- Industrial Goods & Service

- Chemical Injection Pump Market

Chemical Injection Pump Market Size, Share, and Growth Forecast 2026 - 2033

Chemical Injection Pump Market by Product Type (Diaphragm Pumps, Plunger Pumps, Piston Pumps, Peristaltic Pumps, Gear Pumps, Screw Pumps, Hydraulic Pumps, Pneumatic Pumps), Drive Type (Electric-Driven, Hydraulic-Driven, Pneumatic-Driven, Solar-Driven, Engine-Driven), Application, End-Use, and Regional Analysis, 2026 - 2033

Chemical Injection Pump Market Size and Trend Analysis

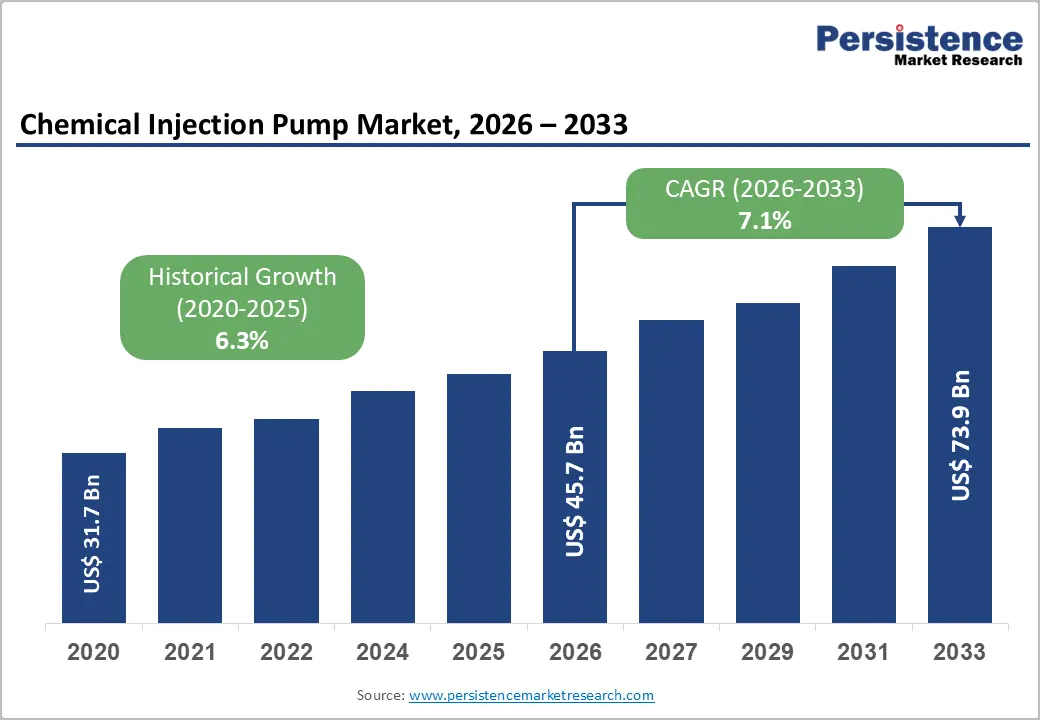

The global chemical injection pump market size is likely to be valued at US$ 45.7 billion in 2026 and is expected to reach US$ 73.9 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033.

The chemical injection pump market is driven by the global oil and gas industry’s sustained upstream and midstream infrastructure investment, rapidly expanding water and wastewater treatment obligations under tightening environmental regulations, and increasing adoption across pharmaceutical, food processing, and agricultural chemical dosing applications.

Key Industry Highlights:

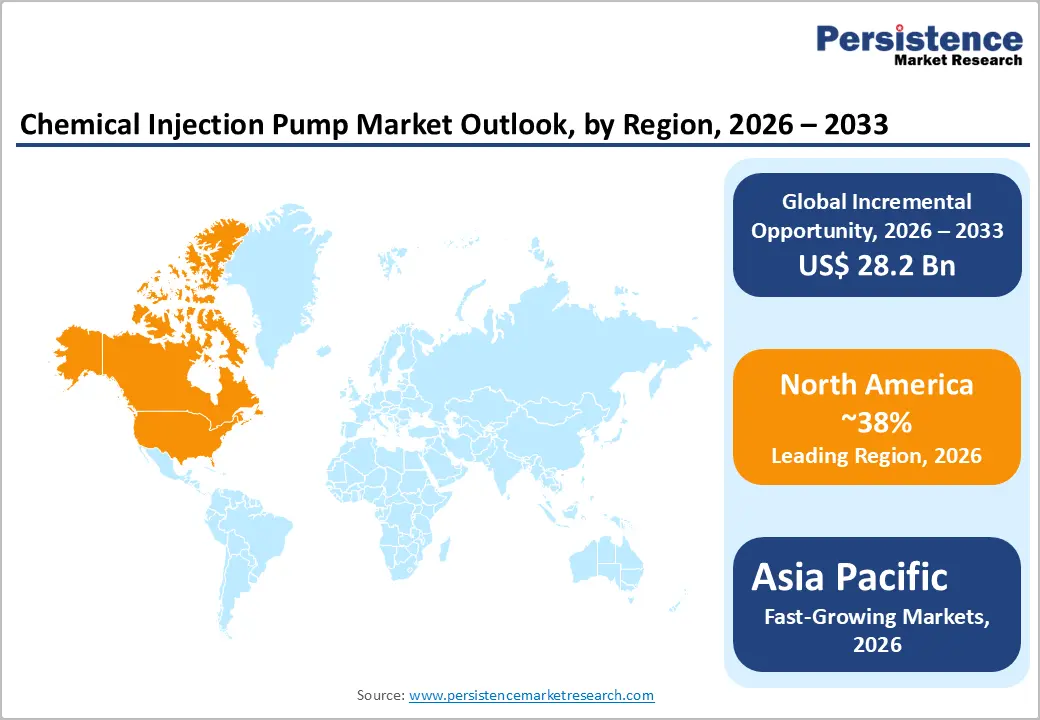

- Leading Region: North America leads the chemical injection pump market, holding 38% share, anchored by U.S. crude oil production exceeding 13 million barrels per day, the EPA Safe Drinking Water Act compliance driving water treatment chemical dosing investment, and the presence of global manufacturers, including Milton Roy, IDEX Corporation, and Dover Corporation.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR of 9.1%, driven by China’s 14th Five-Year Plan water treatment upgrades, India’s Jal Jeevan Mission universal water access infrastructure, and ASEAN’s expanding petrochemical and pharmaceutical manufacturing sectors generating growing chemical injection pump demand.

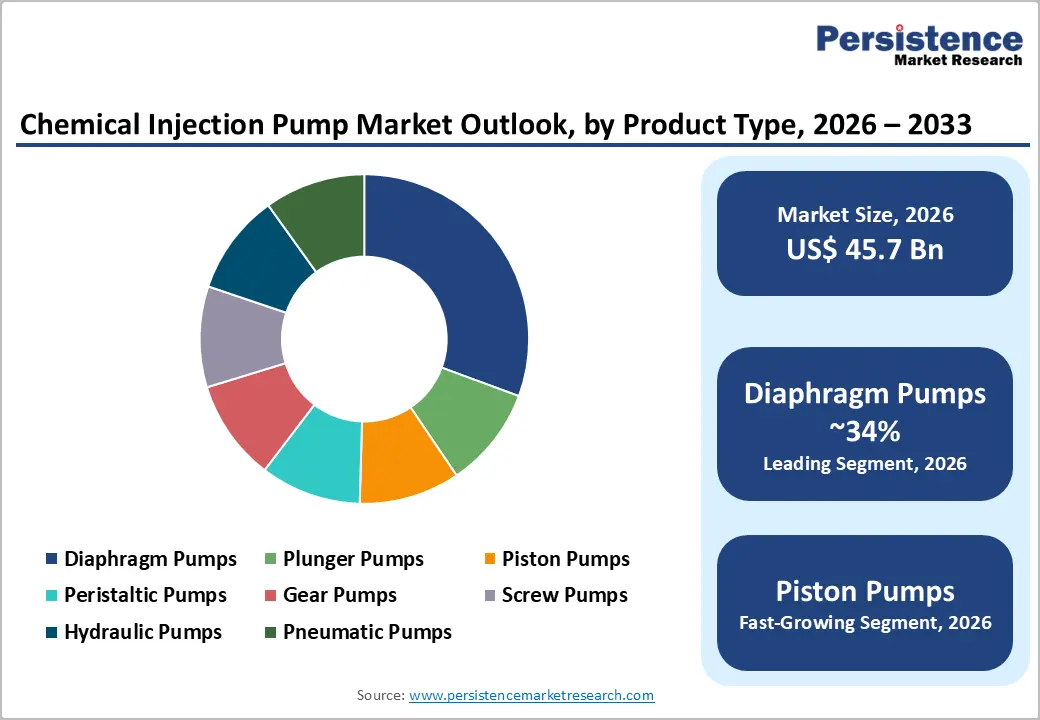

- Dominant Segment: Diaphragm Pumps lead the By Product Type category with approximately 34% market share, preferred for their leak-free hermetic design, ±1% metering accuracy, and compliance with API 675 and ISO 15783 standards across water treatment, pharmaceutical, and chemical dosing applications.

- Fastest Growing Segment: Solar-Driven pumps within the By Drive Type category are the fastest-growing segment, enabled by 90%+ solar cost reductions per BloombergNEF, creating economically viable remote oilfield and agricultural fertigation chemical injection applications previously constrained by grid power unavailability.

- Key Market Opportunity: Smart IoT-connected chemical dosing systems with cloud-based remote monitoring and automatic flow adjustment, endorsed by AWWA and WEF for water utility modernization, represent the highest-value innovation opportunity, with subscription-based monitoring services creating recurring revenue beyond initial equipment sales.

| Key Insights | Details |

|---|---|

| Chemical Injection Pump Market Size (2026E) | US$ 45.7 Billion |

| Market Value Forecast (2033F) | US$ 73.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 6.3% |

Market Dynamics

Drivers - Sustained Oil & Gas Upstream Investment and Aging Infrastructure Replacement

The oil and gas industry represents the largest and most capital-intensive end-use segment for chemical injection pumps, with wellhead corrosion inhibitor injection, scale inhibitor dosing, wax inhibitor injection, and H2S scavenging all requiring dedicated high-pressure chemical injection systems. The IEA’s World Energy Investment Report documents global upstream oil and gas investment recovering to over US$ 570 billion annually by 2023, with Middle East national oil companies, North American shale operators, and deep-water offshore projects driving equipment procurement.

Aging subsea and surface infrastructure in the North Sea, Gulf of Mexico, and Middle East fields is creating significant capital expenditure on chemical injection system upgrades and replacements. The International Association of Oil & Gas Producers (IOGP) has published standards for chemical injection systems that drive equipment specification requirements, supporting demand for certified, precision-metered chemical injection pump systems from qualified manufacturers.

Expanding Water & Wastewater Treatment Infrastructure Investment

Global water scarcity, urban population growth, and tightening environmental discharge standards are driving unprecedented investment in municipal and industrial water treatment infrastructure, a sector that requires chemical dosing pumps as essential process equipment for chlorination, pH adjustment, coagulant addition, and disinfection by-product control. The World Health Organization (WHO) estimates that over 2 billion people currently lack access to safely managed drinking water, driving public sector investment in water treatment across developing economies.

The U.S. Infrastructure Investment and Jobs Act allocated over US$ 55 billion to water infrastructure, and the EU’s Urban Wastewater Treatment Directive revision is compelling wastewater treatment upgrades across member states. Each new water treatment plant installation represents substantial chemical dosing pump procurement across multiple injection points, creating a durable and geographically expanding demand base for the market.

Restraints - High Initial Capital Cost and Maintenance Requirements

High-precision chemical injection pumps, particularly diaphragm metering pumps and high-pressure plunger systems for oil and gas applications, represent significant capital investments, with advanced systems from leading manufacturers ranging from US$ 5,000 to over US$ 100,000 per unit depending on pressure rating, flow range, and material specifications.

In developing markets and among smaller industrial operators, these upfront costs create procurement barriers. Additionally, maintaining chemical compatibility of wetted parts, preventing chemical crystallization in pump heads, and regular diaphragm and check valve maintenance add operational complexity and cost that can deter adoption among operators without dedicated maintenance staff.

Environmental and Safety Regulations on Chemical Handling

Chemical injection pump installations must comply with increasingly stringent environmental and chemical safety regulations including the EU’s REACH Regulation, U.S. EPA’s Risk Management Program (RMP), and OSHA’s Process Safety Management (PSM) standards for facilities handling hazardous chemicals.

Meeting these regulatory requirements adds design complexity, material selection constraints, and documentation burden to chemical injection pump system engineering and procurement. In certain applications involving highly toxic or corrosive chemicals, such as chlorine dosing or acid injection, containment and secondary containment requirements significantly increase total system cost, moderating adoption rates in price-sensitive markets.

Opportunities - Solar-Powered Chemical Injection Systems for Remote Oil & Gas and Agricultural Applications

The development of solar-driven chemical injection pump systems is creating a compelling market opportunity for remote oilfield, offshore, and agricultural applications where electrical grid power is unavailable or prohibitively expensive to supply. Remote well sites in North American shale plays, Middle East desert locations, and subsea tie-back applications are increasingly adopting solar-powered chemical injection skids that eliminate the need for shore power or diesel generator supply.

The declining cost of solar photovoltaic panels, with utility-scale solar costs falling over 90% in the past decade per BloombergNEF, has made solar-powered pumping economically viable at remote sites. Similarly, agricultural chemical injection for irrigation fertigation in remote farmland locations in India, Africa, and Latin America represents a large and underserved market for solar-powered metering pumps. Manufacturers developing certified, weather-resistant solar injection skid packages can command premium pricing in this specialized and growing application segment.

Smart Chemical Dosing Systems with IoT Connectivity and Remote Monitoring

The integration of IoT sensors, wireless connectivity, and cloud-based analytics platforms into chemical injection pump systems is creating a significant product innovation and premium revenue opportunity. Smart chemical dosing systems that automatically adjust injection rates based on real-time process parameter feedback, such as residual chlorine levels in water treatment or corrosion monitoring in oil pipelines, deliver superior process efficiency, chemical cost savings, and regulatory reporting capabilities versus conventional manual-adjustment systems.

The American Water Works Association (AWWA) and Water Environment Federation (WEF) have both highlighted smart chemical dosing as a priority technology for water utility modernization. Manufacturers including Grundfos Holding A/S’ SMART Digital™ dosing pump range and ProMinent GmbH’s Sigma® series are investing heavily in connected pump platforms, with subscription-based remote monitoring services creating recurring revenue streams beyond initial equipment sale.

Category-wise Analysis

By Product Type Insights

Diaphragm Pumps are the leading product type segment, commanding approximately 34% of total market share. Diaphragm metering pumps offer the most versatile and broadly applicable solution for chemical injection across water treatment, pharmaceutical, food processing, and chemical dosing applications where leak-free, contamination-free chemical containment and precise flow control are paramount.

The hermetically sealed diaphragm design eliminates shaft seal leakage, a critical requirement when handling corrosive, toxic, or sterile chemicals, while delivering repeatable metering accuracy of ±1% or better at rated conditions. ISO 15783 and API 675 standards specifically address controlled-volume metering pump performance requirements, formalizing diaphragm pump specifications across regulated industries. Leading manufacturers including Grundfos, Milton Roy, and ProMinent GmbH have built extensive diaphragm metering pump product lines that serve the full spectrum of dosing applications globally.

By Drive Type Insights

Electric-Driven pumps are the dominant drive type segment, representing approximately 56% of total market share. Electric-driven chemical injection pumps, powered by AC or DC motors with variable frequency drives, offer precise, electronically controllable flow rates, compatibility with process automation and SCADA systems, minimal maintenance versus engine-driven alternatives, and reliable operation across indoor and outdoor industrial environments with grid power access.

The proliferation of process automation in water treatment plants, chemical facilities, and pharmaceutical manufacturing has made electrically driven metering pumps the de facto standard for continuous-duty process injection applications. Modern electric metering pumps with integrated 4-20 mA or Modbus control interfaces can be directly integrated into plant DCS or SCADA systems, enabling centralized flow management that justifies their premium pricing versus pneumatic alternatives in most permanent installation scenarios.

By Application Insights

Water Treatment is the leading application segment, representing approximately 27% of total market share. Chemical dosing for water and wastewater treatment, encompassing chlorine disinfection, coagulant addition, pH adjustment, antiscalant dosing for membrane systems, and nutrient removal, represents the single largest and most geographically distributed application for chemical injection pumps globally.

Every municipal drinking water treatment plant, wastewater treatment facility, industrial water treatment system, and swimming pool treatment installation requires chemical dosing pumps as fundamental process components. The WHO’s drinking water quality guidelines and national drinking water standards (including U.S. EPA’s National Primary Drinking Water Regulations) mandate disinfectant residual maintenance that requires reliable chlorine or chloramine dosing equipment. Global investment in water infrastructure ensures this application segment retains market leadership throughout the forecast period.

By End-user Insights

Oil & Gas is the dominant end-use segment, accounting for approximately 31% of total market share. The oil and gas sector’s requirement for precise, high-pressure chemical injection across production, processing, and transportation operations makes it the highest-value and most demanding end-use market for chemical injection pumps.

Corrosion inhibitor injection at wellheads and along pipelines, scale inhibitor dosing in production separators, hydrate inhibitor injection in subsea flowlines, and biocide dosing in water injection systems collectively generate substantial chemical injection pump procurement across upstream, midstream, and downstream operations. According to the American Petroleum Institute (API), chemical treatment is a fundamental operating practice at virtually every oil and gas production facility globally, with chemical injection pump reliability directly linked to production uptime and asset integrity, supporting premium specification and procurement.

Regional Insights

North America Chemical Injection Pump Market Trends

North America is the largest regional market for chemical injection pumps, anchored by the United States’ world-leading oil and gas production, with the U.S. Energy Information Administration (EIA) reporting U.S. crude oil production exceeding 13 million barrels per day in 2023, and the country’s extensive water and wastewater treatment infrastructure. The shale revolution in the Permian Basin, Eagle Ford, and Bakken plays has driven sustained demand for wellhead chemical injection systems. U.S.-based manufacturers including Milton Roy, IDEX Corporation, Dover Corporation, and Pulsafeeder, Inc. serve both domestic and international markets.

The U.S. EPA’s Safe Drinking Water Act, Clean Water Act, and OSHA PSM standards create a stringent regulatory environment that mandates certified, precision-calibrated chemical dosing equipment across water utilities and chemical facilities. Canada’s oil sands operations in Alberta and offshore projects on the East Coast generate significant chemical injection demand, while Mexico’s energy sector reforms and PEMEX infrastructure investment contribute regional growth. The U.S. Infrastructure Investment and Jobs Act’s US$ 55 billion water infrastructure commitment is stimulating municipal water treatment plant upgrades requiring modern smart chemical dosing systems.

Europe Chemical Injection Pump Market Trends

Europe is a mature, technically sophisticated chemical injection pump market characterized by stringent environmental regulations, advanced chemical processing industries, and world-class pump manufacturers. Germany leads the European market, home to globally recognized chemical injection pump manufacturers including ProMinent GmbH, Lewa GmbH, and Lutz-Jesco GmbH. Germany’s world-class chemical industry, anchored by BASF, Bayer, Evonik, generates significant process chemical injection pump demand. The EU’s Water Framework Directive and Urban Wastewater Treatment Directive revision are compelling treatment infrastructure upgrades across member states.

The United Kingdom’s North Sea oil production operations generate ongoing chemical injection system demand for corrosion and scale control, while the UK’s water privatization model has driven substantial investment in treatment technology upgrades. France’s nuclear power and chemical sectors and Spain’s growing desalination and agricultural water treatment markets contribute regional demand. Grundfos Holding A/S, headquartered in Denmark, is among Europe’s most significant chemical dosing pump innovators, with its SMART Digital dosing range incorporating IoT connectivity and cloud-based monitoring capabilities that define the regional premium product standard.

Asia Pacific Chemical Injection Pump Market Trends

Asia Pacific is the fastest-growing regional market for chemical injection pumps, driven by expanding oil and gas production, massive water infrastructure investment, and the growth of chemical processing, pharmaceutical, and food manufacturing sectors across China, India, Japan, and ASEAN nations. China is the dominant regional market, with the government’s 14th Five-Year Plan prioritizing water pollution treatment and upgrading wastewater infrastructure across hundreds of cities. China’s chemical and pharmaceutical manufacturing sectors are also significant chemical dosing pump end-users, with domestic manufacturers including Seko Asia operations and local producers competing with international brands.

India represents the region’s most dynamic growth market, with the Jal Jeevan Mission targeting universal household tap water connections requiring chlorination dosing infrastructure, and the country’s pharmaceutical API manufacturing sector, the world’s largest by volume, generating substantial metering pump demand. ASEAN nations, particularly Indonesia, Vietnam, and Thailand, are expanding petrochemical, food processing, and water treatment infrastructure that drives growing chemical injection pump procurement. Japan’s advanced pharmaceutical, electronics, and specialty chemical industries sustain demand for ultra-precision micro-dosing pump systems from manufacturers including Nikkiso Co., Ltd.

Competitive Landscape

The global chemical injection pump market is moderately consolidated, featuring a blend of large diversified pump and fluid handling conglomerates and specialized metering pump manufacturers. Companies such as Grundfos Holding A/S, IDEX Corporation, Dover Corporation, and SPX FLOW hold significant market positions through broad product portfolios, global service networks, and certified compliance with API 675, ISO 15783, and industry-specific standards.

European specialist manufacturers including ProMinent GmbH and Lewa GmbH command premium positioning in pharmaceutical, chemical, and water treatment applications requiring high precision. Key competitive differentiators include dosing accuracy, chemical compatibility range, IoT connectivity, API certification, and service network coverage. Emerging business model trends include smart dosing-as-a-service subscriptions, remote monitoring platform access fees, and integrated chemical supply and dosing system bundles offered to water utilities and industrial customers.

Key Developments:

- February 2025: Grundfos Holding A/S launched the SMART Digital XL dosing pump series featuring enhanced IoT connectivity, cloud-based analytics integration, and extended chemical compatibility range targeting large-scale water treatment and industrial chemical dosing applications globally.

- September 2024: ProMinent GmbH introduced an updated Sigma® X series of smart metering pumps with integrated Bluetooth Low Energy connectivity, enabling wireless configuration, monitoring, and diagnostics for pharmaceutical, water treatment, and chemical processing installations.

- April 2024: Milton Roy expanded its chemical injection pump product range for offshore oil and gas applications with a new subsea-rated diaphragm metering pump series certified for deepwater deployment, targeting North Sea and Gulf of Mexico subsea production system operators.

Companies Covered in Chemical Injection Pump Market

- Grundfos Holding A/S

- Milton Roy

- ProMinent GmbH

- SEKO S.p.A.

- SPX FLOW, Inc.

- Lewa GmbH

- IDEX Corporation

- Dover Corporation

- Injection Pumps, Inc.

- Petronash

- Pulsafeeder, Inc.

- Lutz-Jesco GmbH

- Blue-White Industries

- Verder Group

- Nikkiso Co., Ltd.

- Sera GmbH

- OBL S.r.l.

- SAMES KREMLIN

Frequently Asked Questions

The global Chemical Injection Pump Market is projected to reach US$ 73.9 Billion by 2033, expanding from US$ 45.7 Billion in 2026 at a CAGR of 7.1% during the 2026-2033 forecast period.

The primary drivers are IEA-documented global upstream oil and gas investment exceeding US$ 570 billion annually requiring wellhead and pipeline chemical injection systems, and WHO-identified water scarcity affecting 2+ billion people driving unprecedented water treatment infrastructure investment globally, where chemical dosing pumps are fundamental process components for disinfection, coagulation, and pH control.

Diaphragm Pumps lead the By Product Type category with approximately 34% market share. Their hermetically sealed, leak-free design, ±1% metering accuracy, and compliance with API 675 and ISO 15783 standards for controlled-volume metering pumps make them the preferred solution across water treatment, pharmaceutical, and chemical process injection applications globally.

North America leads the global Chemical Injection Pump Market, driven by U.S. crude oil production exceeding 13 million barrels per day requiring extensive wellhead chemical injection, EPA Safe Drinking Water Act compliance mandating certified chemical dosing systems, and the presence of major manufacturers including Milton Roy, IDEX Corporation, Dover Corporation, and Pulsafeeder Inc.

The highest-value opportunities are solar-powered chemical injection systems for remote oilfield and agricultural applications, enabled by 90%+ solar cost reduction, and smart IoT-connected dosing platforms endorsed by AWWA and WEF for water utility modernization, where Grundfos and ProMinent are pioneering subscription-based remote monitoring services generating recurring revenue beyond equipment sales.

The key market participants include Grundfos Holding A/S, Milton Roy, ProMinent GmbH, SEKO S.p.A., SPX FLOW Inc., Lewa GmbH, IDEX Corporation, Dover Corporation, Injection Pumps Inc., Petronash, Pulsafeeder Inc., Lutz-Jesco GmbH, Blue-White Industries, Verder Group, and Nikkiso Co., Ltd., spanning oil and gas, water treatment, pharmaceutical, and industrial chemical dosing applications globally.