- Industrial Goods & Service

- Composite Bearings Market

Composite Bearings Market Size, Share, and Growth Forecast, 2026 - 2033

Composite Bearings Market by Product Type (Fiber Matrix, Metal Matrix), Application (Construction & Mining, Automotive, Agriculture, Marine, Aerospace, Others), and Regional Analysis for 2026 – 2033

Composite Bearings Market Size and Trends Analysis

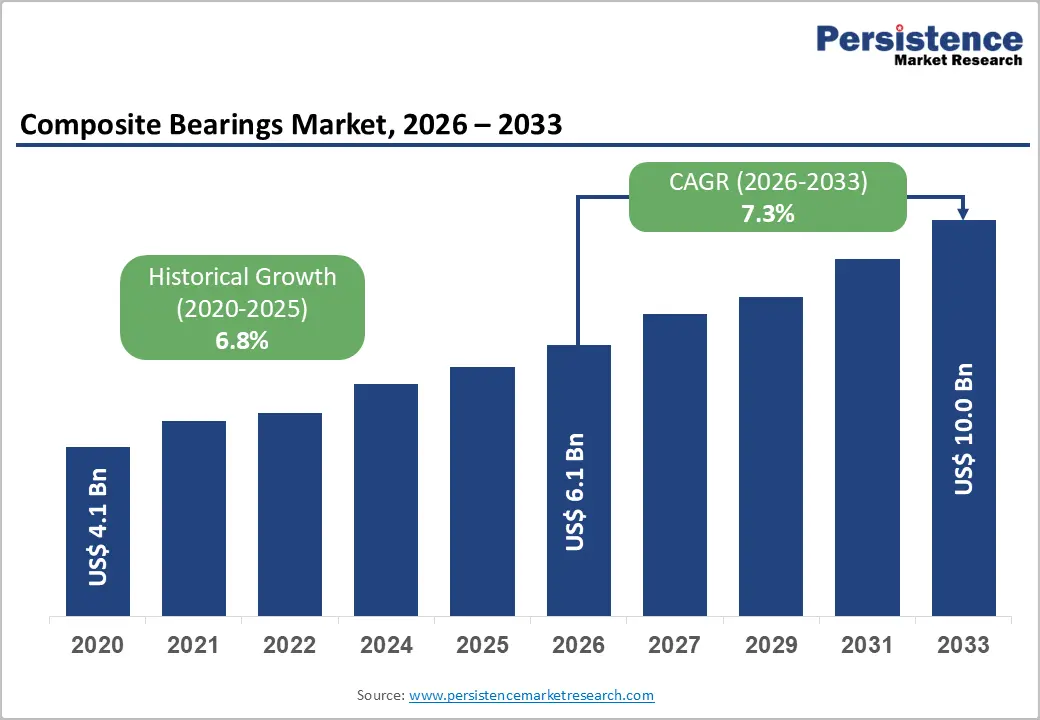

The global composite bearings market size is likely to be valued at US$6.1 billion in 2026, and is expected to reach US$10.0 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of lightweight, self-lubricating bearing demand in aerospace and automotive industries, rising replacement of metal bearings with composite solutions for corrosion resistance and reduced maintenance, and growing adoption of fiber matrix composites in high-load applications.

Growing demand for high-performance, durable composite bearings, particularly fiber-matrix types for aerospace and marine applications, is accelerating adoption across end uses. Advances in metal-matrix composites and hybrid designs are further increasing adoption by offering improved load capacity and thermal stability.

Increasing recognition of composite bearings as critical for weight reduction, friction minimization, and extended service life in emerging EV, renewable energy, and industrial automation markets remains a major driver of market growth.

Key Industry Highlights:

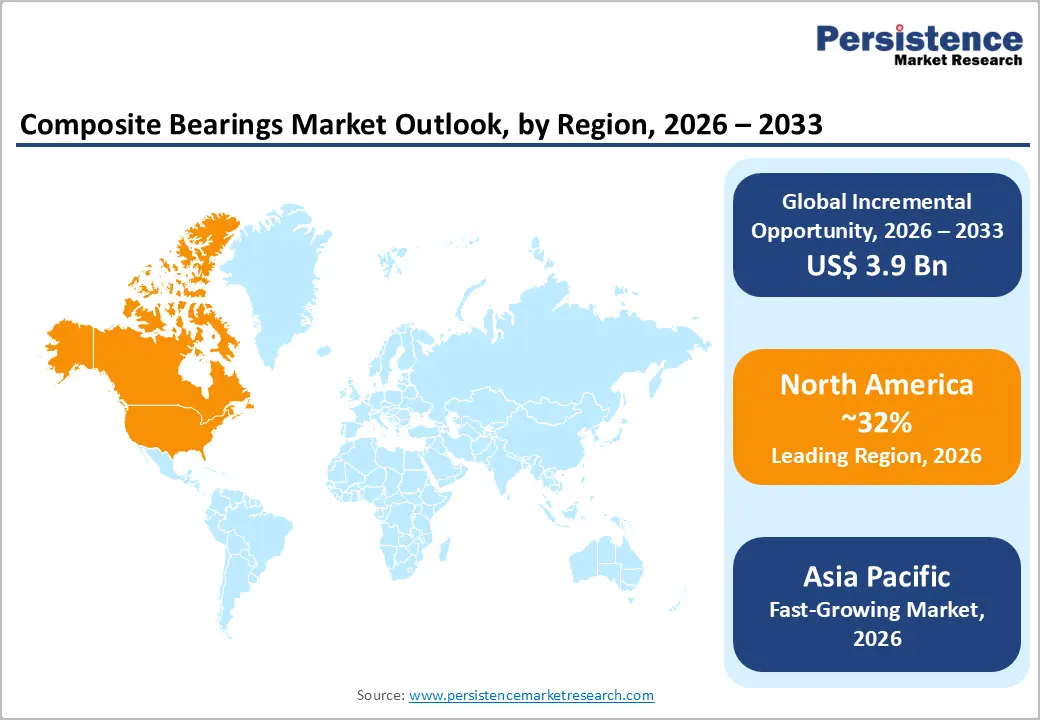

- Leading Region: North America, anticipated to account for a 32% market share in 2026, due to its strong presence of aerospace, automotive, and advanced industrial sectors that demand high-performance composite solutions.

- Fastest-growing Region: Asia Pacific, driven by rapid industrialization, expanding manufacturing bases in countries such as China and India, and rising demand across automotive, machinery, and infrastructure applications

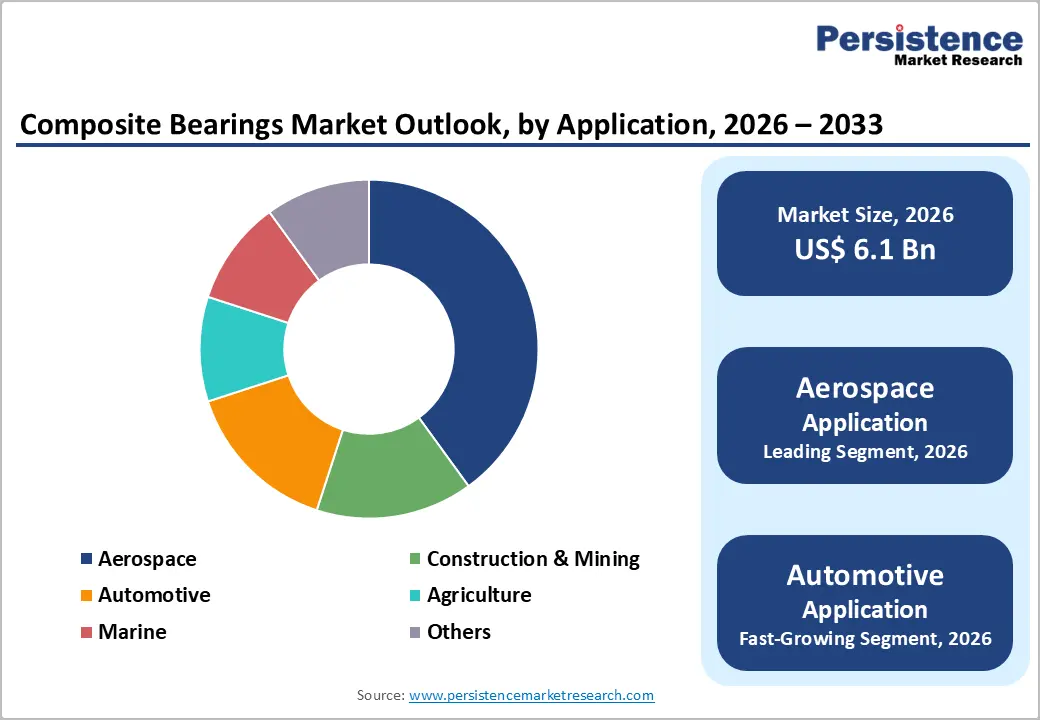

- Dominant Product Type: Fiber Matrix, accounting for approximately 62% of the market share, owing to superior weight savings and corrosion resistance.

- Leading Application: Aerospace, to contribute nearly 32% of the market revenue, due to extensive use in high-load, low-friction components.

| Global Market Attributes | Key Insights |

|---|---|

| Composite Bearings Market Size (2026E) | US$6.1 Bn |

| Market Value Forecast (2033F) | US$10.0 Bn |

| Projected Growth CAGR (2026-2033) | 7.3% |

| Historical Market Growth (2020-2025) | 6.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Demand for Lightweight, Self-Lubricating Bearings in Aerospace and Automotive

Rising demand for lightweight, self-lubricating bearings in the aerospace and automotive sectors is being driven by the need to improve efficiency, reliability, and overall system performance. Manufacturers are increasingly focused on reducing component weight to enhance fuel efficiency, extend driving range in electric vehicles, and lower emissions.

Lightweight bearing materials, including advanced composites and engineered polymers, support these goals without compromising strength or durability.

Self-lubricating bearings are increasingly preferred because they reduce the need for external lubrication systems, lowering maintenance requirements and minimizing the risk of failure in high-stress or hard-to-access applications. In aerospace, these bearings are widely used in flight control systems, landing gear components, and interior mechanisms where consistent performance under extreme temperatures and loads is essential.

In automotive applications, the use of chassis systems, steering assemblies, electric motors, and transmission components is increasing. The shift toward electric and hybrid vehicles further accelerates adoption, as quieter operation and reduced friction are critical.

Increasing Replacement of Metal Bearings in Harsh Environments

The increasing replacement of metal bearings in harsh environments is driven by performance limitations of traditional metallic components. In conditions involving high moisture, chemicals, dust, or extreme temperatures, metal bearings are prone to corrosion, wear, and frequent lubrication requirements. These challenges often lead to higher maintenance costs, unplanned downtime, and reduced equipment reliability.

Industries are shifting toward alternative bearing materials such as engineered polymers, composites, and self-lubricating solutions that perform more reliably in aggressive operating conditions. These bearings offer strong resistance to corrosion, chemicals, and abrasive particles while maintaining stable performance over long service intervals. In sectors such as aerospace, automotive, mining, food processing, and marine equipment, the ability to operate without continuous lubrication is particularly valuable. Reduced friction, lower noise levels, and lighter weight further enhance their appeal.

Barrier Analysis – High Material and Processing Costs

High material and processing costs remain a significant factor influencing the adoption of advanced bearing technologies across industries. Bearings made from engineered polymers, composites, or specialized alloys often require raw materials with superior mechanical, thermal, and chemical resistance properties. These materials are inherently more expensive than conventional steel due to complex manufacturing processes, sourcing challenges, and limited production volumes.

In addition to material costs, the fabrication of high-performance bearings involves precise processing techniques, including injection molding, sintering, and advanced machining. Maintaining tight tolerances and surface finishes is critical for ensuring reliability, particularly in applications subjected to high loads, extreme temperatures, or corrosive environments. This increases energy consumption, equipment investment, and skilled labor requirements, thereby further elevating the overall cost. For manufacturers and end users, these high upfront costs can act as a barrier, particularly for small- and medium-sized operations or applications with cost-sensitive budgets.

Limited Standardization and Certification Challenges

Limited standardization and certification challenges are key constraints in the adoption of advanced bearings, particularly those made from polymers, composites, or self-lubricating materials. Unlike conventional metal bearings, which have well-established standards and widely recognized certification processes, newer materials often lack uniform testing protocols, performance benchmarks, or industry-wide quality criteria. This creates uncertainty among manufacturers and end users regarding reliability, load capacity, lifespan, and environmental suitability.

Certification requirements vary across regions and industries, thereby complicating global deployment. Aerospace, automotive, and food processing sectors, for example, impose strict standards to ensure safety, hygiene, and regulatory compliance. Meeting these diverse certification criteria for non-metallic or hybrid bearings can be time-consuming, costly, and technically challenging. The absence of standardized guidelines also complicates product comparison, procurement decisions, and integration into existing systems.

Opportunity Analysis – Development of Hybrid and Nano-Enhanced Composite Bearings

The development of hybrid and nano-enhanced composite bearings is emerging as a key innovation to meet the growing demand for high-performance, durable, and lightweight components across various industries. Hybrid bearings combine different materials, such as steel races with polymer or ceramic rolling elements, to leverage the strengths of each material. This approach enhances wear resistance, reduces friction, and lowers overall weight, making it ideal for applications in aerospace, automotive, and electric-vehicle systems where performance and efficiency are critical.

Nano-enhanced composite bearings incorporate nanoparticles, such as carbon nanotubes, graphene, or ceramic fillers, into polymer or composite matrices. These nanoparticles significantly improve mechanical strength, thermal stability, and load-bearing capacity while maintaining self-lubricating properties. The integration of nanotechnology also enables improved resistance to wear, corrosion, and high-temperature conditions, thereby extending service life and reducing maintenance requirements.

Expansion in Renewable Energy and Electric Vehicle Applications

The expansion of renewable energy and electric vehicle (EV) applications is creating significant growth opportunities for advanced bearing technologies. In renewable energy, particularly wind and solar power, bearings are critical components in turbines, generators, and tracking systems. These applications demand bearings that can withstand high loads, variable speeds, and harsh environmental conditions while maintaining long service life and minimal maintenance.

Lightweight, corrosion-resistant, and self-lubricating bearings are increasingly preferred to improve energy efficiency and reduce operational downtime in large-scale renewable installations.

In the electric vehicle sector, bearings are essential in electric motors, transmissions, and chassis components. EVs require bearings that are low-friction, durable, and capable of supporting higher rotational speeds and increased torque while contributing to overall weight reduction. The shift from internal combustion engines to electric drivetrains has also increased demand for hybrid and composite bearings that reduce energy losses and extend battery life. As governments and industries invest heavily in decarbonization and sustainable mobility, the integration of advanced bearing solutions in these sectors is being accelerated.

Category-wise Analysis

Product Type Insights

Fiber matrix bearings are expected to dominate the market, capturing around 62% of the market share by 2026. This dominance stems from their exceptional performance in demanding applications. Typically made from reinforced polymer composites, these bearings deliver high strength-to-weight ratios, excellent wear resistance, and self-lubricating properties, making them ideal for environments where traditional metal bearings fall short.

They are extensively used in sectors such as automotive, aerospace, and industrial machinery, where durability, corrosion resistance, and long service life are paramount. For example, GGB manufactures HPMB® self-lubricating fiber-reinforced composite bushings, designed for high-load industrial and hydropower applications. These fiber composite bearings offer superior strength and maintenance-free operation, effectively replacing traditional metallic bearings in environments where low friction and corrosion resistance are essential.

Metal matrix represents the fastest-growing product type, due to its ability to combine the strength and thermal conductivity of metals with enhanced wear and corrosion resistance. These bearings are increasingly used in high-performance applications such as automotive engines, aerospace components, and industrial machinery, where high load capacity, durability, and heat dissipation are critical. Unlike conventional bearings, metal-matrix bearings can operate at extreme temperatures and under heavy loads while reducing friction and maintenance requirements.

Materion Corporation, a materials company known for developing high-performance aluminum and beryllium-based metal matrix composites that are used in demanding aerospace and automotive components, where strength-to-weight ratio and thermal stability are critical.

Application Insights

Aerospace is expected to dominate the market, contributing nearly 32% of revenue share in 2026, fueled by high demand for lightweight, durable, and high-performance components. Bearings used in aircraft engines, landing gear, control surfaces, and auxiliary systems must withstand extreme temperatures, heavy loads, and continuous motion, making advanced materials such as composites, ceramics, and metal matrix alloys essential.

The growing focus on fuel efficiency, noise reduction, and reliability in commercial and military aircraft further drives the adoption of specialized bearings. SKF Aerospace, a division of SKF Group, produces high-performance hybrid and ceramic bearings for aircraft engines, landing gear, and flight control systems. These bearings are engineered to withstand extreme temperatures, high speeds, and heavy loads while maintaining reliability and reducing maintenance requirements.

Automotive is likely to be the fastest-growing application, due to the global shift toward electric and hybrid vehicles, which demand lightweight, low-friction, and high-durability components. Bearings are critical in electric motors, transmissions, steering systems, and chassis assemblies, where efficiency and reliability directly affect performance and energy consumption. Rising adoption of precision-engineered, self-lubricating, and composite bearings helps reduce maintenance, enhance load capacity, and improve overall vehicle efficiency.

NSK Ltd. has developed ultra-high-speed ball bearings and low-friction hub unit bearings specifically for electric vehicle motors and drivetrains. These bearings are designed to handle the high rotational speeds and efficiency needs of EV motors, helping improve range and reduce energy loss compared to traditional designs.

Regional Insights

North America Composite Bearings Market Trends

North America is projected to dominate, accounting for nearly 32% of revenue in 2026, driven by the region’s advanced aerospace and automotive manufacturing, strong research and development capabilities, and high public awareness of the benefits of lightweighting. Production systems in the U.S. and Canada provide extensive support for composite bearing programs, ensuring broad accessibility across fiber-matrix, aerospace, and automotive sectors.

The increasing demand for high-performance, convenient, and easy-to-integrate forms further accelerates adoption, as these formats improve efficiency and reduce barriers associated with metal bearings.

Innovation in composite bearings technology, including stable fiber matrix, improved metal matrix delivery, and targeted lightweight enhancement, is attracting significant investment from both public and private sectors. Government initiatives and FAA/DOE campaigns continue to promote use against weight risks, fuel efficiency concerns, and emerging electrification threats, creating sustained market demand.

The growing focus on automotive grades and specialty applications, particularly in aerospace and other sectors, is expanding the range of target applications for composite bearings.

Europe Composite Bearings Market Trends

Growth in Europe is driven by increasing awareness of the benefits of lightweighting, robust regulatory frameworks, and government-led aerospace and automotive electrification programs. Countries such as Germany, France, the U.K., and Italy have well-established manufacturing frameworks that support routine use of composite bearings and encourage the adoption of innovative material-delivery methods, including fiber-matrix and metal-matrix composites. These high-performance formulations are particularly appealing for aerospace populations, regulation-conscious OEMs, and automotive users, improving efficiency and coverage rates.

Technological advancements in the development of composite bearings, such as enhanced reinforcement, application-specific delivery, and improved hybrid grades, are further enhancing market potential. European authorities are increasingly supporting research and trials on bearings for both routine and specialized applications, thereby strengthening market confidence. The growing emphasis on convenient, lightweight options aligns with the region’s focus on reducing CO emissions through prevention and electrification. Public awareness campaigns and promotional drives are expanding reach in both urban and rural areas, while suppliers are investing in compounding and novel formulations to enhance efficacy.

Asia Pacific Composite Bearings Market Trends

Asia-Pacific is likely to be the fastest-growing market for composite bearings in 2026, driven by rising awareness of automotive and aerospace applications, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting bearing campaigns to address growth in vehicle and aircraft production and emerging high-performance needs.

Composite bearings are particularly attractive in these regions due to their cost-effective administration, ease of integration, and suitability for large-scale automotive and aerospace drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-process composite bearings that can withstand challenging operating conditions and minimize wear dependence. These innovations are critical for reaching domestic OEMs and improving overall component coverage. Growing demand for automotive, aerospace, and industrial applications is contributing to market expansion.

Public-private partnerships, increased manufacturing expenditure, and rising investment in research and production capacity for composite bearings are further accelerating growth. The convenience of bearing delivery, combined with improved durability and reduced risk of failure, positions it as a preferred choice.

Competitive Landscape

The global composite bearings market features competition between established materials leaders and emerging high-performance suppliers. In North America and Europe, Trelleborg Group and Polygon Company lead through strong R&D, distribution networks, and OEM ties, bolstered by innovative fiber matrix and metal matrix programs. In Asia Pacific, Saint-Gobain S.A. and Schaeffler Group advance with localized solutions, enhancing accessibility.

Fiber matrix delivery boosts weight savings, cuts maintenance risks, and enables mass integrations across components. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Hybrid formulations solve load issues, aiding penetration in demanding applications.

Key Industry Developments:

- In October 2024, igus® introduced iglide® JPF, a new polymer bearing material free from per- and polyfluoroalkyl substances (PFAS) and polytetrafluoroethylene (PTFE). This innovation offered an environmentally sustainable alternative to traditional self-lubricating bearings, delivering high performance, durability, and reliability across industrial applications.

- In September 2024, Thordon Bearings launched the Thordon-Blue Ocean Stern Space (T-BOSS), a groundbreaking system that supported the sterntubeless ship concept. Using water-lubricated polymer bearing technology, T-BOSS eliminated the need for a sterntube and oil lubrication, reducing friction, lowering fuel consumption, and preventing oil pollution in marine environments. This development helped ship designers improve vessel efficiency and comply with stricter environmental regulations.

Companies Covered in Composite Bearings Market

- Trelleborg Group

- Polygon Company

- Saint-Gobain S.A.

- Schaeffler Group

- Hycomp LLC

- Tiodize Co. Inc.

- Spaulding Composites Inc.

- Rexnord Corporation

- RBC Bearings Incorporated

Frequently Asked Questions

The global composite bearings market is projected to reach US$6.1 billion in 2026.

The need to extend equipment life, reduce downtime, and minimize lubrication requirements is pushing the adoption of self-lubricating, corrosion-resistant, and advanced material bearings across industrial and transportation applications.

The composite bearings market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Rapid growth in EV production and renewable energy installations, such as wind turbines, creates strong demand for durable, low-friction, and maintenance-free bearings, enabling manufacturers to target high-growth, technology-driven markets.

Trelleborg Group, Polygon Company, Saint-Gobain S.A., Schaeffler Group, and RBC Bearings Incorporated are the key players.