- Automation & Robotics

- Service Robotics Market

Service Robotics Market Size, Share, and Growth Forecast 2026 - 2033

Service Robotics Market by Robot Type (Professional, Personal), End Use (Défense, Field, Medical, Transportation and Logistics, Mobile Platforms, Underwater Systems, Construction, Others), and Regional Analysis for 2026 - 2033

Service Robotics Market Size and Trend Analysis

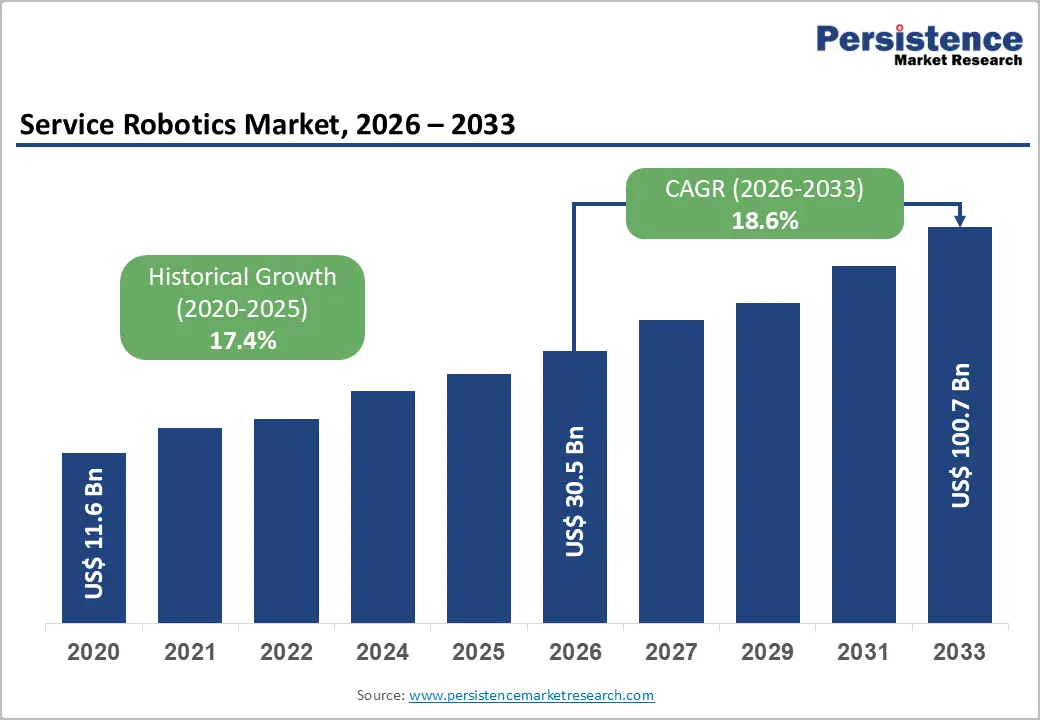

The global Service Robotics Market size is valued at US$ 30.4 billion in 2026 and is projected to reach US$ 100.7 billion by 2033, growing at a CAGR of 18.6% between 2026 and 2033. This exceptional growth trajectory is driven by the convergence of artificial intelligence, advanced sensor technology, and the acute global labour shortage that is compelling enterprises across healthcare, logistics, defence, and consumer sectors to deploy autonomous robotic solutions at scale.

According to the International Federation of Robotics, professional service robot sales reached nearly 200,000 units in 2024, with the Robot-as-a-Service (RaaS) fleet growing by 31% in the same year, reflecting a structural shift in deployment models.

Key Industry Highlights:

- Leading Region: North America leads the service robotics market, anchored by the U.S. which hosts 199 service and medical robot manufacturers, a world-class AI innovation ecosystem, strong défense procurement, and accelerating healthcare and logistics automation investment.

- Fastest Growing Region: Asia Pacific is the fastest-growing market, accounting for nearly 80% of professional service robots sold globally in 2023, driven by China's Robot+ Action Plan, Japan's eldercare robot demand, and India's rapidly expanding healthcare and logistics automation sectors.

- Dominant Segment: Professional service robots are dominant and account for 60% revenue share, supported by higher per-unit revenues, large-scale logistics deployments, and the 31% growth in Robot-as-a-Service fleet deployments recorded by IFR in 2024.

- Fastest Growing Segment: Medical robots are the fastest-growing end-use segment, with reporting 91%-unit sales growth in 2024, including 610% growth in diagnostics and laboratory robots, driven by aging population and acute healthcare labour shortages across developed economies.

- Key Opportunity: Défense and autonomous underwater systems represent a key market opportunity, with global military expenditure reaching US$ 2.44 trillion in 2023 per SIPRI, driving government-backed procurement of AUVs, unmanned ground systems, and autonomous défense platforms at accelerating rates.

DRO Analysis

Drivers - Global Labor Shortages and Industrial Automation Imperatives

Acute labour shortages across healthcare, logistics, manufacturing, and hospitality sectors are the most powerful structural catalyst accelerating the adoption of service robots globally. According to the IFR’s World Robotics 2025 Service Robots report, staff shortages are identified as a key driver compelling organizations to deploy robots designed for trained professionals.

In the United States alone, the Bureau of Labor Statistics (BLS) projects that healthcare and social assistance sectors will add over 2 million jobs by 2033, against a backdrop of chronic workforce deficits a gap increasingly filled by medical and care robots. In logistics, reports suggest that transportation and logistics robots represented more than every other professional service robot sold in 2024, with 102,900 units sold a 14% year-on-year increase as labour-intensive warehouse and fulfilment operations automate at an accelerating pace globally.

AI Integration and Robot-as-a-Service Business Model Expansion

The rapid integration of Artificial Intelligence (AI), machine learning, and advanced sensor fusion technologies into service robot platforms is dramatically expanding the capability envelope and commercial viability of autonomous systems. AI-powered navigation, object recognition, and natural language interaction enable robots to perform increasingly complex tasks with minimal human supervision.

Concurrently, the emergence of the Robot-as-a-Service (RaaS) business model is democratizing access to service robotics by eliminating high upfront capital barriers. According to the World Robotics 2025 report, RaaS fleet deployments grew by an impressive 31% in 2024, with the transportation and logistics sub-segment recording RaaS growth of 42%. This subscription-based model is particularly transformative for small and medium enterprises (SMEs), enabling them to access enterprise-grade robotic automation without prohibitive capital expenditure.

Restraints - High Initial Investment and Total Cost of System Integration

Despite falling unit hardware costs, the total cost of deploying service robots encompassing software integration, system customization, facility modification, cybersecurity infrastructure, and workforce retraining remains a significant barrier, particularly for smaller enterprises and healthcare organizations operating under constrained budgets.

Complex integration with existing Enterprise Resource Planning (ERP) systems, operational technology infrastructure, and safety certification requirements can add substantially to project costs and implementation timelines. These barriers disproportionately affect cost-sensitive application segments such as social care and construction, slowing market penetration in otherwise high-potential end-use environments.

Regulatory Complexity and Cybersecurity Vulnerabilities

The service robotics industry faces a fragmented and evolving global regulatory environment that creates compliance uncertainty for manufacturers and deployers. Standards for robot safety, data privacy, autonomous decision-making, and liability in healthcare and defence applications vary significantly across jurisdictions, increasing compliance costs and slowing cross-border market entry.

Furthermore, as service robots become increasingly networked and AI-driven, cybersecurity risks escalate compromised robotic systems in healthcare, defence, or critical infrastructure could have severe operational or safety consequences. The European Union’s Artificial Intelligence Act, adopted in 2024, introduces tiered risk classifications that directly affect how AI-enabled robots are designed, tested, and deployed, adding regulatory compliance complexity for manufacturers targeting the EU market.

Opportunities - Medical and Eldercare Robotics: A High-Growth Demographic-Driven Opportunity

The rapid global aging of populations presents a massive and structurally sustained growth opportunity for medical and personal care service robots. According to the United Nations, the global population aged 65 and over is projected to more than double from approximately 761 million in 2021 to 1.6 billion by 2050, dramatically expanding demand for rehabilitation robots, surgical assistance systems, and eldercare companions.

Rehabilitation and non-invasive therapy robots posted 106% growth. Governments across Japan, South Korea, Germany, and the United States are actively funding eldercare robotics initiatives, creating a policy-supported demand environment that market participants can leverage through application-specific product development and value-added service contracts.

Défense and Autonomous Underwater Systems: Government-Backed Demand Acceleration

Rise in global défense budgets and the strategic prioritization of autonomous systems by military forces worldwide present a compelling long-term growth opportunity for service robotics companies with défense capabilities. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached a record US$ 2.44 trillion in 2023, with autonomous unmanned systems including ground, aerial, and underwater robots receiving increasing budget allocations.

Kongsberg Maritime AS and ECA Group are among the specialists capitalizing on growing naval demand for Autonomous Underwater Vehicles (AUVs) and remotely operated systems for mine countermeasures, surveillance, and maritime security. The NATO alliance’s commitment to technology modernization and the U.S. Department of Défense’s accelerated autonomous systems procurement further underpin this opportunity, creating a government-backed demand pipeline that provides sustained revenue visibility for défense-oriented service robotics providers.

Category-wise Analysis

Robot Type Insights

Professional service robots dominate the Service Robotics Market by robot type, accounting for approximately 60% revenue share, driven by large-scale deployments across transportation and logistics, défense, medical, and industrial cleaning applications. According to the online sources, professional service robots sold for commercial use nearly reached 200,000 units in 2024, reflecting a 9% year-on-year increase.

The professional segment commands higher per-unit revenue given the sophistication of platforms compared to mass-market personal robots, reinforcing its dominant revenue share despite lower unit volumes than consumer applications. The growing enterprise adoption of RaaS subscription models, reporting 31% fleet growth in 2024, further reinforces the professional segment’s structural advantage as organizations prioritize operational flexibility over outright ownership in high-capex robotic deployments.

End-user Insights

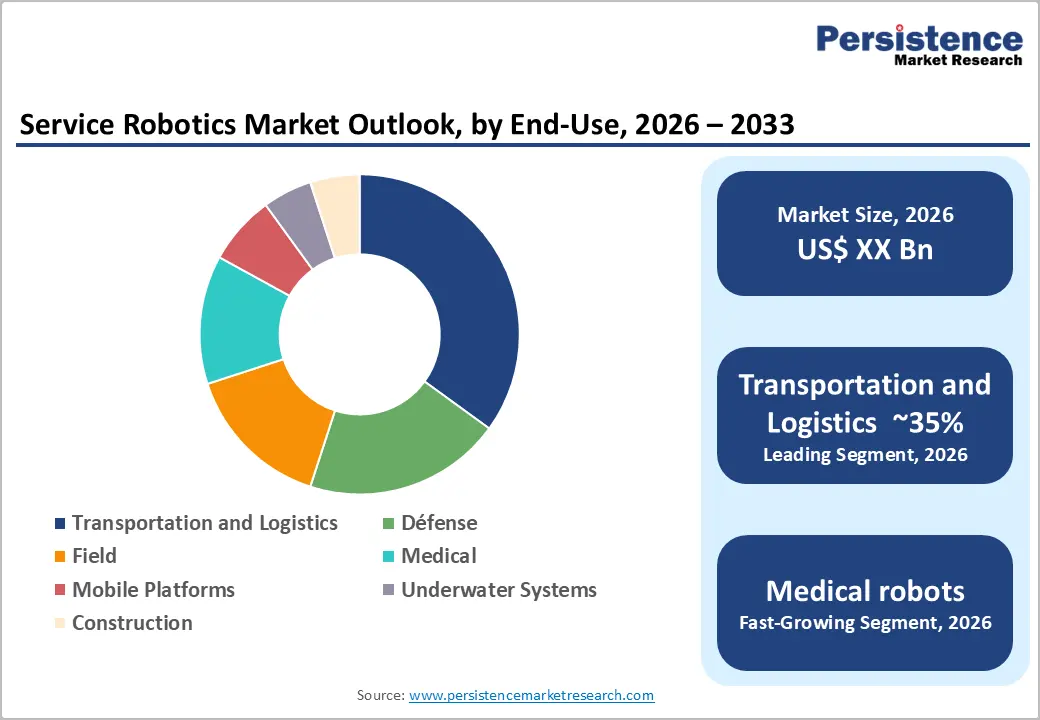

Transportation and logistics is the dominant segment accounting for 35% revenue share in 2026. According to the IFR’s World Robotics 2025 report, 102,900 units were sold in this segment in 2024 alone representing more than every other professional service robot category combined with a 14% year-on-year growth rate. The e-commerce boom, the structural labour shortage in warehouse operations, and the rapid expansion of fulfilment center infrastructure are the primary demand catalysts.

Daifuku Co., Ltd., a global leader in material handling automation, is a key beneficiary of this trend, providing integrated robotic sortation and conveying systems for global logistics operators. The RaaS model has achieved traction in this segment, with transportation and logistics RaaS deployments growing by 42% in 2024, as operators prioritize flexibility and scalability over capital-intensive ownership structures.

Regional Analysis

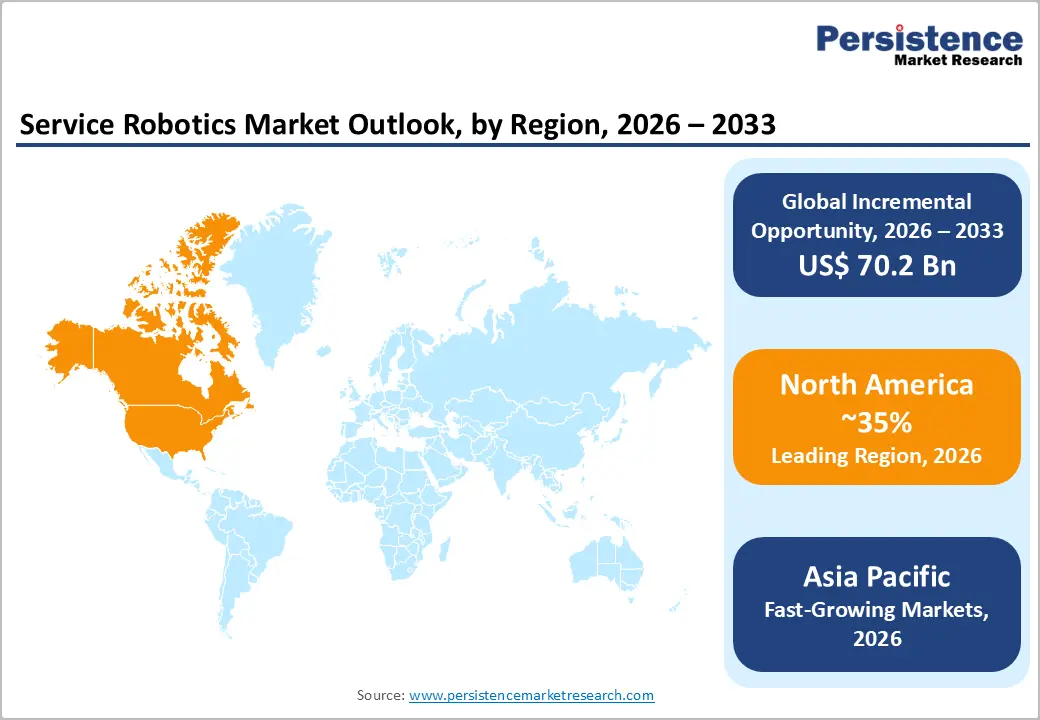

North America Service Robotics Market Trends & Analysis

North America is the leading regional market for service robotics, anchored by the United States, which hosts the largest concentration of service and medical robot manufacturers globally 199 companies, representing approximately 66% professional service and 12% medical robot producers.

The healthcare sector represents a particularly dynamic growth frontier, with U.S. Bureau of Labor Statistics projections highlighting a need for over 2 million additional healthcare workers by 2033a structural deficit that is accelerating deployment of surgical, rehabilitation, and care robots. The logistics transformation driven by Amazon, Walmart, and emerging autonomous delivery networks further reinforces North American demand for mobile platform and transportation robotics.

U.S. Service Robotics Market Size

Estimated at approximately US$ 7.9 Bn in 2026, driven by healthcare robotics, logistics automation, défense procurement, and a mature AI and software ecosystem supporting commercial robot deployment at scale. The U.S. innovation ecosystem, encompassing Silicon Valley, Boston’s robotics corridor, and Pittsburgh’s Carnegie Mellon University cluster, continues to generate breakthrough advances in AI, autonomous navigation, and soft robotics that translate rapidly into commercial product platforms.

Europe Service Robotics Market Trends, Drivers, & Insights

Europe is the second-largest regional market for service robotics, characterized by strong institutional support, advanced manufacturing capabilities, and a deep talent pool in automation engineering. Europe accounted for 33,918 professional service robot units sold in 2023, reflecting the region’s established industrial and healthcare automation base. The European Union’s Horizon Europe research program has allocated substantial funding for robotics and AI research, while the EU Machinery Regulation (EU) 2023/1230 and the Artificial Intelligence Act are shaping a harmonized regulatory framework that supports safe, trustworthy deployment of service robots across member states.

Germany Service Robotics Market Size

Estimated at approximately US$ 2.5 Bn in 2026, led by industrial automation convergence, KUKA AG ecosystem influence, and healthcare robot adoption. Germany leads European demand, leveraging its world-class mechanical engineering heritage and close collaboration between companies like KUKA AG and leading automotive, logistics, and healthcare OEMs.

U.K. Service Robotics Market Size

Estimated at approximately US$ 1.6 Bn in 2026, driven by défense autonomous systems, logistics robotics, and NHS-backed medical robot adoption programs. The United Kingdom is building a significant service robotics ecosystem, supported by UKRI’s robotics and autonomous systems investment programs and a robust défense sector driving procurement of autonomous platforms.

France Service Robotics Market Size

Estimated at approximately US$ 1.2 Bn in 2026, supported by France 2030 industrial investments, healthcare automation, and agricultural robot deployments. France is investing strategically in healthcare robotics and agricultural automation through its France 2030 industrial policy plan, which commits €30 billion to innovative industries including robotics. In May 2025, the European Union announced a €1.5 billion investment in service robot development across healthcare, agriculture, and manufacturing, directly stimulating commercial opportunities across the region.

Asia Pacific Service Robotics Market Drivers & Analysis

Asia Pacific is the dominant region in professional service robot manufacturing and the fastest-growing consumer market globally. Asia Pacific accounted for nearly 80% of professional service robots sold in 2023 162,284 units reflecting the region’s unrivalled manufacturing scale and rapidly expanding domestic demand.

ASEAN economies, particularly Singapore, South Korea (with the world’s highest robot density at 1,012 robots per 10,000 employees), and Australia represent mature sub-markets with strong government support for service robotics in aged care, défense, and mining applications.

China Service Robotics Market Size

Estimated at approximately US$ 6.5 Bn in 2026, underpinned by the Robot+ Action Plan, massive logistics automation investment, and the world’s largest consumer robotics market. China leads both production and consumption, supported by the Chinese government’s national robotics development strategy under the 14th Five-Year Plan and the Robot+ Action Plan (2023–2025), which targets robotics integration across healthcare, mining, construction, and logistics.

India Service Robotics Market Size

Estimated at approximately US$ 1.1 Bn in 2026, driven by healthcare infrastructure investment, logistics automation, and PLI-supported domestic manufacturing growth. India is the fastest-growing country market in the region, catalysed by the government’s Production Linked Incentive (PLI) scheme, digital transformation initiatives, and rising healthcare infrastructure investment. The deployment of service robots in Indian hospitals, warehouses, and public spaces is accelerating as local manufacturing capability develops.

Japan Service Robotics Market Size

Estimated at approximately US$ 2.2 Bn in 2026, supported by the world’s highest robot density, eldercare robot demand from its aging population, and advanced AI research ecosystem. Japan represents the world’s most robotics-dense economy, with the highest industrial robot density globally, and Honda Motor Co., Ltd. playing a leading role in advanced humanoid and mobility service robot research.

Competitive Landscape

The global Service Robotics Market exhibits a highly fragmented yet rapidly consolidating competitive structure. A handful of large technology and automation conglomerates, including SoftBank Group Corp. (post-ABB Robotics acquisition), KUKA AG, and Daifuku Co., Ltd.

Key differentiators include AI software stack maturity, application-specific hardware expertise, global service and support networks, and strategic OEM partnerships. Leading players are aggressively pursuing platform-based business models, offering Robot-as-a-Service (RaaS) subscription contracts alongside traditional hardware sales to expand recurring revenue streams.

Key Market Developments

- In October 2025, SoftBank Group Corp. announced a definitive agreement to acquire ABB Ltd.’s robotics division for an enterprise value of US$ 5.375 billion, creating a combined platform to integrate AI and robotics under the banner of “physical AI,” expected to close in mid-to-late 2026.

- In April 2025, iRobot Corporation raised US$ 150 million in a funding round, bringing total funding to over US$ 500 million, to accelerate the development and commercialization of next-generation home and professional service robots.

Companies Covered in Service Robotics Market

- ABB Ltd

- KUKA AG

- iRobot Corporation

- SoftBank Robotics Holdings

- Kongsberg Maritime AS

- Honda Motor Co., Ltd.

- Daifuku Co., Ltd.

- ECA Group

- Parrot SA

Frequently Asked Questions

The global Service Robotics Market is valued at US$ 30.4 Bn in 2026 and is projected to reach US$ 100.7 Bn by 2033, growing at a CAGR of 18.6% during the forecast period.

The key demand drivers include acute global labour shortages across healthcare, logistics, and hospitality; the rapid integration of AI and advanced sensing technologies into robot platforms; expanding Robot-as-a-Service (RaaS) deployment models and rising government investments in défense autonomous systems and eldercare robotics in response to aging population demographics.

Transportation and Logistics is the dominant end-use segment, holding approximately ~35% revenue share. The IFR reports that 102,900 units were sold in this segment in 2024 representing more than all other professional service robot segments combined driven by the global e-commerce boom, warehouse labour shortages, and the rapid expansion of automated fulfilment and last-mile delivery infrastructure.

North America is the leading regional market, with the United States home to 199 service and medical robot manufacturers according to the IFR the highest globally. The region benefits from a world-leading AI innovation ecosystem, strong défense autonomous systems procurement, and healthcare robot adoption accelerated by projected shortfalls of over 2 million healthcare workers by 2033 per the U.S. Bureau of Labor Statistics.

Leading companies in the global Service Robotics Market include ABB Ltd (being acquired by SoftBank Group Corp. for US$ 5.375 billion), KUKA AG, iRobot Corporation, SoftBank Robotics Holdings, Kongsberg Maritime AS, Honda Motor Co., Ltd., Daifuku Co., Ltd., ECA Group, and Parrot SA, among other specialized global and regional players.