- Automation & Robotics

- Coordinate Measuring Machines Market

Coordinate Measuring Machines Market Size, Share, and Growth Forecast 2026 - 2033

Coordinate Measuring Machines Market by Product Type (Fixed, Bridge, Cantilever, Gantry), by Industry (Automotive, Electronics, Energy & Power, Medical), by Application (Reverse Engineering, Virtual Simulation, Quality Control), by Regional Analysis, 2026 - 2033

Coordinate Measuring Machines Market Size and Trend Analysis

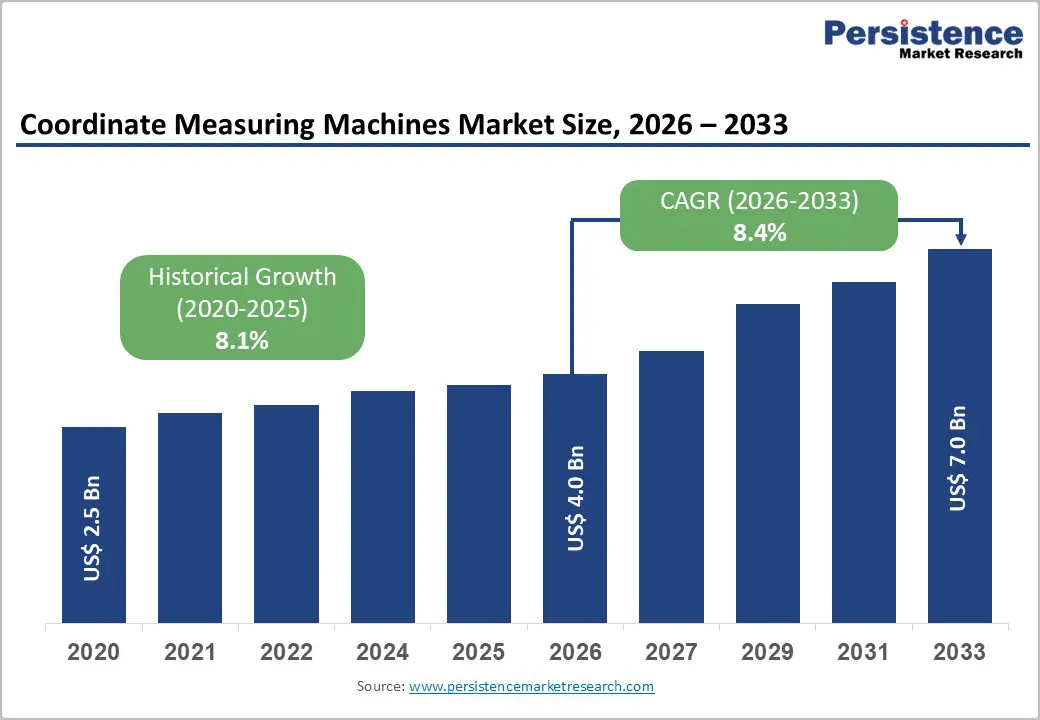

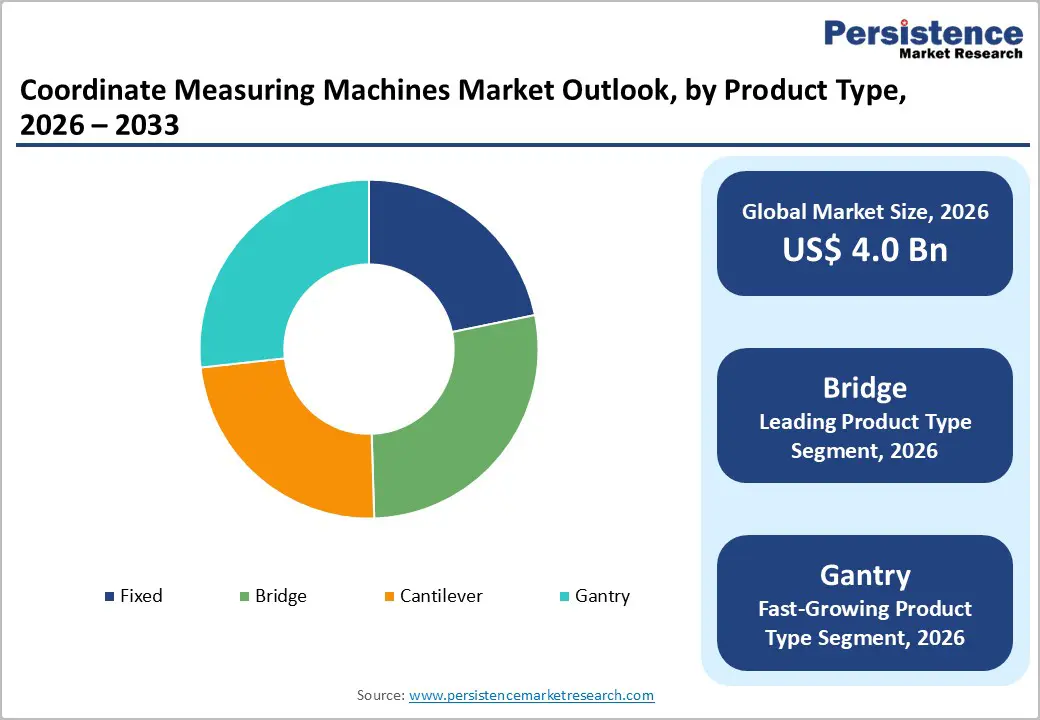

The global coordinate measuring machines market size is expected to be valued at US$ 4.0 billion in 2026 and projected to reach US$ 7.0 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

Rising precision demands in advanced manufacturing, particularly under Industry 4.0 frameworks, are accelerating the adoption of automated and high-accuracy inspection systems. According to the International Federation of Robotics, 553,000 robot units were installed in 2023, increasingly integrated with CMMs for real-time quality control. Additionally, the International Organization of Motor Vehicle Manufacturers reported 92 million vehicles produced globally, reinforcing demand for micron-level measurement solutions.

Key Industry Highlights:

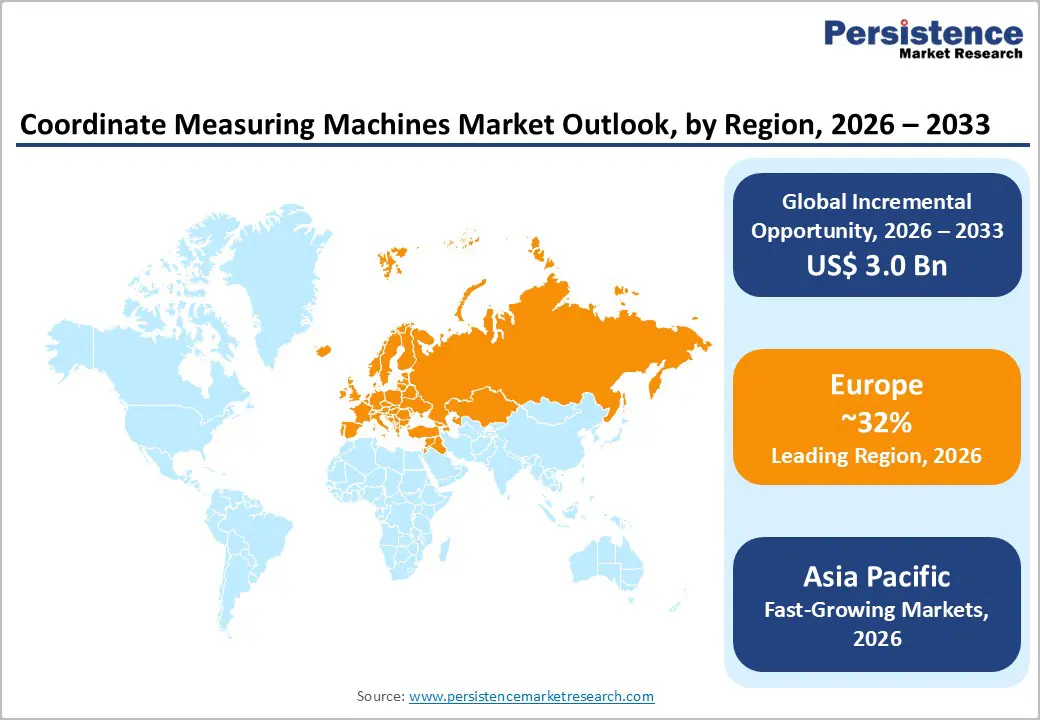

- Leading Region: Europe leads the Coordinate Measuring Machines market with a 32% share in 2025, supported by strong automotive and precision engineering hubs across Germany, France, and the UK.

- Fastest Growing Region: Asia Pacific holds 30% market share in 2025 and remains the fastest-growing regional market, driven by rapid industrialization and expanding electronics and EV manufacturing.

- Leading Product Category: Bridge CMMs dominate the product segment with a 45% share in 2025, favored for their rigidity, modularity, and suitability for high-precision automotive and electronics applications.

- Leading Application Category: Quality Control accounts for 50% market share in 2025, reflecting strong demand for ISO-compliant inspection, defect reduction, and recall prevention.

- Key Opportunity: The medical devices industry represents the fastest-growing opportunity, fueled by rising precision requirements for implants, diagnostics, and regulated manufacturing environments.

| Key Insights | Details |

|---|---|

| Coordinate Measuring Machines Size (2026E) | US$ 4.0 billion |

| Market Value Forecast (2033F) | US$ 7.0 billion |

| Projected Growth CAGR (2026 - 2033) | 8.4% |

| Historical Market Growth (2020 - 2025) | 8.1% |

Market Dynamics

Drivers - Harmonization of Global Metrology Standards and Rapid Automation Integration Strengthening CMM Adoption

Revisions to ISO 10360 led by the National Institute of Standards and Technology have strengthened global confidence in Coordinate Measuring Machines by unifying performance verification protocols. Standard harmonization improves cross-border equipment validation and ensures measurement traceability across high-precision industries. The ASME adoption of B89.4.10360.2 further reinforces reliability standards for aerospace and automotive applications.

Automation integration is accelerating alongside Industry 4.0 deployment. IoT-enabled CMMs equipped with real-time analytics reduce unplanned downtime and enhance predictive maintenance capabilities. Smart factory environments increasingly integrate robotic handling systems with metrology platforms to improve throughput and process control, supporting consistent micron-level inspection accuracy across digitally connected production lines.

Expanding Aerospace Production and Rapid Electric Vehicle Manufacturing Driving High-Precision Inspection Demand

The aerospace sector remains a significant demand driver, with the Federal Aviation Administration overseeing more than 25,000 registered aircraft requiring stringent dimensional compliance and sub-micron inspection standards. Increasing aircraft production and maintenance cycles necessitate advanced CMM deployment to meet regulatory certification and structural safety requirements.

Simultaneously, electric vehicle production reached approximately 14 million units in 2023, intensifying the need for precise battery, drivetrain, and power electronics measurement. According to the American Society of Mechanical Engineers, improved dimensional control can reduce manufacturing scrap rates by 20-25%, reinforcing CMM adoption for efficiency, cost optimization, and regulatory compliance.

Restraints - Significant Capital Expenditure Requirements and Skilled Workforce Constraints Limiting Broader CMM Adoption

Coordinate Measuring Machines involve substantial upfront investment, with system costs typically ranging between US$100,000 and US$500,000 depending on configuration and accuracy class. According to the National Institute of Standards and Technology, precision verification and environmental compliance requirements further increase total ownership expenses. Additional calibration, maintenance, and software integration can add 15-20% to lifecycle costs.

Workforce limitations further constrain adoption. The World Economic Forum projects an 85 million global manufacturing skills gap, limiting the availability of trained metrology specialists. In cost-sensitive and emerging markets, the shortage of qualified operators combined with high capital intensity slows CMM penetration and delays modernization initiatives.

Fragmented International Regulatory Alignment Creating Measurement Inconsistencies and Investment Hesitation

Although European markets broadly align with ISO metrology standards, regulatory variations across parts of Asia and other developing regions create inconsistencies in calibration and validation protocols. According to the International Organization for Standardization surveys, differing interpretations of compliance frameworks can contribute to measurement deviations of 10-15% in certain industrial environments.

The United Nations Industrial Development Organization also highlights supply chain and conformity assessment disparities that increase rework risks and certification delays. These inconsistencies discourage cross-border equipment investments and complicate multinational quality assurance strategies, thereby restraining uniform adoption of advanced CMM systems globally.

Opportunity - Expanding Integration of Additive Manufacturing Processes Creating Advanced 3D Metrology Demand

The rapid growth of additive manufacturing (AM) is creating strong opportunities for Coordinate Measuring Machines in complex 3D part validation. The AM market expanded by 18.5% in 2024, reaching US$5.2 billion, increasing the need for high-accuracy dimensional verification of layered components. The National Institute of Standards and Technology supports advanced metrology research to improve measurement reliability in additively manufactured parts.

Government-backed innovation initiatives are accelerating this integration. U.S. manufacturing programs have allocated approximately US$40 million toward metrology and smart inspection development. Large-format gantry CMM systems are gaining attention for aerospace and industrial AM applications, with strong projected growth as manufacturers prioritize validation of lightweight, topology-optimized components.

Rising Medical Device Manufacturing and Regulatory Compliance Driving Portable CMM Adoption

The medical technology sector presents significant growth potential for precision metrology systems. The World Health Organization projects approximately 12% growth in the medtech industry through 2030, increasing demand for accurate inspection of implants, surgical tools, and diagnostic equipment. Precision validation is critical to ensure patient safety and regulatory conformity.

Regulatory momentum further strengthens this opportunity. The U.S. Food and Drug Administration reported a 25% increase in approvals for advanced and 3D-printed medical devices. Compliance with ISO 13485 quality standards, alongside €1 billion in European health technology funding is accelerating demand for flexible and portable CMM solutions.

Category-wise Analysis

Product Type Insights

Bridge CMMs lead the product type segment, accounting for approximately 45% market share in 2025. Their structural rigidity, thermal stability, and modular configuration make them ideal for medium to large components used in automotive and electronics manufacturing. Compliance with VDI/VDE 2617 guidelines enables measurement errors below 1.5 μm, reinforcing their dominance across nearly 80% of advanced production facilities prioritizing precision and repeatability.

Gantry CMMs are emerging as the fastest-growing category, driven by increasing demand for large-scale inspection in aerospace structures, wind energy components, and heavy machinery. As manufacturers focus on validating oversized and complex geometries, gantry systems are gaining traction due to their extended measurement volumes and enhanced structural robustness in industrial environments.

Industry Insights

The automotive sector holds the largest share at around 35% in 2025, supported by high-volume production and stringent dimensional accuracy requirements. With 92 million vehicles manufactured globally, chassis, drivetrain, and powertrain inspections remain critical. Regulatory frameworks enforced by the National Highway Traffic Safety Administration further strengthen precision compliance requirements, especially for electric vehicle battery assemblies and lightweight structural platforms.

The medical devices industry is the fastest-growing segment, propelled by rising demand for precision-engineered implants, diagnostic tools, and minimally invasive instruments. Increasing regulatory oversight and expanding adoption of advanced manufacturing techniques, including micro-machining and additive production, are driving the need for highly accurate and flexible metrology systems in controlled production environments.

Application Insights

Quality control dominates the application segment with approximately 50% share in 2025, reflecting the essential role of CMMs in defect detection and compliance verification. Over 1.2 million organizations certified under International Organization for Standardization ISO 9001 require stringent dimensional inspections, contributing to recall reductions of nearly 40% through systematic measurement validation and documentation practices.

Reverse engineering is emerging as the fastest-growing application, fueled by product redesign cycles, legacy component replication, and digital twin development. As manufacturers prioritize rapid prototyping and product lifecycle optimization, CMM-generated data is increasingly integrated into CAD modeling and simulation platforms to accelerate innovation and reduce development timelines.

Regional Insights

North America Coordinate Measuring Machines Market Trends and Insights

North America represents a technologically advanced CMM landscape and is projected to expand at a CAGR of approximately 8.0% through the forecast period. The United States leads regional adoption, supported by metrology modernization initiatives from the National Institute of Standards and Technology and collaborative additive manufacturing programs under America Makes, which allocated nearly US$50 million in 2024 toward advanced metrology development.

Aerospace and electric vehicle production remain key growth engines. The Federal Aviation Administration enforces stringent aircraft inspection requirements, while companies such as Boeing and General Motors continue investing in precision-driven manufacturing under clean energy and infrastructure policies, accelerating automated CMM integration across production lines.

Europe Coordinate Measuring Machines Market Trends and Insights

Europe leads the global CMM market with approximately 32% share in 2025, driven by strong automotive and precision engineering sectors. Germany anchors regional dominance through innovation programs supported by VDMA and applied research from Fraunhofer Society, fostering hybrid and multi-sensor CMM advancements across industrial facilities.

Regulatory harmonization under EU Directive 2006/42/EC ensures standardized machinery compliance across Germany, the UK, France, and Spain. Automotive leaders such as BMW are expanding precision manufacturing capacity, while Renishaw plc strengthens aerospace-focused metrology capabilities, reinforcing Europe’s leadership in high-accuracy inspection systems.

Asia Pacific Coordinate Measuring Machines Market Trends and Insights

Asia Pacific accounts for approximately 30% of the market share in 2025 and remains the fastest-growing regional market, driven by rapid industrialization and the expansion of electronics manufacturing. China’s industrial modernization strategy under Ministry of Industry and Information Technology and the “Made in China 2025” initiative has accelerated advanced equipment installations, particularly within electric vehicle manufacturing ecosystems.

Automotive producers such as BYD are increasing precision inspection capacity to support EV growth. Japan and India are also strengthening regional competitiveness through technology exhibitions like JIMTOF 2024. India, in particular, demonstrates strong expansion momentum with an estimated double-digit growth trajectory supported by manufacturing localization initiatives.

Competitive Landscape

The Coordinate Measuring Machines market reflects a moderately consolidated structure, with leading multinational manufacturers maintaining a dominant position supported by strong global distribution networks and advanced R&D capabilities. Competition centers on precision enhancement, software integration, and automation compatibility. Companies are increasingly investing in artificial intelligence-driven inspection algorithms, advanced probing systems, and multi-sensor platforms to differentiate their offerings and improve throughput, repeatability, and data-driven decision-making across smart factory environments.

Strategic expansion is also occurring through targeted acquisitions, portfolio diversification, and modular machine architecture development. Vendors are introducing scalable systems that allow upgrades in software, sensors, and automation interfaces. Additionally, subscription-based metrology services and digital inspection-as-a-service models are emerging, enabling predictable costs and continuous performance optimization for end users.

Key Developments:

- In June 2024, Hexagon AB launched the Leitz PMM-C ultra-accuracy CMM series, designed for high-precision applications in aerospace and advanced manufacturing, enhancing sub-micron measurement performance and strengthening its portfolio in ultra-high accuracy coordinate metrology systems.

- In 2024, ZEISS Group expanded its industrial metrology capabilities through ATOS Q CT integration, combining optical 3D scanning with computed tomography technologies to deliver comprehensive internal and external component inspection solutions for precision-driven industries.

- In April 2023, Hexagon AB introduced its next-generation Leitz PMM-C platform, later updated in 2024, featuring improved structural stability, enhanced sensor compatibility, and upgraded software integration to support automated and smart factory inspection environments.

Companies Covered in Coordinate Measuring Machines Market

- Hexagon AB

- Carl Zeiss AG

- Mitutoyo Corporation

- Nikon Corporation

- Renishaw plc

- FARO Technologies

- Wenzel Group

- Tokyo Seimitsu Co., Ltd.

- LK Metrology Ltd.

- Aberlink Ltd.

- Coord3 Industries

- Creaform Inc.

- Perceptron, Inc.

- Optical Gaging Products

- Quanta Cloud Technology

Frequently Asked Questions

The global Coordinate Measuring Machines market is valued at US$ 4.0 billion in 2026.

Demand is driven by Industry 4.0 integration, automotive production holding 35% share in 2025, and precision-intensive aerospace manufacturing.

Europe leads the market with a 32% share in 2025, supported by strong precision engineering and automotive hubs.

Quality Control dominates with a 50% share in 2025, reflecting widespread ISO-compliant inspection requirements.

Medical devices represent the fastest-growing opportunity, supported by rising precision demand and expanding regulated manufacturing environments.

Key players in the market include Hexagon AB, Carl Zeiss AG, Mitutoyo Corporation, Nikon Corporation, and Renishaw plc.