- Animal Health

- Companion Animal Infectious Disease Diagnostics Market

Companion Animal Infectious Disease Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Companion Animal Infectious Disease Diagnostics Market by Product Type (Consumables, Reagents and Kits), Technology (Immunodiagnostics), by Animal Type (Canine, Feline), End-user, and Regional Analysis, 2026 - 2033

Companion Animal Infectious Disease Diagnostics Market Size and Trends Analysis

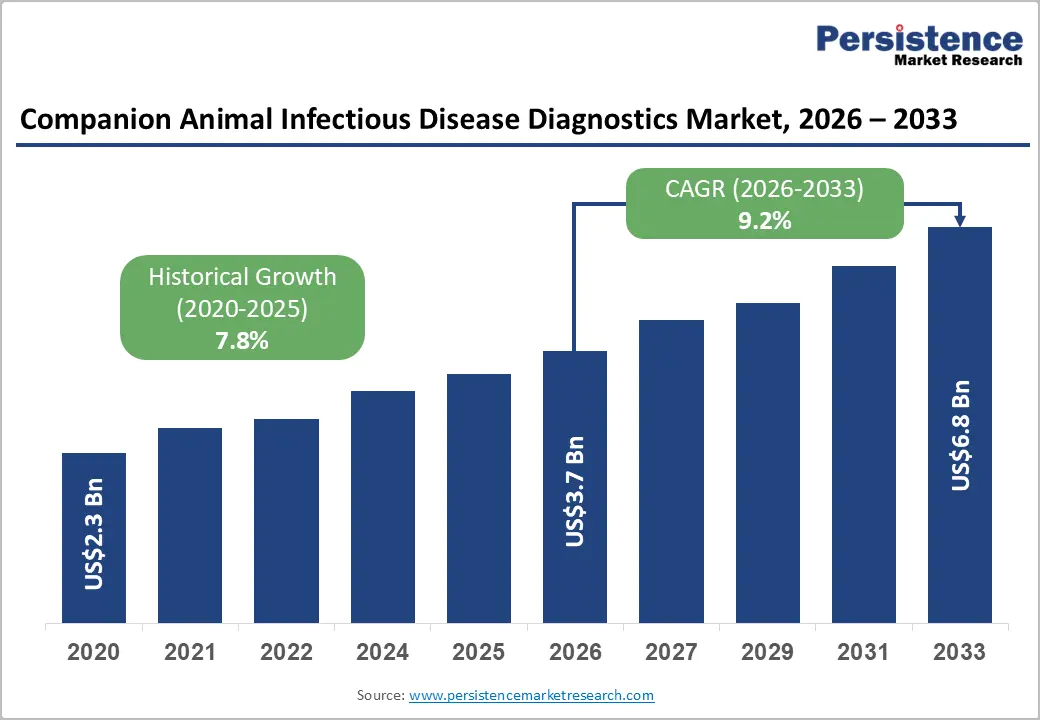

The global companion animal infectious disease diagnostics market size is likely to be valued at US$3.7 billion in 2026 and is expected to reach US$6.8 billion by 2033, growing at a CAGR of 9.2% during the forecast period from 2026 to 2033, driven by increasing pet ownership, rising incidence of zoonotic and vector-borne diseases, and high demand for early and accurate disease detection.

The market is also benefiting from the ongoing adoption of point-of-care diagnostic solutions and the expansion of in-clinic PCR testing.

Key Industry Highlights:

- New Product: In June 2025, bioMérieux announced the launch of VETFIRE, a ready-to-use PCR kit enabling quick and accurate testing for equine infectious respiratory diseases. Built on proven BIOFIRE FILMARRAY molecular PCR technology, the test delivers results in under 20 minutes from a nasopharyngeal swab.

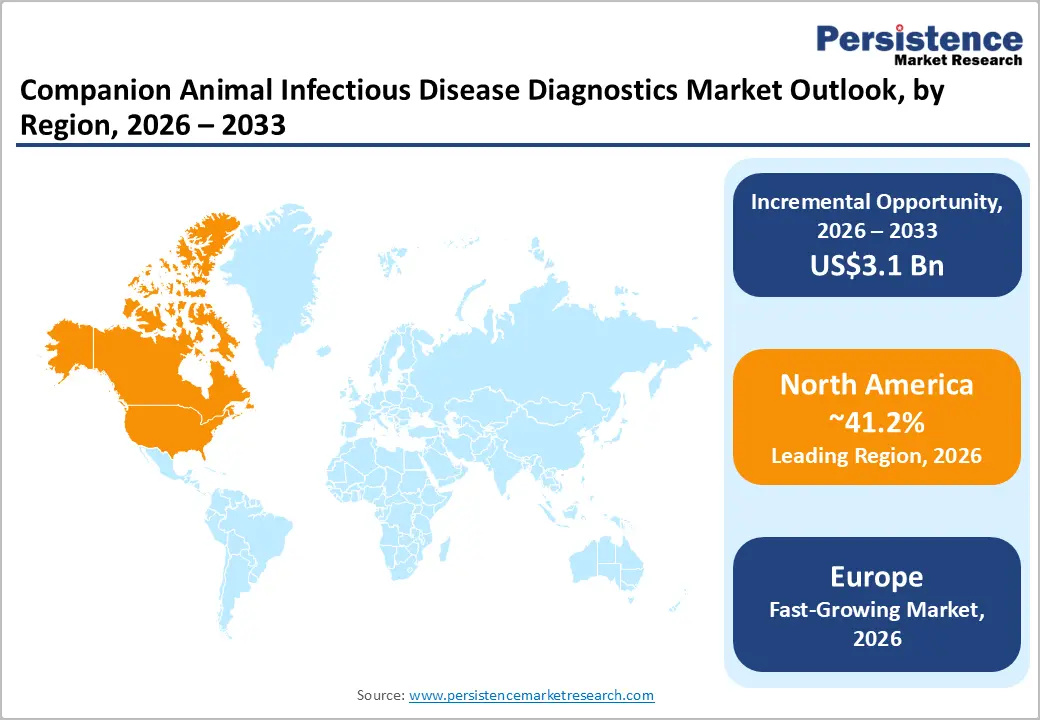

- Leading Region: North America, with about 41.2% share in 2026, owing to its well-established veterinary infrastructure and high pet healthcare spending.

- Fast-growing Region: Europe, backed by strict animal health regulations and cross-border disease surveillance frameworks.

- Leading Product Type: Consumables, reagents, and kits, approximately 66.8% share in 2026, as they generate continuous repeat demand across routine screening and disease surveillance.

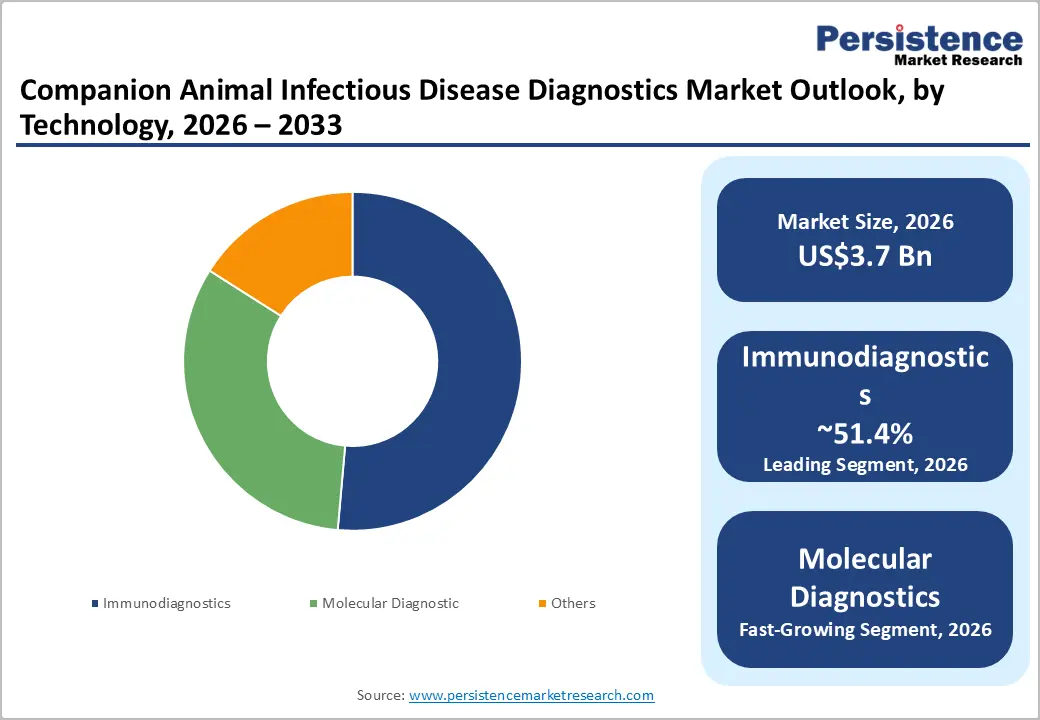

- Dominant Technology: Immunodiagnostics, nearly 51.4% in 2026, as rapid antigen and antibody tests are widely trusted for initial screening.

DRO Analysis

Driver - Rising Pet Adoption to Propel Routine Diagnostic Testing

The steady rise in pet adoption is increasing demand for infectious disease diagnostics, especially preventive screening. Pet owners are now treating animals as family members, which is pushing routine health checks. According to the American Pet Products Association, over 66% of U.S. households owned a pet in 2023, and younger owners are more likely to opt for annual diagnostic testing.

This shift is visible in Europe as well, where the Fédération Européenne de l'Industrie des Aliments pour Animaux Familiers (FEDIAF) reported over 90 million households owning pets. Clinics are responding by bundling infectious disease panels into wellness visits. This behavioral change is important as it converts diagnostics from a reactive tool into a routine service, increasing test volumes consistently across urban veterinary practices.

Surging Disease Burden to Encourage Early Detection

The increasing spread of infectious diseases in pets is pushing clinics to adopt fast and highly accurate diagnostics. Vector-borne diseases such as Lyme disease and ehrlichiosis are expanding due to climate change. The Centers for Disease Control and Prevention (CDC) has reported a steady rise in tick-borne infections in animals and humans, with dogs often acting as early indicators.

Outbreaks of canine influenza and H5N1 infections in cats have also been documented in recent veterinary alerts. A 2024 study published in Frontiers in Veterinary Science showed the rising co-infection rates in dogs, which require multiplex testing. This trend is compelling clinics to rely more on infectious disease diagnostics for timely and accurate treatment decisions.

Restraint - Persistence of Antibodies to Limit Diagnostic Accuracy

A key restraint in this market is the limited ability of serology tests to confirm active infections. Antibody-based tests often remain positive even after the pathogen is cleared, which can mislead clinical decisions. The World Organization for Animal Health notes that serological assays are better suited for exposure screening rather than confirming current infection.

For example, in diseases such as canine leishmaniasis, antibodies can persist for months despite successful treatment, as reported in studies from Parasites & Vectors. This creates uncertainty for veterinarians, especially in endemic regions. Hence, clinics often need follow-up PCR testing, which increases cost and delays treatment decisions, limiting the standalone use of serology-based diagnostics.

Opportunity - Clinic-Based Molecular Testing to Improve Turnaround Time

The shift toward in-clinic molecular diagnostics is creating new growth opportunities. Real-time PCR systems are now being designed for veterinary clinics, reducing dependence on external labs. These systems allow the same-day detection of pathogens in respiratory and gastrointestinal infections.

For instance, IDEXX Laboratories has introduced rapid molecular platforms that deliver results within hours instead of days. This complies with guidance from the American Veterinary Medical Association, which emphasizes early diagnosis to improve treatment outcomes. Quick results help veterinarians start targeted therapy immediately, improving recovery rates and reducing unnecessary antibiotic use.

Multiplex Testing Platforms to Enable Broad Pathogen Detection

Novel multiplex technologies are creating new opportunities by detecting multiple pathogens in a single test. Suspension microarrays and bead-based systems can identify dozens of infectious agents at once, which is useful in complex or co-infection cases. Research published by the National Center for Biotechnology Information shows that multiplex assays significantly improve diagnostic efficiency in respiratory and vector-borne diseases.

The platforms are also valuable for zoonotic disease monitoring, where multiple pathogens may circulate simultaneously. This capability is gaining importance as veterinarians face more mixed infections. It reduces the requirement for repeat testing and helps in speedy clinical decision-making, making it attractive for advanced veterinary practices.

Category-wise Analysis

Product Type Insights

Consumables, reagents, and kits are predicted to lead with a share of approximately 66.8% in 2026, as these are used repeatedly in every test. Unlike instruments, they generate continuous demand. Each diagnostic cycle requires fresh reagents, especially in ELISA and rapid antigen tests. The World Organization for Animal Health highlights that routine surveillance programs rely heavily on disposable diagnostic materials for disease screening. In veterinary clinics, infectious disease panels for parvovirus, Lyme disease, and feline leukemia are performed frequently, which increases repeat purchases. Companies such as Zoetis and IDEXX Laboratories follow a razor-and-blade model, where instruments are placed once but consumables drive long-term revenue. This recurring usage pattern keeps this segment dominant across both developed and emerging markets.

Equipment and instruments are estimated to be the fastest-growing segment in the forecast period, backed by the shift toward in-clinic diagnostics. Veterinary clinics are investing in compact analyzers and PCR systems to reduce turnaround time. The American Veterinary Medical Association supports early and rapid diagnosis, which is pushing clinics to adopt automated systems. New platforms now integrate AI and cloud connectivity, improving workflow efficiency. Rising demand for quick clinical decisions, especially in emergency infections, is encouraging clinics to upgrade their diagnostic infrastructure, making this segment expand at a fast pace.

Technology Insights

The immunodiagnostics segment is anticipated to dominate with a share of nearly 51.4% in 2026, as it is simple, cost-effective, and widely available. Tests such as ELISA and lateral flow assays are commonly used for detecting diseases, including heartworm and parvovirus. These tests do not require complex infrastructure, making them suitable for small clinics. CDC also recognizes serological testing as an important tool for surveillance and exposure assessment. In several regions, veterinarians prefer rapid antigen and antibody tests for quick screening during consultations. Their ease of use and low cost ensure continued dominance, especially in high-volume clinical settings.

The molecular diagnostics segment is expected to remain in the second position in 2026, as it delivers high sensitivity and specificity. PCR-based tests can detect infections at an early stage, even before symptoms appear. This is important for diseases with low pathogen load. According to research from the National Center for Biotechnology Information, PCR testing improves detection accuracy in co-infections and complex cases. Clinics are also adopting multiplex PCR panels that detect multiple pathogens in one run. This reduces diagnostic time and improves treatment decisions. As infectious diseases become more complex, veterinarians are moving toward molecular tools for confirmatory diagnosis.

Regional Insights

North America Companion Animal Infectious Disease Diagnostics Market Trends

In 2026, North America is expected to dominate with a share of around 41.2%, owing to its advanced veterinary infrastructure and high awareness of pet health. The American Pet Products Association reports that a large share of households own pets, and spending on preventive care is rising. The region also has well-established diagnostic networks and reference labs. Government agencies such as the CDC actively monitor zoonotic diseases, encouraging regular testing. Companies also frequently launch new diagnostic technologies in the U.S. first. This combination of awareness, infrastructure, and innovation keeps North America at the forefront.

U.S. Companion Animal Infectious Disease Diagnostics Market Trends

The U.S. shows exponential growth, backed by its focus on preventive veterinary care. Pet owners are constantly opting for routine diagnostic screening rather than waiting for symptoms. The American Veterinary Medical Association promotes annual testing guidelines for pets, which supports diagnostic demand. There is also rising concern about zoonotic diseases such as Lyme disease, which has been increasing in several states, as per CDC updates. Corporate veterinary chains are expanding diagnostic capabilities across clinics. This organized structure supports consistent adoption of infectious disease diagnostics across the country.

Europe Companion Animal Infectious Disease Diagnostics Market Trends

Europe is estimated to be the fastest-growing region, fueled by structured animal health programs and strict disease monitoring. The European Commission enforces surveillance for zoonotic diseases, which increases diagnostic testing. Countries are investing in early detection systems to prevent cross-border disease spread. The FEDIAF also highlights rising pet ownership across the region. Veterinary clinics are adopting advanced diagnostics to meet regulatory and clinical requirements. This combination of policy support and rising pet care awareness is bolstering market expansion.

Germany Companion Animal Infectious Disease Diagnostics Market Trends

Germany shows decent growth, spurred by its focus on veterinary research and diagnostics innovation. Institutes such as the Friedrich Loeffler Institute conduct extensive studies on animal diseases and zoonotic risks. The country has strict disease monitoring systems, which require regular diagnostic testing. Local clinics are early adopters of molecular diagnostics and automated systems. This scientific and regulatory environment supports the steady expansion of infectious disease diagnostics in the country.

U.K. Companion Animal Infectious Disease Diagnostics Market Trends

The U.K. is seeing stable growth, boosted by increasing pet insurance coverage and organized veterinary services. The Royal Veterinary College has reported surging awareness of infectious diseases among pet owners. Insurance providers often cover diagnostic testing, which encourages early screening. Large veterinary groups are also broadening clinic networks, improving access to diagnostic services. This structured network supports consistent growth in the U.K. market.

Asia Pacific Companion Animal Infectious Disease Diagnostics Market Trends

Asia Pacific is growing gradually due to increasing pet adoption in urban areas. Countries such as China and India are seeing a shift toward nuclear families, where pets are treated as companions. Governments are also focusing on zoonotic disease control. The Food and Agriculture Organization (FAO) has highlighted the importance of surveillance in Asia Pacific due to emerging infectious diseases. Veterinary infrastructure is still developing, but awareness is improving. This creates steady demand for diagnostic solutions across the region.

Japan Companion Animal Infectious Disease Diagnostics Market Trends

Japan is witnessing substantial growth due to its aging pet population and advanced healthcare approach. Old pets require frequent diagnostic testing, especially for infections and chronic conditions. The Ministry of Agriculture, Forestry, and Fisheries promotes animal health monitoring and disease prevention. Local clinics are also quick to adopt advanced diagnostic tools, including molecular and AI-based systems. High awareness and willingness to spend on pet care are supporting the ongoing expansion of diagnostics in the country.

China Companion Animal Infectious Disease Diagnostics Market Trends

China is becoming a key market due to constant growth in pet ownership and veterinary services. Urban pet populations are increasing, and owners are spending more on healthcare. The country’s government has strengthened disease monitoring systems after zoonotic outbreaks. Research published in China CDC shows increased surveillance of animal diseases in recent years. Private veterinary chains are also extending their diagnostic capabilities. This blend of policy support and market demand makes China highly attractive.

Competitive Landscape

The global companion animal infectious disease diagnostics market is moderately consolidated. IDEXX Laboratories remains the dominant player globally due to its extensive installed base of in-clinic analyzers, reference laboratory network, and recurring consumables business. The company has strengthened its position through AI-enabled diagnostic workflows, oncology diagnostics, and next-generation analyzers such as the inVue Dx platform. IDEXX’s strong relationships with veterinary clinics create high switching costs, giving it a key competitive advantage over small-scale players.

Zoetis is using its massive animal health interface to compete in diagnostics, particularly through integrated testing and therapeutics strategies. Unlike pure diagnostics firms, it combines vaccines, parasiticides, and diagnostic platforms, allowing cross-selling opportunities within veterinary clinics. Antech Diagnostics, backed by Mars Petcare, has emerged as one of the strongest challengers to IDEXX by extending reference laboratory capabilities and launching affordable rapid diagnostic solutions.

Key Industry Developments:

- In July 2025, the U.K.'s Veterinary Medicines Directorate (VMD) and Scotland's Rural College (SRUC) launched what was described as the world's first dedicated surveillance system for antimicrobial resistance (AMR) in healthy cats and dogs. This pilot study aimed to generate AMR surveillance data in healthy companion animals for the first time, with SRUC conducting the program over a four-year period.

- In June 2025, MUSE Microscopy, Inc. announced the formation of MUSE Veterinary Digital Pathology, LLC. It is a wholly-owned subsidiary focused on transforming pathology through point-of-care service, aiming to provide same-day results for tissue biopsies.

- In June 2025, IDEXX Laboratories announced the launch of the Catalyst Cortisol Test. It measures real-time quantitative cortisol concentrations to support the diagnosis of Addison's disease and the diagnosis and management of Cushing's syndrome in dogs.

Companies Covered in Companion Animal Infectious Disease Diagnostics Market

- IDEXX Laboratories Inc.

- Zoetis Services LLC.

- Antech Diagnostics, Inc.

- Virbac

- Thermo Fisher Scientific, Inc.

- bioMérieux SA

- Neogen Corporation

- Agrolabo S.p.A.

- IDVet

- Bio-Rad Laboratories, Inc.

Frequently Asked Questions

The global companion animal infectious disease diagnostics market is projected to be valued at US$3.7 billion in 2026.

The companion animal infectious disease diagnostics market is expected to reach US$6.8 billion by 2033.

Key market trends include rising adoption of in-clinic PCR testing and increasing use of multiplex diagnostics for co-infections.

Immunodiagnostics are expected to be the leading technology with a share of nearly 51.4% in 2026, as it delivers quick and low-cost testing methods that fit well into high-volume veterinary clinical workflows.

The companion animal infectious disease diagnostics market is expected to grow at a CAGR of 9.2% from 2026 to 2033.

IDEXX Laboratories Inc., Zoetis Services LLC., Antech Diagnostics, Inc., and Virbac are a few key market players.