- Automation & Robotics

- Machine Tending Robots Market

Machine Tending Robots Market Size, Share, and Growth Forecast 2026 - 2033

Machine Tending Robots Market by Robot Type (Articulated Robots, Collaborative Robots, SCARA Robots, Cartesian Robots, Delta Robots, Cylindrical Robots), Application (CNC Machine Tending, Injection Molding Tending, Press Machine Tending, Die Casting, Grinding & Polishing, Welding Support, Packaging & Sorting, Inspection Handling, Material Loading & Unloading), End-user, and Regional Analysis, 2026 - 2033

Machine Tending Robots Market Size and Trend Analysis

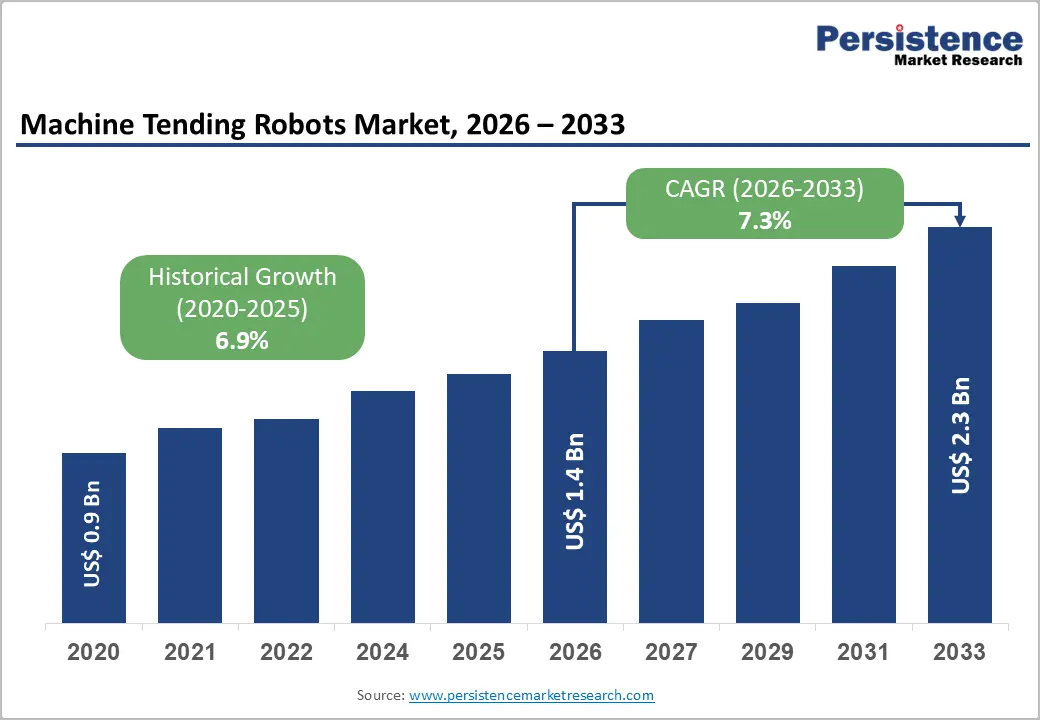

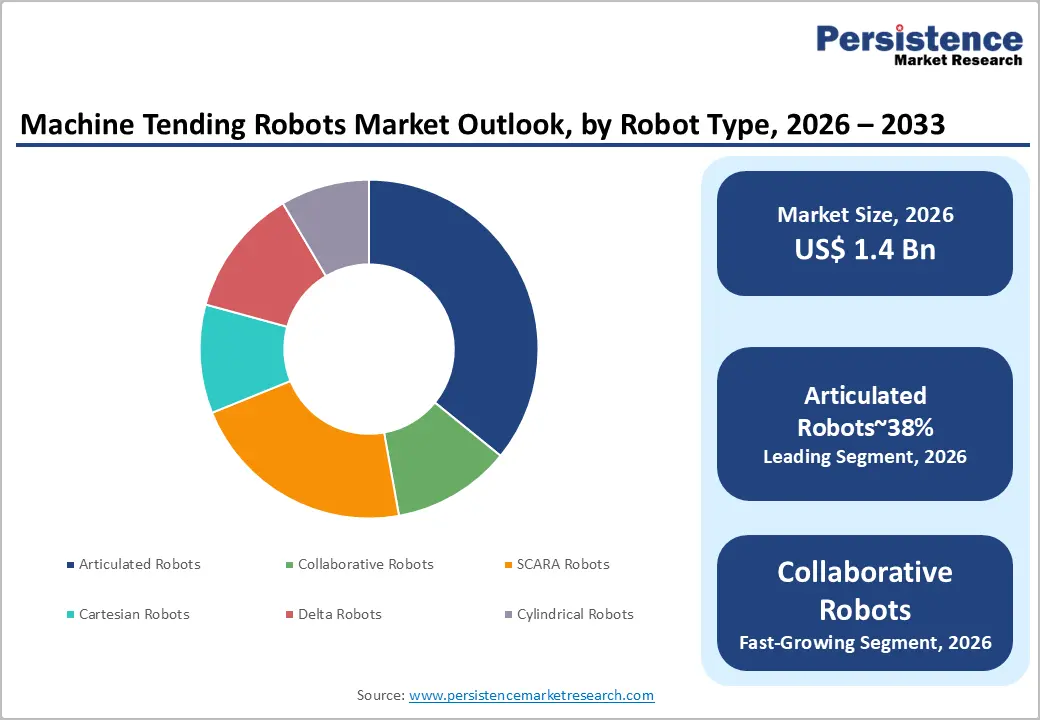

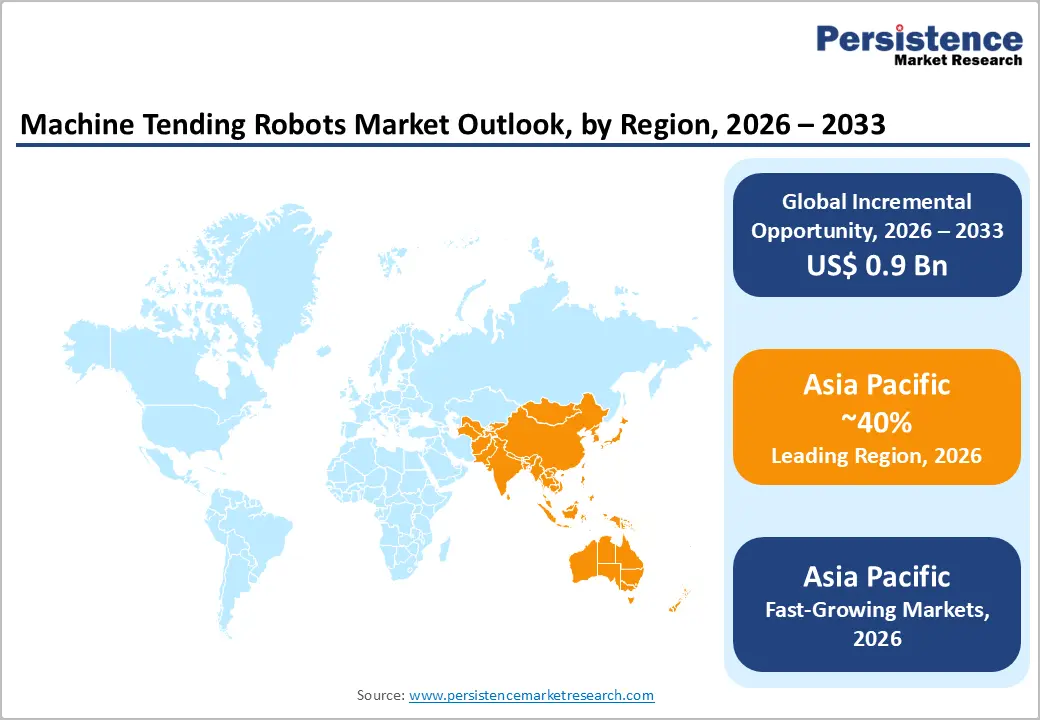

The global Machine Tending Robots market size is likely to be valued at US$ 1.4 Billion in 2026 and is expected to reach US$ 2.3 Billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033.

The machine tending robots market is propelled by accelerating industrial automation across manufacturing sectors, rising labor costs, and the push for precision-driven production. Growing demand from the automotive, metal & machinery, and electronics sectors, which together account for a majority of robot deployments, is fueling adoption.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the global machine tending robots market holding 40% share, driven by China's government-backed automation mandates, Japan's OEM strength, and rapidly growing manufacturing bases in India and ASEAN countries fueling continuous demand.

- Fastest Growing Region: Asia Pacific also registers the highest growth rate, propelled by India's PLI scheme, China's 'Robot+' Action Plan targeting 500 robots per 10,000 workers, and surging electronics manufacturing investments across Vietnam and Indonesia.

- Dominant Segment: Articulated Robots dominate the by robot type category with approximately 38% market share, owing to their multi-axis flexibility, high payload capacity, and compatibility with diverse machine tending applications across automotive and metal sectors.

- Fastest Growing Segment: Collaborative Robots (Cobots) represent the fastest growing robot type segment, driven by their ease of deployment, human-safe operation, and accessibility for SMEs across electronics, pharmaceuticals, and consumer goods manufacturing industries.

- Key Opportunity: Integration of AI and machine vision into tending robots offers high-margin growth potential, enabling adaptive, inspection-capable systems for semiconductor fabrication, aerospace, and pharmaceutical applications requiring zero-defect precision automation.

Market Dynamics

Drivers - Rising Industrial Automation and Labor Shortage Pressures

The escalating adoption of industrial automation is a primary catalyst for machine tending robot deployments. According to the International Federation of Robotics (IFR), global robot installations in manufacturing reached approximately 553,000 units in 2022, with the figure continuing to climb year-over-year. Labor shortages, particularly in precision manufacturing roles, are pushing manufacturers to invest in automated machine tending systems.

In the United States, the Bureau of Labor Statistics (BLS) projected over 600,000 unfilled manufacturing jobs annually through the mid-2020s. Machine tending robots address this gap by enabling 24/7 unmanned operations, reducing cycle times and improving throughput, directly enhancing factory profitability and competitiveness.

Expansion of Collaborative Robot (Cobot) Technology

The growing penetration of collaborative robots (cobots) is reshaping the machine tending landscape. Unlike traditional industrial robots, cobots are designed with inherent safety features enabling them to work alongside human workers without extensive guarding. The IFR noted that cobots represent one of the fastest-growing robot segments, with annual shipment growth exceeding 20% in recent years.

Companies such as Universal Robots and Techman Robot have made deployments accessible to small and medium-sized enterprises (SMEs) through lower upfront investment and simplified programming. This democratization of automation is driving adoption in sectors such as electronics, plastics, and food & beverage, significantly expanding the addressable market for machine tending solutions.

Restraints - High Initial Capital Investment and Integration Complexity

Despite long-term ROI benefits, the substantial upfront investment required for machine tending robot systems remains a significant barrier, particularly for small and medium enterprises. A fully integrated robotic machine tending cell, including the robot, grippers, sensors, safety systems, and programming, can cost between US$ 100,000 and US$ 500,000 or more, depending on complexity.

This capital intensity, combined with integration challenges involving legacy machinery and the need for specialized engineering talent, often delays purchase decisions. According to surveys by the Robotics Industries Association (RIA), integration costs frequently exceed the initial equipment cost, creating a total cost of ownership challenge that tempers adoption among budget-constrained manufacturers.

Skilled Workforce Gap in Robot Programming and Maintenance

The effective deployment and upkeep of machine tending robots demands a skilled workforce proficient in robotics programming, systems integration, and predictive maintenance. However, the global talent pipeline has not kept pace with market demand. The World Economic Forum (WEF) estimated that by 2025, over 85 million jobs could be displaced by automation while new technical roles go unfilled.

The complexity of programming platforms, especially for multi-axis articulated robots, further amplifies this skills gap, slowing deployment timelines and increasing operational costs. This restraint particularly impacts emerging markets where technical training infrastructure remains underdeveloped, limiting market penetration despite strong economic incentives for automation.

Opportunities - Surge in Semiconductor and Electronics Manufacturing Automation

The global semiconductor supply chain reshoring drive, accelerated by policies such as the U.S. CHIPS and Science Act (2022), which allocated US$ 52 billion for domestic chip manufacturing, is creating a substantial demand wave for precision machine tending robots in electronics and semiconductor fabrication. Similarly, the European Chips Act targets doubling Europe's semiconductor market share to 20% by 2030.

These investments are translating into greenfield fab construction projects that require highly precise robotic machine tending for wafer handling, chip packaging, and PCB assembly. Given the high-mix, low-volume nature of semiconductor production, cobots and SCARA robots with vision systems are positioned as ideal tending solutions, offering significant revenue opportunity for market participants.

Integration of AI and Machine Vision in Smart Machine Tending

The convergence of artificial intelligence (AI), machine vision, and industrial IoT with machine tending robots is opening a new frontier of intelligent automation. Modern machine tending systems equipped with 2D/3D vision systems and AI-powered defect detection can dynamically adjust to part variation, optimize grip force, and perform inline quality inspection simultaneously.

Companies such as FANUC Corporation and ABB Ltd. have introduced AI-powered robot platforms with adaptive learning capabilities. According to the Japan Robot Association (JARA), intelligent robots with embedded AI capabilities are expected to account for a growing share of new deployments by 2030. For market participants, developing AI-enhanced tending solutions for high-precision applications such as aerospace components and pharmaceutical packaging represents a high-margin growth avenue.

Category-wise Analysis

By Robot Type Insights

Articulated Robots dominate the machine tending robots market by robot type, commanding an estimated market share of approximately 38%. Their leadership stems from unparalleled flexibility, with 6 or more degrees of freedom (DoF), articulated robots can navigate complex workpiece geometries, access difficult-to-reach machine compartments, and execute multi-step tending sequences with precision.

The IFR consistently identifies articulated robots as the most widely installed robot type globally, accounting for the majority of annual industrial robot shipments. Their compatibility with CNC machine tending, die casting, and welding support applications, all major market verticals, reinforces their dominance. Leading suppliers, including FANUC, KUKA, and Yaskawa continue to expand articulated robot portfolios with improved payload and reach.

By Application Insights

CNC Machine Tending represents the leading application segment, capturing an estimated 28% share of the overall machine tending robots market. CNC machine tending, encompassing automated loading of raw stock, part fixturing, and finished part unloading, is one of the most labor-intensive and repetitive tasks in precision machining.

Automating this workflow dramatically reduces cycle times and human error while enabling continuous production. The global CNC machine tool market, valued in the tens of billions, generates persistent demand for robotic tending solutions. According to the Gardner Business Media World Machine Tool Survey, global machine tool consumption continues to grow, particularly in China, the U.S., and Germany, directly fueling CNC tending robot deployments across automotive and aerospace supply chains.

By End-user Insights

The Automotive sector remains the dominant end-use industry for machine tending robots, holding an estimated market share of around 32%. Automotive manufacturing involves high-volume, repetitive processes including stamping, die casting, CNC machining of engine components, and injection molding of interior parts, all prime candidates for automated machine tending.

The IFR World Robotics Report consistently identifies the automotive sector as the single largest employer of industrial robots globally. Moreover, the industry's accelerating transition to electric vehicles (EVs) is driving fresh capital expenditure in battery component manufacturing and lightweight structural part production, both of which require sophisticated machine tending automation from suppliers like ABB, KUKA AG, and Comau S.p.A.

Regional Insights

North America Machine Tending Robots Market Trends & Analysis

North America represents a technologically mature market, contributing approximately 30% of the global market. Growth is driven by reshoring initiatives, labor shortages, and policy-backed manufacturing expansion. High adoption in automotive, aerospace, and metal machining sectors continues to sustain steady demand for machine tending automation.

- U.S. Machine Tending Robots Market Size

The U.S. dominates the regional landscape, accounting for nearly 75% of North America. Federal incentives such as the CHIPS Act and Inflation Reduction Act are accelerating smart factory investments. Strong presence of system integrators and rising SME adoption of collaborative robots further support consistent market expansion.

Europe Machine Tending Robots Market Trends, Drivers & Insights

Europe holds around 27% share, supported by its advanced manufacturing ecosystem and strong machine tool industry. Demand is fueled by precision engineering sectors, sustainability-driven automation, and EU-backed industrial policies. Increasing cobot adoption among SMEs is also reshaping regional automation strategies.

- Germany Machine Tending Robots Market Size

Germany leads Europe with approximately 35% regional share. Its strong automotive and CNC machining base drives continuous robot deployment. The country’s focus on Industry 4.0 and leadership in machine tool manufacturing sustains high demand for advanced machine tending solutions.

- U.K. Machine Tending Robots Market Size

The U.K. accounts for nearly 12% of Europe. Growth is supported by aerospace and precision engineering sectors. Increasing labor costs and government-backed digital manufacturing initiatives are encouraging SMEs to adopt flexible robotic tending systems, particularly collaborative robots.

- France Machine Tending Robots Market Size

France contributes about 10%, driven by automation in aerospace, automotive, and defense manufacturing. Government programs promoting industrial modernization and smart factories are boosting robot integration, especially in high-value production environments requiring precision and repeatability.

Asia Pacific Machine Tending Robots Market Drivers & Analysis

Asia Pacific dominates with 40% share and is the fastest-growing region. Rapid industrialization, rising labor costs, and government-led automation initiatives are key drivers. Strong electronics, automotive, and heavy machinery production hubs ensure sustained high demand for machine tending robots.

- China Machine Tending Robots Market Size

China leads globally, accounting for 45% of APAC. Government initiatives like the “Robot+” Action Plan and aggressive factory automation are accelerating adoption. The country’s massive manufacturing base and increasing robot density targets are key growth catalysts.

- India Machine Tending Robots Market Size

India is an emerging high-growth market with 6.8% share of APAC. Growth is driven by PLI schemes, expanding automotive and electronics manufacturing, and rising labor cost pressures. Adoption is increasing among large enterprises and gradually penetrating SMEs.

- Japan Machine Tending Robots Market Size

Japan holds around 18% of APAC. As a global robotics leader, the country benefits from strong domestic demand and advanced automation culture. High robot density, aging workforce, and leadership in precision manufacturing continue to drive steady adoption of machine tending robots.

Competitive Landscape

The machine tending robots market exhibits a moderately consolidated structure, dominated by a handful of global robotics leaders including ABB Ltd., FANUC Corporation, KUKA AG, and Yaskawa Electric Corporation. These incumbents compete on robot performance, ecosystem depth (software, integrators), and global service networks.

The cobot segment is relatively more fragmented, with challengers such as Universal Robots and Techman Robot disrupting traditional OEMs through easier deployment and lower TCO. Key differentiators include AI-powered vision integration, open software platforms, and modular gripper ecosystems. M&A activity and strategic partnerships with system integrators are common expansion strategies, while R&D investment focuses on AI-driven adaptive tending and human-robot collaboration safety frameworks.

Key Market Developments

- January, 2025: ABB Ltd. launched its next-generation GoFa cobot series featuring enhanced payload capacity of up to 10 kg and integrated force-torque sensing, specifically targeting CNC machine tending and assembly applications in automotive and electronics sectors.

- September, 2024: FANUC Corporation announced the expansion of its FIELD system AI-integrated platform to support real-time adaptive machine tending, enabling robots to autonomously adjust gripping and part-placement sequences based on live machine feedback without human reprogramming.

- March, 2024: Universal Robots introduced its UR30 cobot, offering a 30 kg payload in a compact form factor, directly addressing heavy-part machine tending applications in metal machining, die casting, and press tending operations globally.

Companies Covered in Machine Tending Robots Market

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Universal Robots A/S

- Kawasaki Heavy Industries Ltd.

- Omron Corporation

- DENSO Corporation

- Stäubli International AG

- Epson Robots

- Comau S.p.A.

- Nachi-Fujikoshi Corp.

- Doosan Robotics Inc.

- Techman Robot Inc.

- Rethink Robotics GmbH

- Aubo Robotics

- Kassow Robots

Frequently Asked Questions

The global machine tending robots market is estimated to be valued at US$ 1.4 Billion in 2026, and it is projected to reach US$ 2.3 Billion by 2033, growing at a CAGR of 7.3% over the forecast period. Historically, the market grew at a CAGR of 6.9% between 2020 and 2025, reflecting robust adoption across manufacturing sectors.

The primary growth drivers include escalating industrial automation to address manufacturing labor shortages (with over 600,000 unfilled manufacturing jobs annually in the U.S. alone per the Bureau of Labor Statistics), rapid proliferation of collaborative robot technology enabling SME adoption, and large-scale government manufacturing investment programs such as the U.S. CHIPS and Science Act and EU Industrial Strategy.

Articulated Robots dominate the market by robot type with an estimated 38% share, driven by their superior degrees of freedom, high payload capacity, and versatility across CNC tending, die casting, and welding support applications. The IFR confirms articulated robots consistently represent the largest category of globally installed industrial robots.

Asia Pacific is the leading region, accounting for the largest share of the global machine tending robots market. China's government-backed 'Robot+' Action Plan, Japan's world-class robotics OEM base (FANUC, Yaskawa), India's PLI scheme, and rapid electronics manufacturing growth across ASEAN collectively underpin the region's dominant market position.

A significant opportunity lies in the integration of AI and machine vision systems into machine tending robots, enabling adaptive, intelligent automation for high-precision industries. Semiconductor fabrication reshoring programs (U.S. CHIPS Act, US$ 52 billion; European Chips Act) are generating demand for smart tending solutions in wafer handling and chip packaging applications, offering high-margin growth prospects.

Key market players include ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, Mitsubishi Electric Corporation, Universal Robots A/S, Kawasaki Heavy Industries Ltd., Omron Corporation, DENSO Corporation, Stäubli International AG, Epson Robots, Comau S.p.A., Nachi-Fujikoshi Corp., Doosan Robotics Inc., and Techman Robot Inc., among other emerging regional players.