- Animal Health

- Zoonotic Disease Market

Zoonotic Disease Market Size, Share, and Growth Forecast, 2026 - 2033

Zoonotic Disease Market by Disease Type (Rabies, Malaria, Tuberculosis, Lyme Disease, Viral Hepatitis, Animal Flu, Dengue, Others), Treatment Type (Antibiotics, Antibacterial Medications, Antifungal Medications, Antiviral Drugs, Vaccines, Immunoglobulins, Others), Route of Administration (Oral, Intravenous (IV), Intramuscular (IM), Topical), End-user (Hospitals, Clinics, Ambulatory Surgical Centers, Homecare Settings, Research Institutions), and Regional Analysis for 2026 - 2033

Zoonotic Disease Market Share and Trends Analysis

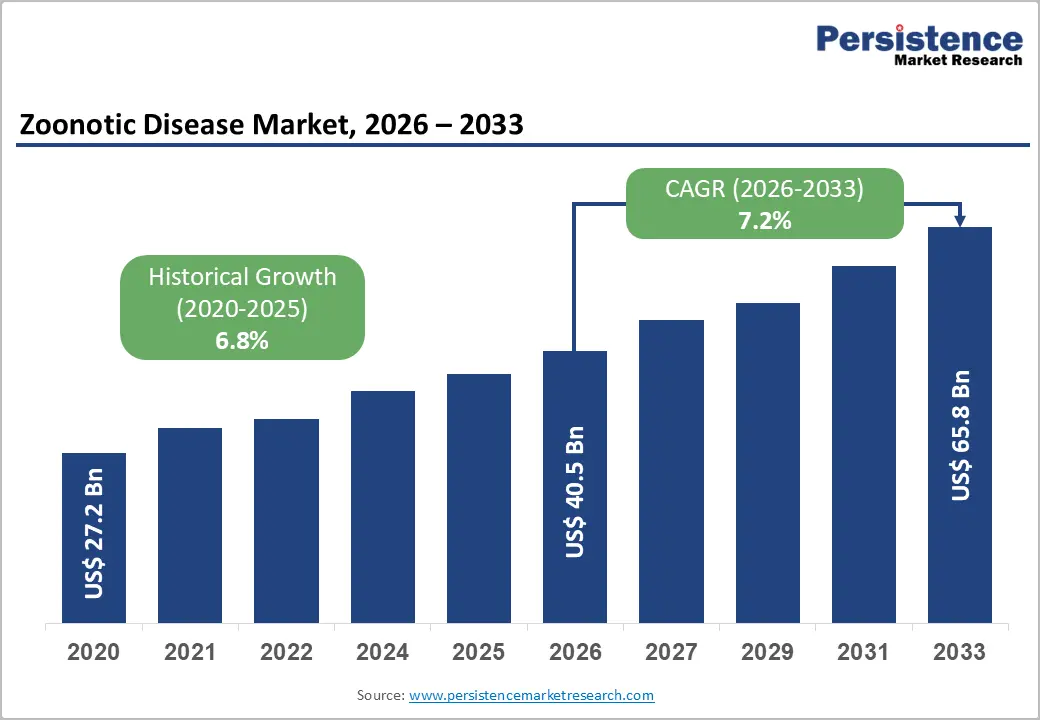

The global zoonotic disease market size is likely to be valued at US$ 40.5 billion in 2026 and is estimated to reach US$ 65.8 billion by 2033, growing at a CAGR of 7.2% during the forecast period 2026−2033. Rising prevalence of zoonotic infections in humans and animals drives demand for treatments, while growing clinical awareness promotes early diagnosis and higher therapy adoption. Advances in biotechnology and digital health enable targeted, personalized interventions, expanding patient reach.

Population growth and urbanization increase human–animal contact, elevating exposure risk and the need for preventive measures. Expansion of healthcare infrastructure in emerging markets improves access to diagnostics and therapeutics. Regulatory approvals and global health initiatives facilitate vaccine and antiviral availability. Telemedicine and AI-assisted monitoring enhance disease management and treatment adherence.

Key Industry Highlights

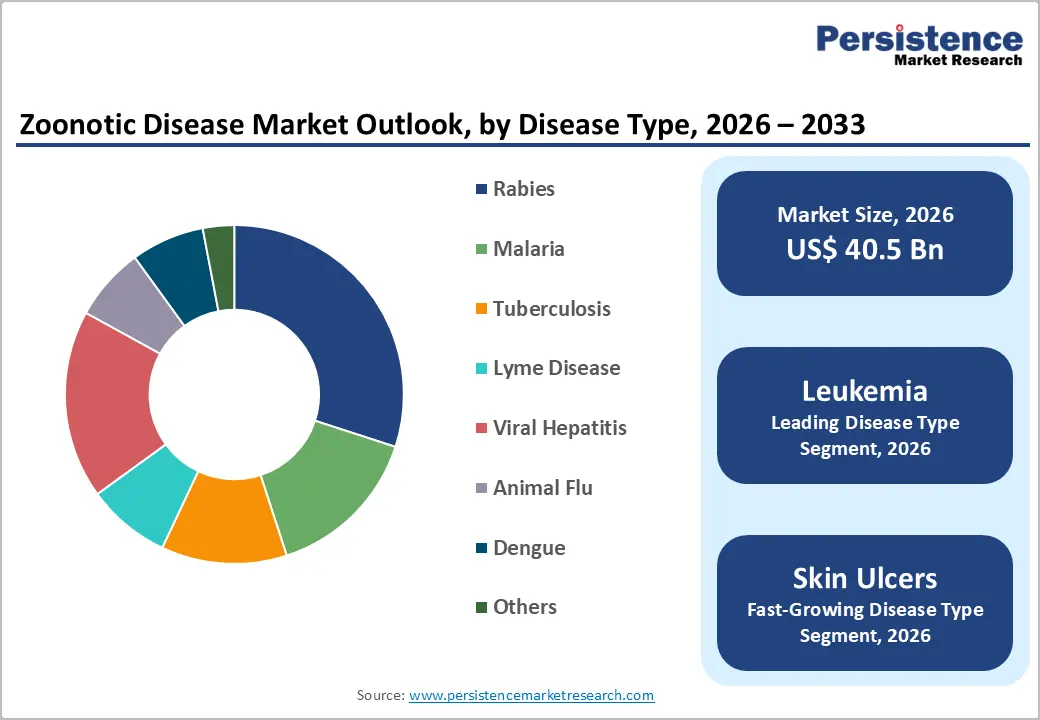

- Leading Disease Type: Rabies is set to hold around 30% revenue share in 2026, supported by high clinical awareness and established treatment protocols.

- Fastest-Growing Disease Type: Viral hepatitis is anticipated to be the fastest-growing segment during 2026–2033, driven by increasing diagnosis rates and novel antiviral therapies.

- Leading Treatment Type: Vaccines are expected to capture nearly 40% market revenue share in 2026, owing to preventive focus, provider trust, and widespread integration in healthcare programs.

- Fastest-Growing Treatment Type: Antiviral drugs are projected to be the fastest-growing segment during 2026-2033, stimulated by emerging viral infections and regulatory facilitation.

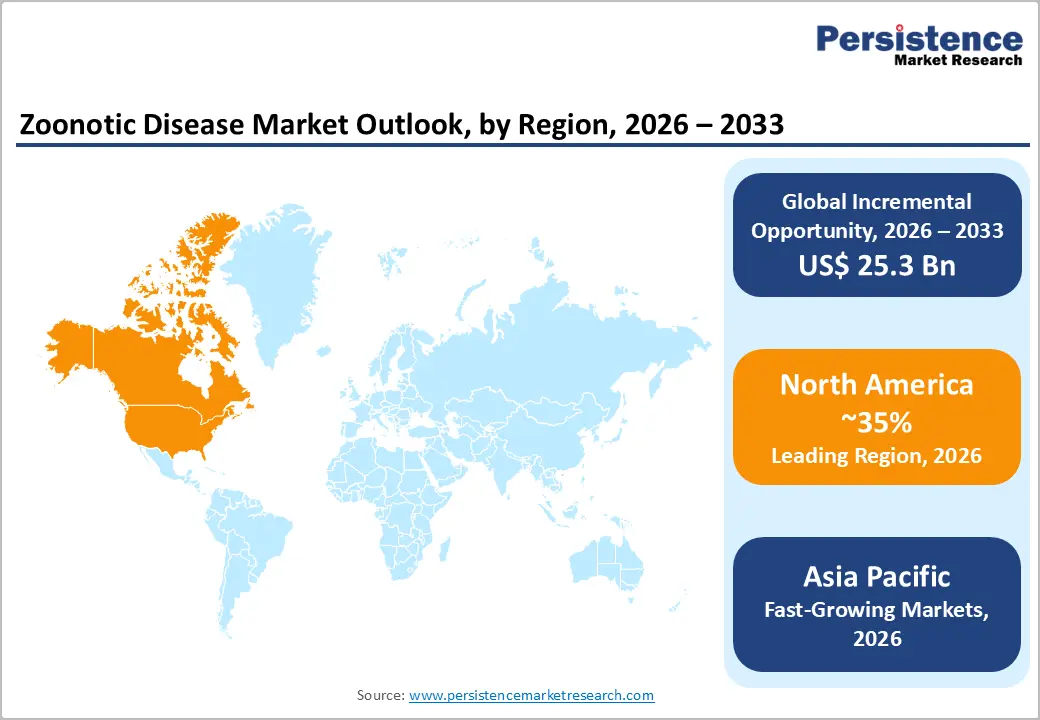

- Regional Leadership: North America is projected to capture roughly 35% of the market share by 2026, while Asia Pacific is forecasted to record the fastest growth between 2026 and 2033, driven by population density, urbanization, and expanding healthcare access.

- Competitive Environment: Moderately consolidated, with multinational pharmaceutical and biotechnology companies emphasizing innovation, strategic partnerships, and portfolio diversification.

- Innovation Trends: Integration of digital health platforms, AI-assisted diagnostics, mRNA vaccines, and telemedicine solutions to optimize disease management and improve treatment adherence.

| Key Insights | Details |

|---|---|

|

Zoonotic Disease Market Size (2026E) |

US$ 40.5 Bn |

|

Market Value Forecast (2033F) |

US$ 65.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.8% |

DRO Analysis

Driver - Rising Zoonotic Infections Increase Treatment Demand

The increase in zoonotic infections directly expands demand for therapeutic interventions as human–animal interactions intensify through agriculture, urbanization, and wildlife exposure. U.S. government data indicate that over 60% of known infectious diseases in humans come from animal sources, highlighting broad transmission potential across multiple pathogens. Higher incidence elevates clinical caseloads, prompting hospitals and clinics to invest in diagnostics, treatments, and monitoring infrastructure. Pharmaceutical and biotechnology firms respond with expanded production of antivirals, vaccines, and supportive care products. Health systems adjust procurement and supply chain strategies, ensuring rapid availability of therapies, while payers allocate resources to manage increased treatment costs and operational pressures.

Frequent zoonotic outbreaks drive healthcare providers to integrate specialized treatment pathways into standard care protocols. Recurrent infections increase utilization rates of therapeutic products, stimulating inventory turnover and accelerating adoption of innovative medications. Treatment pipelines expand as demand grows for pathogen-specific interventions. Operational budgets shift toward clinical readiness, including laboratory capacity, staff training, and equipment acquisition. Sustained incidence encourages pharmaceutical competition, enhancing accessibility of therapies and incentivizing continuous product development. Expanded treatment consumption reinforces healthcare system reliance on scalable therapeutics and underlines the structural role of epidemiological trends in shaping long-term demand patterns across regional and national networks.

Greater Clinical Awareness Improves Early Diagnosis

Early detection of infections enables faster clinical intervention, reducing symptom progression and limiting secondary transmission. Clinicians trained to evaluate animal exposure and vector contact during patient intake identify potential cases that would otherwise be overlooked. The Centers for Disease Control and Prevention (CDC) reports that over 75% of emerging infectious diseases originate from animals, indicating a substantial volume of conditions requiring clinician vigilance. Structured clinical training improves diagnostic sensitivity across healthcare settings, increasing laboratory confirmations.

Confirmed cases feed public health surveillance, refining incidence data and supporting resource allocation. Early recognition shortens time to treatment, lowering hospitalization durations and care costs. Evidence-based risk profiles accelerate testing decisions, optimizing clinical workflows and payer confidence in targeted therapies.

Provider education strengthens operational efficiency by standardizing triage protocols that flag zoonotic risk early in patient journeys. Clinical decision support tools in electronic health records prompt pathogen-specific testing based on exposure and symptom clusters, raising diagnostic yield. Primary care recognition of atypical presentations channels cases into the correct referral and testing pathways, decreasing misdiagnosis. Timely positive diagnoses trigger public health notifications, enabling containment before broader spread. Widespread clinician competence in screening promotes demand for preventive care and routine surveillance testing. This increased demand expands utilization of specialized diagnostics and supports growth across healthcare networks.

Restraint - Low Public Awareness of Preventive Measures

Limited public knowledge of preventive practices reduces adoption of vaccines, prophylactic treatments, and hygiene protocols, weakening demand for therapeutic solutions. Communities with minimal awareness experience higher infection rates, which strains healthcare systems and increases reliance on emergency care instead of structured treatment pathways. Inefficient preventive behaviors elevate disease transmission, creating unpredictable demand patterns and complicating supply chain planning for pharmaceuticals. Health education gaps restrict patient engagement with diagnostics and prophylactic programs, reducing operational efficiency and increasing resource allocation toward outbreak management rather than organized therapeutic interventions.

Reduced understanding of risk factors and preventive actions slows uptake of immunization campaigns and prophylactic measures, limiting revenue growth for manufacturers and service providers. Public hesitancy or ignorance delays disease detection, reducing opportunities for early-stage interventions. Operational efficiency declines as healthcare providers face higher caseload variability and emergency treatment needs. Limited engagement in rural or underserved areas impedes targeted therapeutics and surveillance, weakening planning, outreach, and adoption of structured disease management programs.

Shortage of Trained Healthcare Professionals in Rural Areas

Limited availability of skilled healthcare personnel in rural regions constrains treatment access for zoonotic diseases. Many remote areas lack clinicians trained in diagnosing and managing infectious conditions, delaying intervention and increasing disease progression. Infrastructure investment often prioritizes urban centers, leaving rural populations underserved. Delays in diagnosis reduce demand for therapeutics and preventive measures, weakening overall market uptake. Operational inefficiencies emerge as healthcare facilities struggle to manage patient loads with inadequate staff, increasing treatment costs and reducing throughput. Workforce shortages also slow the adoption of advanced technologies and digital health solutions, restricting service reach and efficiency improvements.

Rural workforce gaps affect supply chain dynamics and investment allocation within the sector. Providers may avoid establishing clinics in areas with insufficient trained staff, limiting geographic coverage. Training and retention programs require significant funding, and high turnover exacerbates staffing challenges. Limited professional presence reduces awareness campaigns and preventive initiatives, maintaining a high infection risk. Economic growth in underserved regions remains constrained by inadequate healthcare delivery. Persistent staffing deficits undermine patient trust, reduce treatment adherence, and restrict the introduction of innovative therapeutics, suppressing market momentum in rural zones.

Opportunity - Growth of Homecare and Remote Monitoring Solutions

Remote monitoring solutions create a structural shift in healthcare by enabling continuous health tracking outside clinical facilities. Devices and platforms transmit real-time physiological data directly to clinicians, reducing reliance on in-person visits and lowering operational costs. This approach expands oversight of patients with infectious or chronic conditions and supports proactive intervention. Widespread adoption demonstrates demand. By 2025, over 71 million Americans (26% of the population) will use remote patient monitoring services. Scale drives investment in connected care infrastructure, expands payer reimbursement opportunities, and incentivizes integration of digital tools into routine treatment workflows.

Remote monitoring improves operational efficiency by shortening response times and enabling early intervention through continuous data flow and automated alerts. Home healthcare tasks previously requiring clinician travel or facility resources are now performed digitally, reducing readmissions and optimizing staff allocation. Millions receive post-acute care in home settings supported by remote monitoring. This transition enables decentralized care delivery, meeting patient preferences for comfort and convenience. Rural and underserved regions benefit from scalable models with limited clinical staffing, increasing adoption rates. Technology partnerships expand capabilities and support data-driven decision-making, strengthening overall system performance and treatment quality.

Use of AI and Data Analytics for Outbreak Management

Government investment in artificial intelligence systems accelerates surveillance, pattern recognition, and response coordination, increasing capacity to analyze complex health data at scale. In 2025, the U.S. Centers for Disease Control and Prevention reported real-time emergency department visit data coverage from at least 90% of states and the District of Columbia, supporting automated detection of public health threats. Machine learning models applied to aggregated case, laboratory, and syndromic data improve outbreak detection speed and accuracy, reduce manual burden on epidemiologists, and amplify situational awareness. Predictive analytics inform targeted interventions and resource allocation, enhancing operational readiness and interjurisdictional coordination.

Integration of advanced analytics strengthens the utility of shared health information systems and improves outbreak forecasting and strategic planning. AI tools extract actionable insights from diverse clinical, environmental, and genomic data volumes that exceed manual processing capacity. Real-time dashboards and visualizations enable rapid interpretation, supporting public health leadership, hospitals, and emergency response teams. Scalable AI infrastructure expands analytic capacity efficiently, while continuous algorithm refinement allows adaptive learning, improving responsiveness to evolving pathogens. Automated anomaly detection enhances sensitivity and enables tailored intervention strategies across demographic and geographic populations.

Category-wise Analysis

Disease Type Insights

Rabies is likely to be the leading segment with a revenue share of approximately 30% in 2026, driven by high clinical awareness and established treatment protocols. Global vaccination campaigns and standardized post-exposure prophylaxis maintain steady demand, especially in endemic regions. Hospitals and clinics prioritize management due to the fatal risk of untreated cases, driving widespread use of immunoglobulins and vaccines. World Health Organization (WHO)-guided protocols, accessible vaccines, and digital tracking systems enhance treatment compliance. Research programs and international funding support vaccine innovation, improving delivery and coverage efficiency.

Viral hepatitis is expected to witness the fastest growth between 2026 and 2033, reflecting increasing diagnosis rates and rising clinical prioritization in both developed and emerging regions. Expanded screening programs and improved access to antiviral therapies drive adoption across hospitals, clinics, and home care. Emerging combination therapies enhance outcomes and patient adherence, while telemedicine integration supports remote monitoring. Regulatory facilitation accelerates novel therapeutics uptake. Socioeconomic development and healthcare infrastructure expansion, particularly in Asia Pacific and Africa, increase treatment accessibility and market penetration.

Treatment Type Insights

Vaccines are poised to lead with a forecasted over 40% market share in 2026, owing to their established efficacy, preventive focus, and global public health adoption. Governments and organizations like the WHO and CDC drive immunization campaigns for rabies, viral hepatitis, and dengue. Hospitals and clinics integrate vaccines into standard care. Proven safety, predictable outcomes, and wide distribution ensure consistent uptake. Innovations in thermostable formulations, cold-chain logistics, and digital tracking enhance coverage in urban and remote areas.

Antiviral drugs are anticipated to be the fastest-growing segment between 2026 and 2033, driven by the increasing incidence of viral zoonotic infections and expansion of therapeutic options. Novel antivirals for viral hepatitis, influenza, and emerging zoonoses gain adoption due to clinical effectiveness. Rising public awareness and preventive care adoption encourage patient acceptance, while retail and digital pharmacy reach improve accessibility. Telemedicine integration supports adherence and optimized outcomes. Regulatory approval of new compounds and combination therapies accelerates uptake, particularly in underserved regions, reinforcing market growth.

Regional Insights

North America Zoonotic Disease Market Trends

North America is expected to lead with an estimated 35% of the zoonotic disease market share, supported by advanced healthcare infrastructure and widespread adoption of preventive care measures. High clinical awareness among providers ensures early diagnosis and consistent treatment uptake. Well-established vaccination programs and standardized post-exposure protocols maintain stable demand across hospitals and clinics. Integration of digital health platforms enables real-time disease monitoring, adherence tracking, and efficient resource allocation. Strong funding from government and private institutions drives research and development of innovative vaccines and therapeutics, reinforcing treatment availability. Urbanized population centers allow efficient distribution of medical interventions, sustaining market penetration.

Robust pharmaceutical and biotechnology sectors contribute to rapid deployment of antiviral and immunoglobulin therapies. Healthcare systems implement electronic health records and AI-assisted surveillance, enhancing outbreak response and patient management. Regulatory frameworks streamline approval of novel compounds, accelerating commercialization of advanced treatments. High public awareness and preventive health orientation increase patient acceptance of vaccination and therapy protocols. Collaboration between research institutions, hospitals, and public health agencies supports clinical trials and protocol standardization. Wide distribution networks ensure accessibility in urban and semi-urban areas, sustaining continuous adoption of advanced therapeutics.

Europe Zoonotic Disease Market Trends

Europe maintains a strong position in the zoonotic disease market due to well-established healthcare infrastructure, high clinical awareness, and effective public health policies. Widespread vaccination programs and standardized post-exposure protocols sustain demand across hospitals and clinics. Investment in research by biotechnology and pharmaceutical companies drives development of antiviral therapies, immunoglobulins, and combination treatments. Digital tracking, electronic health records, and AI-assisted surveillance improve monitoring, patient adherence, and treatment efficiency. Urbanized populations and robust distribution networks support rapid deployment of interventions.

Regulatory frameworks enable efficient approval of new vaccines and antiviral agents, facilitating introduction of advanced therapies. Public awareness campaigns promote early diagnosis and adherence to treatment protocols. Expansion of outpatient and homecare services improves access in semi-urban and remote areas. Collaboration among hospitals, research institutions, and governmental agencies standardizes care and strengthens outbreak response. Telemedicine platforms support remote patient monitoring, while innovations in cold-chain logistics and thermostable vaccines enhance reach to underserved populations.

Asia Pacific Zoonotic Disease Market Trends

Asia Pacific is forecasted to be the fastest-growing market for the zoonotic disease market between 2026 and 2033, stimulated by the rising incidence of zoonotic infections and expanding healthcare access in both urban and rural areas. China demonstrates rapid adoption of vaccination programs and telemedicine-enabled monitoring, improving early diagnosis and treatment adherence. India experiences growth in hospital networks and public health initiatives, increasing access to antiviral therapies and immunoglobulins. Japan focuses on technological integration in healthcare facilities, supporting digital tracking of immunization coverage. South Korea invests in advanced laboratory infrastructure and outbreak surveillance, enabling efficient disease management and preventive care deployment.

Population growth and urbanization elevate human–animal interactions, driving demand for diagnostics, vaccines, and therapeutics. Expansion of healthcare infrastructure in semi-urban regions facilitates broader distribution of treatments. Regulatory facilitation allows faster approval of novel antiviral compounds and combination therapies, enabling rapid market penetration. Public awareness campaigns improve patient compliance and uptake of preventive measures. Private and government collaboration supports clinical trials and protocol standardization. Distribution networks in emerging cities ensure access to hospitals, clinics, and homecare, sustaining adoption of advanced interventions. Telemedicine and AI-based monitoring enhance treatment efficiency and long-term patient management.

Competitive Landscape

The global zoonotic disease market is moderately consolidated, with several multinational pharmaceutical and biotechnology companies holding substantial market shares. Key players include Gilead Sciences, Merck & Co., GlaxoSmithKline (GSK), Pfizer, Sanofi, Johnson & Johnson, Bharat Biotech, and CureVac. Leading firms maintain dominance through established vaccine portfolios, antiviral pipelines, and immunoglobulin therapies, while smaller regional companies serve niche therapeutic and geographic segments, contributing to overall market diversity and specialized solutions.

Competitive strategies focus on innovation in vaccine development, rapid antiviral production, and strategic partnerships with healthcare providers. Companies leverage research capabilities and technological integration to enhance clinical efficacy and treatment reach. Expansion into emerging markets, combined with collaboration with government programs, strengthens adoption of preventive and therapeutic measures. Emphasis on protocol standardization, regulatory compliance, and digital health tools ensures operational efficiency, sustained market penetration, and long-term commercial scalability across global healthcare networks.

Key Developments:

- In February 2026, India rolled out an AI-driven pathogen detection tool under the National One Health Mission to predict outbreaks of zoonotic diseases by analysing genomic data and early warning signals, aiming to shift from reactive responses to proactive surveillance and strengthen pandemic preparedness.

- In November 2025, India announced a INR 383 crore National One Health Mission to strengthen surveillance, research, and response systems for zoonotic diseases such as Nipah virus, avian influenza, scrub typhus, and COVID-19 using coordinated human, animal, and environmental health strategies.

- In April 2025, the Ministry of Health and Family Welfare announced an inter-ministerial scientific study to create a real-time surveillance model at bird sanctuaries and wetlands to detect zoonotic spillover risks at the human-wildlife-environment interface, aiming to strengthen early diagnosis and preparedness for emerging infections.

Companies Covered in Zoonotic Disease Market

- Gilead Sciences

- Merck & Co.

- GlaxoSmithKline (GSK)

- Pfizer

- Sanofi

- Johnson & Johnson

- Bharat Biotech

- CureVac

- Moderna

- Takeda Pharmaceutical

- Shionogi & Co., Ltd.

- Seqirus

- Emergent BioSolutions

- Valneva SE

- BioNTech SE

Frequently Asked Questions

The zoonotic disease market is projected to reach US$ 40.5 billion in 2026.

Rising incidence of zoonotic infections, growing clinical awareness, and expansion of vaccination and antiviral therapies drive the zoonotic disease market.

The zoonotic disease market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Development of novel vaccines, antiviral therapies, and digital health-enabled surveillance solutions presents key market opportunities.

Some of the key market players include Gilead Sciences, Merck & Co., GlaxoSmithKline (GSK), Pfizer, Sanofi, Johnson & Johnson, Bharat Biotech, and CureVac.