- Technology

- Data Centre Infrastructure Market

Data Centre Infrastructure Market Size, Share, and Growth Forecast 2026 - 2033

Data Centre Infrastructure Market by Offering Type (Solution, Service), Data Centre Type (Enterprise Data Centre, Managed Data Centre, Colocation Edge Data Centre, Cloud and Edge Data Centre), Deployment Outlook (On-Premises, Cloud), Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises), End Use (BFSI, Government and Public Sector, IT and ITeS, Manufacturing, Healthcare and Life Science, Others), and Regional Analysis for 2026 - 2033

Data Centre Infrastructure Market Size and Trend Analysis

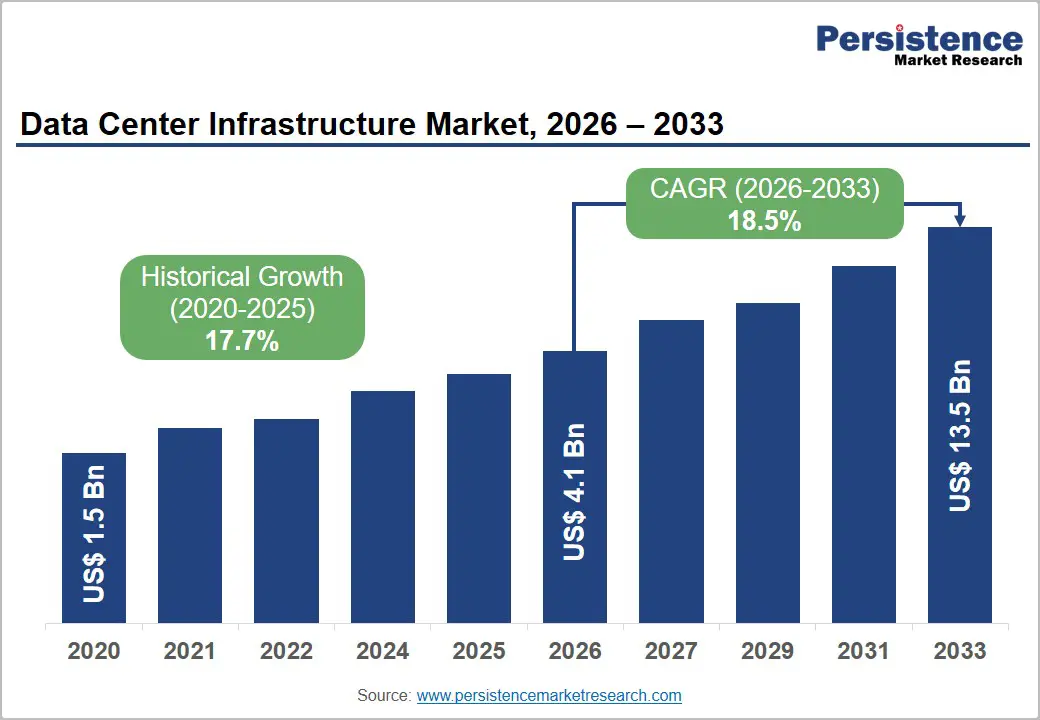

The global data centre infrastructure market size is supposed to be valued at US$ 4.1 billion in 2026 and is projected to reach US$ 13.5 billion by 2033, growing at a CAGR of 18.5% between 2026 and 2033. This expansion is primarily driven by the exponential growth of artificial intelligence workloads, cloud adoption, and hyperscale computing deployments worldwide.

The International Data Corporation (IDC) has consistently highlighted surging enterprise spending on compute, storage, networking, and power infrastructure to support digitization initiatives.

Key Industry Highlights:

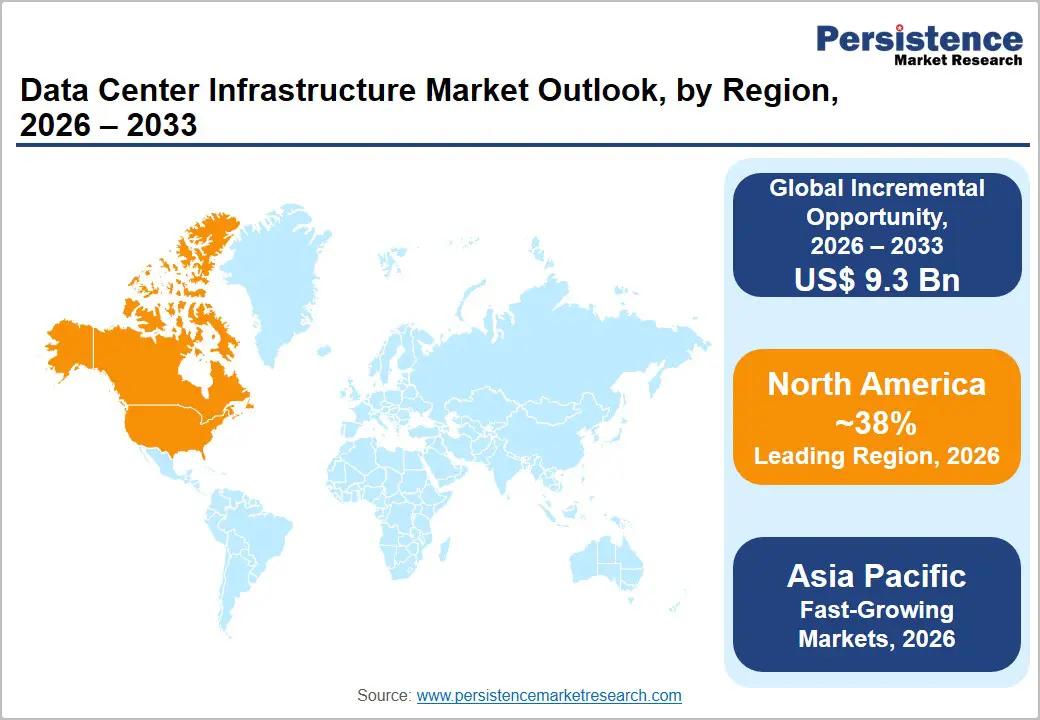

- Leading Region: North America leads the global data centre infrastructure market with approximately 38% share in 2026, anchored by hyperscale cloud provider campuses, AI-driven infrastructure densification, and the world's largest concentration of colocation and internet exchange assets.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by China's "East Data, West Computing" policy, India's greenfield data Centre buildout under Digital India, and enterprise cloud modernization across Japan and Southeast Asia, collectively sustaining above-average CAGR through 2033.

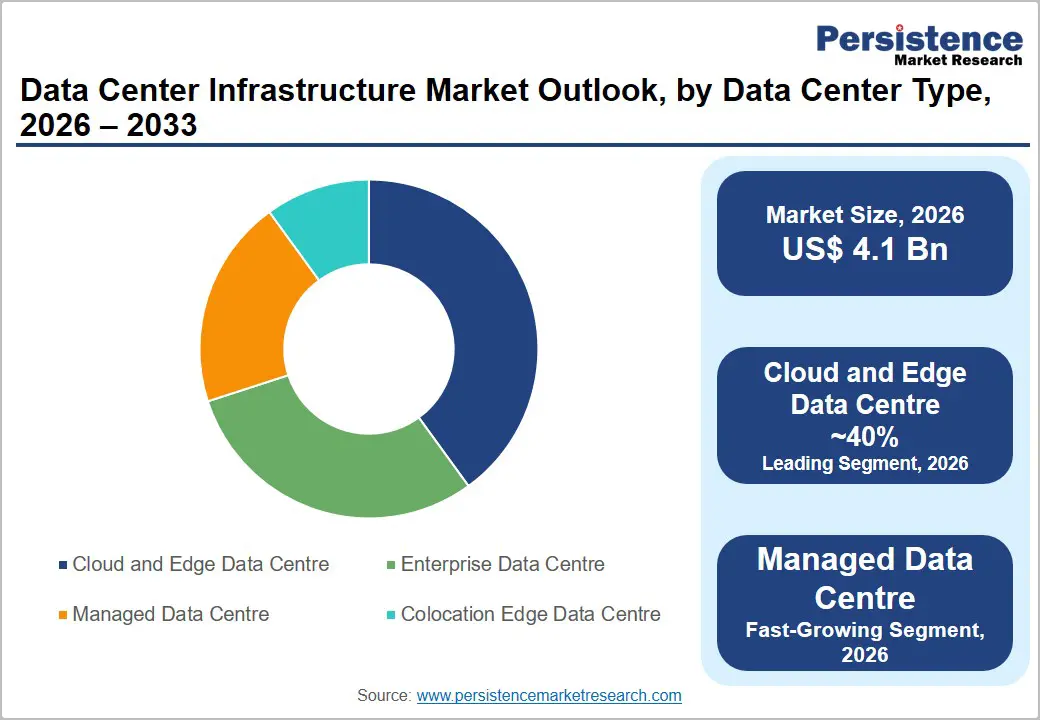

- Dominant Segment: Cloud and Edge Data Centres dominate the data Centre type category with approximately 40% market share in 2025, reflecting the structural migration of enterprise workloads to hyperscale cloud environments and the rapid expansion of edge computing nodes to support 5G and IoT applications.

- Fastest Growing Segment: BFSI is the fastest-growing end-use vertical, propelled by digital banking transformation, core system modernization, and the EU's Digital Operational Resilience Act (DORA), compelling financial institutions to invest in resilient, compliant, low-latency data Centre infrastructure.

- Key Opportunity: AI-ready infrastructure modernization represents the most actionable near-term opportunity over 60% of enterprise data Centre operators plan major AI-oriented upgrades, creating exceptional demand for liquid cooling, high-density racks, and GPU-optimized power distribution systems.

DRO Analysis

Drivers - Explosive Growth of AI and Hyperscale Cloud Workloads Driving Infrastructure Investment

The rapid commercialization of generative artificial intelligence and machine learning applications is fundamentally reshaping data Centre infrastructure requirements, compelling enterprises and hyperscalers to invest in high-density compute, GPU clusters, high-speed networking, and advanced cooling systems at unprecedented speed and scale.

Synergy Research Group reported that hyperscale data Centre operators, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, collectively committed over US$ 200 billion in capital expenditure in 2023 alone, with AI infrastructure representing a growing share of that spend.

The U.S. Department of Energy projects that data Centre electricity consumption in the U.S. could double by 2026 under accelerated AI deployment scenarios, directly translating into demand for power distribution, cooling, and modular infrastructure solutions.

Digital Transformation Mandates and Cloud-First Enterprise Strategies Expanding the Addressable Market

Enterprise-wide digital transformation programs are extending data Centre infrastructure demand beyond traditional hyperscalers to mid-market enterprises, government agencies, and regulated industry verticals, broadening the addressable market for infrastructure vendors.

The World Economic Forum estimates that digital transformation will add US$ 100 trillion in value to the global economy by 2025, and the infrastructure enabling that transformation, servers, storage arrays, networking switches, UPS systems, and precision cooling, represents the physical foundation of this shift. Gartner data indicates that global IT spending on data Centre systems surpassed US$ 270 billion in 2023, growing at double-digit rates year-over-year.

Restraints - High Capital Expenditure and Energy Costs Creating Adoption and Profitability Barriers

The capital-intensive nature of data Centre infrastructure deployment, encompassing land acquisition, civil construction, power and cooling systems, networking, and security, creates a substantial financial barrier for smaller enterprises and emerging market operators seeking to build or upgrade facilities.

A hyperscale data Centre campus can require US$ 1 billion or more in upfront investment, and the total cost of ownership is amplified by energy costs that can represent 30–40% of operational expenditure. The International Energy Agency (IEA) estimates that global data Centres consumed approximately 240–340 TWh of electricity in 2022, and with energy prices remaining elevated in Europe and parts of Asia, operating margins for colocation and managed service providers are under sustained pressure.

Sustainability Regulations and Water Consumption Constraints Complicating Site Development

Stringent environmental regulations and growing scrutiny of data Centre water and energy consumption are creating compliance complexity and site development constraints that slow infrastructure expansion in key markets. The European Union's Energy Efficiency Directive mandates that data Centres above 500 kW report sustainability metrics under the European Green Deal framework, and several EU member states, including the Netherlands and Ireland, have introduced moratoriums or restrictions on new hyperscale data Centre permits in major cities due to power grid capacity concerns.

The Water Research Foundation has documented that air-cooled data Centres consume significant volumes of water for evaporative cooling, a growing concern in drought-prone regions. For operators and infrastructure vendors, navigating this regulatory landscape adds development timeline risk and capital cost, particularly in markets where sustainability standards are tightening faster than grid infrastructure can be expanded.

Opportunities - Edge Computing Expansion, Creating Distributed Infrastructure Demand

The proliferation of edge computing processing data closer to the point of generation to reduce latency for applications such as autonomous vehicles, industrial IoT, smart healthcare, and real-time analytics is creating a new and rapidly expanding demand pool for distributed data Centre infrastructure that operates outside the traditional hyperscale or enterprise data Centre paradigm.

The Linux Foundation's LF Edge initiative and the European Telecommunications Standards Institute (ETSI) have both published frameworks positioning multi-access edge computing (MEC) as a foundational architecture for 5G network deployments, and telecom operators globally are investing in edge nodes co-located with cell towers and network exchange points.

AI-Ready Infrastructure Upgrades Driving Accelerated Replacement Cycles in Enterprise Data Centres

The incompatibility of legacy enterprise data Centre infrastructure with the high-density power, liquid cooling, and high-bandwidth networking requirements of AI accelerator clusters is compelling a wave of infrastructure replacement and modernization investment among organizations that cannot afford to deploy exclusively in the cloud.

The Uptime Institute's global data Centre survey indicates that over 60% of enterprise data Centre operators plan significant infrastructure upgrades within the next two years to support AI and machine learning workloads, and this upgrade cycle is creating exceptional demand for high-density server racks (30–100 kW+ per rack), direct liquid cooling systems, high-bandwidth networking (400G/800G), and modular UPS with improved efficiency ratings.

Category-wise Analysis

Offering Type Insights

The solution segment commands approximately 65% of the global data Centre infrastructure market by offering type in 2026, reflecting the capital-intensive nature of physical infrastructure procurement encompassing servers, storage systems, networking equipment, power distribution units, UPS systems, and precision cooling that organizations must deploy before any managed service or software layer can be consumed.

The dominance of the solution segment is reinforced by the ongoing buildout of hyperscale and colocation facilities, where physical equipment procurement represents the largest spend category per project. The IDC Worldwide Datacentre Tracker consistently reports that hardware infrastructure investments dwarf services spending in new facility deployments.

Data Centre Type Insights

Cloud and edge data Centres account for approximately 40% of the global market by data Centre type in 2025, a position that reflects the structural migration of enterprise workloads to cloud environments and the emergence of distributed edge nodes as a complement to centralized hyperscale infrastructure.

The Synergy Research Group reports that the hyperscale cloud segment, dominated by AWS, Microsoft Azure, Google Cloud, Alibaba Cloud, and Meta, accounts for most new data Centre capacity additions globally, and this momentum shows no sign of abating as AI workload demands incentivize further capital deployment.

Deployment Outlook Insights

The cloud deployment segment holds approximately 62% of the global data Centre infrastructure market by deployment outlook in 2026, driven by the overwhelming preference of enterprise and government clients for cloud-hosted or cloud-managed infrastructure over fully on-premises deployments.

The Flexera 2024 State of the Cloud Report found that 89% of enterprises have adopted a multi-cloud strategy, and the infrastructure investments supporting these deployments, whether in the form of direct purchases by cloud providers or colocation agreements by enterprises, flow predominantly into cloud-aligned infrastructure categories.

Enterprise Size Insights

Large enterprises account for approximately 72% of the global data centre infrastructure market by enterprise size in 2026, underpinned by their disproportionate IT budgets, complex multi-site infrastructure requirements, and strategic investment in AI, analytics, and digital platform capabilities that demand sophisticated data Centre deployments.

The Gartner CIO and Technology Executive Survey consistently finds that Fortune 500 organizations allocate the majority of IT capital expenditure to infrastructure, including servers, storage, and networking, and large enterprises are the primary customers for hyperscale colocation, direct cloud consumption, and on-premises AI cluster deployments.

End-user Insights

The IT and ITeS sector leads the end-use category with approximately 30% of the global data Centre infrastructure market in 2026, a position that reflects the sector's fundamental role as both a primary consumer and a commercial intermediary for data Centre services operating managed services, cloud platforms, and software delivery infrastructure on behalf of clients across all other verticals. IT and ITeS firms, including hyperscalers, system integrators, and managed service providers, are the largest individual procurers of data Centre hardware, driving demand for servers, networking, and cooling equipment.

Regional Analysis

North America Data Centre Infrastructure Market Trends & Analysis

North America leads the global data Centre infrastructure market with approximately 38% share in 2025, anchored by the world's largest concentration of hyperscale data Centre campuses, a mature colocation ecosystem, and the headquarters presence of the dominant cloud providers Amazon, Microsoft, Google, Meta, and Apple. The region benefits from a well-established regulatory environment, abundant land in secondary markets (Phoenix, Columbus, Dallas, and Atlanta), and a growing availability of renewable energy that is enabling hyperscalers to meet sustainability commitments while expanding capacity.

U.S. Data Centre Infrastructure Market Size

The U.S. accounts for approximately 85% of the North American data Centre infrastructure market, representing the world's single largest national market by installed capacity and annual capital investment. Northern Virginia (Ashburn) remains the globally dominant data Centre hub, hosting approximately 70% of the world's internet traffic according to the Data Centre Map industry tracker.

Europe Data Centre Infrastructure Market Trends, Drivers, & Insights

Europe accounts for approximately 22% of the global data Centre infrastructure market in 2025, with a sophisticated colocation and cloud ecosystem concentrated in the AMS-IX (Amsterdam), DE-CIX (Frankfurt), and London internet exchange hubs. The region faces a dual dynamic: strong digital transformation demand from enterprises across Germany, France, and the Nordics driving infrastructure investment, while simultaneously contending with stringent EU Green Deal sustainability requirements and power grid capacity constraints that are limiting new development permits in major cities.

Germany Data Centre Infrastructure Market Size

Germany represents approximately 20% of the European data Centre infrastructure market, with Frankfurt serving as the continent's premier financial data processing hub for the Deutsche Börse trading systems and a dense ecosystem of Tier III+ colocation facilities. The country's strong industrial base drives demand for manufacturing-oriented edge computing and private cloud infrastructure.

U.K. Data Centre Infrastructure Market Size

The U.K. accounts for approximately 18% of the European data centre infrastructure market, with London ranking as Europe's largest individual data centre market by total capacity. The post-Brexit regulatory environment has enabled some divergence from EU GDPR frameworks, and the UK Government's National Data Strategy positions data Centres as critical national infrastructure. Slough and the M4 corridor remain primary hyperscale development zones.

France Data Centre Infrastructure Market Size

France represents approximately 10% of European data centre infrastructure consumption, with Paris and its Île-de-France region dominating domestic capacity. OVHcloud's major hyperscale investments and the presence of Equinix, Digital Realty, and Interxion facilities are expanding the colocation ecosystem.

Asia Pacific Data Centre Infrastructure Market Drivers & Analysis

Asia Pacific accounts for approximately 30% of the global data centre infrastructure market in 2026 and is the world's fastest-growing region, driven by cloud adoption acceleration, government digital infrastructure mandates, and the emergence of China as the world's second-largest data Centre economy after the United States. China alone accounts for approximately 40% of Asia Pacific's data Centre infrastructure capacity, with Alibaba Cloud, Tencent Cloud, and Huawei Cloud operating large-scale hyperscale campuses across Beijing, Shanghai, and Guangzhou corridors.

China Data Centre Infrastructure Market Size

China represents approximately 40% of the Asia Pacific data Centre infrastructure market, underpinned by China's 14th Five-Year Plan for digital infrastructure that designates data Centres as a priority "new infrastructure" investment category and targets major capacity expansions in inner provinces to relieve coastal grid pressure under the "East Data, West Computing" policy initiative. Domestic hyperscalers, including Alibaba Cloud, ByteDance, and Huawei Cloud, are the primary infrastructure buyers, and government-mandated data localization requirements sustain domestically controlled infrastructure investment.

India Data Centre Infrastructure Market Size

India accounts for approximately 12% of the Asia Pacific data Centre infrastructure market and is the fastest-growing market, driven by India's Digital India initiative, rapid cloud adoption by enterprises, and a large and growing internet user base that surpassed 900 million active users as of 2024 per the Telecom Regulatory Authority of India (TRAI).

Japan Data Centre Infrastructure Market Size

Japan represents approximately 15% of the Asia Pacific data Centre infrastructure market, supported by a technologically mature enterprise base, active cloud modernization programs among major corporations, and government-backed digital transformation initiatives under the Digital Agency of Japan. Tokyo and Osaka anchor the domestic market, with NTT Communications, Equinix, and IIJ operating significant colocation capacity.

Competitive Landscape

The global data centre infrastructure market is moderately consolidated at the hyperscale infrastructure vendor tier, with a handful of global leaders, including Schneider Electric, Vertiv Holdings, Eaton Corporation, Cisco Systems, and HPE, commanding significant share in power, cooling, networking, and compute categories. Simultaneously, the market remains fragmented at the regional colocation, edge, and specialty segments, where hundreds of local and regional operators compete on proximity, connectivity, and service customization.

The dominant competitive strategy among market leaders is vertical portfolio integration, offering end-to-end infrastructure solutions spanning power, cooling, IT hardware, and management software to capture a larger wallet share per customer engagement.

Key Developments:

- In January 2026, Vertiv introduced updated configurations of its Vertiv MegaMod HDX, a prefabricated infrastructure solution designed to address the rising demands of high-density computing environments such as artificial intelligence (AI) and high-performance computing (HPC). The latest configurations provide greater flexibility for operators to manage increasing power and cooling requirements while improving space utilization and deployment timelines.

- In September 2025, Johnson Controls expanded its data centre thermal management portfolio with the introduction of the Silent-Aire Coolant Distribution Unit (CDU) platform, aimed at supporting the shift toward liquid cooling in high-density environments. The new CDU systems are designed to help data centres efficiently adapt to rising rack power densities by enabling seamless integration with liquid-cooling technologies.

Data Centre Infrastructure Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.5 Bn |

| Current Market Value (2026) | US$ 4.1 Bn |

| Projected Market Value (2033) | US$ 13.5 Bn |

| CAGR (2026-2033) | 18.5% |

| Leading Region | North America, 35% share |

| Dominant Application | Solution, 65% share |

| Top-ranking Product | solution, 40% |

| Incremental Opportunity | US$ 9.3 Bn |

Companies Covered in Data Centre Infrastructure Market

- Equinix

- Digital Realty Trust

- NTT Communications

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Schneider Electric

- Vertiv Holdings

- Eaton Corporation

- HPE

- Dell Technologies

- Cisco System

- IBM

- Siemens AG

- CommScope

- Legrand SA

- Airedale

- AdaniConneX,

- CtrlS Datacentres

- OVHcloud

Frequently Asked Questions

The global data centre infrastructure market is projected to grow from US$ 4.1 billion in 2026 to US$ 13.5 billion, expanding at a CAGR of 18.5% during the forecast period. This growth is underpinned by hyperscale cloud investment, AI workload proliferation, and enterprise digital transformation programs across all major geographies.

The primary drivers are the explosive growth of AI and generative AI workloads compelling hyperscalers to invest in high-density, AI-optimized infrastructure, and enterprise-wide digital transformation mandates expanding the addressable market to regulated industries including BFSI, government, and healthcare. Policy-backed programs such as India's Digital India, the EU's Digital Decade, and the U.S. CHIPS Act are creating sustained, government-supported infrastructure investment pipelines.

Cloud and edge data centres lead the data centre type category with approximately 40% market share in 2026. This dominance reflects the structural migration of enterprise and government workloads to hyperscale cloud environments operated by AWS, Microsoft Azure, Google Cloud, and Alibaba Cloud, combined with the rapid expansion of edge computing nodes supporting 5G and IoT deployments.

North America leads with approximately 38% share in 2026, anchored by the world's largest hyperscale data Centre campuses, the headquarters of dominant cloud providers including Amazon, Microsoft, and Google, and a mature colocation and interconnection ecosystem. The U.S. remains the single largest national market globally, with Northern Virginia hosting the world's densest concentration of data Centre capacity.

The most actionable opportunity is AI-ready infrastructure modernization. Over 60% of enterprise data Centre operators are planning major AI-oriented upgrades within two years, creating exceptional demand for liquid cooling systems, high-density racks, GPU-optimized UPS solutions, and high-bandwidth networking. Vendors offering validated, integrated AI-ready reference architectures, such as Schneider Electric, Vertiv, and HPE, are best positioned to capture this accelerating replacement cycle.

Key market players include Equinix, Inc., Digital Realty Trust, Schneider Electric SE, Vertiv Holdings Co., Eaton Corporation, Hewlett Packard Enterprise (HPE), Cisco Systems, Dell Technologies, NTT Communications, IBM Corporation, and Siemens AG. These companies compete through vertical portfolio integration, AI-optimized product launches, hyperscaler supply agreements, and geographic expansion into high-growth markets in the Asia Pacific and the Middle East.