- Construction & Engineering

- Concrete Block and Brick Manufacturing Market

Concrete Block and Brick Manufacturing Market Size, Share, and Growth Forecast 2026 - 2033

Concrete Block and Brick Manufacturing Market by Product Type (Concrete Blocks: Hollow Blocks, Solid Blocks, AAC Blocks, Paving Blocks, Retaining Wall Blocks; Bricks: Clay Bricks, Fly Ash Bricks, Sand-Lime Bricks, Concrete Bricks, Interlocking Bricks, Facing Bricks), Material Type (Cement, Clay, Fly Ash, Sand-Lime, Aggregates, Additives & Admixtures), Construction Type, by Distribution Channel, End-user, and Regional Analysis, 2026 - 2033

Concrete Block and Brick Manufacturing Market Size and Trend Analysis

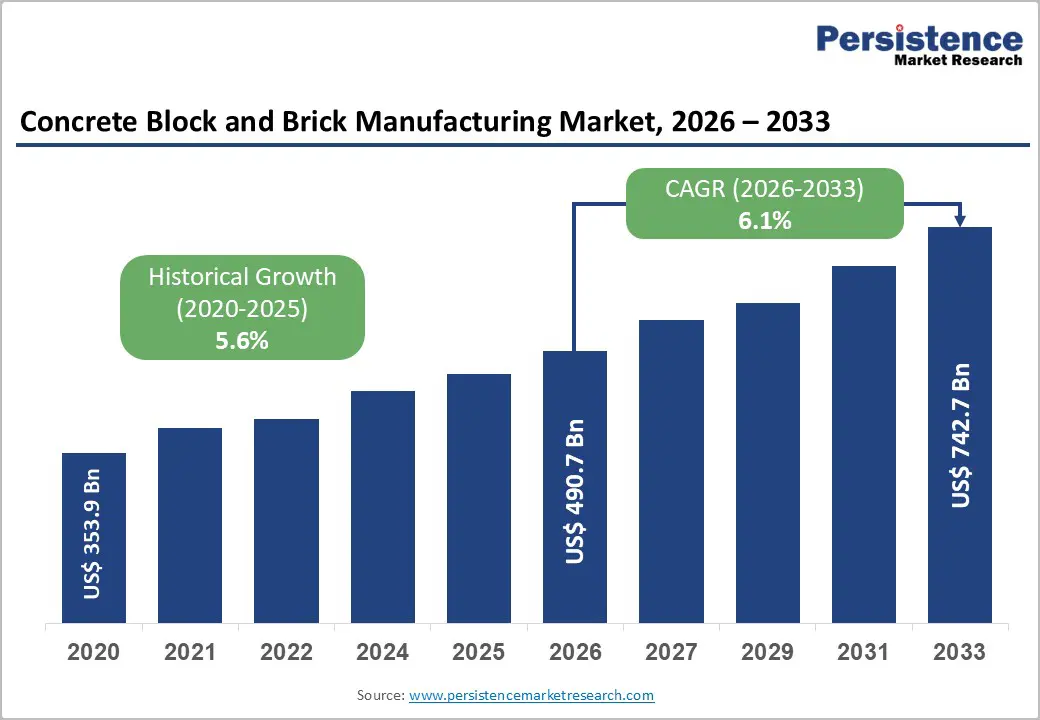

The global concrete block and brick manufacturing market size is likely to be valued at US$ 490.7 Billion in 2026 and is expected to reach US$ 742.7 Billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033.

The market's robust expansion is fundamentally driven by accelerating global urbanisation, large-scale government infrastructure investment programmes, and the growing adoption of sustainable, energy-efficient building materials including Autoclaved Aerated Concrete (AAC) blocks and fly ash bricks as construction industries worldwide pivot toward green-certified and code-compliant building solutions.

Key Market Highlights

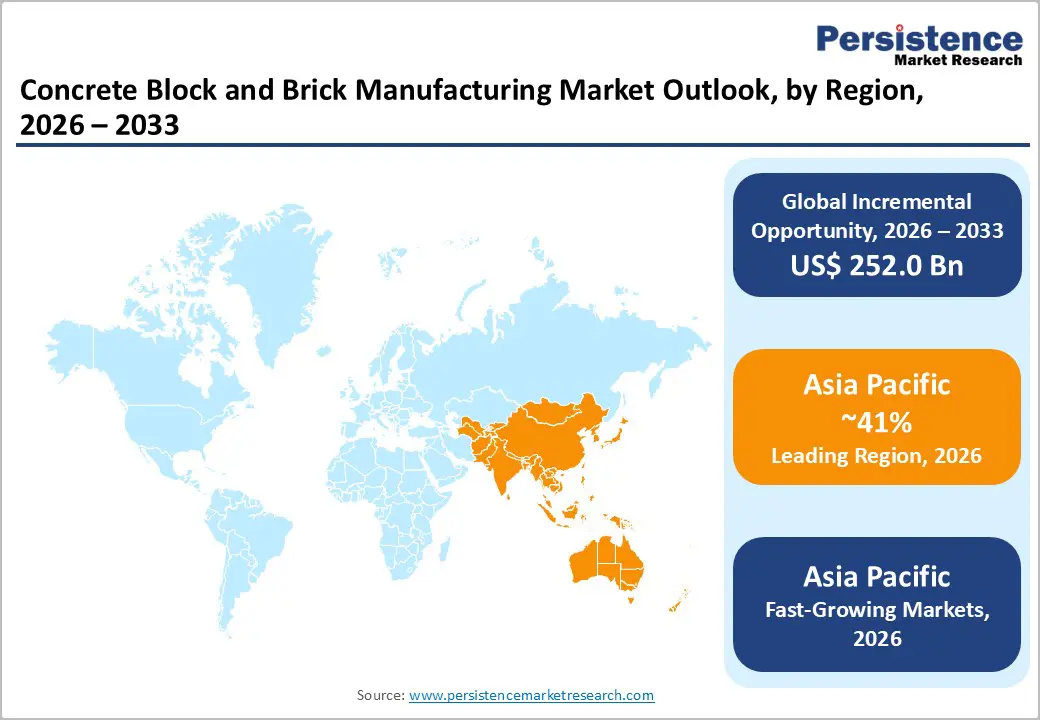

- Leading Region: Asia Pacific leads the global Concrete Block and Brick Manufacturing Market holding 41% share, driven by China's urbanisation of over 300 million rural migrants and India's PMAY housing programme targeting 20 million urban units, generating the world's largest combined masonry product demand base across residential and infrastructure segments.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing regional market with rising CAGR of 7.8%, with ASEAN infrastructure investment programmes in Indonesia, Vietnam, and Thailand, combined with India's National Infrastructure Pipeline (NIP) investment of over INR 111 lakh crore, creating unprecedented multi-year volume demand across all concrete block and brick product categories.

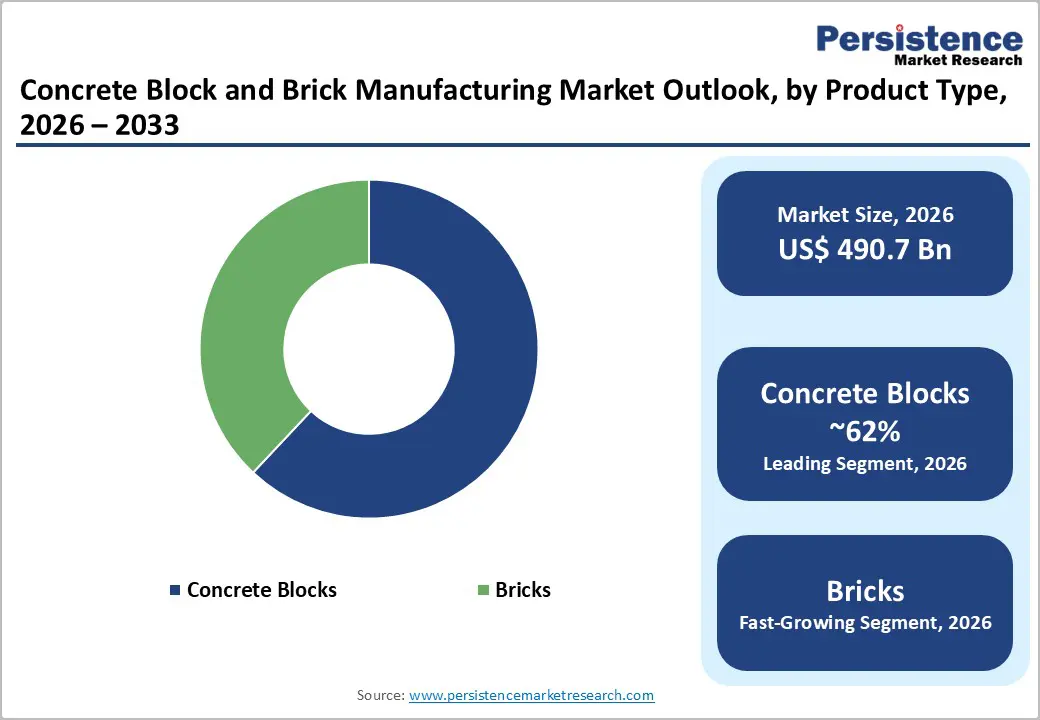

- Leading Segment: Concrete Blocks dominate the product type segment at approximately 62% market share, underpinned by CMU adoption across commercial construction, the Portland Cement Association (PCA)'s endorsement of concrete masonry in institutional buildings, and the rapid growth of AAC blocks as the leading sustainable alternative to conventional clay bricks.

- Fastest-Growing Segment: AAC Blocks represent the fastest-growing product sub-segment, expanding at over 7% CAGR in high-growth markets including India, where fly ash utilization policies and BEE energy efficiency norms are mandating the transition from clay bricks, and across Middle Eastern markets where thermal performance requirements in extreme climates drive AAC specification.

- Key Opportunity: Sustainability-aligned masonry product development represents the key strategic opportunity, as EU EPBD mandates, India's green building codes, and LEED certification requirements globally drive specifier and developer preference toward AAC blocks, fly ash bricks, and insulated CMU systems that command premium pricing and create sustainable competitive differentiation for leading manufacturers.

| Key Insights | Details |

|---|---|

| Concrete Block and Brick Manufacturing Market Size (2026E) | US$ 490.7 Billion |

| Market Value Forecast (2033F) | US$ 742.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.1% |

| Historical Market Growth (2020 - 2025) | 5.6% |

DRO Analysis

Drivers - Rapid Urbanisation and Government-Led Affordable Housing Programmes Driving Structural Demand

Urbanisation is growing rapidly across the world, and according to the United Nations Department of Economic and Social Affairs (UN DESA), around 68% of the global population is expected to live in urban areas by 2050. This shift is creating strong demand for new housing, commercial buildings, and public infrastructure. Governments are supporting this growth through large-scale affordable housing programmes.

India’s Pradhan Mantri Awas Yojana (PMAY) aims to deliver 20 million urban homes, while China continues to invest in public housing and Sponge City projects. These initiatives are directly increasing demand for concrete blocks and bricks, which are essential construction materials. Additionally, the World Bank estimates that developing countries need nearly US$ 1 trillion annually for urban infrastructure through 2030, further strengthening long-term demand for masonry products across residential, commercial, and infrastructure construction projects worldwide.

Surging Infrastructure Investment and Smart City Development Creating Sustained Volume Demand

Global infrastructure investment is rising significantly, supported by economic recovery programmes, climate-focused initiatives, and the rapid development of smart cities. These large-scale projects require high volumes of concrete blocks, paving materials, and structural systems. For instance, the American Society of Civil Engineers (ASCE) highlights the urgent need for major infrastructure upgrades in the United States. Similarly, the European Commission’s €1.8 trillion Recovery and Resilience Facility is funding transportation, water, and urban development projects across Europe.

In Asia, major initiatives such as Indonesia’s Nusantara capital project, India’s National Infrastructure Pipeline (NIP) with investments exceeding INR 111 lakh crore, and Saudi Arabia’s NEOM project are driving massive construction activity. These developments are creating steady and long-term demand for masonry products, as concrete blocks and bricks remain cost-effective, scalable, and reliable materials for building large infrastructure and urban development projects efficiently.

Restraints - Volatile Raw Material Prices and Energy Cost Escalation Compressing Manufacturer Margins

The concrete block and brick manufacturing industry is highly sensitive to changes in raw material and energy costs. Key inputs such as cement, aggregates, clay, and fuel account for nearly 50-65% of total production expenses. Cement prices, in particular, fluctuate due to rising energy costs, as the International Energy Agency (IEA) notes that cement production consumes about 2 exajoules of energy annually. This makes the industry heavily dependent on the prices of coal, natural gas, and electricity.

When these input costs increase, manufacturers face difficult choices: either absorb the costs and reduce profit margins or increase product prices, which may lead to losing customers to competitors. This ongoing cost pressure limits the ability of companies to invest in capacity expansion, adopt new technologies, or improve operational efficiency, ultimately slowing overall market growth and innovation within the industry.

Environmental Regulations and Clay Extraction Restrictions Constraining Traditional Brick Production

Environmental regulations are becoming stricter, creating challenges for traditional clay brick manufacturers, especially in regions like India, China, and Southeast Asia. Brick kilns are known to contribute significantly to air pollution, including particulate matter and greenhouse gas emissions. In India, the Central Pollution Control Board (CPCB) has introduced stricter emission standards, requiring manufacturers to adopt cleaner technologies such as Zigzag kilns. However, many small producers struggle to afford these upgrades.

China’s Ministry of Ecology and Environment has imposed tighter controls on kiln operations and restricted clay extraction in environmentally sensitive areas. These regulations are reducing the availability of raw materials and increasing compliance costs. As a result, traditional brick production is becoming less viable, pushing manufacturers to explore alternative materials and more sustainable production methods to remain competitive in the evolving regulatory environment.

Opportunities - Rapid Adoption of AAC Blocks and Sustainable Building Materials Creating a High-Growth Premium Segment

The growing focus on sustainability and energy efficiency in construction is creating strong opportunities for advanced materials like Autoclaved Aerated Concrete (AAC) blocks. These blocks are lightweight, provide excellent thermal insulation, and offer better fire and sound resistance compared to traditional bricks. Additionally, AAC blocks use fly ash, an industrial waste material, making them environmentally friendly. In India, the AAC blocks market is valued at around US$ 3.11 billion in 2025 and is expected to grow at a CAGR of 7.71% through 2031.

Government policies such as the Fly Ash Utilisation Policy and energy efficiency standards from the Bureau of Energy Efficiency (BEE) are encouraging their adoption. AAC blocks also reduce construction costs by lowering labour and foundation requirements. Manufacturers investing in AAC production can benefit from higher margins and increasing demand across India, Southeast Asia, and the Middle East.

E-Commerce and Digital Distribution Channel Expansion: Opening New Market Access Pathways

The rise of e-commerce and digital platforms is transforming the way construction materials are bought and sold. Increasing internet penetration and digital adoption are enabling contractors, builders, and individual homeowners to purchase materials online more easily. In India, platforms like Amazon Business, Moglix, and OfBusiness are witnessing strong growth in construction material transactions, especially in Tier-2 and Tier-3 cities. This shift creates new opportunities for manufacturers to expand their reach beyond traditional distribution networks.

By adopting digital sales channels or partnering with online marketplaces, companies can reduce dependence on intermediaries, improve profit margins, and gain better control over pricing. Additionally, digital platforms provide valuable customer data, helping manufacturers forecast demand more accurately and improve production planning. This transformation is making supply chains more efficient and opening new growth avenues in the concrete block and brick market.

Category-wise Analysis

Product Type Insights

Concrete blocks lead the product type segment, holding about 62% share in 2025. This leadership is driven by their strong structural versatility, high load-bearing capacity, ease of large-scale manufacturing, and wide use across residential, commercial, and infrastructure projects. Among sub-segments, hollow concrete blocks are the most commonly used, as they provide cost-effective wall construction along with built-in thermal and sound insulation due to their hollow core design.

At the same time, AAC blocks are the fastest-growing segment, supported by rising sustainability regulations and energy efficiency standards across India, China, the Middle East, and Europe. The Portland Cement Association (PCA) in the United States consistently highlights concrete masonry units (CMUs) as the preferred material for structural walls in commercial and institutional buildings, reinforcing the strong and well-established position of concrete blocks within the overall product landscape.

Material Type Insights

Cement remains the leading material type in the concrete block and brick manufacturing market, accounting for around 48% of total material consumption by value. This dominance reflects its essential role as the primary binding agent in concrete block production, which is the largest product segment in the market. According to the Global Cement and Concrete Association (GCCA), global cement production exceeded 4.1 billion tonnes in 2023, with a large share used in manufacturing concrete masonry products for construction.

At the same time, the growing use of supplementary cementitious materials (SCMs) such as fly ash, ground granulated blast furnace slag (GGBS), and silica fume is transforming the segment. These materials partially replace Portland cement clinker, helping manufacturers lower carbon emissions while maintaining product strength and quality, and supporting compliance with green building standards such as LEED and BREEAM.

Construction Type Insights

Residential buildings dominate the construction type segment, contributing around 54% of the total market share. This growth is mainly driven by the ongoing global housing shortage and government-led affordable housing programs in rapidly urbanizing regions. The United Nations Human Settlements Programme (UN-Habitat) estimates that more than 1 billion people worldwide live in inadequate housing conditions, highlighting the urgent need for large-scale residential construction. This creates continuous demand for concrete blocks and bricks as primary building materials.

Government initiatives such as India’s PMAY, China’s Social Housing Programme, and housing schemes in Mexico, Africa, and the Middle East are generating consistent, high-volume demand. These policy-backed projects provide long-term visibility for manufacturers, ensuring stable procurement pipelines and supporting sustained growth in the residential construction segment across both developing and emerging markets.

Distribution Channel Insights

Distributors and wholesalers lead the distribution channel segment, accounting for about 42% of the market share. Their dominance comes from their ability to efficiently connect large-scale manufacturing units with a highly fragmented base of contractors, developers, and construction sites spread across different regions. In emerging markets such as India, Nigeria, and Indonesia, traditional wholesale networks play a critical role through multi-level systems involving regional stockists and local dealers.

These networks not only ensure timely delivery but also provide credit support to small contractors, which direct sales channels often cannot offer at scale. Direct sales, however, remain the second-largest channel, especially for large construction firms and government infrastructure projects that require bulk procurement and standardized product specifications, ensuring cost efficiency and consistency in supply for large-scale developments.

End-user Insights

Construction companies dominate the end-user segment, contributing approximately 38% of total market demand. Large contractors and civil engineering firms purchase concrete blocks and bricks in bulk quantities for use in multi-storey residential, commercial, and infrastructure projects. Their centralized procurement systems allow for better cost management and standardized material usage across projects.

Major construction companies such as Larsen & Toubro (L&T), China State Construction Engineering Corporation (CSCEC), and Saudi Binladin Group generate significant and recurring demand, making them key customers in the supply chain. Real estate developers form the second-largest end-user group, as their demand is directly linked to new residential and commercial project developments. Together, these segments drive consistent market demand and play a crucial role in shaping production volumes and distribution strategies for manufacturers worldwide.

Regional Insights

North America Concrete Block and Brick Manufacturing Trends

North America’s concrete block and brick manufacturing market is defined by high-quality standards, advanced manufacturing technologies, and a well-established regulatory environment. The region consistently sees strong demand from residential construction, with the U.S. Census Bureau reporting around 1.3 to 1.6 million housing starts annually, each creating demand for concrete masonry units, paving blocks, and bricks.

In addition, the Bipartisan Infrastructure Law (BIL), which allocates over USD 1.2 trillion for infrastructure development, is driving long-term demand for construction materials used in transportation, water systems, and public facilities. Canada’s housing demand, supported by population growth and immigration, and Mexico’s affordable housing programs further contribute to regional growth. Industry bodies such as the National Concrete Masonry Association (NCMA) continue to promote the use of CMUs for their durability, fire resistance, and energy efficiency, strengthening their adoption across commercial and institutional construction projects.

Europe Concrete Block and Brick Manufacturing Market Trends

Europe’s market is strongly influenced by sustainability regulations and energy efficiency goals set by the European Union. Policies such as the Energy Performance of Buildings Directive (EPBD) require all new buildings to meet near-zero energy standards by 2030, driving demand for advanced masonry materials such as AAC blocks, sand-lime bricks, and insulated concrete systems. Key countries, including Germany, France, the United Kingdom, and Spain account for a large share of demand, supported by leading manufacturers such as Wienerberger AG and Xella International.

National regulations like Germany’s Building Energy Act and the U.K.’s Future Homes Standard further push the adoption of energy-efficient construction materials. Additionally, initiatives such as the New European Bauhaus promote sustainable and aesthetically appealing building solutions, encouraging the use of premium masonry products, including high-quality facing bricks and innovative concrete block designs.

Asia Pacific Concrete Block and Brick Manufacturing Market Trends

Asia Pacific is the largest regional market, driven by rapid urbanization and large-scale construction activities across countries such as China, India, Vietnam, Indonesia, and Bangladesh. China’s ongoing urbanization plans, which aim to move millions of people into cities, create massive demand for residential and commercial buildings. Similarly, India’s housing initiatives, including PMAY and Smart Cities Mission, are significantly boosting construction activity.

Southeast Asian countries are also investing heavily in infrastructure projects, such as Indonesia’s National Strategic Projects, Vietnam’s infrastructure plans, and Thailand’s Eastern Economic Corridor, all contributing to increased demand for concrete blocks and related products. The region also benefits from cost advantages, including lower labor costs and easy access to raw materials. These factors make Asia Pacific not only the largest consumer market but also a key global manufacturing hub for concrete blocks and bricks.

Competitive Landscape

The global concrete block and brick manufacturing market is highly fragmented, with many local and regional manufacturers competing alongside a smaller number of large multinational companies such as Wienerberger AG, Xella International, CEMEX, Boral, and CRH. Competition in the market is driven by factors such as product quality, certification standards, proximity to construction sites, and the ability to offer a wide product range.

Sustainability is becoming an important differentiator, with companies investing in low-carbon materials and environmentally friendly production methods. Leading players are also focusing on automation to improve efficiency and reduce costs, as well as expanding production capacity in high-growth regions like Asia and Africa. New business models are emerging, including direct digital sales platforms, the use of recycled materials, and modular construction systems, which help companies build stronger customer relationships and reduce competition from substitute products.

Key Developments:

- In February 2025: Wienerberger AG commissioned a new automated brick manufacturing plant in Poland, improving production efficiency and reducing CO2 emissions by 25% per unit. This supports its sustainability roadmap and 2026 carbon reduction goals while strengthening its European production network.

- In September 2024: Xella International introduced its advanced YTONG AAC blocks across Europe, offering improved thermal insulation aligned with EU 2030 NZEB standards. The launch targets rising demand for energy-efficient residential construction and supports stricter building performance regulations.

- In March 2025, UltraTech Cement expanded its ready-mix concrete and block production capacity in India through a INR 32,000 crore investment, focusing on high-growth states. This expansion aims to meet rising demand from residential housing and large-scale infrastructure development projects.

Companies Covered in Concrete Block and Brick Manufacturing Market

- Acme Brick Company

- Bauroc International

- Boral

- Brickworks Limited

- CEMEX, S.A.B. de C.V.

- CRH

- General Shale, Inc.

- Lignacite Ltd

- Midwest Block & Brick

- Mona Precast Ltd

- UltraTech Cement

- Wienerberger AG

- Xella International

- Oldcastle APG

- Kansai Nerolac

- Interblock d.o.o.

- Thermalite

Frequently Asked Questions

The global Concrete Block and Brick Manufacturing Market is valued at US$ 490.7 Billion in 2026 and is projected to reach US$ 742.7 Billion by 2033, expanding at a CAGR of 6.1%, driven by accelerating global urbanisation, government infrastructure investment programmes, affordable housing initiatives, and the growing adoption of sustainable masonry products across all major construction markets worldwide.

Primary demand drivers include the UN DESA-projected urbanisation of 68% of the global population by 2050, national housing programmes such as India's PMAY targeting 20 million units, the European Commission's €1.8 trillion Recovery and Resilience Facility, and India's National Infrastructure Pipeline of over INR 111 lakh crore, collectively generating unprecedented multi-year procurement demand for concrete blocks and bricks across residential, commercial, and infrastructure construction categories.

Concrete Blocks lead with approximately 62% market share, supported by CMU adoption in commercial and institutional construction endorsed by the Portland Cement Association (PCA), the structural versatility of hollow and solid block configurations, and the rapidly growing AAC block sub-segment driven by India's Fly Ash Utilisation Policy and Bureau of Energy Efficiency (BEE) building norms mandating energy-efficient construction materials.

Asia Pacific dominates the global market, driven by China's National New Urbanisation Plan requiring construction for over 300 million rural migrants, India's PMAY and Smart Cities Mission, and ASEAN infrastructure investment programmes across Indonesia, Vietnam, and Thailand, collectively constituting the world's largest and fastest-growing demand base for concrete block and brick manufacturing products.

The primary opportunity lies in the AAC block and sustainable masonry product segment, where regulatory mandates including the EU's Energy Performance of Buildings Directive (EPBD), India's BEE building efficiency codes, and global LEED/BREEAM certification requirements are driving specifier preference toward thermally efficient, low-carbon masonry alternatives, creating a premium, policy-guaranteed demand pathway for manufacturers investing in AAC and fly ash brick production capacity in high-growth emerging markets.

Key players include Wienerberger AG, Xella International, CEMEX S.A.B. de C.V., CRH, Boral, Brickworks Limited, Acme Brick Company, General Shale Inc., UltraTech Cement, Lignacite Ltd, Midwest Block & Brick, Bauroc International, Mona Precast (Anglesey) Ltd, and Oldcastle APG, competing through product quality certifications, sustainability credentials, geographic manufacturing footprint breadth, and digital distribution channel development across global construction markets.