety and oral administration, are well positioned to benefit from this expansion. Improved screening directly translates into earlier pharmacological intervention. This dynamic supports long-term volume growth.

Recent government-led initiatives reinforce this opportunity. India’s Armed Forces Medical Services (AFMS) rolled out an AI-based diabetic retinopathy screening program across major cities, improving early detection of diabetes-related complications and identifying untreated patients earlier in the disease course. Similarly, NHS England’s proposal to commission diabetic eye screening through community pharmacies and opticians from 2026 expands access points for both undiagnosed and chronic patients. These programs signal a structural shift toward proactive diabetes identification. Earlier diagnosis increases the addressable population for long-term oral glucose-lowering therapies.

Policy-Driven Focus on Integrated Diabetes Care and Chronic Therapy Continuity

Global policy frameworks increasingly emphasize integrated, life-course diabetes management, supporting sustained pharmacological demand. The World Health Organization’s World Diabetes Day 2025 campaign highlighted prevention, early diagnosis, and continuity of care as core priorities across healthcare systems. Such initiatives encourage earlier treatment initiation and long-term disease management rather than episodic care. Oral antidiabetic agents remain central to these pathways due to ease of use and scalability. DPP-IV inhibitors align well with this model, particularly for patients requiring stable, long-term glycemic control. This policy direction supports consistent therapy uptake.

These efforts are further reinforced by the WHO Global Diabetes Compact, which targets 80% of people with diabetes being diagnosed and receiving comprehensive care by 2030. Alignment of national screening and treatment programs with this target indicates sustained momentum beyond short-term initiatives. As healthcare systems work to close diagnosis and treatment gaps, demand for accessible, affordable oral therapies is expected to grow. DPP-IV inhibitors benefit from inclusion in standardized treatment pathways once patients enter care. Such policy-driven movements strengthen the long-term opportunity landscape for the market.

Category-wise Analysis

Drug Type Insights

Sitagliptin is expected to continue its dominance with an estimated 39% DPP-IV market revenue share in 2026 due to its early market entry, extensive regulatory approvals, and deep clinical experience across geographies. Its broad acceptance stems from widespread physician familiarity and inclusion in treatment protocols for type 2 diabetes. Sitagliptin’s presence in both branded formulations and multiple generic listings enhances accessibility in developed and emerging markets alike. This leadership position is supported by continued generic expansion, with multiple manufacturers preparing additional generic DPP-IV inhibitor launches as patents expire. For example, regulatory activity in Japan indicates multiple copycat entries for established DPP-IV drugs such as sitagliptin, broadening availability and reinforcing its dominant presence.

Teneligliptin is anticipated to be the fastest-growing drug type, particularly in Asia Pacific markets where healthcare systems emphasize cost-effective therapy. This segment is projected to grow at a CAGR of approximately 8.2% from 2026 to 2033, driven by competitive pricing and increasing adoption in countries such as India and Japan. Teneligliptin’s rapid uptake reflects broader trends in generic preference and region-specific prescribing behavior, where price sensitivity is high and access barriers lower than in mature markets. Local manufacturers are expanding production tailored to regional formularies, further accelerating growth. Volume expansion for Teneligliptin positions it as an important future driver for drug-type diversification within the DPP-IV inhibitor class.

Medication Type Insights

Branded medications are projected to maintain leadership, capturing an estimated 47% of the DPP-IV market share in 2026, particularly in North America and Europe where payer confidence and long-standing brand recognition influence prescribing behavior. These products benefit from strong safety data and entrenched formulary coverage, supporting premium pricing even under competitive pressure. Brand loyalty remains a key differentiator in established markets, where physicians and insurers prioritize long-term clinical evidence and predictable outcomes. This leadership is reinforced by expanded regulatory indications for branded drugs in related therapy areas, which helps sustain market visibility amid shifting treatment dynamics.

Generic medications are poised to be the fastest-growing category by volume, with projected 7.5% CAGR during the 2026–2033 forecast period, as patent expirations and regulatory incentives broaden access. Government support for generic development including streamlined regulatory pathways and forums such as the U.S. Food and Drug Administration (FDA)’s Generic Drugs Forum in April 2025, which enhanced industry engagement on generic approvals has helped accelerate approvals and market entry of multiple generic medications. This expanding availability is reshaping competitive dynamics by offering lower-cost alternatives that improve therapy access globally. Generics’ strong volume growth reflects wider treatment penetration, particularly in cost-sensitive healthcare systems that prioritize affordability without compromising clinical efficacy.

Regional Insights

North America DPP-IV Inhibitors Market Trends

North America is estimated to remain the largest regional market for DPP-IV inhibitors, accounting for approximately 37% of global market value in 2026, led by the United States. High diabetes prevalence, broad insurance coverage, and early adoption of branded oral antidiabetic therapies underpin regional leadership. Well-established prescribing practices and strong outpatient management frameworks support sustained utilization across care settings. The region’s robust pharmaceutical ecosystem enables rapid integration of combination therapies and effective post-approval lifecycle strategies. These structural advantages collectively position North America as the value anchor of the global market.

Recent policy developments reinforce affordability and long-term access while maintaining volume stability. In 2026, the U.S. Centers for Medicare & Medicaid Services (CMS) initiated the first implementation phase of negotiated pricing under the Inflation Reduction Act, expanding patient access to select oral antidiabetic therapies within Medicare Part D formularies. While pricing pressure is expected to persist, broader coverage is likely to support consistent prescription volumes. The overall growth is projected to be moderate, reflecting market maturity and intensifying therapeutic competition.

Europe DPP-IV Inhibitors Market Trends

Europe continues to represent a mature yet resilient market for DPP-IV inhibitors, with Germany, the U.K., France, and Spain serving as the primary contributors. The region benefits from a harmonized regulatory environment overseen by the European Medicines Agency (EMA), which ensures consistent safety, efficacy, and approval standards across member states. Demand is supported by well-established diabetes care pathways and sustained reliance on oral antidiabetic therapies during early and mid-stage disease management. Strong primary care infrastructure, combined with routine monitoring and follow-up, helps maintain steady prescription volumes. Even amid pricing constraints, clinical familiarity and predictable treatment outcomes continue to support baseline demand.

In 2025, the U.K.’s National Institute for Health and Care Excellence (NICE) revised its type 2 diabetes treatment guidance to reinforce the use of cost-effective oral therapies within structured stepped-care pathways. This update supports the continued role of DPP-IV inhibitors in defined patient populations where safety and tolerability are prioritized. Across Europe, similar reimbursement decisions increasingly favor generics, limiting premium pricing flexibility while preserving broad patient access. These dynamics restrain value expansion but stabilize utilization levels. Consequently, the European market is expected to grow at a contained growth rate, with growth driven more by treatment continuity than pricing uplift

Asia Pacific DPP-IV Inhibitors Market Trends

Asia Pacific is projected to be the fastest-growing regional market for DPP-IV inhibitors, expanding at an estimated 8% CAGR between 2026 and 2033. The growth is driven by China, India, Japan, and key ASEAN economies, where rapid urbanization, dietary shifts, and sedentary lifestyles are contributing to rising diabetes prevalence. Improving diagnosis rates and broader screening initiatives are expanding the treated patient pool. Increased access to affordable oral antidiabetic therapies is accelerating treatment uptake. Large population bases and rising public healthcare expenditure further amplify volume-driven demand dynamics across the region.

Policy and regulatory developments continue to reinforce this growth trajectory. China’s National Medical Products Administration (NMPA) approved multiple additional generic oral antidiabetic formulations while strengthening their inclusion within provincial reimbursement lists. Similarly, several ASEAN countries expanded national essential medicines lists in 2026 to prioritize affordable diabetes treatments under public health programs. Strong regional pharmaceutical manufacturing capacity enhances supply reliability and cost efficiency. These factors position Asia Pacific as a central contributor to global volume growth and ongoing competitive realignment within the DPP-IV inhibitors market.

Competitive Landscape

The global DPP-IV inhibitors market structure is moderately consolidated, with leading pharmaceutical companies such as Merck & Co., Boehringer Ingelheim, AstraZeneca, Novartis, and Takeda Pharmaceutical accounting for a substantial share of global revenue. These players benefit from strong brand recognition, extensive clinical evidence, and established relationships with healthcare providers and payers. Broad regulatory approvals and continued investment in lifecycle management and fixed-dose combinations support their market leadership, particularly in North America and Europe.

Alongside global leaders, regional and generic manufacturers are strengthening their presence, especially in Asia Pacific and Latin America, by leveraging cost-efficient production and local regulatory expertise. Entry barriers remain moderate due to regulatory and pharmacovigilance requirements, though patent expirations have widened access for new participants. The market is expected to see gradual consolidation through licensing agreements and portfolio acquisitions, while digital distribution channels and combination therapies increasingly influence competitive positioning.

Key Industry Developments

- In February 2026, Novo Nordisk announced that it will launch new oral Ozempic (semaglutide) tablet doses in the U.S. in the second quarter of 2026, after FDA approval of 1.5mg, 4mg, and 9mg doses of semaglutide under the Ozempic name, expanding its oral diabetes treatment portfolio and offering a differentiated delivery option that aligns with patient preference for non injectable therapies.

- In January 2026, Eli Lilly signed a strategic collaboration with Repertoire Immune Medicines worth up to US$ 1.93 billion to co2 develop innovative therapies for multiple autoimmune diseases, including treatments that could overlap with chronic diabetes care pathways.

- In January 2025, Zydus Lifesciences saw its stock rise after sitagliptin (Zituvio™) and combination products (Zituvimet™ and Zituvimet™ XR) received U.S. FDA approval and were included in a formulary via a strategic partnership with CVS Caremark, bolstering its presence in the U.S. diabetes market.

Companies Covered in DPP-IV Inhibitors Market

- Merck & Co.

- AstraZeneca

- Boehringer Ingelheim

- Novartis

- Takeda Pharmaceutical

- Sun Pharmaceutical Industries

- Lupin Limited

- Dr. Reddy’s Laboratories

- Cipla Limited

- Glenmark Pharmaceuticals

- Pfizer Inc.

- Mylan

Frequently Asked Questions

The global DPP-IV inhibitors market is projected to reach US$ 15.2 billion in 2026.

Rising prevalence of type 2 diabetes, favorable safety profiles of DPP-IV inhibitors, and expanding access through generics and digital pharmacies are key growth drivers.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Growth opportunities include expanding diabetes screening in emerging markets, increasing the adoption of fixed-dose combinations, and rapid expansion of online pharmacy channels.

Merck & Co., Boehringer Ingelheim, AstraZeneca, Novartis, and Takeda Pharmaceutical are among the leading market participants.