- Automotive Components & Materials

- Friction Material Market

Friction Material Market Size, Share, and Growth Forecast, 2026 - 2033

Friction Material Market by Material Type (Semi-Metallic Friction Materials, Ceramic Friction Materials, Others), Product Type (Brake Pads, Brake Linings, Others), End-user Industry, and Regional Analysis for 2026 - 2033

Friction Material Market Size and Trends Analysis

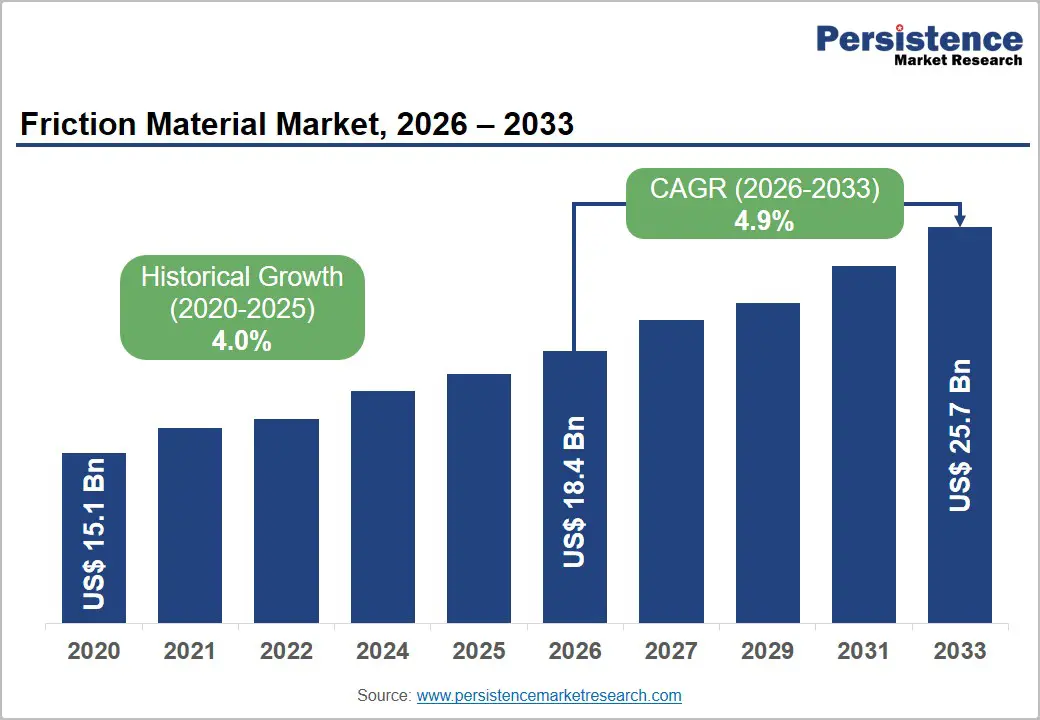

The global friction material market size is likely to be valued at US$18.4 billion in 2026 and is expected to reach US$25.7 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033, driven by replacement demand and continuous advancements in braking technologies.

Growth is supported by rising vehicle production, expanding electric vehicle adoption, tightening regulations on brake particulate emissions, and increasing investment in railway and industrial transportation infrastructure. The industry is also witnessing a gradual shift toward advanced ceramic and low-emission friction materials to meet evolving performance and environmental requirements.

Key Industry Highlights:

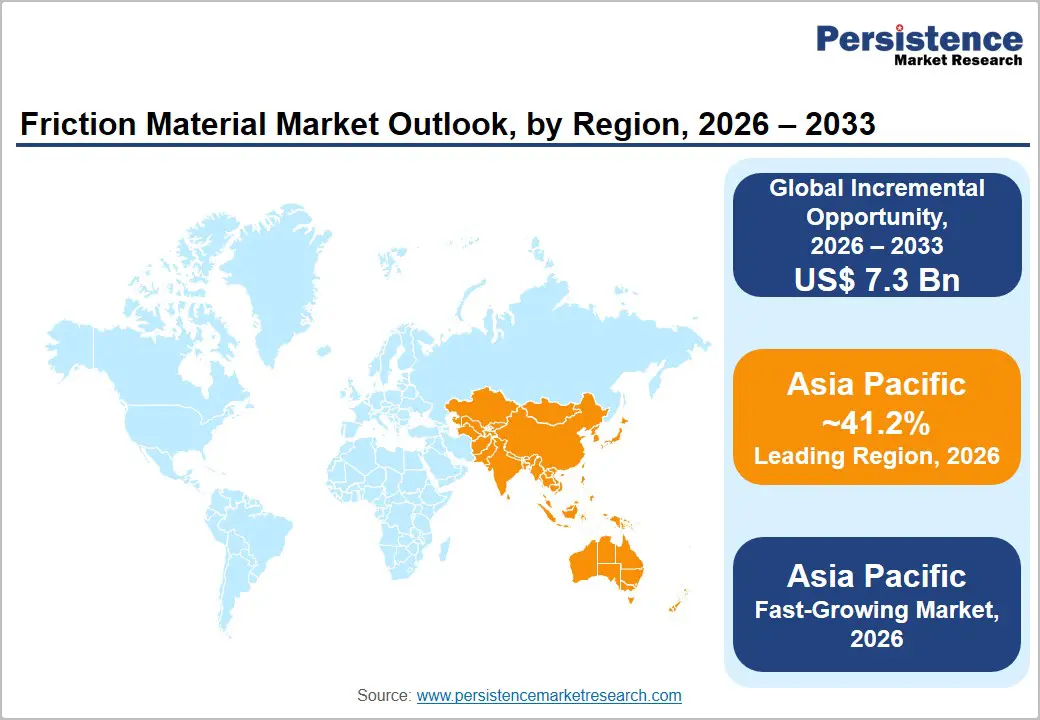

- Leading Region: Asia Pacific is anticipated to account for 41.2% of the market share in 2026, supported by strong automotive production, expanding EV adoption, and large-scale railway infrastructure investments across China, Japan, and India.

- Fastest-growing Region: Asia Pacific is expected to register the highest growth rate during the forecast period, driven by rapid industrialization, increasing vehicle ownership, railway modernization projects, and rising demand for advanced friction materials in emerging economies.

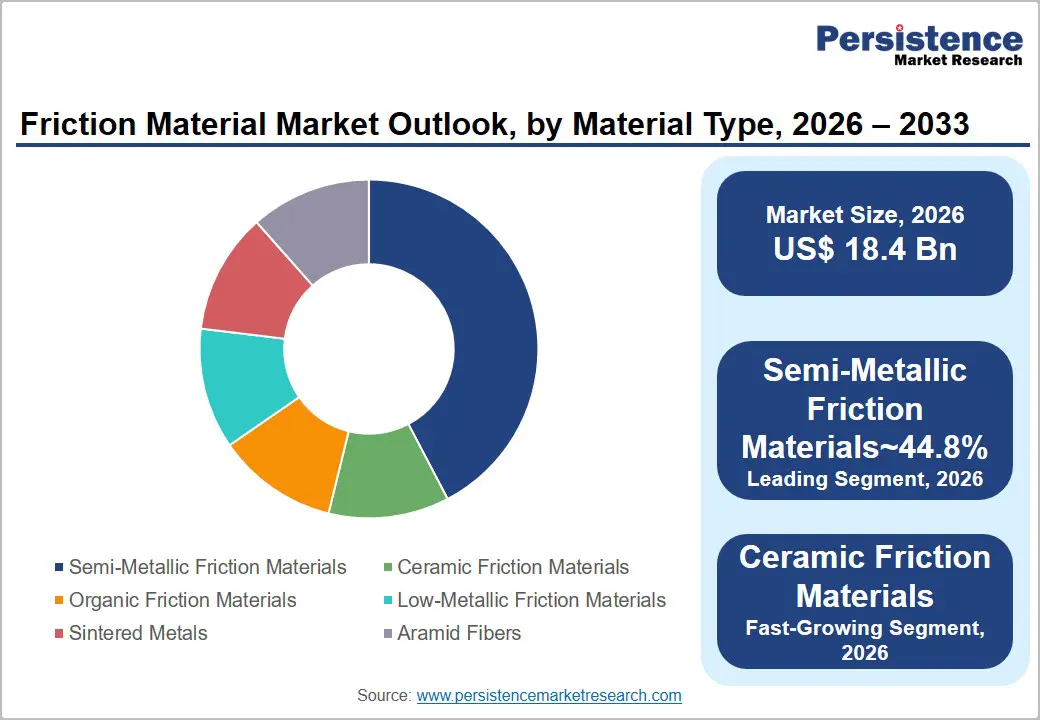

- Dominant Material Type: Semi-metallic friction materials are anticipated to hold approximately 44.8% of the market share in 2026, owing to their superior durability, thermal conductivity, cost-effectiveness, and widespread use in passenger and commercial vehicles.

- Leading Product Type: Brake pads are expected to account for approximately 51.7% of the market share in 2026, driven by their extensive adoption in passenger vehicles, recurring replacement demand, and continuous advancements in low-noise and low-dust braking technologies.

DRO Analysis

Drivers - Growing Vehicle Electrification Driving Advanced Friction Material Demand

The rapid expansion of electric vehicle (EV) adoption is transforming friction material requirements rather than reducing market demand. Although EVs utilize regenerative braking systems, conventional friction brakes remain essential for vehicle safety, emergency stopping, and low-speed operations. The increasing penetration of EVs has accelerated demand for friction materials that offer lower dust emissions, reduced noise, enhanced durability, and superior thermal stability.

Manufacturers are investing heavily in ceramic-based and hybrid friction formulations designed specifically for EV platforms. These materials help maintain braking efficiency while minimizing particulate emissions generated during braking. The growing global vehicle fleet, coupled with rising EV production, continues to support OEM and aftermarket demand for high-performance friction materials. As automotive manufacturers prioritize sustainability and compliance with emerging environmental regulations, friction material suppliers are expected to benefit from long-term product replacement cycles and increased research and development spending.

Stricter Brake Emission Regulations Accelerating Product Innovation

Governments and regulatory authorities are increasingly focusing on non-exhaust vehicle emissions, particularly particulate matter generated by braking systems. New regulatory frameworks targeting brake dust emissions are encouraging manufacturers to redesign friction materials with lower environmental impact while maintaining safety and performance standards.

These regulations are driving the development of advanced ceramic, organic, and low-metallic friction materials that generate fewer airborne particles. Compliance requirements have elevated the importance of testing, validation, and material engineering capabilities among suppliers. Automotive OEMs are increasingly seeking friction material partners capable of meeting evolving environmental standards across multiple regions. This regulatory transition is creating opportunities for technologically advanced manufacturers while simultaneously increasing barriers to entry for smaller suppliers lacking sufficient research, testing, and certification resources.

Restraint - Raw Material Price Volatility and Rising Compliance Costs

The friction material industry relies on a wide range of raw materials, including metal powders, resins, fibers, ceramics, and specialty additives. Fluctuations in commodity prices directly affect manufacturing costs and profit margins throughout the supply chain. Price volatility in metals such as copper, aluminum, and steel can significantly impact production economics, particularly for semi-metallic friction materials.

Suppliers also face increasing compliance costs associated with product testing, certification, and environmental regulations. Meeting evolving brake emission standards requires substantial investment in material reformulation, laboratory validation, and performance testing. These additional expenditures create financial pressure on manufacturers, particularly small and medium-sized companies. The combination of volatile input costs and growing regulatory obligations remains a key challenge for industry participants seeking to maintain profitability while remaining competitive.

Opportunity - Expansion of Ceramic and Low-Emission Friction Materials

Rising consumer preference for low-noise, low-dust braking systems is creating strong demand for ceramic formulations across passenger vehicles and electric mobility platforms. Premium vehicle manufacturers increasingly favor ceramic friction materials because they provide improved braking consistency, reduced wear, and enhanced thermal performance. The trend toward sustainable transportation further strengthens market opportunities as regulators focus on reducing particulate emissions from braking systems. Manufacturers capable of delivering certified low-emission products are expected to gain competitive advantages in both OEM and aftermarket channels.

Railway Infrastructure Investments Creating New Growth Avenues

Growing investment in railway modernization and transportation infrastructure is creating significant opportunities for friction material suppliers. Railway applications require specialized brake linings, discs, and friction systems capable of operating under demanding conditions while maintaining high safety standards. Urban transit expansion, high-speed rail projects, freight network upgrades, and railway electrification initiatives are contributing to rising demand for advanced braking solutions. Suppliers with expertise in rail-certified friction materials are expected to benefit from long product qualification cycles, stable aftermarket demand, and high technical barriers to entry.

Category-wise Analysis

Material Type Insights

Semi-metallic friction materials are anticipated to account for approximately 44.8% of the market share in 2026, making them the leading material category. Their dominance is supported by a strong balance of durability, heat dissipation, braking efficiency, and cost-effectiveness. These materials are widely used in passenger vehicles, light commercial vehicles, heavy-duty trucks, and buses, particularly in models produced by major automotive manufacturers such as Ford, Toyota, and General Motors. Strong OEM adoption and a large replacement market continue to support segment growth, especially in emerging economies where vehicle ownership and freight transportation activities are expanding.

Ceramic friction materials are projected to register the fastest growth at a CAGR of 6.8% during the forecast period. The segment is benefiting from rising electric vehicle production, stricter brake-emission standards, and increasing consumer preference for quieter and cleaner braking systems. Ceramic brake pads are increasingly used in premium and electric vehicle models from manufacturers such as Tesla, BMW, and Mercedes-Benz due to their lower dust generation, reduced noise, and longer service life. Growing adoption in both OEM and aftermarket channels is expected to strengthen the segment's market position.

Product Type Insights

Brake pads are anticipated to capture approximately 51.7% of the market share in 2026, making them the dominant product segment. Their leadership is driven by extensive use of disc braking systems across passenger cars, SUVs, and light commercial vehicles. Regular wear and replacement requirements generate consistent aftermarket demand, while OEM production volumes continue to support growth. Manufacturers are increasingly introducing low-noise and low-dust brake pad technologies for modern vehicles, including electric and hybrid models, further reinforcing the segment’s market leadership.

Brake linings are expected to expand at a CAGR of 5.9%, making them the fastest-growing product category. Growth is primarily driven by rising demand from railway systems, commercial trucks, buses, and industrial equipment. For example, high-speed rail networks in China and Europe, along with expanding freight rail infrastructure in North America and India, are increasing the need for durable braking components. Their longer operating life and ability to perform under heavy-load conditions make brake linings a preferred solution in transportation and industrial applications.

Regional Insights

North America Friction Material Market Trends

North America remains a significant market for friction materials, supported by a mature automotive industry, a large vehicle parc, and a well-established aftermarket ecosystem. Rising electric vehicle adoption, investments in railway modernization, and increasing demand for high-performance braking systems continue to support market expansion. The region also benefits from strong research and development capabilities, advanced manufacturing infrastructure, and stringent vehicle safety standards.

U.S. Friction Material Market Trends

The U.S. represents the largest friction material market in North America, accounting for the majority of regional demand. Growth is supported by extensive passenger vehicle ownership, a large commercial vehicle fleet, and strong aftermarket replacement demand. Increasing adoption of electric vehicles is driving demand for low-noise and low-emission friction materials, while ongoing investments in freight rail and public transportation infrastructure are creating opportunities for advanced brake linings and railway braking components.

Canada Friction Material Market Trends

Canada contributes significantly to regional growth through its automotive manufacturing activities and expanding transportation sector. Demand for friction materials is supported by commercial vehicle operations, railway freight transportation, and increasing vehicle maintenance expenditures. The country's focus on sustainable mobility and transportation modernization is expected to encourage adoption of advanced friction technologies.

Europe Friction Material Market Trends

Europe is one of the most technologically advanced friction material markets, characterized by stringent environmental regulations, strong automotive production capabilities, and growing electric vehicle adoption. Regulatory measures targeting brake particulate emissions are accelerating innovation in ceramic, organic, and low-emission friction materials. The region also benefits from a strong presence of leading braking system manufacturers and extensive research capabilities.

Germany Friction Material Market Trends

Germany is the largest friction material market in Europe, supported by its position as a global automotive manufacturing and engineering hub. The country's premium vehicle manufacturers continue to invest in advanced braking technologies, creating strong demand for high-performance friction materials. Growth is further supported by increasing EV production and ongoing investments in sustainable mobility solutions.

U.K. Friction Material Market Trends

The U.K. remains a key market due to its established automotive aftermarket and growing electric vehicle sector. Demand for friction materials is driven by replacement cycles, vehicle maintenance requirements, and increasing adoption of advanced braking systems. Regulatory emphasis on environmental performance is encouraging manufacturers to introduce low-dust and low-emission products.

France Friction Material Market Trends

France benefits from a strong automotive sector and government initiatives promoting low-emission transportation. Rising EV adoption and investments in railway modernization projects are contributing to demand for advanced friction materials. The country's focus on sustainable transportation is expected to support long-term market growth.

Asia Pacific Friction Material Market Trends

Asia Pacific is anticipated to account for 41.2% of the market share in 2026, making it both the largest and fastest-growing regional market. Rapid industrialization, expanding vehicle production, rising vehicle ownership, and large-scale railway infrastructure investments continue to drive demand. The region's strong manufacturing base and growing electric vehicle ecosystem position it as the primary growth engine for the global market.

China Friction Material Market Trends

China is expected to dominate the Asia Pacific market, accounting for approximately 49% of regional demand in 2026. As the world's largest automotive manufacturing hub and electric vehicle market, China generates substantial demand for brake pads, brake linings, and advanced friction materials. Government support for EV adoption, strong domestic vehicle production, and extensive railway expansion projects continue to strengthen market growth. Local manufacturers are also investing heavily in ceramic and low-emission friction technologies to support export opportunities.

Japan Friction Material Market Trends

Japan is expected to account for approximately 19% of the regional market in 2026, supported by its technologically advanced automotive industry and strong expertise in braking systems. Japanese manufacturers continue to develop high-performance friction materials focused on durability, safety, and environmental compliance. Demand remains strong from both domestic vehicle production and export-oriented automotive manufacturing.

India Friction Material Market Trends

India is expected to contribute approximately 15% of Asia Pacific demand in 2026 and is emerging as one of the fastest-growing country markets. Rising passenger vehicle sales, expanding two-wheeler production, increasing commercial vehicle demand, and growing investments in transportation infrastructure are supporting market expansion. The government's focus on domestic manufacturing and road safety improvements is expected to further stimulate demand for friction materials.

Competitive Landscape

The global friction material market exhibits a moderately fragmented competitive structure characterized by the presence of multinational manufacturers, regional specialists, and niche application providers. Leading companies maintain strong positions through advanced material engineering capabilities, extensive OEM relationships, broad product portfolios, and established aftermarket distribution networks.

Leading companies are focusing on advanced material innovation, regional manufacturing expansion, strategic partnerships, and environmental compliance. Investments in ceramic friction technologies, low-emission braking solutions, and localized production facilities remain central to competitive strategies. Manufacturers are also strengthening OEM collaborations and aftermarket distribution networks to enhance market penetration and long-term revenue stability.

Key Industry Developments:

- In October 2025, Akebono Brake Corporation expanded its ProACT and EURO product portfolios with seven new ultra-premium ceramic disc brake pad part numbers.

- In May 2025, Akebono Brake Corporation introduced new Ultra-Premium Disc Brake Pad offerings across its ProACT, EURO, and Severe Duty product lines.

Companies Covered in Friction Material Market

- Brembo S.p.A.

- Knorr-Bremse AG

- TMD Friction Group GmbH

- Nisshinbo Brake Inc.

- Akebono Brake Industry Co., Ltd.

- ADVICS Co., Ltd.

- Fras-le S.A.

- Brakes India Private Limited

- MAT Holdings, Inc.

- Sangsin Brake Co., Ltd.

- Miba AG

- Federal-Mogul Motorparts (Ferodo)

- ITT Inc. (Wolverine Advanced Materials)

- AISIN Corporation

- HL Mando Corporation

- Continental AG (ATE Brake Systems)

Frequently Asked Questions

The global friction material market is estimated to be valued at US$18.4 billion in 2026.

The friction material market is expected to reach US$25.7 billion by 2033.

Key trends include the increasing adoption of ceramic friction materials, growing demand for low-dust and low-noise braking systems, expansion of electric vehicle production, stricter regulations on brake particulate emissions, and rising investments in railway infrastructure and transportation modernization.

Semi-metallic friction materials lead the market and are anticipated to account for approximately 44.8% of the market share, owing to their durability, thermal stability, and cost-effectiveness across automotive and commercial vehicle applications.

The friction material market is projected to grow at a CAGR of 4.9% between 2026 and 2033.

Major companies include Brembo S.p.A., Knorr-Bremse AG, TMD Friction Group, Nisshinbo Holdings Inc., and Akebono Brake Industry Co., Ltd.