- Construction & Engineering

- Slat Wall Panels Market

Slat Wall Panels Market Size, Share, and Growth Forecast 2026 - 2033

Slat Wall Panels Market by Material Type (MDF, Plastic, Metal, Wood, Others), Application (Specialty Retail, Hardware & Home Improvement, Electronics & Accessories, Grocery & Convenience, Residential & Garage Organization, Others), and Regional Analysis for 2026 - 2033

Slat Wall Panels Market Size and Trend Analysis

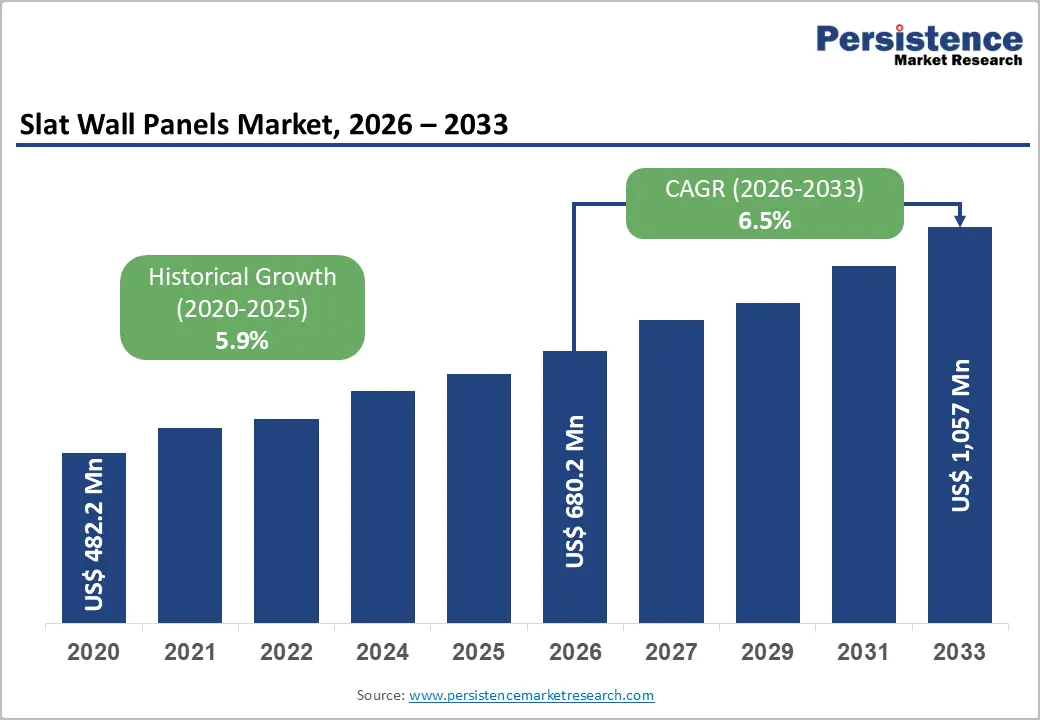

The global slat wall panels market is valued at USD 680.2 million in 2026 and is projected to reach USD 1057 million by 2033, growing at a CAGR of 6.5%.

Market growth is driven by rising investments in organized retail and specialty store expansions, particularly in emerging economies. Increasing demand for flexible and modular display systems has expanded usage beyond retail into residential applications such as garages and home organization. Additionally, the shift toward experiential retail environments in North America and Europe continues to strengthen adoption, as visually appealing and versatile display solutions play a key role in influencing consumer purchasing behavior.

Key Industry Highlights:

- Acoustic Performance Driving Demand: Acoustic slat wall panels are gaining strong traction due to their ability to enhance sound insulation and reduce noise, making them ideal for home offices, gaming rooms, and commercial environments.

- Expanding Multi-Application Usage: Slat wall panels are increasingly used across kitchens, media walls, ceilings, furniture, and retail interiors, showcasing their high versatility and broader adoption across residential and commercial sectors.

- Customizable Aesthetic Design Trends: Growing consumer preference for modular, customizable, and visually appealing interiors, including feature walls, ambient lighting, and hidden storage, is driving demand for innovative slat wall panel designs.

- Retail Infrastructure Expansion: Rapid growth of organized retail globally, with India’s sector expanding at 20-25% annually and U.S. specialty retail exceeding US$ 700 billion, is significantly driving demand for modular slat wall panel display systems.

- Residential Demand Acceleration: Increasing home improvement spending above US$ 500 billion and high garage ownership (70% in the U.S.) are boosting adoption, with the residential segment projected to grow at a CAGR of 9.2% through 2033.

- Raw Material Cost Volatility: Rising costs of MDF, wood, and plastic inputs, which surged 30-40% during 2021 - 2023, are pressuring manufacturer margins and creating pricing challenges, particularly impacting small-scale producers and price-sensitive markets.

- Alternative Display Competition: Growing adoption of gridwalls, pegboards, and digital display systems is intensifying competition, as retailers increasingly invest in technology-driven merchandising, reducing budget allocation for traditional slat wall panels.

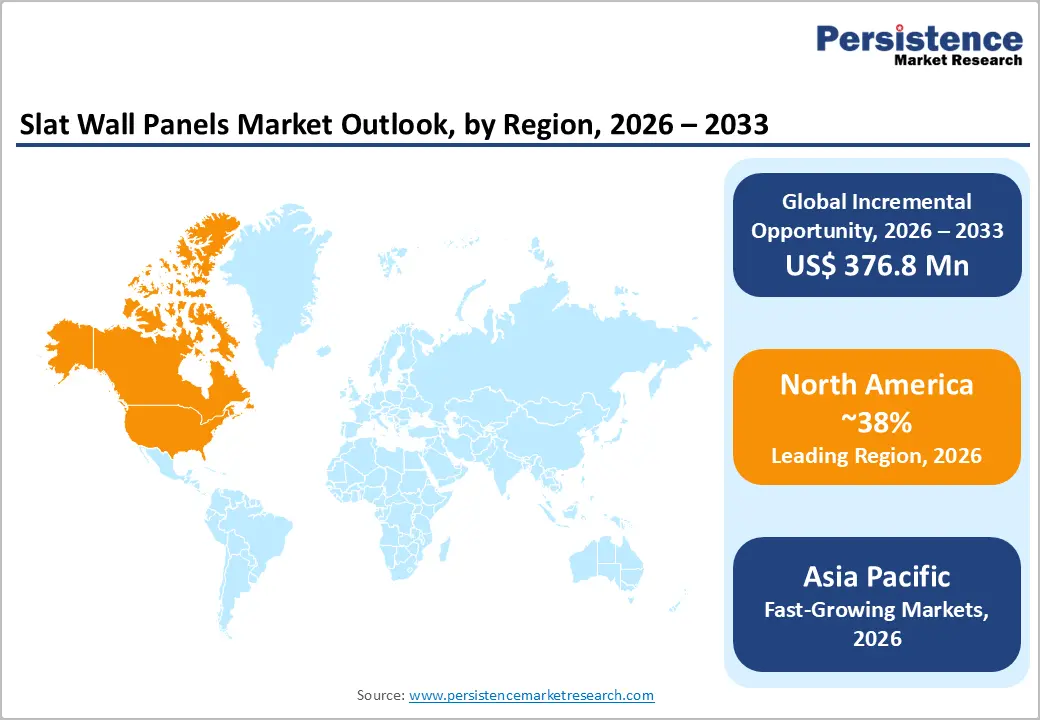

- Regional Growth Dynamics: North America leads with 38% market share, while Asia Pacific is the fastest-growing region at 8.0% CAGR, with India (10.2% CAGR) and China (8.5% CAGR) driving significant market expansion.

Market Dynamics

Drivers - Rapid Expansion of Organized Retail and Specialty Store Formats

The accelerating buildout of organized retail infrastructure worldwide is a pivotal force sustaining demand for retail display systems, including slat wall panels. According to the India Brand Equity Foundation (IBEF), India’s retail sector, one of the fastest-growing globally, is projected to reach US$ 2 trillion by 2032, with modern organized retail growing at nearly 20-25% annually. Similarly, the U.S. Census Bureau reports that specialty retail trade, a primary end-user of slat wall panels, constituted over US$ 700 billion in annual sales as of 2023.

Slat wall panels enable retailers to maximize vertical space, rapidly rearrange product displays, and maintain brand aesthetic with minimal refit costs. As global specialty retail formats, including fashion boutiques, electronics outlets, and health & beauty chains, continue to proliferate in both mature and emerging markets, demand for versatile, high-density modular wall panels in retail environments is expected to remain robust throughout the forecast period.

Growing Residential Adoption for Garage and Home Storage Organization

Beyond commercial applications, residential end-use, particularly garage & storage organization, has emerged as a meaningful growth avenue for slat wall panel manufacturers. The American Housing Survey (AHS) indicates that approximately 70% of U.S. households own a home with a garage, and increasing homeowner investment in functional storage solutions has driven the home improvement segment. The U.S. Bureau of Labor Statistics reported that residential home improvement spending surpassed US$ 500 billion in 2022.

Post-pandemic shifts in the work-from-home culture have further underscored the need for well-organized home spaces, including workshops and hobby areas. Slat wall panels with customizable hook, shelf, and bin attachment configurations are well-positioned to capitalize on this trend. Retail chains like The Home Depot and Lowe’s have expanded dedicated wall-organization product ranges, indicating strong consumer demand momentum across the residential segment.

Restraints - Volatility in Raw Material Costs

Slat wall panel production is materially dependent on wood-derived inputs, particularly Medium Density Fiberboard (MDF) and solid wood, as well as petroleum-based inputs for plastic variants. The Food and Agriculture Organization (FAO) has documented that global timber and wood panel prices experienced upward pressure of over 30-40% during the 2021-2023 period due to supply chain disruptions and elevated energy costs.

Plastic resin prices tracked crude oil volatility during the same period. These input cost fluctuations compress manufacturer margins, particularly for small- and mid-size panel producers with limited ability to forward-contract raw material procurement, resulting in pricing pressure that may dampen adoption in price-sensitive markets.

Intense Competition from Alternative Display Systems

The store fixtures & shopfitting industry presents slat wall panel manufacturers with intensifying competition from alternative in-store display formats, including gridwall panels, pegboards, freestanding gondolas, and digital display fixtures. As retail chains increasingly invest in technology-driven customer experiences, budget allocations can shift away from traditional wall display systems. According to the British Retail Consortium (BRC) annual retail reports, visual merchandising technology adoption among mid-to-large format retailers has risen steadily since 2020, limiting the share of capital expenditure available for conventional panel-based display infrastructure in mature Western markets.

Opportunities - E-Commerce-Driven Physical Retail Reinvention and Omnichannel Stores

The omnichannel retail transformation presents a substantial growth opportunity for slat wall panel manufacturers. The rise of e-commerce has incentivized brick-and-mortar retailers to reimagine physical spaces as experience-centric showrooms and fulfillment hubs. According to the International Council of Shopping Centers (ICSC), physical retail stores that offer an experiential format experience up to 32% higher foot traffic than transactional-only formats. MDF slatwall panels, due to their superior surface finish and paint compatibility, are particularly favored in high-aesthetic concept stores and brand flagship locations.

As brands globally increase investment in concept-store rollouts, the need for high-quality, customizable modular wall panels that can be rapidly reconfigured for seasonal campaigns and promotional events is set to grow significantly through 2033, generating incremental demand across both mature and emerging retail markets.

Sustainability-Led Innovation in Material Technology

The growing imperative for environmental sustainability in construction and retail outfitting presents manufacturers with an opportunity to develop eco-certified, recycled-material slat wall panels. The U.S. Green Building Council (USGBC) reports that the number of LEED-certified commercial interiors projects has grown by over 18% since 2019, directly incentivizing the use of certified sustainable materials in retail fit-outs. Manufacturers incorporating recycled wood fiber, low-VOC coatings, and FSC-certified timber into MDF slatwall panels and composite variants can unlock premium price positioning and preferential procurement from retailers committed to sustainability KPIs.

In Europe, the European Green Deal policy framework is embedding eco-design requirements in retail infrastructure, further elevating the commercial relevance of sustainable slat wall panel alternatives in the EU market.

Category-wise Analysis

Material Type Insights

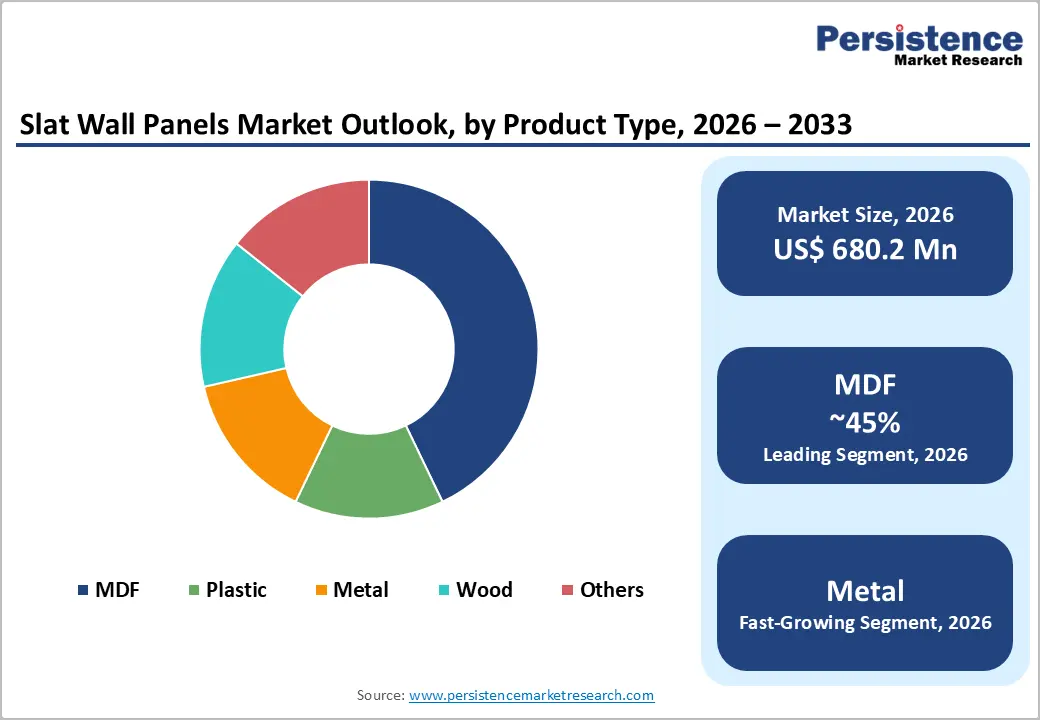

The MDF (Medium Density Fiberboard) segment dominates the Slat Wall Panels market, accounting for approximately 42% of the total market share in 2025. MDF’s dominance is rooted in its cost-effectiveness, machinability, and surface consistency, making it the preferred substrate for routed slatwall profiles across retail and commercial applications. Its ability to accept a variety of finishes including laminates, foils, and paint makes it highly versatile for brand-customized retail environments.

According to the European Panel Federation (EPF), MDF production in Europe alone exceeded 11 million cubic meters in 2022, underscoring deep supply-chain availability. Major retailers and store fixtures & shopfitting contractors preferentially specify MDF-based slatwall panels due to the balance of performance and affordability. Additionally, MDF slatwall is compatible with standard aluminum inserts, enhancing load-bearing capacity for heavier merchandise such as tools and hardware accessories.

Metal is the fastest-growing material category within the slat wall panels market, projected to expand at a CAGR of approximately 8.1% through 2033 well above the overall market forecast rate. Growing adoption of metal slatwall systems in automotive accessories retail, industrial tool displays, and premium home organization is driving volume. Metal panels offer superior durability, moisture resistance, and modern aesthetics increasingly preferred in high-traffic commercial settings and upscale residential garages.

Application Insights

The specialty retail segment is the dominant application for slat wall panels, commanding approximately 31% of total market share. Specialty retail stores including apparel boutiques, sporting goods outlets, beauty supply chains, and hobby stores rely extensively on reconfigurable wall display systems to maximize floor-space efficiency and adapt displays for seasonal merchandise. According to the National Retail Federation (NRF), the United States alone has over 1 million specialty retail establishments, many of which undergo periodic store refreshes requiring updated fixture installations.

The versatility of retail display systems in specialty retail environments, enabling rapid conversion from apparel display to accessory display without structural changes, underpins the segment’s leadership. Slat wall panels also find significant traction in franchise-format specialty retailers seeking cost-efficient, brand-consistent in-store display systems scalable across multiple locations.

The residential & garage organization is the fastest-growing application category, projected to grow at a CAGR of 9.2% through 2033. The surge in DIY home improvement adoption, facilitated by accessible retail channels and instructional digital content, is propelling residential slat wall demand. The segment’s growth trajectory is reinforced by increasing consumer spending on personalized home workshop and hobby spaces, with major home improvement retailers expanding dedicated organization product ranges.

Regional Insights

North America Slat Wall Panels Trends

North America is the leading regional market for slat wall panels, holding approximately 38% of global market share in 2025, driven by a large, mature retail infrastructure base and high consumer spending on home improvement. The United States is the primary market within the region, supported by strong demand from specialty retail chains, hardware stores, and the rapidly expanding residential organization segment.

The U.S. retail sector’s resilience, evidenced by the National Retail Federation (NRF) reporting total annual retail sales exceeding US$ 5.3 trillion in 2023 provides a structural foundation for continued investment in in-store fixtures, including slat wall panel systems. Canada contributes complementarily, with sustained demand from hardware retail chains and ongoing residential renovation activity supported by government housing programs.

- U.S. Slat Wall Panels Market

The United States accounts for approximately 80-85% of the North America slat wall panels market and is expected to maintain this dominance through 2033, growing at a CAGR of approximately 6.1%. The country’s enormous specialty retail base, spanning The Home Depot, Lowe’s, Target, and thousands of independent specialty chains, creates persistent demand for flexible, high-quality display systems.

Residential demand is further amplified by a large suburban homeowner base actively investing in garage & storage organization solutions. Increasing adoption of slat wall panels for utility spaces in multi-family residential construction, driven by real estate developers offering differentiated amenity packages, is an emerging demand channel. The availability of established manufacturing and distribution networks for panel and fixture products across the U.S. supports competitive pricing and widespread accessibility for both commercial and residential buyers.

Europe Slat Wall Panels Trends

Europe holds the second-largest share in the global slat wall panels market, approximately 29%, with sustained demand from organized retail, specialty shopfitting, and growing DIY retail segments across Western and Northern Europe. Germany, the U.K., and France collectively represent the core of European market activity, supported by robust retail infrastructure and high shopfitter demand.

Regulatory harmonization under the European Green Deal and EU Ecodesign Regulation is shaping material procurement practices in the European retail fit-out sector, creating favorable conditions for sustainably certified MDF slatwall panels. Spain and Italy are showing accelerating uptake, particularly in premium retail and boutique hotel shopfitting. The European Shopfitting and Visual Merchandising Association (POPAI Europe) highlights increasing adoption of modular display infrastructure among European mid-market retailers, further supporting slat wall panel demand across the continent.

- Germany Slat Wall Panels Market

Germany accounts for approximately 22% of the European slat wall panels market, growing at a CAGR of approximately 5.8% through 2033. As Europe’s largest economy and home to one of the continent’s most advanced retail sectors, Germany’s dominance is anchored by a dense specialty retail network, a strong DIY home improvement culture exemplified by major chains such as OBI and Bauhaus and a sophisticated manufacturing ecosystem for wood-based panels.

German retailers’ emphasis on store efficiency and modular display systems aligns well with slat wall panel functionality. Additionally, Germany’s strong manufacturing base enables domestic production of premium MDF and wood slatwall panels, contributing to both supply security and export activity across the EU market.

- United Kingdom Slat Wall Panels Market

The United Kingdom holds approximately 18% of the European market share, with a projected CAGR of 6.0% through 2033. The U.K.’s extensive specialty retail sector including major fashion chains, electronics retailers, and independent boutiques represents a significant consumption base for slat wall panel systems.

Post-Brexit adjustments in retail trade have prompted many U.K. retailers to optimize store space efficiency, driving incremental investment in modular retail display systems. The popularity of home improvement programs and residential organization trends has also driven residential slatwall adoption. Major DIY retailers such as B&Q and Wickes actively stock wall organization systems, reflecting sustained consumer demand across the U.K. market.

- France Slat Wall Panels Market

France represents approximately 16% of European market share, expanding at a CAGR of 5.6% through 2033. The French market is characterized by strong demand from fashion retail one of the country’s most commercially significant retail categories alongside growing uptake in the hypermarket and grocery modernization segment.

French regulatory emphasis on sustainable materials procurement aligns with the EU’s broader green construction agenda, benefiting suppliers of certified eco-friendly slat wall panels. Paris’s status as a global fashion retail hub generates consistent demand for premium display solutions in concept stores and flagship boutiques, positioning modular wall panels as a favored specification among interior architects and shopfitters serving high-end retail clients.

- Italy Slat Wall Panels Market

Italy accounts for approximately 14% of the European slat wall panels market and is expected to grow at a CAGR of 6.3% through 2033, making it one of the faster-growing European markets. Italy’s strong furniture and interior fit-out manufacturing tradition provides a competitive advantage in producing premium wood and MDF slat wall panel variants.

Italian specialty retailers in fashion, food, and homewares represent active end-users of slat wall display systems. The booming experiential retail and design-led flagship store culture particularly in Milan and Rome generates elevated demand for aesthetically differentiated store fixtures & shopfitting products, including high-finish slat wall panel configurations.

Asia Pacific Slat Wall Panels Trends

Asia Pacific is the fastest-growing region in the global slat wall panels market, expanding at a projected CAGR of approximately 8.0% through 2033, fueled by the rapid formalization of retail infrastructure across China, India, and Southeast Asia. The region’s accelerating pace of organized retail development, combined with low-cost manufacturing advantages, positions it as both a major demand center and a significant production hub for slat wall panel components.

China’s sprawling retail expansion, India’s ongoing modern trade buildout, and ASEAN countries’ rising consumer spending power are collectively amplifying regional demand for versatile in-store display solutions. The manufacturing cost advantage for wood panels and plastic components across China, Vietnam, and Malaysia also positions the region as a key global supply base for competitively priced slat wall panel products exported to North America and Europe.

- China Slat Wall Panels Market

China represents approximately 40% of the Asia Pacific slat wall panels market, growing at a CAGR of 8.5% through 2033. China’s massive and rapidly evolving retail sector anchored by both domestic consumption growth and global brand store rollouts creates a high-volume demand environment for slat wall panels. According to the National Bureau of Statistics of China, total retail sales of consumer goods in China exceeded CNY 47 trillion in 2023.

Domestic manufacturing of MDF-based and plastic slat wall panels at scale, supported by China’s robust wood panel industry, provides both supply security and competitive export pricing. The China Timber and Wood Products Distribution Association (CTWPDA) reports China produces over 300 million cubic meters of wood-based panels annually, underscoring the country’s foundational role in global slat wall panel supply chains.

- India Slat Wall Panels Market

India accounts for approximately 18% of the Asia Pacific market, with a projected CAGR of 10.2% through 2033, among the highest growth rates of any country in the regional market. India’s rapidly expanding organized retail sector, underpinned by an increasing number of modern trade formats, brand-owned specialty stores, and mall-based retail, is a primary demand driver. According to IBEF, India’s organized retail market is expected to grow at over 20% annually over the next decade. The country’s expanding urban middle class, combined with growing DIY home improvement culture catalyzed by e-commerce-driven product accessibility, is simultaneously creating nascent residential demand for garage & storage organization solutions including slat wall panels.

- South Korea Slat Wall Panels Market

South Korea represents approximately 10% of the Asia Pacific slat wall panels market, growing at a CAGR of 7.2% through 2033. South Korea’s sophisticated retail sector characterized by high-density urban shopping districts, K-beauty specialty retail chains, and technologically advanced flagship stores generates consistent demand for high-quality display fixtures, including slat wall panel systems.

The design-forward retail culture and premium store fitout standards favor aesthetically advanced slat wall configurations. South Korean manufacturers are also active contributors to regional panel supply, leveraging strong wood processing and industrial design capabilities to serve both domestic and export markets.

Competitive Landscape

The global slat wall panels market exhibits a moderately fragmented competitive structure, with a mix of large multinational store fixture manufacturers, specialized slatwall producers, and regional panel fabricators. Market leaders differentiate through product breadth, material customization capabilities, and established relationships with major retail chains and shopfitting contractors.

Key expansion strategies include geographic market entry into high-growth Asia Pacific and Latin American retail markets, acquisition of regional panel manufacturers to consolidate supply chains, and investment in eco-certified product lines aligned with sustainability procurement policies. Emerging business model trends include direct-to-consumer residential sales through e-commerce channels and panel-as-a-service leasing arrangements for pop-up retail formats.

Key Market Developments

- In April 2026, MSI expanded its Acoustic Slat Wall Panel portfolio with eight new designs, including painted panels and larger acoustic wood formats. The development enhances design flexibility, color variety, and acoustic performance, reinforcing the company’s focus on innovation and growing demand for versatile interior panel solutions.

- In 2025, Naturepanel, a sister brand of Multipanel, launched a nature-inspired wall panel collection featuring Bleached Cuneo Oak, Brown Cuneo Oak, and Warmia Walnut, offering a realistic, knot-detailed alternative to traditional wooden slat panels.

- January 2025: Handy Store Fixtures expanded its U.S. e-commerce distribution channel to include direct residential slat wall panel kits targeting garage and home workshop organization consumers, significantly broadening its addressable market beyond commercial retail.

- March 2024: Trion Industries launched an expanded line of aluminum-insert MDF slat wall panels with enhanced weight capacity ratings, targeting hardware and tool specialty retail across North American markets, strengthening its position in the commercial display segment.

- September 2024: D&B Display announced the integration of recycled-content composite slat wall panels into its standard product range, achieving FSC certification for its core slatwall lineup to meet EU Green Deal procurement requirements and expand its European distribution network.

Companies Covered in Slat Wall Panels Market

- Trion Industries

- Handy Store Fixtures

- D&B Display

- Metromax Industries

- Displays2go

- Econoco

- Lozier Corporation

- Madix Inc.

- Marrs Displays

- Retail Resources Inc.

- Southern Imperial

- Tegometall International AG

- Vend-Rite Manufacturing

- Chadwick Metal Products

- Retail Display Solutions Inc.

Frequently Asked Questions

The global Slat Wall Panels market is valued at US$ 680.2 Mn in 2026 and is projected to reach US$ 1057 Mn by 2033, representing a CAGR of 6.5% over the forecast period 2026 - 2033, driven by retail infrastructure expansion and growing residential organization demand.

The primary drivers include the rapid global expansion of organized specialty retail formats requiring flexible modular display systems, as well as surging residential adoption of slat wall panels for garage and home storage organization driven by increased home improvement spending post-pandemic.

MDF (Medium Density Fiberboard) is the dominant material segment with approximately 42% market share in 2025, favored for its cost-effectiveness, surface finish versatility, and compatibility with aluminum insert systems across commercial retail and shopfitting applications globally.

North America leads the global Slat Wall Panels market with approximately 38% market share in 2025, supported by a large specialty retail sector, extensive DIY home improvement spending, and well-established distribution networks for store fixtures and wall organization products.

Key opportunities include the growing adoption of eco-certified and recycled-material slat wall panels aligned with LEED and EU Green Deal sustainability mandates, and the omnichannel retail reinvention trend driving investment in reconfigurable, premium in-store display fixtures for experience-centric retail formats.

Key market players include Trion Industries, Handy Store Fixtures, D&B Display, Lozier Corporation, Madix Inc., Econoco, Southern Imperial, Displays2go, Tegometall International AG, and Metromax Industries, among others operating globally across commercial and residential end-use segments.