- Pharmaceuticals

- Diuretic Drugs Therapy Market

Diuretic Drugs Therapy Market Size, Share, and Growth Forecast, 2025 - 2032

Diuretic drugs therapy market by Product Type (Thiazide Diuretics, Loop Diuretics, Potassium-Sparing Diuretics, Calcium-Sparing Diuretics, Osmotic Diuretics, Low Ceiling Diuretics, Others), Route of Administration (Oral, Intravenous), Application (Hypertension, Glaucoma, Heart Failure, Kidney Stones, Others), and Regional Analysis for 2025 - 2032

Diuretic Drugs Therapy Market Size and Trends Analysis

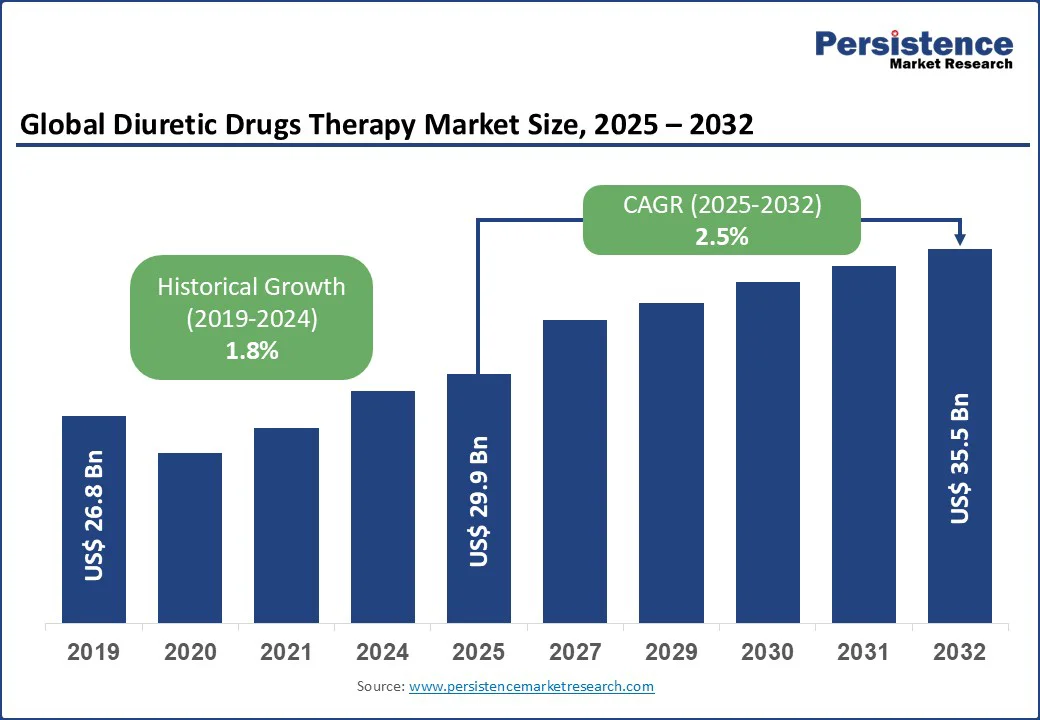

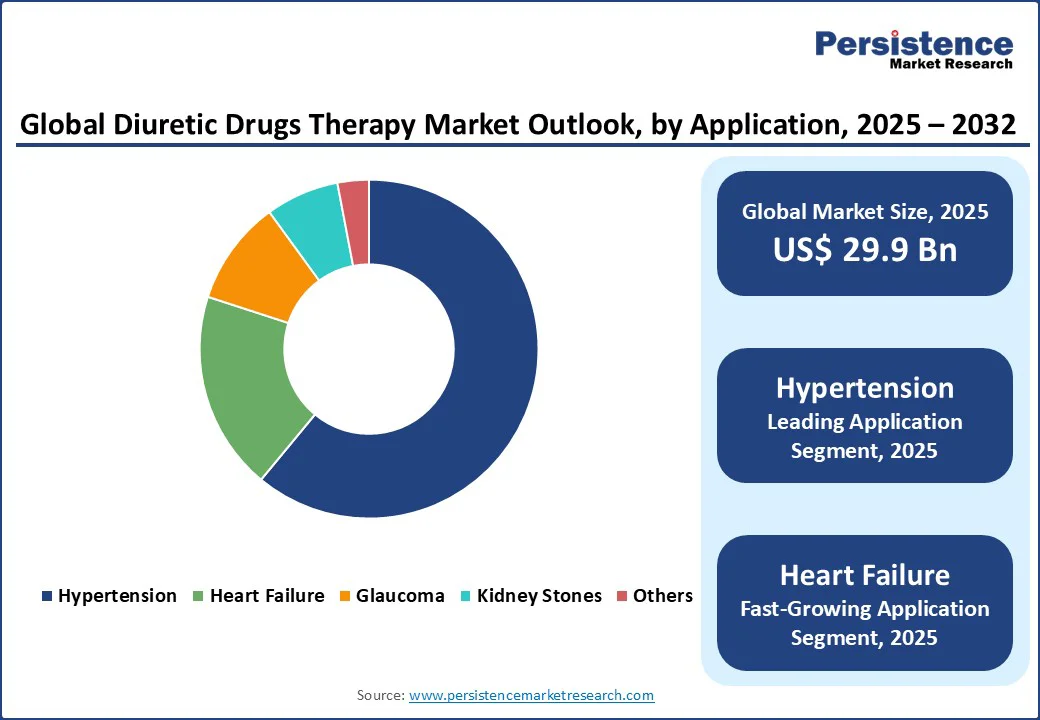

The global diuretic drugs therapy market size is likely to be valued at US$ 29.9 Bn in 2025 and reach US$ 35.5 Bn by 2032, registering a CAGR of 2.5% during the forecast period from 2025 to 2032.

The increasing prevalence of chronic conditions such as hypertension, heart failure, and kidney-related disorders, coupled with an aging global population, encourages the need for diuretic drugs therapy.

The demand for effective diuretic therapies is further fueled by advancements in pharmaceutical formulations, growing awareness of disease management, and the expansion of healthcare infrastructure in emerging economies. The sector is supported by the critical role diuretics play in managing fluid retention and related conditions, making them a cornerstone of treatment across various medical applications.

Key Industry Highlights:

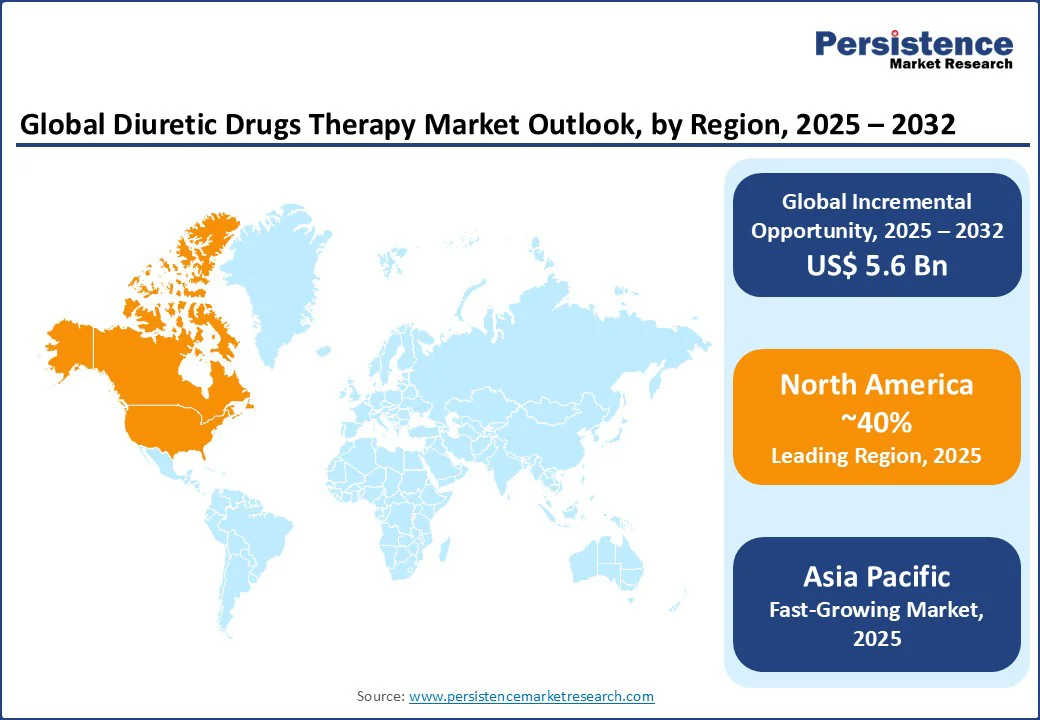

- Leading Region: North America, holding a 40% market share in 2025, driven by advanced healthcare systems, high prevalence of cardiovascular diseases, and robust pharmaceutical R&D.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization, increasing healthcare expenditure, and rising awareness of chronic disease management. Europe is advancing through initiatives such as the EU’s focus on precision medicine and increased funding for cardiovascular research.

- Dominant Product Type: Thiazide Diuretics, commanding nearly 48% market share, reflecting their widespread use in hypertension and heart failure management.

- Leading Application: Hypertension, accounting for over 61% of market revenue, driven by the global rise in cardiovascular conditions.

- Historical Growth: The sector registered a CAGR of 1.8% from 2019 to 2024, driven by increasing demand for effective diuretic therapies and improved access to healthcare.

|

Global Market Attribute |

Key Insights |

|

Diuretic Drugs Therapy Market Size (2025E) |

US$29.9 Bn |

|

Market Value Forecast (2032F) |

US$ 35.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

2.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

1.8% |

Market Dynamics

Driver - Rising Prevalence of Cardiovascular and Kidney-Related Disorders

The rising prevalence of cardiovascular and kidney-related disorders is a major driver fueling the growth of the diuretic drugs therapy market. Conditions such as hypertension, heart failure, chronic kidney disease (CKD), and edema are increasing globally due to aging populations, sedentary lifestyles, poor dietary habits, and rising obesity rates.

According to the World Health Organization (WHO), cardiovascular diseases remain the leading cause of death worldwide, while CKD affects millions, often progressing silently until advanced stages.

Diuretics play a crucial role in managing these conditions by helping reduce excess fluid, lowering blood pressure, and easing the workload on the heart and kidneys. Their effectiveness, affordability, and inclusion in standard treatment guidelines make them a preferred choice among healthcare providers. Moreover, the growing awareness of early diagnosis and treatment, coupled with improved healthcare access in emerging markets, is expanding the patient base.

For instance, the U.S. Centers for Disease Control and Prevention (CDC) reports that nearly half of U.S. adults have hypertension, many of whom rely on diuretics as part of their treatment regimen. As the global burden of these chronic diseases continues to rise, the demand for diuretic therapies is expected to grow steadily.

Restraint - Side Effects and Drug Interactions

Side effects and drug interactions pose a significant restraint to the growth of the diuretic drugs therapy market. While diuretics are effective in managing conditions such as hypertension, heart failure, and kidney disorders, their use can lead to adverse effects, including dehydration, electrolyte imbalances (such as low potassium or sodium levels), dizziness, and muscle cramps. Long-term use may also increase the risk of metabolic complications such as gout or increased blood sugar levels.

Diuretics can interact with other commonly prescribed medications, such as antihypertensives, lithium, and certain diabetes drugs, potentially altering their effectiveness or increasing the risk of toxicity. These safety concerns often lead to cautious prescribing practices by healthcare providers, especially for elderly patients or those with multiple comorbidities.

For instance, potassium-sparing diuretics may cause hyperkalemia when combined with ACE inhibitors or ARBs, posing serious cardiac risks. Such side effects and interactions can reduce patient adherence and slow the growth potential.

Opportunity - Advancements in Drug Formulations to Fuel Growth

Advancements in drug formulations present a significant opportunity for the growth of the diuretic drugs therapy market. Pharmaceutical companies are increasingly focusing on developing innovative formulations that improve efficacy, reduce side effects, and enhance patient compliance.

New approaches include extended-release tablets, fixed-dose combinations with other antihypertensives, and formulations designed to minimize electrolyte imbalances. These innovations not only improve therapeutic outcomes but also reduce the frequency of dosing, making treatment more convenient for patients, particularly those on long-term therapy.

Additionally, research into targeted delivery systems and novel diuretic molecules aims to address limitations associated with traditional drugs, such as dehydration or metabolic disturbances.

For instance, combination therapies integrating thiazide diuretics with ACE inhibitors or ARBs are gaining popularity, as they improve blood pressure control while mitigating potassium loss. Such advancements can expand the sector by attracting more prescribers and enhancing patient adherence, ultimately driving sustained demand in both developed and emerging regions.

Category-wise Analysis

Product Type Insights

Thiazide diuretics dominate and are expected to account for approximately 48% share in 2025. Their dominance stems from their widespread use in managing hypertension and heart failure due to their efficacy in reducing blood pressure and fluid retention.

Thiazide diuretics, such as hydrochlorothiazide, are cost-effective and well-tolerated, making them a first-line treatment in clinical guidelines globally. Their compatibility with combination therapies further enhances their applicability across various patient populations.

The loop diuretics segment is the fastest-growing driven by increasing demand for managing severe edema associated with heart failure and kidney disorders. Loop diuretics, such as furosemide, offer rapid and potent diuretic effects, making them ideal for acute conditions requiring immediate fluid removal.

The rise in hospital admissions for heart failure, particularly in aging populations, and advancements in intravenous formulations are accelerating the adoption of loop diuretics, especially in North America and Europe.

Route of Administration Insights

Oral administration holds the largest market share, accounting for approximately 60% of revenue in 2025. Its popularity is driven by its convenience, cost-effectiveness, and widespread use in outpatient settings for chronic conditions such as hypertension and heart failure. Oral diuretics, such as thiazides and potassium-sparing diuretics, are easy to administer and widely prescribed, supporting their dominance in the industry.

Intravenous administration is the fastest-growing segment, fueled by its critical role in acute care settings, such as hospitals and emergency departments. Intravenous diuretics, particularly loop diuretics, are essential for managing acute heart failure and severe edema, where rapid fluid removal is required.

The increasing prevalence of cardiovascular emergencies and advancements in intravenous drug delivery systems are driving the rapid adoption of this segment, particularly in developed markets.

Application Insights

Hypertension accounts for a 61% share and is leading in 2025. The segment’s dominance is driven by the global surge in cardiovascular diseases, with diuretics being a cornerstone of hypertension management due to their efficacy and affordability. Major clinical guidelines, such as those from the American Heart Association, recommend diuretics as a first-line treatment, further boosting their adoption.

The Heart Failure segment is the fastest-growing, driven by the increasing incidence of heart failure globally, particularly among aging populations. According to the American College of Cardiology, heart failure affects over 6 million adults in the U.S. alone, with diuretics playing a critical role in managing fluid overload. The growing demand for effective therapies in acute and chronic heart failure settings is accelerating the adoption of diuretics in this segment.

Regional Insights

North America Diuretic Drugs Therapy Market Trends

North America, holding a 40% market share in 2025, dominates the global diuretic drugs therapy market due to its advanced healthcare infrastructure, strong pharmaceutical industry, and high disease prevalence. The region has a significant burden of cardiovascular diseases, hypertension, and chronic kidney disorders, which are key indications for diuretic use.

According to the Centers for Disease Control and Prevention (CDC), nearly half of U.S. adults have hypertension, and cardiovascular diseases remain the leading cause of death. The availability of state-of-the-art diagnostic facilities ensures early detection and treatment, further boosting demand for diuretics.

Additionally, robust pharmaceutical research and development (R&D) in the U.S. and Canada contribute to the introduction of innovative drug formulations and combination therapies, improving treatment outcomes and patient compliance.

Government healthcare programs such as Medicare and Medicaid, along with favorable reimbursement policies, enhance accessibility to these medications. Moreover, the growing aging population, sedentary lifestyles, and rising obesity rates continue to fuel the demand for diuretic therapies, solidifying North America’s position as the leading market for this drug category in the forecast period.

Europe Diuretic Drugs Therapy Market Trends

Europe holds a significant share of the global diuretic drugs therapy market, driven by robust healthcare systems, advanced pharmaceutical manufacturing, and the growing adoption of precision medicine. Leading countries include Germany, the UK, and France. Germany benefits from its robust pharmaceutical industry and leadership in cardiovascular research, with companies such as Novartis investing heavily in innovative diuretic formulations.

The UK’s market is bolstered by the rising prevalence of hypertension and government initiatives promoting early diagnosis and treatment. France’s market is supported by significant investments in healthcare infrastructure and a focus on sustainable pharmaceutical practices. The EU’s stringent regulations, such as the European Medicines Agency’s guidelines on drug safety, drive the adoption of high-quality diuretic therapies; however, compliance with these complex regulations poses challenges. Europe’s diuretic drugs therapy market is projected to grow steadily from 2025 to 2032.

Asia Pacific Diuretic Drugs Therapy Market Trends

Asia Pacific is emerging as one of the fastest-growing regions in the diuretic drugs therapy market, fueled by rapid urbanization, increasing healthcare expenditure, and rising awareness of chronic disease management. The region is witnessing a surge in lifestyle-related conditions such as hypertension, heart failure, and chronic kidney disease, driven by changing dietary habits, sedentary lifestyles, and aging populations.

Countries such as China, India, and Japan are investing heavily in healthcare infrastructure, improving access to diagnostics and treatment options. Growing government initiatives to promote early detection and management of cardiovascular and kidney disorders are further driving demand for diuretic therapies.

According to the World Health Organization (WHO), Asia is home to a large proportion of the global hypertensive population, making it a significant target market for diuretic drugs. Rising healthcare spending, expanding pharmaceutical manufacturing capabilities, and the availability of affordable generic medications are enhancing market accessibility.

Additionally, increasing patient education and awareness campaigns about the benefits of early treatment are encouraging adoption, positioning the Asia Pacific as a key growth engine for the diuretic drugs therapy market in the coming years.

Competitive Landscape

The global diuretic drugs therapy market is characterized by intense competition, regional strengths, and a mix of global and local pharmaceutical manufacturers. In developed regions such as North America and Europe, large firms such as Sanofi, Merck & Co., and Pfizer dominate through scale, advanced R&D capabilities, and established partnerships with healthcare providers.

In the Asia Pacific, rapid growth in healthcare infrastructure and generic drug production is attracting significant investments from both local and international players. Companies are focusing on innovation, cost-efficiency, and strategic alliances to gain a competitive edge.

The development of novel formulations and combination therapies has emerged as a key differentiator, enabling faster market penetration and improved patient outcomes. Strategic partnerships and acquisitions are further intensifying the competitive landscape.

Overall, the market shows a dual nature consolidated at the top by global giants like Pfizer and Sanofi, while fragmented and scattered across numerous regional and generic manufacturers such as Cipla in India, which actively supplies affordable diuretic drugs to emerging markets.

Industry Developments:

- In January 2023, Glenmark launched a generic version of bumetanide injection, available in 1 mg/4 mL single-dose and 2.5 mg/10 mL multi-dose vials. This product is targeted at treating fluid retention associated with congestive heart failure, liver disease, and kidney disease.

- In October 2022, the FDA approved FUROSCIX, a subcutaneous formulation of furosemide designed for heart failure patients. This innovation offers an at-home, injectable alternative to IV diuretics for fluid overload management.

Companies Covered in Diuretic Drugs Therapy Market

- Sanofi

- Merck & Co.

- Pfizer

- Teva Pharmaceutical Industries

- Mylan

- Novartis

- GlaxoSmithKline (GSK)

- Roche

- Cipla

- AstraZeneca

- Others

Frequently Asked Questions

The Global Diuretic Drugs Therapy market is projected to reach US$ 29.9 Bn in 2025.

The rising prevalence of cardiovascular and kidney-related disorders is a key driver.

The Diuretic Drugs Therapy market is poised to witness a CAGR of 2.5% from 2025 to 2032.

Advancements in drug formulations, such as extended-release and combination therapies, are a key opportunity.

Sanofi, Merck & Co., Pfizer, Teva Pharmaceutical Industries, and Novartis are key players.