- Chemicals and Materials

- Copper Alloys for Connector Market

Copper Alloys for Connector Market Size, Share, and Growth Forecast, 2026 - 2033

Copper Alloys for Connector Market by Alloy Type (High-Conductivity Copper Alloys, Copper-Nickel-Silicon Alloys, Others), Application (Telecommunications & Data Centers, Consumer Electronics, Others), Connector Type, and Regional Analysis for 2026 - 2033

Copper Alloys for Connector Market Size and Trends Analysis

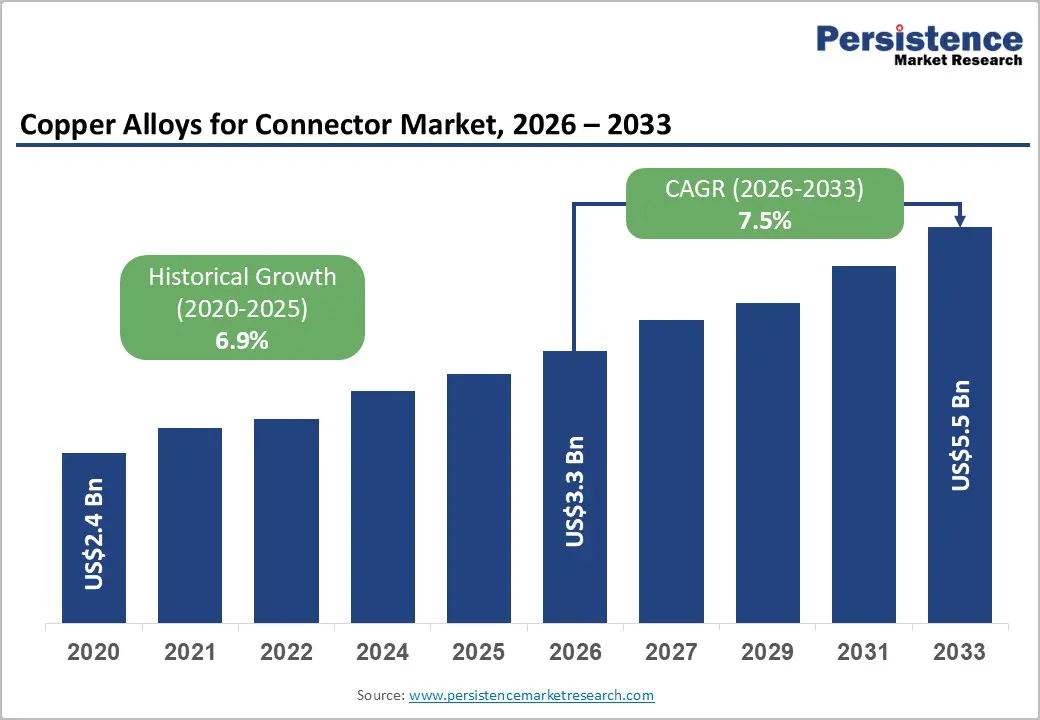

The global copper alloys for connector market size is likely to be valued at US$3.3 billion in 2026 and is expected to reach US$5.5 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033, driven by increasing demand for high-performance electrical connectivity solutions across telecommunications, automotive, industrial automation, medical equipment, and consumer electronics sectors. Copper alloys remain indispensable in connector manufacturing due to their unique combination of high electrical conductivity, mechanical strength, corrosion resistance, thermal stability, and formability. The accelerating deployment of data centers, 5G infrastructure, electric vehicles (EVs), and advanced electronic devices is increasing demand for connector materials capable of maintaining reliable electrical performance under challenging operating conditions.

Key Industry Highlights:

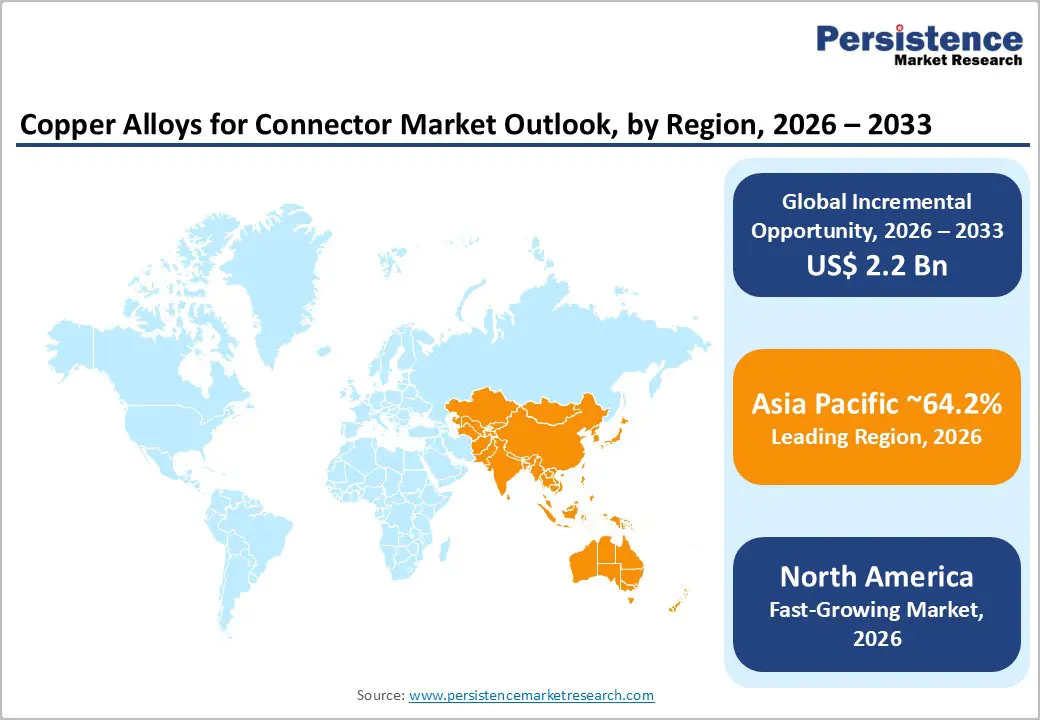

- Leading Region: Asia Pacific is expected to account for approximately 64.2% of the market share in 2026, supported by its dominance in electronics manufacturing, EV production, telecommunications equipment, and industrial automation.

- Fastest-growing Region: North America is anticipated to register the highest growth rate during the forecast period, driven by investments in AI data centers, cloud infrastructure, semiconductor manufacturing, EV production, and advanced telecommunications networks.

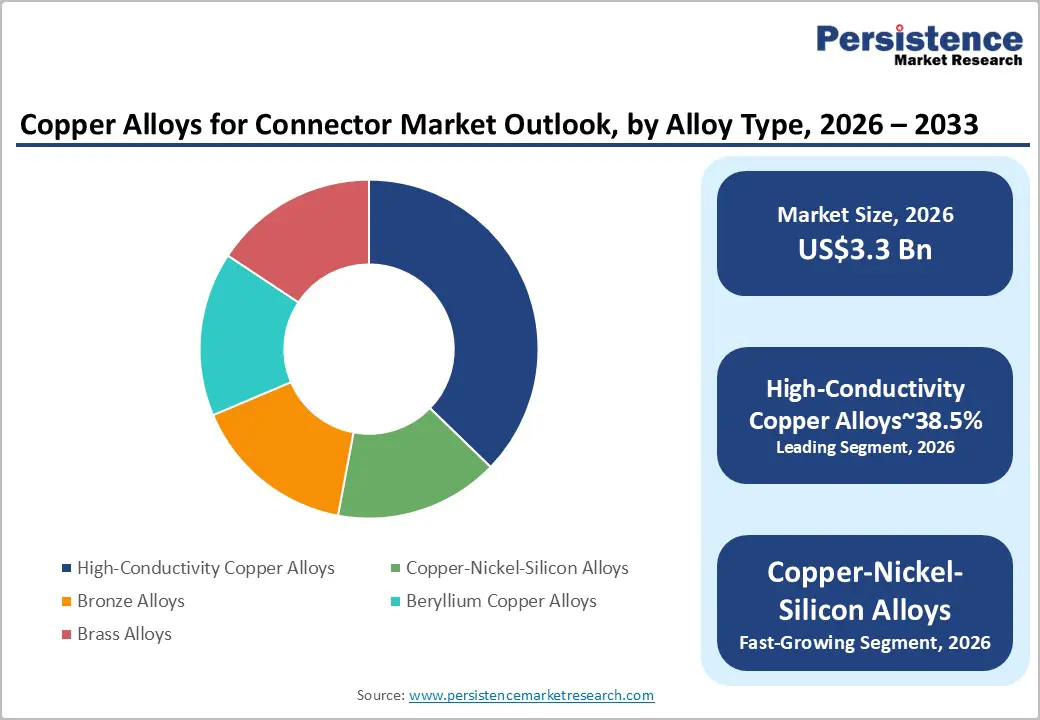

- Dominant Alloy Type: High-conductivity copper alloys are anticipated to account for approximately 38.5% of market revenue in 2026, owing to extensive usage in telecommunications equipment, data centers, consumer electronics, and automotive electrical systems.

- Leading Application: Telecommunications & data centers are anticipated to hold approximately 31.4% of market revenue in 2026, supported by increasing cloud computing adoption, AI infrastructure deployment, rising internet traffic, and continued expansion of global 5G networks.

DRO Analysis

Driver - Expansion of Digital Infrastructure and Data Traffic

The rapid growth of global data consumption is creating substantial demand for advanced connector materials. The expansion of hyperscale data centers, cloud computing facilities, artificial intelligence platforms, and 5G telecommunications networks requires high-performance electrical connectors capable of handling increased power densities and faster data transmission speeds.

Data centers are becoming increasingly energy-intensive as organizations deploy AI-driven computing infrastructure. Higher server densities and advanced networking architectures require connectors with superior thermal and electrical performance. Copper alloys provide the conductivity and reliability necessary for power distribution units, storage systems, network switches, routers, and high-speed interconnects.

The continued rollout of 5G infrastructure and edge computing facilities is further increasing demand for connector components. As telecommunications operators expand network capacity and improve transmission speeds, manufacturers are adopting advanced copper alloys to ensure long-term signal integrity, durability, and reliability.

Electrification of Transportation Systems

The global transition toward electric mobility represents one of the most significant growth drivers for the copper alloys for the connector market. Electric vehicles contain substantially more electrical and electronic components than conventional internal combustion engine vehicles, requiring a larger number of connectors and terminals throughout the vehicle architecture.

Battery packs, charging systems, power electronics, electric motors, inverters, and advanced driver assistance systems rely on highly reliable electrical connections. Copper alloys such as beryllium copper and copper-nickel-silicon alloys are increasingly used because they offer excellent conductivity, fatigue resistance, and stress-relaxation performance under elevated temperatures.

As automotive manufacturers increase EV production volumes and develop next-generation vehicle platforms, demand for high-performance connector materials is expected to rise significantly. This trend is creating long-term growth opportunities for suppliers capable of delivering advanced copper alloy solutions that meet stringent automotive qualification requirements.

Restraint - Raw Material Price Volatility and Regulatory Compliance Requirements

Despite favorable demand fundamentals, the market faces challenges associated with fluctuations in raw material prices. Copper, nickel, and specialty alloying elements are subject to global commodity market volatility, creating uncertainty for manufacturers and impacting production costs.

Regulatory compliance requirements present an additional challenge. Environmental regulations governing hazardous substances in electronic products continue to evolve, requiring manufacturers to reformulate products and qualify alternative alloy compositions. Restrictions on certain materials have increased development costs and extended qualification timelines.

Furthermore, the emergence of alternative conductive materials, including aluminum-based alloys and advanced conductive polymers, creates competitive pressure in specific applications. Although copper alloys continue to dominate high-performance connector applications, manufacturers must continually invest in innovation to maintain their competitive position.

Opportunities - Development of Lead-Free and Sustainable Alloy Solutions

Growing emphasis on sustainability and environmental compliance is creating opportunities for next-generation copper alloy materials. Connector manufacturers increasingly seek lead-free and environmentally compliant alloys that maintain high conductivity while satisfying evolving regulatory requirements.

Advanced copper-nickel-tin, copper-zirconium, and specialty copper alloy formulations are gaining adoption across telecommunications, automotive, aerospace, and industrial applications. These materials provide improved mechanical performance and corrosion resistance while supporting sustainability objectives.

Manufacturers capable of developing environmentally compliant materials without compromising performance are expected to benefit from higher-value contracts and stronger long-term customer relationships.

Manufacturing Expansion across Asia Pacific

Asia Pacific continues to serve as the global manufacturing hub for electronics, telecommunications equipment, automotive components, and industrial systems. Ongoing investments in semiconductor production, electronics assembly, EV manufacturing, and telecommunications infrastructure are driving demand for connector-grade copper alloys.

Government initiatives supporting domestic manufacturing, supply chain localization, and advanced technology development are creating favorable market conditions. Rising production of smartphones, consumer electronics, industrial automation equipment, and EVs is increasing demand for copper alloy strips, terminals, contacts, and connector components.

Companies that align production capabilities with regional manufacturing ecosystems and local sourcing requirements are expected to gain significant competitive advantages during the forecast period.

Category-wise Analysis

Alloy Type Insights

High-conductivity copper alloys are anticipated to account for approximately 38.5% of market share in 2026, maintaining their position as the largest alloy category. Their leadership is driven by extensive use in telecommunications infrastructure, hyperscale data centers, consumer electronics, and automotive electrical systems where low resistance and high current-carrying capacity are essential. Examples include connector terminals used in server racks, 5G base stations, USB-C interfaces, and vehicle power distribution modules. Their combination of excellent conductivity, corrosion resistance, and manufacturability continues to support widespread adoption across high-volume connector applications.

Copper-nickel-silicon (CuNiSi) alloys are expected to register the fastest CAGR during the forecast period due to their superior strength, thermal stability, and stress-relaxation resistance. These alloys are increasingly utilized in EV battery connectors, high-speed telecom connectors, industrial automation systems, and aerospace electronic assemblies where elevated temperatures and continuous mechanical stress are common. As manufacturers pursue connector miniaturization and higher power densities, CuNiSi alloys are gaining preference over conventional materials, supporting their rapid market expansion.

Application Insights

Telecommunications & data centers are anticipated to account for approximately 31.4% of the market share in 2026, making them the largest application segment. Growth is fueled by expanding cloud computing infrastructure, AI workloads, 5G network deployment, and rising global data traffic. Copper alloy connectors are widely used in servers, switches, routers, optical transceivers, and power distribution units where signal integrity and reliability are critical. The increasing construction of hyperscale data centers worldwide continues to reinforce demand for high-performance connector materials.

Consumer electronics is projected to be the fastest-growing application segment throughout the forecast period. Rising demand for smartphones, tablets, smartwatches, wireless earbuds, and smart home devices is increasing the need for compact, high-performance connectors. Copper alloys are commonly used in charging ports, board-to-board connectors, battery terminals, and wearable device interconnects. As devices become smaller, more powerful, and feature-rich, manufacturers are increasingly adopting advanced copper alloy materials that deliver superior conductivity, durability, and miniaturization capabilities.

Regional Insights

North America Copper Alloys for Connector Market Trends

North America is anticipated to be the fastest-growing regional market during the forecast period, supported by substantial investments in artificial intelligence infrastructure, cloud computing facilities, electric vehicle manufacturing, telecommunications networks, and industrial automation. The region benefits from a highly developed innovation ecosystem comprising advanced connector manufacturers, specialty alloy suppliers, semiconductor companies, and research institutions. Growing demand for high-speed connectivity, data processing capabilities, and vehicle electrification continues to drive consumption of copper alloy connectors across multiple industries.

U.S. Copper Alloys for Connector Market Trends

The U.S. represents the largest market within North America and serves as the primary growth engine for the region. Expanding investments in hyperscale data centers, AI computing infrastructure, EV charging networks, aerospace systems, and advanced manufacturing facilities are increasing demand for high-performance connectors. Federal initiatives supporting semiconductor production, grid modernization, and domestic manufacturing are further strengthening the market outlook. The presence of major connector manufacturers and technology companies continues to support innovation and adoption of advanced copper alloy materials.

Canada Copper Alloys for Connector Market Trends

Canada is witnessing a steady growth due to increasing investments in telecommunications infrastructure, renewable energy projects, EV supply chains, and industrial automation. The country's strong mining and metals sector also supports the availability of raw materials required for copper alloy production. Growing deployment of 5G networks and smart-grid technologies is expected to contribute to future demand for high-reliability connector solutions.

Europe Copper Alloys for Connector Market Trends

Europe remains a significant market characterized by advanced engineering capabilities, strict regulatory standards, and strong automotive and industrial manufacturing sectors. The region's focus on sustainability, electrification, renewable energy deployment, and industrial digitalization is driving demand for high-performance connector materials. Manufacturers increasingly prioritize lead-free, recyclable, and low-carbon copper alloy solutions to comply with evolving environmental regulations.

Germany Copper Alloys for Connector Market Trends

Germany represents the largest market in Europe due to its leadership in automotive manufacturing, industrial automation, machinery production, and electrical engineering. The country's transition toward electric mobility and Industry 4.0 technologies continues to generate strong demand for advanced connector systems. German manufacturers remain at the forefront of adopting high-performance copper alloy materials for automotive and industrial applications.

U.K. Copper Alloys for Connector Market Trends

The U.K. is benefiting from investments in telecommunications infrastructure, aerospace technologies, defense electronics, and renewable energy projects. Continued expansion of data centers and digital infrastructure is increasing demand for specialized connectors capable of supporting high-speed data transmission and reliable power distribution.

France Copper Alloys for Connector Market Trends

France maintains a strong position in aerospace, defense, transportation, and energy sectors. Investments in electrification technologies, smart manufacturing, and digital transformation initiatives are supporting demand for copper alloy connectors. The country's emphasis on sustainable industrial development is also encouraging the adoption of environmentally compliant materials.

Spain Copper Alloys for Connector Market Trends

Spain is emerging as an important market supported by growth in renewable energy installations, EV manufacturing investments, and industrial modernization programs. Expanding solar and wind energy projects require reliable electrical connectivity solutions, creating opportunities for advanced copper alloy connector suppliers.

Asia Pacific Copper Alloys for Connector Market Trends

Asia Pacific accounted for approximately 64.2% of the market share in 2026, making it the dominant regional market. The region benefits from extensive electronics manufacturing capacity, strong automotive production volumes, rapidly expanding telecommunications networks, and growing investments in industrial automation. Favorable government policies, cost-efficient manufacturing ecosystems, and expanding consumer electronics production continue to support market growth.

China Copper Alloys for Connector Market Trends

China represents the largest market globally and serves as the center of electronics manufacturing, telecommunications equipment production, EV manufacturing, and industrial machinery development. The country's extensive supply chain infrastructure and large-scale manufacturing capabilities generate substantial demand for connector-grade copper alloys. Continued investments in semiconductor manufacturing, artificial intelligence infrastructure, and electric mobility are expected to reinforce market growth.

Japan Copper Alloys for Connector Market Trends

Japan plays a critical role through its leadership in advanced materials development and precision manufacturing. The country's expertise in high-performance copper alloys, automotive electronics, semiconductors, and industrial automation supports demand for specialized connector materials. Japanese manufacturers continue to develop innovative alloy technologies for high-reliability applications.

India Copper Alloys for Connector Market Trends

India is emerging as one of the fastest-growing markets in the region due to expanding electronics manufacturing, telecommunications infrastructure deployment, and government-backed industrial development programs. Rapid 5G rollout, increasing smartphone production, and growing EV adoption are driving demand for advanced connector materials. Production-linked incentive programs and semiconductor investments are expected to further strengthen domestic demand.

Competitive Landscape

The global copper alloys for connector market is moderately fragmented, with competition occurring across both materials manufacturing and connector production segments. Leading participants compete through alloy innovation, manufacturing scale, application expertise, and long-term customer relationships.

Leading companies are prioritizing materials innovation, acquisition-led growth, manufacturing expansion, sustainability initiatives, and strategic partnerships. Key competitive differentiators include high-conductivity alloy development, regulatory compliance expertise, advanced manufacturing capabilities, and close collaboration with OEMs during product development and qualification processes.

Key Industry Developments:

- In May 2025, KME Group launched the KupferDigital 2 initiative to develop a digital twin for copper-processing operations.

- In August 2025, CommScope announced the divestiture of its Connectivity and Cable Solutions business to Amphenol as part of a strategic portfolio transformation.

Companies Covered in Copper Alloys for Connector Market

- Amphenol Corporation

- TE Connectivity Ltd.

- Molex LLC

- Yazaki Corporation

- Aptiv PLC

- Materion Corporation

- Proterial, Ltd.

- Mitsubishi Materials Corporation

- NGK Insulators, Ltd.

- Wieland Group

- KME Group S.p.A.

- Lebronze Alloys Group

- AMPCO METAL S.A.

- Diehl Metall Stiftung & Co. KG

- Aurubis AG

- Wieland Rolled Products North America, LLC

Frequently Asked Questions

The global copper alloys for connector market is estimated to be valued at US$3.3 billion in 2026.

The copper alloys for connector market is expected to reach US$5.5 billion by 2033.

Key trends shaping the market include growing adoption of high-performance copper alloys in EV connectors, and expansion of AI-driven data centers and cloud infrastructure.

High-conductivity copper alloys are the leading alloy type segment, anticipated to account for approximately 38.5% of market revenue, owing to their extensive use in telecommunications equipment, data centers, consumer electronics, and automotive electrical systems.

The copper alloys for connector market is projected to grow at a CAGR of 7.5% between 2026 and 2033.

Major companies include Amphenol Corporation, TE Connectivity, Molex LLC, Materion Corporation, and Yazaki Corporation.