- Construction & Engineering

- Control Tower Market

Control Tower Market Size, Share, and Growth Forecast 2026 - 2033

Control Tower Market by Product Type (Commercial, Operational), Application (Supply Chain, Transportation), End User (Aerospace & Défense, Chemicals, Retail & Consumer Goods, Healthcare, Manufacturing, High Technology Products, Others), and Regional Analysis for 2026 - 2033

Control Tower Market Size and Trend Analysis

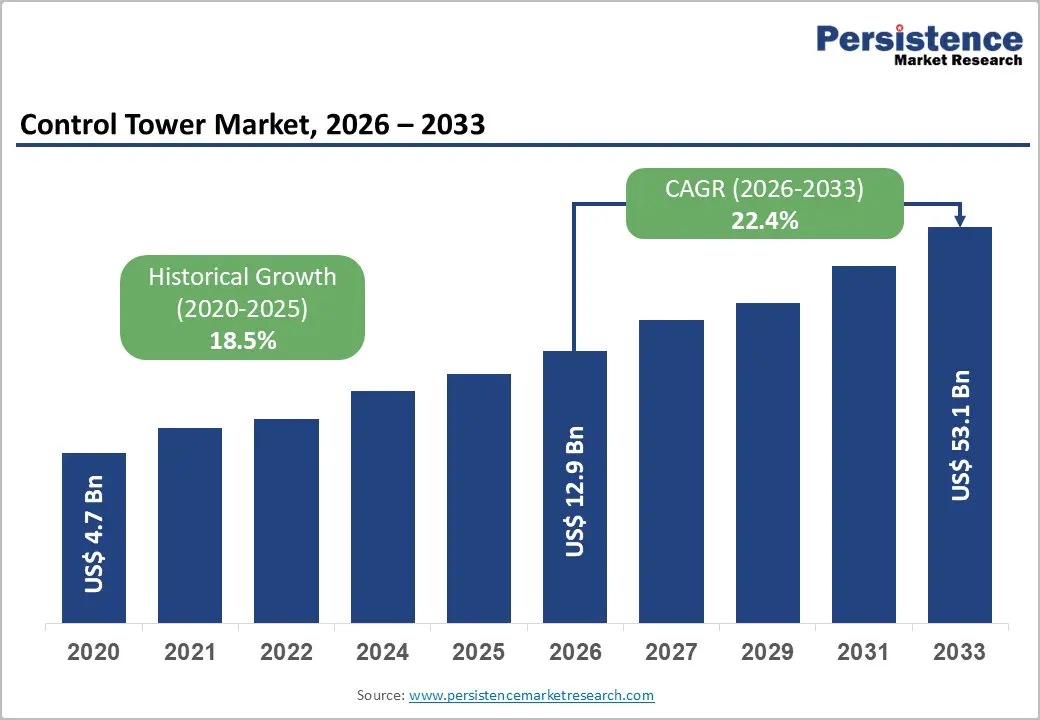

The global control tower market is valued at US$ 12.9 billion in 2026 and is projected to reach US$ 53.1 billion by 2033, growing at a CAGR of 22.4% between 2026 and 2033.

This exceptional growth trajectory is driven by enterprises' urgent need for real-time, end-to-end supply chain visibility amid compounding geopolitical disruptions, persistent logistics volatility, and accelerating digital transformation mandates. The integration of Artificial Intelligence (AI), machine learning, IoT sensors, and digital twin simulation into control tower platforms has elevated them from passive monitoring dashboards into autonomous, prescriptive orchestration engines, making them indispensable for organizations managing complex, multi-enterprise supply chains.

Key Industry Highlights:

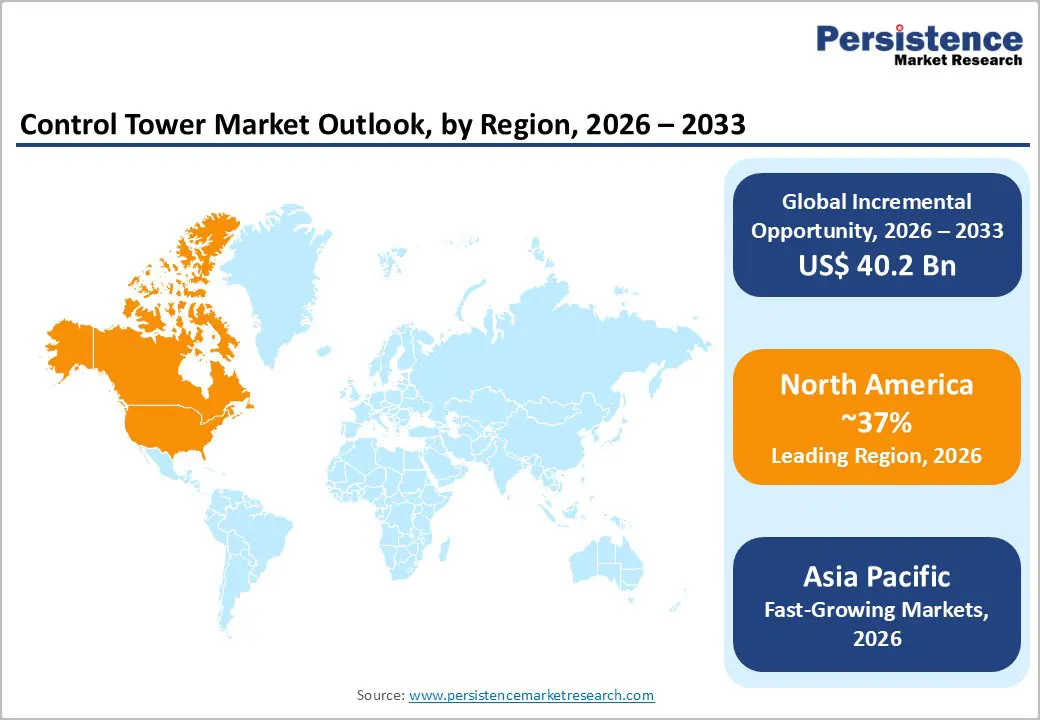

- Leading Region - North America leads the global Control Tower market with approximately 37% revenue share, driven by the U.S. concentration of leading platform vendors, including Blue Yonder, Kinaxis, E2open, high enterprise IT sophistication, and strong manufacturing and retail adoption.

- Fastest Growing Region - Asia Pacific is the fastest growing region, capturing over 28% of global revenue in 2024, driven by China's Made in China 2025 digitalization, India's PLI manufacturing expansion, and ASEAN greenfield supply chain deployments.

- Dominant Product Segment - The operational segment dominates with approximately 83% market share, preferred by enterprises for its dual role in real-time exception detection and active corrective intervention, further enhanced by AI and IoT integration.

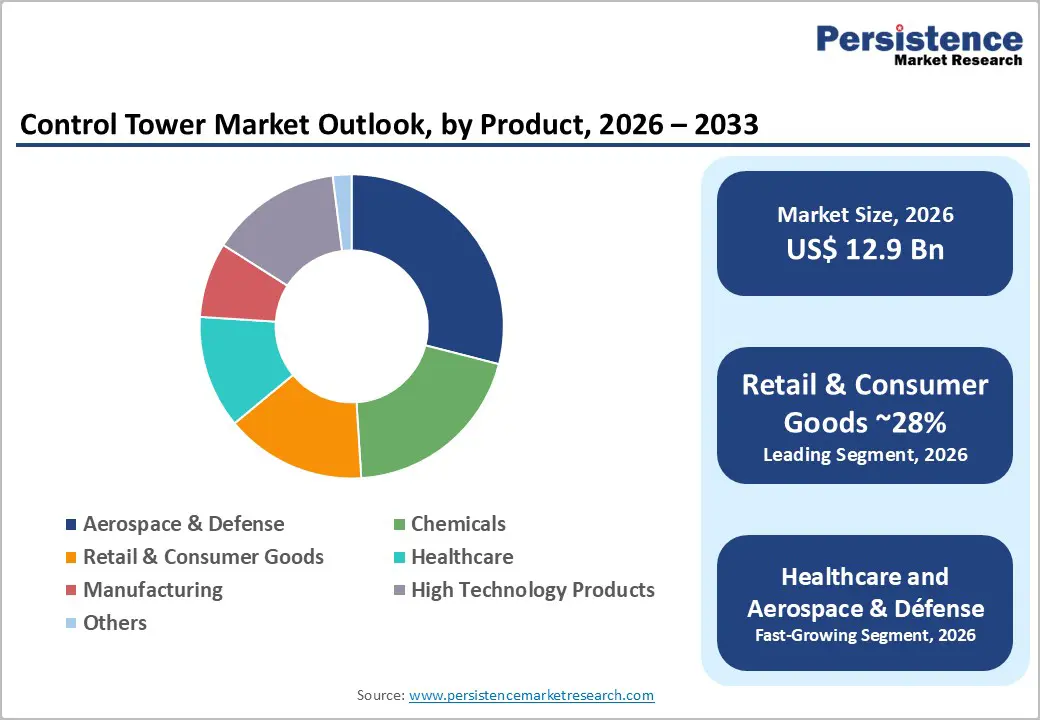

- Fastest Growing Segment - Healthcare is the fastest growing end-user vertical, driven by DSCSA and EU FMD drug traceability mandates, cold-chain compliance requirements, and post-pandemic investment in pharmaceutical supply chain resilience platforms.

- Key Opportunity - The transition to Control Tower as-a-Service (CTaaS) and AI-autonomous orchestration, where platforms like Blue Yonder Cognitive Solutions resolve disruptions in minutes, creates recurring, high-margin subscription revenue for platform providers across all geographies.

| Key Insights | Details |

|---|---|

| Control Tower Market Size (2026E) | US$ 12.9 Bn |

| Market Value Forecast (2033F) | US$ 53.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 22.4% |

| Historical Market Growth (2020 - 2025) | 18.5% |

DRO Analysis

Drivers - Post-Pandemic Supply Chain Resilience Imperative and Geopolitical Disruption Driving Widespread Adoption

The repeated exposure of global supply chains to severe disruptions from the COVID-19 pandemic, the Red Sea shipping crisis, and semiconductor shortages has created a structural demand for real-time orchestration platforms. Automotive manufacturers faced input cost inflation of 15% in 2024 due to raw material price spikes and component shortages, prompting mass adoption of predictive analytics platforms that model disruption scenarios before they materialize.

Control towers that integrate IoT sensors, AI-driven exception management, and scenario modeling enable organizations to reduce reaction times from days to minutes. In 2023, global enterprises processed over 720 million shipping events and 14 billion data transactions annually through control tower platforms, a 28% increase over 2021, demonstrating the rapid scaling of adoption across manufacturing, retail, and logistics sectors worldwide.

AI and Digital Twin Integration: Transforming Control Towers into Autonomous Decision-Making Engines

The rapid integration of Artificial Intelligence (AI), machine learning, and digital twin simulation is fundamentally redefining control tower capabilities, shifting them from reactive visibility tools to proactive, prescriptive orchestration platforms. In 2023-2024, over 190 new modules and features were launched across global control tower solutions, with 80% of recent updates incorporating AI or machine learning components.

Real-time dynamic rerouting, capable of recalculating logistics routes within 60 seconds of a disruption, became a standard feature deployed in 62% of control towers globally. Blue Yonder launched its Cognitive Solutions platform in May 2025, built on a cloud-native design and AI data cloud with its proprietary SADA Loop (See, Analyze, Decide, Act) AI model, reducing disruption response times from days or weeks to minutes. Kinaxis also launched Rapid Response NextGen, with integrated digital twins and autonomous decision-making capabilities, in January 2024.

Restraints - High Implementation Cost and Data Integration Complexity Limiting SME Adoption

Enterprise control tower deployments represent a substantial financial commitment that remains prohibitive for many small and medium-sized enterprises. Implementation costs typically range from US$ 2 million to US$ 15 million per deployment, with up to 60% of that budget dedicated to cleansing and harmonizing data from incompatible ERP, WMS, and supplier-portal systems.

Johnson Controls' control tower initiative, which linked 14 manufacturing sites and 800 suppliers, illustrates the scale and spending required even for mid-tier implementations. For SMEs, these outlays can represent 3-5% of annual revenue, widening the digital divide within the control tower ecosystem and creating a significant barrier to broad market penetration.

Cybersecurity Vulnerabilities in Interconnected Supply Chain Networks

As control towers aggregate sensitive operational data across multi-enterprise networks, including supplier financial data, inventory positions, and logistics routes, they become high-value targets for cyberattacks. The logistics sector recorded 27 significant cyber incidents between July 2023 and July 2024, and cybersecurity software expenditure in the sector is projected to grow from US$ 8.4 Bn in 2024 to US$ 36.6 Bn by 2037.

Supply chain control towers that lack robust data encryption, access controls, and cybersecurity governance expose organizations to operational disruption, regulatory penalties, and reputational damage, creating hesitancy, particularly among regulated verticals such as healthcare and aerospace.

Opportunities - Healthcare and Life Sciences: Cold-Chain Compliance and Drug Supply Traceability as High-Growth Verticals

The healthcare and life sciences sector is among the fastest-growing and highest-value verticals for control tower adoption, driven by regulatory mandates for cold-chain integrity, pharmaceutical traceability, and real-time monitoring of critical medical supplies. Global drug serialization regulations, including the U.S. Drug Supply Chain Security Act (DSCSA) and EU Falsified Medicines Directive (FMD)require end-to-end product traceability that is inherently dependent on control tower-class visibility platforms.

The COVID-19 pandemic exposed catastrophic vulnerabilities in global pharmaceutical supply chains, accelerating investment in resilience-oriented control towers. Hospitals and health systems are also deploying operational control towers to manage medical device inventory, optimize procurement across decentralized networks, and ensure an uninterrupted supply of critical care products. More than 480 new investments were made in control tower platforms across healthcare and adjacent sectors between 2023 and 2024.

Aerospace & Défense and High-Technology Manufacturing: Multi-Tier Supplier Risk Management Opportunity

Aerospace, defense, and high-technology product manufacturers operate within the most complex multi-tier supplier networks globally, making them an exceptional fit for advanced control tower platforms with predictive supplier risk, component traceability, and regulatory compliance capabilities. The semiconductor shortage of 2020-2024 demonstrated how single-tier disruptions can propagate across entire production ecosystems, motivating OEMs, defense primes, and electronics manufacturers to invest in multi-tier control tower platforms that monitor sub-tier supplier health and component availability in real time.

A Q-CTRL collaboration with Airbus and BMW on quantum-optimized route planning illustrates how cutting-edge technologies are being integrated into control tower platforms for these complex sectors. As defense procurement agencies globally increase digital supply chain requirements, the Aerospace & Défense end-user segment is positioned to record one of the highest CAGRs within the control tower market through 2033.

Category-wise Analysis

Product Type Insights

The operational segment is the dominant product type in the Control Tower market, accounting for approximately 83% of total market revenue. Operational control towers serve a dual purpose of real-time monitoring and active intervention, detecting exceptions, notifying authorized operators, and enabling immediate corrective action across logistics, inventory, procurement, and production workflows.

Their growing integration with AI, machine learning, and IoT sensors has transformed them into predictive and prescriptive orchestration platforms that proactively identify bottlenecks before they escalate into disruptions. The segment's dominance reflects enterprise preference for platforms that deliver both visibility and actionable intelligence within a single, unified architecture. In contrast, the Commercial segment is growing rapidly, driven by demand from mid-market enterprises seeking commercially available, cloud-deployable control tower software with faster time-to-value and lower implementation overhead.

Application Insights

The supply chain application dominates the control tower market, accounting for approximately 65% of total application revenue in 2025. Supply chain control towers address the full spectrum of enterprise logistics and operations challenges, including inventory visibility, supplier collaboration, transportation status, demand forecasting, and order management across multi-enterprise networks spanning dozens of countries and thousands of nodes.

The average control tower in 2023 managed visibility over 1.2 million stock-keeping units (SKUs) and monitored 5,800 daily orders, with 88% deploying exception management alerts for delays or disruptions. The Transportation application sub-segment is growing rapidly, fueled by the explosion of e-commerce, the complexity of last-mile logistics, and the growing adoption of real-time transport visibility platforms by logistics service providers and fleet operators.

End-user Insights

The retail & consumer goods is the leading end-user vertical in the control tower market, accounting for approximately 28% of total end-user revenue in 2025. This leadership is driven by omnichannel retail complexity, rapid SKU proliferation, and intense consumer pressure for real-time order status and fast fulfillment. The surge in global e-commerce, which crossed US$ 6 trillion in global retail sales in 2024 per data from the International Trade Center, has forced retailers to deploy end-to-end visibility platforms to synchronize inventory across warehouses, stores, and logistics partners.

The Manufacturing segment is the second-largest vertical, while Healthcare and Aerospace & Défense are the fastest-growing end-user categories, each driven by stringent compliance requirements, complex multi-tier supplier networks, and increasing regulatory mandates for supply chain traceability and resilience.

Regional Analysis

North America Control Tower Market

North America is the dominant regional market for control tower solutions, accounting for approximately 37% of global revenue in 2025. The United States is the single largest market, driven by the concentration of leading control tower solution providers, including Blue Yonder Group, E2open, Kinaxis, Llama Soft, and One Network Enterprises, and by the region's high supply chain sophistication across retail, manufacturing, and technology sectors.

North America's innovation ecosystem, anchored by Silicon Valley's technology infrastructure and enterprise software clusters in Atlanta, Chicago, and Toronto, continues to define global control tower R&D direction. Blue Yoder’s May 2025 launch of Cognitive Solutions and AI agents for Inventory Ops, Shelf Ops, and Logistics Ops was developed primarily from its Scottsdale, Arizona headquarters. Kinaxis (Ottawa, Canada) launched its Rapid Response NextGen platform in January 2024, featuring integrated digital twins and autonomous decision-making adopted by global consumer goods and electronics leaders.

Asia Pacific Control Tower Trends

Asia Pacific is the fastest-growing regional market for control tower solutions, accounting for over 28% of global revenue in 2024 and recording the highest forecast CAGR through 2033. China is the most developed APAC market for control tower implementation, driven by its massive manufacturing capacity, the "Made in China 2025" industrial digitalization strategy, and rapidly growing supply chain complexity across the electronics, automotive, and consumer goods sectors. Japan follows as a sophisticated adopter, with Toyota, Honda, and other automotive OEMs deploying multi-tier supply chain visibility platforms to manage intricate keiretsu supplier networks.

India is an accelerating growth market, with government initiatives including the Production Linked Incentive (PLI) scheme driving domestic manufacturing expansion and a corresponding need for supply chain orchestration platforms. ASEAN nations, including Vietnam, Indonesia, and Thailand, are benefiting from manufacturing diversification strategies as multinationals reduce their dependence on China, creating opportunities for greenfield control tower deployments.

Europe Control Tower Market Share

Europe is the second-largest regional market for control tower solutions, with Germany, the United Kingdom, France, and Spain as the primary demand centers. German manufacturing enterprises, concentrated in automotive, chemicals, and industrial machinery, are among the most advanced adopters of supply chain control towers globally, driven by the complexity of their multi-tier supplier networks and their exposure to geopolitical trade disruptions.

Regulatory frameworks are accelerating the adoption of European control towers. The EU Corporate Sustainability Reporting Directive (CSRD) requires large companies to report supply chain emissions and environmental impact mandate that is driving procurement of carbon-visibility and ESG analytics modules within control tower platforms. The EU's Digital Product Passport initiative and strengthened supply chain due diligence requirements under the Corporate Sustainability Due Diligence Directive (CSDDD) are similarly creating structural, compliance-driven demand for traceability and multi-tier supplier monitoring capabilities across the manufacturing sectors in France, Spain, and Benelux.

Competitive Landscape

The control tower market exhibits a moderately concentrated competitive structure, with incumbent integrated suite providers SAP SE, Oracle, and IBM, wielding significant competitive advantages through deep ERP ecosystem integrations that create high switching costs. Pure-play specialists Blue Yonder, Kinaxis, E2open, o9 Solutions, and One Network Enterprises counter by releasing tightly focused, AI-first modules that plug into any ERP environment.

Key differentiators include depth of machine learning and generative-AI explainability, multi-enterprise network breadth, and readiness for quantum optimization. Emerging business models include Control Tower as-a-Service (CTaaS), subscription-based AI analytics modules, and outcome-based pricing tied to measurable supply chain KPI improvements.

Key Developments:

- In January 2025, FourKites, a leading supply chain solutions provider, announced the launch of its Intelligent Control Tower. This innovative tool is designed to autonomously manage complex supply chain operations, provide actionable insights, evaluate risks, and deliver prescriptive recommendations.

- In May 2025, Blue Yonder launched its Cognitive Solutions platform featuring AI agents across Inventory Ops, Shelf Ops, Logistics Ops, and Warehouse Ops, built on cloud-native architecture with the proprietary SADA Loop AI model, reducing supply chain disruption response times from days to minutes.

Companies Covered in Control Tower Market

- Blue Yonder Group, Inc.

- E2open, LLC

- Elementum

- Infor

- Kinaxis

- Llamasoft

- One Network Enterprises

- Pearl Chain

- SAP SE

- Viewlocity Technologies Pty Ltd.

Frequently Asked Questions

The global Control Tower market is valued at US$ 12.9 Bn in 2026 and is projected to reach US$ 53.1 Bn by 2033, growing at a CAGR of 22.4% over the forecast period.

The key demand drivers are the global urgency for end-to-end supply chain resilience following repeated disruption events, and the rapid maturation of AI, digital twin, and IoT technologies that have transformed control towers into autonomous orchestration platforms.

The Operational segment dominates the Control Tower market with approximately 83% market share. Operational control towers provide both real-time exception detection and active corrective intervention, making them the preferred architecture for enterprises managing complex, multi-enterprise supply chains.

North America is the leading region in the global Control Tower market, accounting for approximately 37% of global revenue. The United States commands the largest national share, supported by the headquarters of leading vendors including Blue Yonder, Kinaxis, E2open, and One Network Enterprises, combined with high enterprise supply chain sophistication across retail, manufacturing, and defense sectors.

The leading companies in the Control Tower market include Blue Yonder Group, Inc., Kinaxis, SAP SE, E2open LLC, Infor, One Network Enterprises, o9 Solutions, Llamasoft, Elementum, PearlChain, Viewlocity Technologies Pty Ltd., and IBM Corporation.