- Construction & Engineering

- Commercial Glazing System Market

Commercial Glazing System Market Size, Share, and Growth Forecast 2026 - 2033

Commercial Glazing System Market by Product Type (Curtain Wall Systems, Storefront Systems, Window Wall Systems, Others), Material Type (Aluminum Frames, Steel Frames, uPVC Frames, Wooden Frames, Composite Frames), End-user (Office Buildings, Retail Stores & Shopping Malls, Hotels & Hospitality, Healthcare Facilities, Educational Institutions, Others), and Regional Analysis for 2026 - 2033

Commercial Glazing System Market Size and Trend Analysis

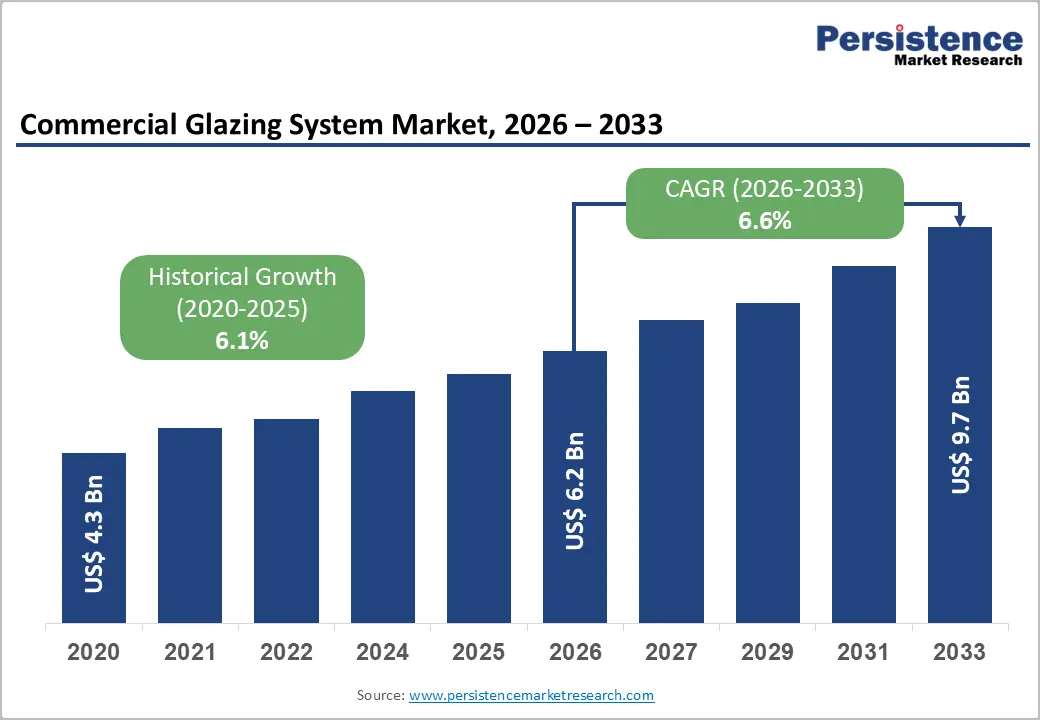

The global commercial glazing system market size is valued at US$ 6.2 billion in 2026 and is projected to reach US$ 9.7 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033. This robust growth is driven by accelerating global commercial construction activity, stringent building energy efficiency regulations mandating high-performance glazing systems, and the rapid adoption of advanced glass technologies, including triple-glazed, low-emissivity (Low-E), and electrochromic units, across office, hospitality, and healthcare building typologies.

The convergence of green building certification demand, urban densification, and commercial real estate investment is structurally sustaining the commercial glazing system market's expansion through 2033.

Key Industry Highlights:

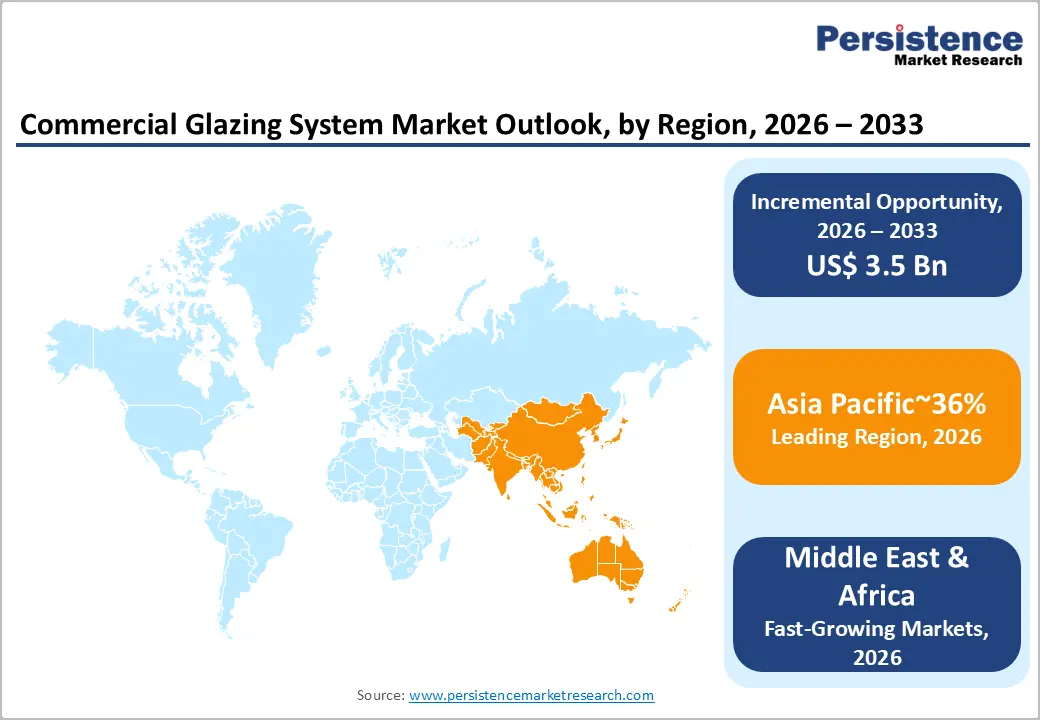

- Leading Region: Asia Pacific leads the global commercial glazing system market, with China commissioning hundreds of millions of square meters of commercial floor space annually, India's National Infrastructure Pipeline allocating over US$ 1.4 trillion for construction, and progressively tightening energy codes elevating glazing specification standards across the region's major economies.

- Fastest Growing Region: Asia Pacific is simultaneously the fastest-growing region, with India's Smart Cities Mission targeting 100 cities, ASEAN's commercial construction boom driven by foreign investment and hospitality sector expansion, and China's Green Building Action Plan mandating Low-E and thermally broken glazing systems in an increasing share of new commercial developments.

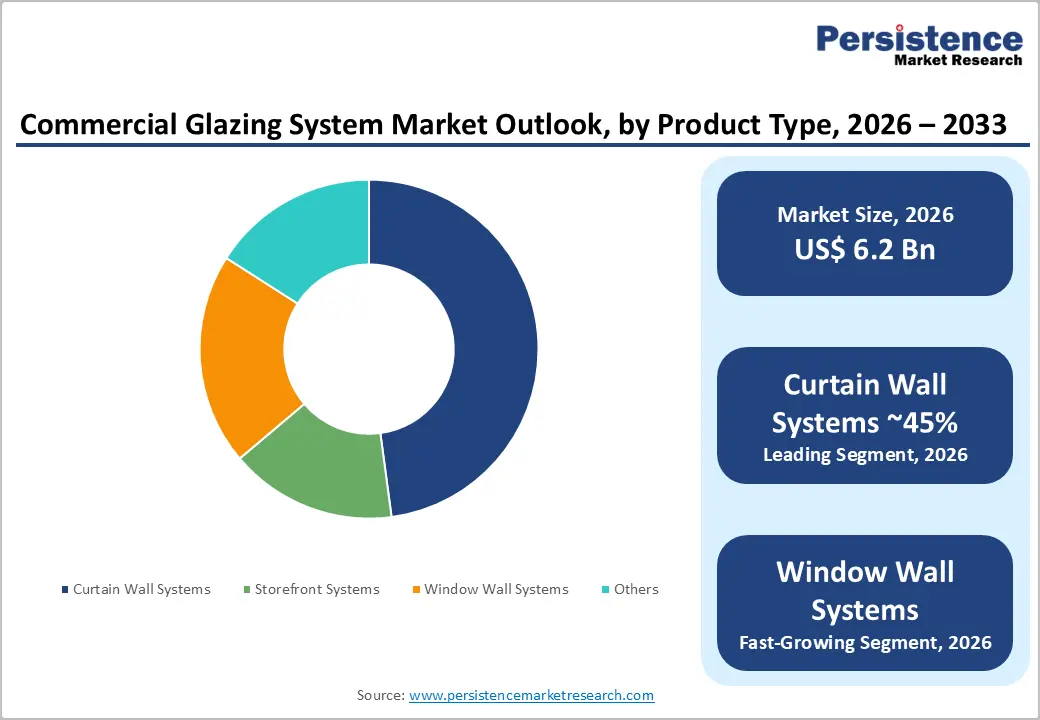

- Dominant Segment: Curtain Wall Systems dominate the product type category with approximately 45% revenue, driven by the Council on Tall Buildings and Urban Habitat (CTBUH) recording record completions of 200-meter-plus buildings globally between 2020 and 2025, with virtually all these projects specifying unitized curtain wall glazing envelopes.

- Fastest Growing Segment: Smart and Electrochromic Glazing within the advanced product type tier is the fastest-growing segment, driven by the EU EPBD 2024 Net Zero Buildings mandate, LEED and BREEAM certification credit frameworks, and landmark deployments by View, Inc. at Apple Park and Google campus buildings, establishing commercial viability and occupant acceptance at scale.

- Key Market Opportunity: The EU's Renovation Wave initiative, targeting deep energy retrofits of 35 million buildings by 2030, combined with the EPBD 2024 zero-emission buildings mandate, creates a multi-billion-dollar commercial glazing replacement opportunity across Europe, favoring suppliers of Low-E, triple-glazed, and electrochromic curtain wall re-cladding systems for aging commercial real estate stock.

DRO Analysis

Drivers - Stringent Building Energy Efficiency Regulations Compelling High-Performance Glazing Adoption

The global regulatory environment for commercial building energy efficiency has become the most powerful structural driver of demand for commercial glazing systems, as increasingly stringent energy codes and green building certification frameworks mandate the deployment of high-performance glazing solutions that minimize building envelope thermal losses. The European Union's revised Energy Performance of Buildings Directive (EPBD 2024), adopted in May 2024, requires all new commercial buildings in EU member states to achieve zero-emission building status by 2030, making high-performance insulating glass units (IGUs) with Low-E coatings, warm-edge spacer bars, and thermally broken aluminum frames a compliance necessity rather than an optional upgrade.

In the United States, ASHRAE Standard 90.1-2022 has progressively tightened fenestration U-value requirements for commercial buildings across all climate zones, thereby increasing demand for triple-pane and Low-E-coated commercial glazing. The U.S. Department of Energy (DOE)'s Building Technologies Office has invested over US$ 200 million in building envelope efficiency R&D programs since 2020, accelerating the commercialization of next-generation advanced glazing systems. These regulatory forces are compelling commercial developers, architects, and building owners globally to specify higher-performance glazing systems as a fundamental project requirement, directly sustaining the commercial glazing market's growth trajectory through 2033.

Global Commercial Construction Boom Driven by Urbanization and Infrastructure Investment

A multi-decade global wave of commercial construction activity, fueled by urbanization, economic development, and government-led infrastructure investment, is the second foundational demand driver for the commercial glazing system market. According to Oxford Economics, global construction output is projected to reach US$ 15.2 trillion by 2030, growing at 3.6% annually, with Asia Pacific and the Middle East contributing the largest incremental output volumes.

Commercial offices, retail, healthcare, and hospitality sectors are all experiencing substantial new construction activity, each requiring large-format curtain walls, storefronts, or window wall glazing systems to complete building envelopes.

The Global Infrastructure Hub (GIH) estimates a US$ 15 trillion global infrastructure investment gap that must be resolved by 2040, with commercial real estate investment and public-sector building programs representing a significant component. In China alone, commercial floor space under construction averaged approximately 2-3 billion square meters annually in recent years, with glazing systems specified in virtually all multi-story commercial building projects.

The U.S. Infrastructure Investment and Jobs Act (IIJA) of 2021 allocated US$ 1.2 trillion for infrastructure development, including public buildings and civic facilities, creating a sustained multi-year construction demand pipeline that directly benefits commercial glazing system suppliers.

Restraints - High Initial Installation Costs and Long Payback Periods Limiting Broad Adoption

The premium pricing of advanced commercial glazing systems, particularly unitized curtain wall systems with Low-E coatings, thermally broken frames, and triple-pane insulating glass units, relative to conventional glazing alternatives, presents a significant barrier to widespread adoption, particularly in cost-sensitive commercial construction markets in Southeast Asia, Africa, and Latin America. Installed costs for unitized curtain wall systems can reach US$80-150 per square foot, compared to US$25-50 per square foot for conventional storefront systems.

While the long-term energy savings and reduced HVAC load justify the investment, typical simple payback periods of 10-20 years create a fundamental misalignment with short-horizon commercial real estate developer economics, particularly for build-to-sell projects where the developer does not occupy the building and therefore does not capture the energy savings benefit. This split-incentive problem systematically impedes the adoption of premium glazing in speculative commercial development.

Aluminum Price Volatility and Supply Chain Disruptions Affecting Production Economics

Aluminum frames represent the dominant material in commercial glazing systems, accounting for approximately 65-70% of frame material consumption by value. The London Metal Exchange (LME) aluminum price has exhibited significant volatility, ranging from approximately US$ 1,400 per ton during the COVID-19 market trough in 2020 to over US$ 3,800 per ton at peak levels in 2021, driven by higher energy costs at aluminum smelters, geopolitical trade disruptions, and constraints on raw bauxite supply.

This raw material price volatility directly impacts glazing system manufacturers' production economics and project cost estimates, making contract pricing and margin management complex for fabricators with fixed-price installation agreements. Supply chain disruptions in glass and specialty coatings, exacerbated by the 2021-2023 global logistics crisis, further introduced lead-time uncertainty, constraining the reliability of commercial glazing system deliveries.

Opportunities - Smart and Electrochromic Glazing: The Transition to Intelligent Building Envelopes

Electrochromic and smart glazing technologies, which dynamically modulate solar heat gain, visible light transmission, and thermal performance in response to electrical signals, daylight levels, or occupant controls, represent one of the most transformational commercial opportunities for advanced glazing system manufacturers over the 2026-2033 forecast period. Smart glass can reduce HVAC energy consumption in commercial buildings by 20-30% according to studies published in the Energy and Buildings journal, while simultaneously improving occupant visual comfort and eliminating the need for interior window blinds or shading devices.

The U.S. DOE's Building Technologies Office has identified dynamic glazing as a priority technology for achieving the net-zero building targets set out in the Biden-Harris Administration's Federal Sustainability Plan, and multiple federal agencies now specify electrochromic glazing for new government building construction.

View, Inc., one of the leading electrochromic glass manufacturers, has deployed its smart windows in major commercial projects, including Apple Park, Boston Logan International Airport, and multiple Google campus buildings, establishing a proof of concept at a significant scale.

The EU's EPBD 2024 Net Zero Buildings mandate and the proliferation of LEED, BREEAM, and WELL Building Standard certifications, each of which awards credits for dynamic glazing deployment, are creating a policy-backed commercial incentive for smart glazing procurement in premium office, healthcare, and hospitality projects globally. Companies that invest early in electrochromic and photovoltaic-integrated glazing platforms will gain access to this high-value, rapidly growing product segment.

Healthcare and Educational Facility Construction: High-Growth End-Use Expansion Opportunity

Healthcare facilities and educational institutions represent two of the fastest-growing and most underserved end-use segments for commercial glazing systems, offering glazing manufacturers and system integrators a strategically important revenue diversification opportunity beyond the dominant office building category. The World Health Organization (WHO) has documented a global shortfall of healthcare infrastructure, particularly in Asia, Africa, and Latin America, that is driving multi-decade hospital and clinic construction programs funded by both governments and multilateral development institutions.

In the United States, the American Institute of Architects (AIA) reported that healthcare construction spending reached over US$ 45 billion in 2023, with modern hospital design emphasizing daylighting through expansive glazed façades, clinical priority given documented evidence that natural light exposure reduces patient recovery times and improves clinical outcomes.

High-performance glazing systems in healthcare facilities must also meet stringent acoustic insulation, thermal comfort, antimicrobial surfaces and blast-resistance specifications, creating demand for premium-specification commercial glazing products. Similarly, the global expansion of educational infrastructure, driven by population growth in South Asia, Sub-Saharan Africa, and ASEAN, and the EU's school renovation wave under the Renovation Wave initiative, is creating sustained procurement pipelines for high-performance storefront and window wall glazing systems. Companies that develop healthcare- and education-specific glazing product certifications and delivery capabilities are well-positioned to capture this growing, premium-specification segment through 2033.

Category-wise Analysis

Product Type Insights

Curtain Wall Systems dominate the product type category, accounting for approximately 45% of total global Commercial Glazing System market revenue. Curtain wall systems, which are non-structural, exterior building cladding systems that hang from the primary structural frame and accommodate floor-to-floor glass and frame panel assemblies, are the defining glazing solution for multi-story commercial towers, corporate headquarters, landmark civic buildings, and premium hospitality facilities. Their dominance reflects the global concentration of commercial construction investment in high-rise office and mixed-use developments across Asia Pacific, North America, and the Middle East, where curtain wall systems are specified for virtually every building exceeding 10 stories.

The Council on Tall Buildings and Urban Habitat (CTBUH) reported that a record number of 200-meter-plus buildings were completed globally between 2020 and 2025, with curtain wall glazing systems installed on essentially all of these projects. Unitized curtain wall systems, pre-fabricated in factory-controlled conditions and crane-lifted into position on-site, have emerged as the preferred delivery method for high-rise projects given their installation speed, quality consistency, and reduced on-site labor requirements, sustaining premium demand for curtain wall systems from leading suppliers including Schüco, Kawneer, and Oldcastle BuildingEnvelope.

Material Type Insights

Aluminum Frames dominate the material type category, commanding approximately 65% of the total global Commercial Glazing System market revenue. Aluminum's structural versatility, light weight, approximately one-third the density of steel, excellent corrosion resistance, design flexibility, and recyclability make it the universal framing material of choice for commercial curtain wall, storefront, and window wall applications globally. Modern thermally broken aluminum frame profiles, featuring polyamide thermal break inserts that interrupt the aluminum's conductive heat flow path, deliver the structural performance of aluminum while meeting the thermal insulation requirements of ASHRAE 90.1 and EU EPBD energy codes.

The Aluminum Association and European Aluminium industry bodies confirm that architectural aluminum extrusions represent one of the fastest-growing end-use applications for aluminum, driven directly by commercial building construction activity, with North America and Europe consuming millions of tonss of thermally broken extrusions annually. Leading aluminum frame fabricators including Schüco International, Kawneer, and Arconic Corporation serve the global market with comprehensive thermally broken and structural glazing frame system portfolios.

End-user Insights

Office buildings are the dominant end-use segment, accounting for approximately 38% of the total global commercial glazing system market revenue. The office building sector is the largest and most consistent driver of global commercial glazing system demand, reflecting the near-universal specification of glazed curtain wall, storefront, and window wall systems in new commercial office construction across every major urban market.

Demand is sustained by two parallel investment streams: new office tower construction in rapidly urbanizing Asia Pacific and Middle East markets, and the extensive retrofitting and re-cladding of aging commercial office stock in North America and Europe to meet updated energy codes and sustainability certification requirements.

The CBRE Global Investors annual office market report identifies a growing bifurcation in global office markets between premium "flight-to-quality" buildings, which feature full-height glazed façades and LEED or BREEAM-certified envelope performance, and commodity office space, with tenants increasingly concentrating leasing demand in premium-specification glazed buildings that support employee wellbeing and corporate sustainability commitments. This flight-to-quality trend directly amplifies demand for high-performance commercial glazing systems in office-sector retrofit and new-build projects globally.

Regional Analysis

North America Commercial Glazing System Trends & Insights

The United States is the world's largest single-country commercial glazing system market, underpinned by one of the global's most active commercial construction sectors, a comprehensive and progressively tightening building energy code infrastructure, and a well-established glazing manufacturing and distribution ecosystem. ASHRAE Standard 90.1-2022, the most widely adopted commercial building energy code in the U.S., mandates progressively lower fenestration U-values and solar heat gain coefficients (SHGC) across all climate zones, compelling commercial developers and building owners to invest in high-performance Low-E, triple-glazed, and thermally broken framing systems.

The Green Building Initiative (GBI) and U.S. Green Building Council (USGBC's LEED v4.1) certification frameworks are compelling commercial developers in major metro markets, particularly New York, Chicago, Los Angeles, and Boston, to specify premium glazing systems to earn LEED credits for energy performance and daylighting.

Canada contributes through commercial construction in Toronto, Vancouver, and Calgary, with the National Energy Code of Canada for Buildings (NECB 2020) mandating high-performance glazing envelope specifications. Apogee Enterprises, Viracon, and Oldcastle BuildingEnvelope are among the most influential commercial glazing system suppliers in the North American market, collectively serving the full project spectrum from storefront to unitized curtain wall installations. North America is expected to maintain its position as the world's second-largest commercial glazing market through 2033, with sustained investment in commercial office, healthcare, and educational building sectors providing a durable demand foundation.

Europe Commercial Glazing System Trends & Insights

Europe is the world's most regulatory-advanced commercial glazing market, characterized by the most stringent building energy performance standards globally and a deep heritage of architectural glazing innovation, particularly in the Netherlands, Germany, France, and the United Kingdom. The European Union's revised EPBD 2024, mandating all new commercial buildings to meet zero-emission standards by 2030, represents the most consequential near-term policy driver for premium commercial glazing system demand across all 27 EU member states.

The Renovation Wave initiative, targeting the deep energy retrofit of at least 35 million buildings across the EU by 2030, is generating unprecedented demand for curtain wall and window wall replacement projects on aging commercial stock, with Germany and France representing the largest renovation glazing markets.

The United Kingdom has adopted the Future Buildings Standard and progressively updated Part L of the Building Regulations, mandating commercially significant improvements to the performance of commercial building fabric that are driving glazing system upgrades across the country's large commercial property stock. Spain and France are investing heavily in zero-carbon commercial building programs under their respective National Energy and Climate Plans, each citing glazing performance as a key lever for achieving building-sector decarbonization targets.

Asia Pacific Commercial Glazing System Trends & Insights

Asia Pacific dominates the commercial glazing system market, accounting for nearly 36% of the market, driven by the unprecedented scale of commercial construction activity in China, India, Southeast Asia, and Australia, combined with rapidly modernizing building energy codes that are progressively mandating higher-performance glazing specifications. China, the world's largest single construction market, has been commissioning several hundred million square meters of commercial floor space annually, generating the highest absolute volume of demand for curtain wall and storefront glazing systems globally.

The Chinese government's Green Building Action Plan and the mandatory GB 50189 energy efficiency standard for commercial buildings have driven the adoption of Low-E insulating glass units and thermally broken aluminum frames in an increasing proportion of new commercial developments, particularly in Tier 1 and Tier 2 cities. AGC Inc., Guardian Industries, and Saint-Gobain all operate significant glass manufacturing facilities in China to serve this demand.

India is the region's fastest-growing individual national market, supported by the government's Smart Cities Mission, covering 100 cities, and the National Infrastructure Pipeline (NIP), which has allocated over US$ 1.4 trillion for infrastructure development through 2025, including large-scale commercial building construction in Mumbai, Bengaluru, Hyderabad, and Delhi NCR.

The Bureau of Energy Efficiency (BEE) has progressively updated India's Energy Conservation Building Code (ECBC) and its commercial sector equivalent, incorporating fenestration performance thresholds that are elevating glazing specification requirements for new commercial projects. ASEAN nations, particularly Singapore, Vietnam, Indonesia, and Malaysia, are experiencing robust commercial construction activity driven by foreign direct investment, manufacturing sector expansion, and hospitality infrastructure development, creating growing demand for international-specification commercial glazing systems from both local and imported suppliers.

Competitive Landscape

The global commercial glazing system market exhibits a moderately consolidated competitive structure at the top tier, with a small number of globally integrated glass manufacturers and system suppliers, including Saint-Gobain, AGC Inc., Guardian Industries, Schüco International, and Oldcastle BuildingEnvelope, commanding significant market influence through vertically integrated glass production, coating technology, and system fabrication capabilities. Mid-tier competition is fragmented across regional glazing fabricators, system integrators, and specialized curtain wall contractors.

Key competitive differentiators include proprietary glass coating technologies (Low-E, solar control, self-cleaning), thermally broken frame system performance ratings, BIM software integration for design and specification, and project engineering and installation support capabilities. Emerging competitive models include façade-as-a-service offerings, performance-guaranteed energy retrofit contracting, and integrated Building Integrated Photovoltaic (BIPV) glazing system packages targeting net-zero building certifications.

Key Developments:

- In 2025, Schüco International KG launched its SchüCal® 6.0 BIM object library and digital façade configurator platform, enabling architects and developers globally to design, specify, and generate compliant energy performance documentation for curtain wall and façade systems in real time, reducing project design cycle times.

- In May 2024, Saint-Gobain announced the launch of its next-generation SGG COOL-LITE XTREME solar control glazing range, featuring advanced magnetron sputtered coatings achieving a light-to-solar-gain ratio of up to 3.0, targeting premium commercial curtain wall and façade applications in high solar irradiance markets.

- In 2024, AGC Inc. expanded its Stopray solar control glass production capacity at its Osterweddingen, Germany float glass facility, investing in additional coating line capacity to meet growing European demand for triple-silver Low-E coated commercial glazing products under the EU EPBD zero-emission building mandate.

Companies Covered in Commercial Glazing System Market

- Saint-Gobain

- Guardian Industries

- AGC Inc.

- Schüco International KG

- Kawneer

- Oldcastle BuildingEnvelope

- EFCO Corporation

- YKK AP America Inc.

- Viracon

- Trulite Glass & Aluminum Solutions

- W&W Glass

- Apogee Enterprises, Inc.

- Pilkington

- Arconic Corporation

- Chase Industries, Inc.

Frequently Asked Questions

The global Commercial Glazing System market is valued at US$ 6.2 Bn in 2026 and is projected to reach US$ 9.7 Bn by 2033, growing at a CAGR of 6.6% during the forecast period.

The primary drivers are, stringent building energy efficiency regulations, including the EU's EPBD 2024 Net Zero Buildings mandate and U.S. ASHRAE 90.1-2022, compelling high-performance glazing adoption; and the global commercial construction boom, with Oxford Economics projecting global construction output to reach US$ 15.2 trillion by 2030, driven by the U.S. IIJA's US$ 1.2 trillion infrastructure investment and Asia Pacific urbanization programs.

Curtain Wall Systems lead the Product Type category with approximately 45% of global market revenue, driven by record-breaking high-rise commercial construction globally, with the CTBUH reporting record completions of 200-meter-plus buildings between 2020-2025, and the near-universal specification of unitized curtain wall glazing systems in premium office towers and commercial landmarks by architects and developers worldwide.

Asia Pacific leads the global commercial glazing system market, driven by China's scale of commercial construction, several hundred million square meters of floor space commissioned annually, India's over US$ 1.4 trillion National Infrastructure Pipeline, and the Smart Cities Mission targeting 100 cities. Rapidly modernizing energy codes including China's GB 50189 and India's ECBC are progressively elevating commercial glazing specification standards across the region.

The most significant opportunity is the EU's Renovation Wave initiative, targeting deep energy retrofits of 35 million buildings by 2030 under the EPBD 2024 Zero-Emission Buildings mandate, creating a multi-billion-dollar curtain wall and window wall re-cladding demand across Europe's aging commercial building stock, favoring suppliers of Low-E, triple-glazed, and electrochromic smart glazing systems with certified energy performance documentation.

The global commercial glazing system market is led by Saint-Gobain, AGC Inc., Guardian Industries, Schüco International KG, Kawneer (Arconic), Oldcastle BuildingEnvelope, Pilkington (NSG Group), Apogee Enterprises, YKK AP America Inc., Viracon, EFCO Corporation, Trulite Glass & Aluminum Solutions, W&W Glass, Arconic Corporation, Chase Industries, and View, Inc., among others.