- Pharmaceuticals

- Cluster Headache Market

Cluster Headache Market Size, Share, and Growth Forecast 2026 - 2033

Cluster Headache Market by Drug Class (Triptans, Calcium Channel Blockers, CGRP Inhibitors, Others), by Treatment Type (Acute/Abortive Treatment, Preventive/Prophylactic Treatment, Interventional/Advanced Therapies), Route of Administration (Injectable, Oral, Intranasal, Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others), and Regional Analysis, 2026 - 2033

Cluster Headache Market Size and Trend Analysis

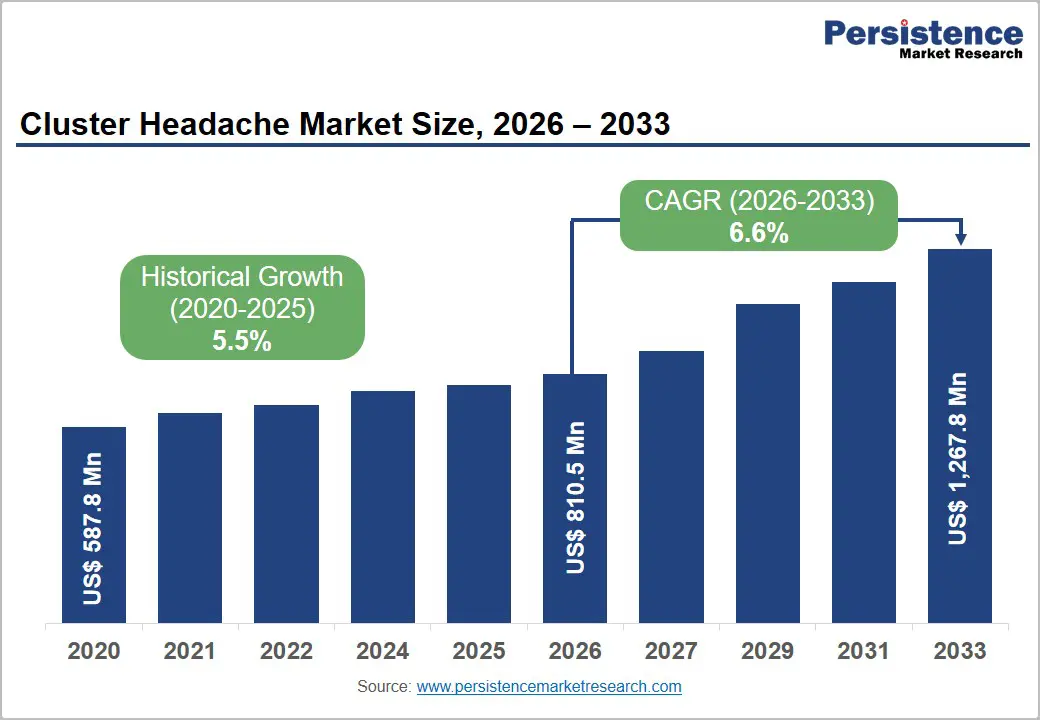

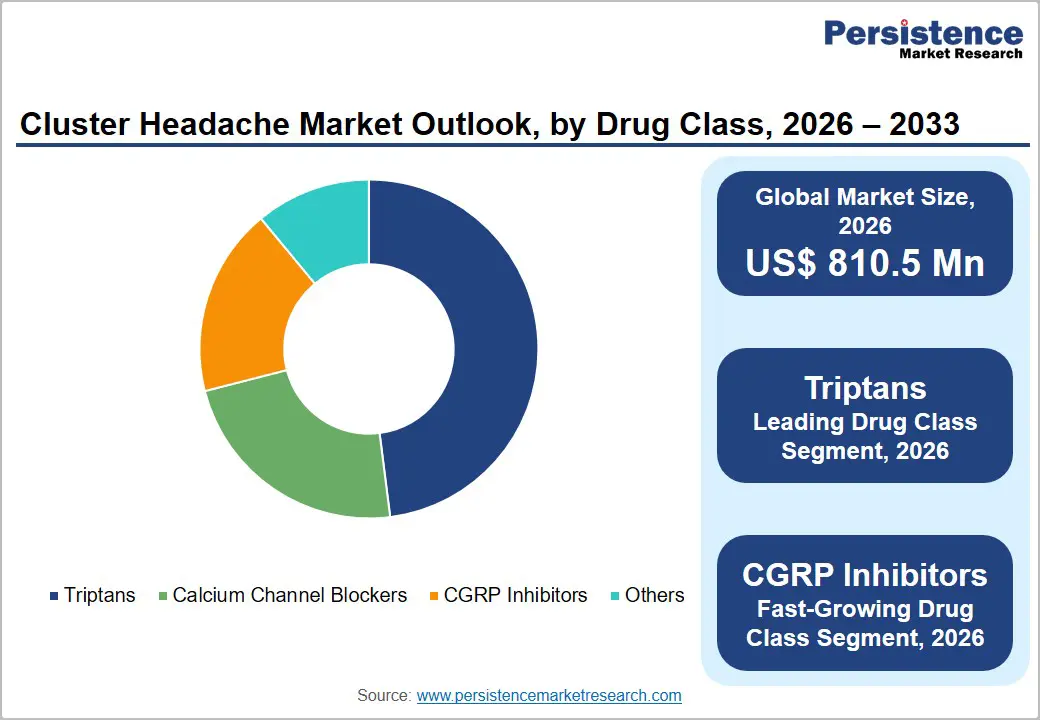

The global cluster headache market size is expected to be valued at US$ 810.5 million in 2026 and is projected to reach US$ 1,267.8 million by 2033, growing at a CAGR of 6.6% between 2026 and 2033. Increasing recognition of cluster headache as one of the most debilitating neurological pain conditions, combined with transformative advances in CGRP-targeted therapies that are reshaping treatment paradigms.

Historically underdiagnosed and undertreated, cluster headache affects an estimated 0.1% of the global population according to the International Headache Society (IHS), and the emergence of disease-specific biologic therapies, particularly anti-CGRP monoclonal antibodies, is dramatically expanding the addressable therapeutic market. Supportive regulatory frameworks in North America and Europe, rising neurological disease awareness, and expanding specialist care infrastructure are collectively reinforcing sustained demand across all treatment categories.

Key Industry Highlights:

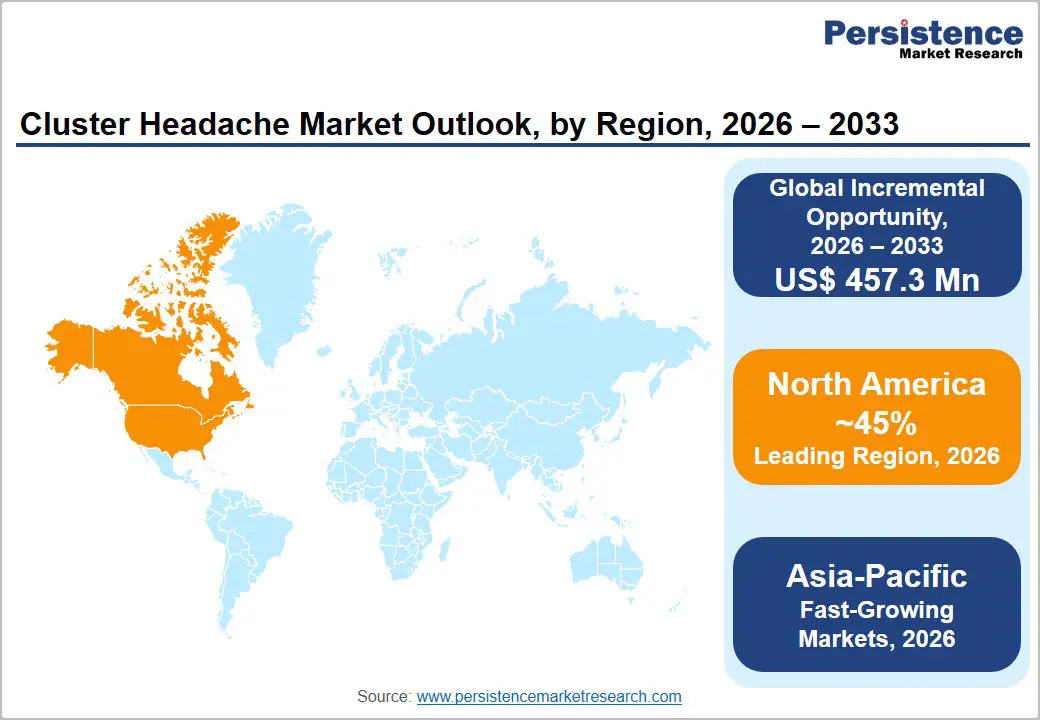

- Leading Region: North America leads the global cluster headache market with 45% market share in 2025, driven by FDA-approved CGRP biologics, well-reimbursed specialty pharma infrastructure, and the largest concentration of certified headache specialist centers.

- Fast-Growing Market: Asia Pacific is projected to register a positive CAGR, fueled by improving neurological healthcare infrastructure, rising headache disorder awareness, and regulatory modernization enabling CGRP therapy approvals in China, Japan, and India.

- Dominant Segment: Triptans are likely to lead the drug class category with 48% share in 2026, anchored by subcutaneous sumatriptan's gold-standard status in acute cluster headache management and its broad availability across generic and branded formulations.

- Fast-Growing Drug Class Segment: CGRP Inhibitors are the fastest-growing drug class through 2033, with new clinical approvals, label expansions, and real-world evidence generation steadily capturing preventive treatment market share from older verapamil-based regimens.

- Key Opportunity: Neuromodulation devices including FDA-authorized non-invasive vagus nerve stimulation represent a high-growth, drug-free treatment frontier, with expanding insurance coverage and physician awareness driving adoption in pharmacotherapy-refractory patient populations.

Market Dynamics

Drivers - Rising Disease Awareness and Improved Diagnosis Rates for Cluster Headache

Cluster headache, often described as the most severe pain a human being can experience, has historically suffered from significant diagnostic delays, with the European Headache Federation (EHF) reporting that patients wait an average of 6.6 years from symptom onset to accurate diagnosis. Growing awareness campaigns by patient advocacy organizations such as the Organisation for the Understanding of Cluster Headache (OUCH UK) and the Cluster Headache Support Group, combined with improved neurologist training under guidelines published by the International Headache Society (IHS), are significantly reducing diagnostic latency. As diagnosis rates improve, the pool of patients entering formal treatment pathways expands, directly growing the addressable market for both acute abortive therapies and long-term preventive treatments.

In the United States, the National Institute of Neurological Disorders and Stroke (NINDS) has prioritized cluster headache in its neurological disease research agenda, further elevating clinical and public awareness.

Restraints - High Cost of Biologic Therapies and Reimbursement Barriers

Despite their clinical efficacy, CGRP monoclonal antibodies carry significant annual treatment costs typically ranging from USD 6,000 to USD 10,000 per patient per year in the United States creating substantial reimbursement barriers for payers and access challenges for patients without comprehensive insurance coverage. Stringent prior authorization requirements from major U.S. insurance providers and restrictive national formulary decisions in European markets limit patient access.

The National Institute for Health and Care Excellence (NICE) in the U.K. has published conditional reimbursement guidance for anti-CGRP therapies that restricts access to patients failing multiple prior treatment lines, narrowing the commercially addressable patient population.

Opportunities - CGRP Receptor Antagonists and Novel Mechanism Drugs Addressing Unmet Needs

The ongoing development of gepants, small-molecule CGRP receptor antagonists, and other novel mechanism drugs presents a high-value commercial opportunity in cluster headache, particularly for patients who fail or cannot tolerate biologic therapies. Atogepant and rimegepant, currently approved for migraine, are being evaluated in exploratory cluster headache trials, with the oral and convenient dosing profiles of gepants representing a potential competitive advantage over injectable biologics.

According to the ClinicalTrials.gov database maintained by the U.S. National Library of Medicine, over 25 active clinical trials are enrolling patients for novel cluster headache pharmacological interventions as of 2024. As gepants and other orally bioavailable agents secure regulatory approvals for cluster headache indications, they are projected to capture meaningful market share particularly in patient segments with compliance or injection-aversion challenges, creating a new revenue layer for pharmaceutical manufacturers through 2033.

Category-wise Analysis

Drug Class Insights

The Triptans segment commands the leading position in the cluster headache market by drug class, accounting for approximately 48% of total market revenue in 2026. Triptans, particularly sumatriptan subcutaneous injection (6 mg) remain the gold-standard acute abortive treatment for cluster headache attacks, endorsed by both the International Headache Society (IHS) and the European Headache Federation (EHF) treatment guidelines.

Subcutaneous sumatriptan reliably aborts cluster headache attacks within 15 minutes in the majority of patients, a speed of onset unmatched by oral alternatives. The widespread availability of generic sumatriptan formulations following patent expiry has further broadened market access and reinforced utilization across diverse healthcare settings globally. CGRP Inhibitors, however, represent the fastest-growing drug class, with the segment expected to capture increasing market share as new approvals, label expansions, and real-world evidence accumulate through 2033.

Treatment Type Insights

Acute/Abortive Treatment is the leading treatment type segment in the cluster headache market, accounting for approximately 52% of total share in 2026. The dominance of acute treatment reflects the episodic and unpredictable nature of cluster headache attacks which can occur up to 8 times daily, each lasting 15 to 180 minutes per the IHS ICHD-3 diagnostic criteria creating immediate and unavoidable demand for rapid-onset abortive therapies.

High-flow 100% oxygen inhalation and subcutaneous triptans are the most widely utilized first-line abortive options per neurological treatment guidelines. Preventive / Prophylactic Treatment is emerging as the fastest-growing treatment type, driven by the introduction of CGRP-targeted biologics and the growing clinical consensus supporting early prophylaxis initiation to reduce attack burden and improve patient quality of life.

Regional Insights

North America Cluster Headache Market Trends and Insights

North America dominated the global cluster headache market due to advanced neurological care infrastructure, higher diagnosis rates, strong biologics adoption, and favorable reimbursement systems. The regional market benefited from early uptake of CGRP-targeted therapies such as galcanezumab and widespread use of oxygen and triptan-based acute treatments. The region also had strong awareness among neurologists and headache specialists.

U.S. Cluster Headache Market Trends and Insights

The United States led the North American cluster headache market and was expected to reach approximately US$ 0.29 Bn by 2026 due to strong adoption of advanced headache therapies and high specialty-neurology access. According to neurological literature, cluster headache prevalence in the United States remained around 0.1% of the population, with men predominantly affected.

The country witnessed increasing adoption of CGRP inhibitors, oxygen therapy, and neuromodulation devices supported by FDA approvals and specialized headache centers. The U.S. healthcare system also enabled quicker commercialization of premium biologics including Emgality. Academic institutions and headache societies continued to expand diagnosis awareness, reducing historical underdiagnosis rates and supporting sustained treatment demand.

Canada Cluster Headache Market Trends and Insights

Canada is likely to reach a CAGR of approximately 7.2% during the forecast period, owing to the awareness of rare neurological disorders and expanding access to specialty headache clinics. Canada increasingly adopted CGRP-targeted biologics and evidence-based cluster headache protocols aligned with North American neurological guidelines. Growing insurance acceptance for advanced migraine and cluster headache therapies also improved treatment penetration.

Online patient communities and advocacy groups significantly increased disease awareness and earlier diagnosis. Canadian clinicians additionally reported rising use of preventive therapies such as verapamil and galcanezumab for episodic cluster headache management. Expansion of neurology services in urban provinces further supported market growth across the country.

Europe Cluster Headache Market Trends and Insights

Europe represented a major cluster headache market due to established headache treatment guidelines, universal healthcare systems, and strong neurological research activity. European organizations including the European Academy of Neurology and European Headache Federation played an important role in standardizing treatment protocols involving oxygen therapy, triptans, verapamil, and CGRP therapies.

Use of preventive therapies and strong physician awareness of refractory chronic cluster headache is highly prevalent in Europe. Europe benefits from the adoption of neuromodulation approaches and improved reimbursement access in Western European countries. Regulatory support for episodic cluster headache biologics further strengthened regional demand. Countries across Europe continued expanding specialist headache clinics and multidisciplinary pain-management programs.

Germany Cluster Headache Market Trends and Insights

Germany dominated the European cluster headache market and was expected to reach approximately US$ 80 Mn in 2026, owing to advanced neurology infrastructure and strong reimbursement support for headache therapies. Germany had one of Europe’s most developed headache treatment ecosystems, supported by specialist neurology clinics and strong physician awareness.

The country widely adopted verapamil as standard prophylactic therapy and increasingly explored CGRP inhibitors for episodic cluster headache patients. German clinicians actively participated in European headache research and guideline implementation. Availability of oxygen therapy and specialty neurologist access remained significantly higher than many Eastern European countries, strengthening treatment penetration and improving patient management outcomes.

UK Cluster Headache Market Trends and Insights

United Kingdom was projected to grow at a CAGR of approximately 6.9% during the forecast period due to rising awareness and increasing referral rates to specialist headache centers. The country experienced growing recognition of cluster headache as a severe neurological disorder requiring rapid intervention and preventive management. Organizations such as headache charities and neurological support groups improved patient education and promoted earlier diagnosis.

Increasing demand for CGRP-targeted therapies and evidence-based treatment protocols also supported market growth. The UK healthcare system further expanded access to oxygen therapy and specialist consultations, particularly for refractory chronic cluster headache cases requiring multidisciplinary management approaches.

Asia Pacific Cluster Headache Market Trends and Insights

Asia Pacific was projected to be the fastest-growing regional market due to improving neurological diagnosis rates, expanding healthcare infrastructure, and increasing awareness of headache disorders. Historically, cluster headache remained underdiagnosed across several Asian countries because symptoms were often confused with migraine or sinus-related disorders. However, increasing neurologist availability and expansion of specialty hospitals significantly improved diagnosis rates.

Rising healthcare spending in China, India, Japan, and South Korea also supported access to advanced therapies including triptans and CGRP-targeted biologics. The region additionally benefited from a large untreated patient population and improved pharmaceutical distribution networks. These factors collectively position Asia Pacific as the fast-growing region throughout the forecast period.

Japan Cluster Headache Market Trends and Insights

Japan led the Asia Pacific cluster headache market and was expected to reach approximately US$ 0.05 Bn by 2026 due to strong neurological care systems and high adoption of innovative headache therapies. Japan had advanced diagnostic infrastructure and relatively higher awareness of trigeminal autonomic cephalalgias compared with several neighboring countries. The country also demonstrated increasing use of CGRP-based therapies and guideline-supported prophylactic treatments including verapamil and corticosteroids.

Japan’s aging healthcare infrastructure and strong pharmaceutical innovation ecosystem further supported the adoption of premium neurological treatments. Continuous research into neurovascular disorders and increasing headache-specialist availability contributed to stable market expansion and improved patient outcomes.

India Cluster Headache Market Trends and Insights

India was expected to grow at a CAGR of approximately 8.1% during the forecast period owing to rapidly improving neurological care accessibility and rising awareness of rare headache disorders. India historically faced substantial underdiagnosis of cluster headache, particularly in secondary-care settings where symptoms were often mistaken for migraine or sinusitis. However, increasing urban neurology centers, expanding health insurance penetration, and stronger physician education initiatives significantly improved diagnosis rates.

Availability of affordable generic triptans from domestic manufacturers also supported broader treatment access. Growth in tertiary hospitals, tele-neurology services, and headache clinics across metropolitan cities further accelerated market development throughout the country.

Competitive Landscape

The global cluster headache market is highly consolidated, with a small number of large pharmaceutical companies, particularly Eli Lilly & Co., Amgen Inc., Pfizer Inc., and GlaxoSmithKline commanding dominant market positions through proprietary biologic therapies, established brand recognition, and extensive commercial infrastructure. Market leaders differentiate through proprietary CGRP-targeting mechanisms, physician engagement programs, and real-world evidence generation.

Key strategic trends include lifecycle management of approved biologics, pipeline investment in gepants and neuromodulation devices, patient support and adherence programs, and geographic expansion into underpenetrated Asia Pacific markets. Orphan drug designations for cluster headache therapies in the U.S. and EU provide market exclusivity advantages that reinforce the consolidated competitive structure.

Key Developments:

- November, 2025: Pfizer launched Rimegepant ODT in India for the treatment of migraine in adults with inadequate response to triptan therapies. The orally disintegrating CGRP receptor antagonist was introduced as a 75 mg tablet designed for administration without water.

- August, 2024: Organon and Eli Lilly and Company expanded their migraine commercialization agreement to include 11 additional markets. Under the expanded partnership, Organon received commercialization rights for Lilly’s migraine therapies, including Emgality (galcanezumab), across selected international regions.

Companies Covered in Cluster Headache Market

- Eli Lilly & Co.

- Amgen Inc.

- Pfizer Inc.

- GlaxoSmithKline

- Others

Frequently Asked Questions

The global cluster headache market size is projected to reach US$ 810.5 million in 2026.

Rising diagnosis rates, increasing CGRP adoption, severe pain burden, and expanding neurology treatment accessibility.

North America leads the global cluster headache market with approximately 45% of the total share in 2026.

Development of targeted biologics, neuromodulation therapies, and improved diagnosis in underserved emerging healthcare markets.

Eli Lilly & Co., Amgen Inc., Pfizer Inc., GlaxoSmithKline.