- Pharmaceuticals

- Blood Transfusion Diagnostics Market

Blood Transfusion Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Blood Transfusion Diagnostics Market by Product (Reagents & Kits, Instruments & Analyzers, Consumables & Accessories, Software & Services), by Technology (Serological Testing, Nucleic Acid Testing (NAT), Polymerase Chain Reaction (PCR), Microarray Technology, Others), Application (Blood Group Typing, Infectious Disease Screening, Antibody Screening and Identification, Molecular Immunohematology Testing, Others), End-user (Blood Banks, Hospitals, Diagnostic Laboratories, Research Institutes & Academic Centers, Others), and Regional Analysis, 2026 - 2033

Blood Transfusion Diagnostics Market Size and Trend Analysis

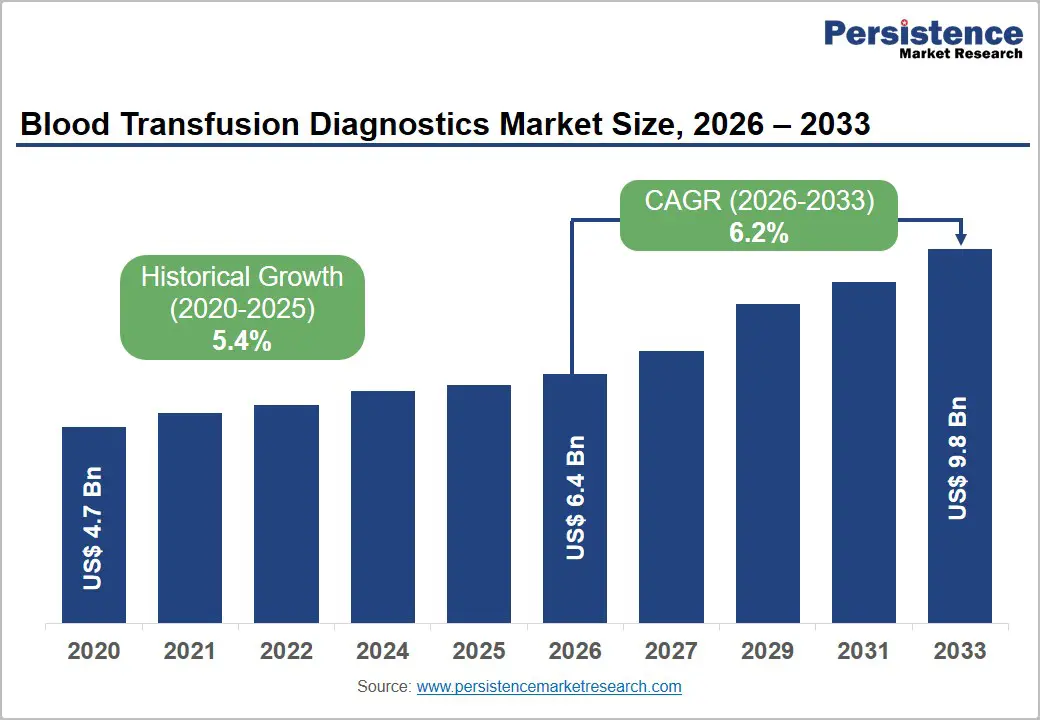

The global blood transfusion diagnostics market size is expected to be valued at US$ 6.4 billion in 2026 and projected to reach US$ 9.8 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This sustained growth is driven by the non-negotiable patient safety imperative of blood compatibility testing, global expansion of transfusion medicine infrastructure, and the systematic adoption of nucleic acid testing (NAT) and automated immunohematology platforms that are replacing manual serological workflows across blood banking networks globally.

According to the World Health Organization (WHO), approximately 118.5 million blood donations are collected globally each year, with each donation requiring mandatory pre-transfusion testing across blood group typing, infectious disease screening, and antibody identification protocols a testing volume that creates consistent high-frequency reagent, kit, and analyzer procurement demand independent of disease cycle or healthcare budget fluctuations through 2033.

Key Market Highlights

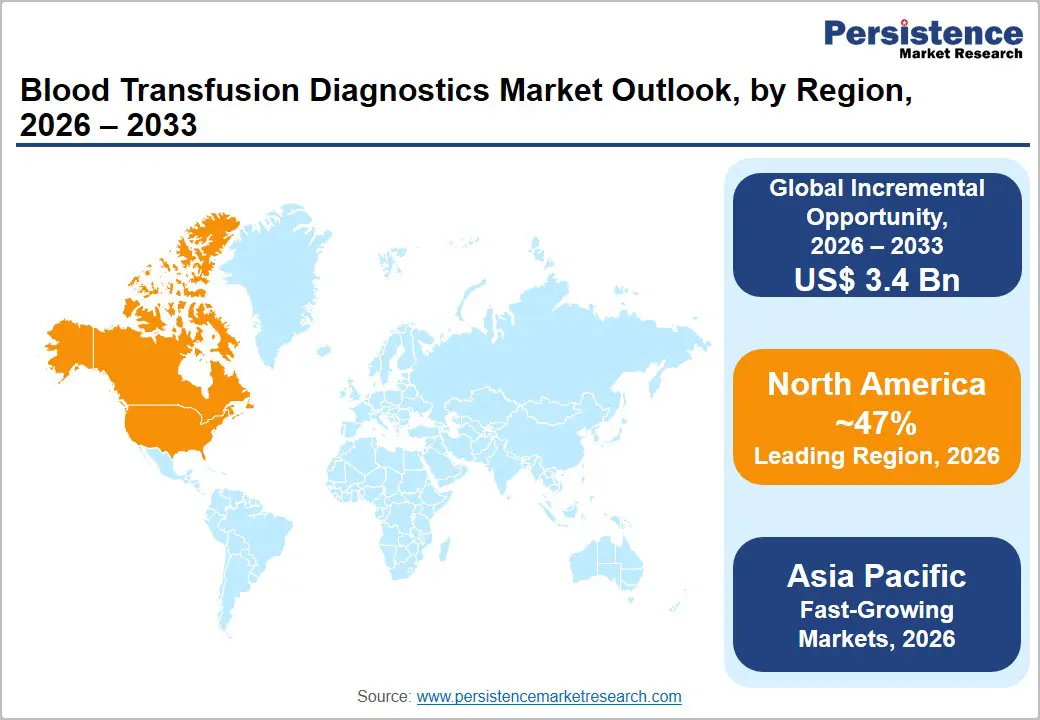

- Leading Region: North America is likely to lead the global market with 47% share in 2026, anchored by FDA 21 CFR 606/610/640 compliance mandates, AABB accreditation requirements, the American Red Cross’ 6.8M annual unit collection, and the highest automated immunohematology and NAT platform penetration globally.

- Fastest Growing Region: Asia Pacific is projected to register the highest CAGR during 2026 - 2033, driven by China’s CSBT-documented 24M+ annual donation NAT mandate, India’s NBTC mandating NAT across 2,760+ blood banks, and ASEAN national blood safety framework formalization aligned with WHO Blood Screening Guidelines.

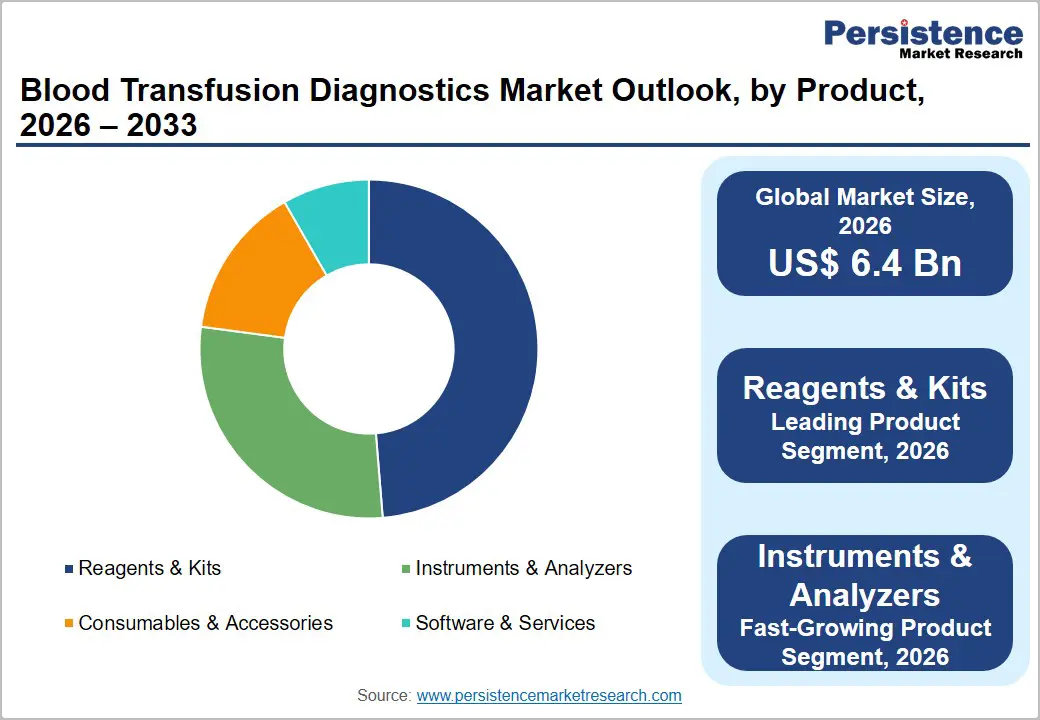

- Dominant Segment: Reagents & kits are likely to command approximately 48% share in 2026, driven by AABB Standards mandating blood group typing reagent consumption at every donation and pre-transfusion patient testing event, generating high-frequency recurring procurement from WHO-documented 118.5 million annual global blood donations.

- Fastest Growing Segment: Instruments & analyzers represent the fast-growing product type driven by ASCP-documented transfusion medicine workforce shortages, incentivizing walk-away automation investment, QuidelOrtho Vision Max® 2.0 FDA clearance, and Asian blood bank modernization programs implementing fully automated NAT and immunohematology workstations.

- Key Opportunity: Asia Pacific’s blood bank NAT mandate implementation covering China’s 24M+ and India’s 12M+ annual donations across 2,760+ licensed blood banks, combined with AliveDx MosaiQ® microarray CE-IVDR certification, enabling next-generation antigen profiling, represents the highest incremental revenue expansion opportunity for diagnostics companies.

Market Dynamics

Drivers - WHO-Documented Global Blood Donation Volume Creating Non-Discretionary Testing Demand

The scale of global blood transfusion activity generates structurally mandated demand for blood transfusion diagnostics that is largely insensitive to economic cycles. The World Health Organization (WHO) Global Status Report on Blood Safety and Availability 2016 and subsequent surveillance data document approximately 118.5 million annual blood donations globally, with each unit requiring at minimum blood group ABO/RhD typing, crossmatch testing, and infectious disease screening for HIV, HBV, HCV, and syphilis.

The American Association of Blood Banks (AABB)’s Standards for Blood Banks and Transfusion Services mandates comprehensive pre-transfusion testing workflows as regulatory compliance requirements in accredited facilities. Furthermore, the WHO’s 100% voluntary non-remunerated blood donation target pursued through national blood programs across 180 member states is driving systematic blood banking infrastructure expansion in low- and middle-income countries (LMICs) that generates incremental testing volume growth beyond the established developed market base.

NAT Platform Adoption Replacing Serology Windows and Improving Blood Safety Standards

The systematic adoption of Nucleic Acid Testing (NAT) as the gold standard for infectious disease screening in blood banks, required by FDA’s Title 21 CFR Part 610 for licensed blood establishments and endorsed by WHO’s Blood Screening Guidelines, is a primary driver of premium instrument and reagent revenue growth in the blood transfusion diagnostics market. NAT detects viral RNA/DNA during the pre-seroconversion window period where antibody-based serological tests produce false negatives: the FDA estimates NAT reduces the HIV window period from 22 days to approximately 9 days, and the HCV window period from 70 days to 7 days.

As China, India, Brazil, and Southeast Asian national blood programs implement NAT mandates aligned with WHO Technical Series recommendations, demand for high-throughput NAT analyzers from Grifols, Roche, and Abbott is accelerating across all major developing market blood banking networks.

Market Restraints

High Capital Cost of Automated Immunohematology Analyzers Limiting Adoption in LMICs

Fully automated immunohematology workstations, including QuidelOrtho’s Vision Max®, Grifols’ ERYTRA®, and Bio-Rad’s IH-500™, carry capital equipment costs of US$ 80,000-US$ 250,000 per system, representing significant procurement barriers for hospital blood banks and blood collection centers in Sub-Saharan Africa, South Asia, and Latin America with constrained healthcare capital expenditure budgets. The WHO Global Status Report documents that 40% of blood transfusion facilities in low-income countries lack access to basic automated testing equipment, relying instead on manual tube and gel card techniques that deliver suboptimal standardization and throughput, constraining overall market adoption velocity in the highest-growth regional markets.

Shortage of Trained Transfusion Medicine Specialists Constraining Complex Testing Adoption

Advanced blood transfusion diagnostic applications, including molecular immunohematology testing, rare blood group genotyping, and complex antibody identification panels, require specialized transfusion medicine physicians and medical laboratory scientists whose supply is globally constrained. The American Society for Clinical Pathology (ASCP) Workforce Report consistently identifies blood bank/transfusion medicine as among the most critically understaffed laboratory specialties in the U.S., with similar shortages documented in Europe and the Asia Pacific. This workforce shortage limits the implementation velocity of complex molecular immunohematology platforms and constrains the full utilization of automated analyzer capabilities, moderating premium instrument segment revenue growth below the underlying clinical demand potential.

Opportunities - Automated Immunohematology Analyzers: Fastest Growing Instrument Segment

Automated immunohematology workstations and blood grouping analyzers represent the fastest growing product segment within the blood transfusion diagnostics market, driven by hospital and blood bank automation initiatives aimed at improving throughput, reducing manual errors, and achieving regulatory compliance consistency. QuidelOrtho Corporation’s Vision Max® and Grifols’ ERYTRA® EFLEXIS represent the current generation of high-throughput, fully automated blood grouping systems capable of processing 400-600 samples per hour with minimal operator intervention.

AABB’s Standard 5.16.8.1 on blood group testing automation and FDA 21 CFR 606 quality system requirements create regulatory incentives for blood bank automation investment. The Joint Commission’s Transfusion Medicine standards in the U.S. and UK Blood Standards’ BCSH guidelines both emphasize traceability and standardization benefits of automated over manual blood banking workflows, sustaining institutional investment justification for premium analyzer procurement through 2033.

Asia Pacific Blood Bank Modernization and NAT Mandate Implementation

Asia Pacific is the fast-growing regional market for blood transfusion diagnostics, driven by national blood bank modernization programs, government-mandated NAT implementation, and the world’s largest blood donation volumes in China and India. China’s National Health Commission mandated NAT screening across all provincial blood stations by 2015, covering over 24 million annual donations per Chinese Society of Blood Transfusion data, and is now advancing to next-generation platform upgrades.

India’s National Blood Policy and National Blood Transfusion Council (NBTC) guidelines mandate NAT implementation across all licensed blood banks, driving procurement of Roche cobas® s 201 and Grifols Procleix® NAT platforms. The ASEAN Blood Standards Network’s harmonization initiatives are simultaneously formalizing blood banking quality frameworks across Southeast Asian markets, each representing untapped automation upgrade potential for leading diagnostics companies through 2033.

Category-wise Analysis

Product Insights

Reagents & Kits dominate the blood transfusion diagnostics market by product type, accounting for approximately 48% share in 2026. This revenue leadership reflects the consumable-driven economics of blood transfusion testing: every blood donation unit and pre-transfusion patient sample consumes a defined panel of blood group typing reagents, antibody screening cells, and infectious disease testing kits creating a high-frequency, non-negotiable recurring purchase cycle at every blood banking facility globally.

AABB Standards require blood group typing with anti-A, anti-B, anti-D, and reverse grouping cells for every donor unit, mandating specific reagent consumption at defined volumes. Immucor’s BioClone® blood grouping antisera, Grifols’ DG Gel® ID-Cards, Bio-Rad’s ID-Cards™, and QuidelOrtho’s BioVue® cassette systems collectively represent the dominant consumable reagent platforms consumed across global blood banking networks, generating predictable, volume-driven revenue streams that sustain the segment’s leading market position.

Application Insights

Blood Group Typing represents the leading application segment in the blood transfusion diagnostics market in 2025, as it is the most universally required, highest-frequency testing procedure performed on every blood donation unit and every pre-transfusion patient sample globally. ABO/Rh blood group determination is a mandatory prerequisite for all transfusion events under AABB, BCSH (British Committee for Standards in Haematology), and WHO transfusion guidelines, creating a non-discretionary testing volume that directly correlates with global blood collection activity.

With WHO documenting 118.5 million annual donations, each requiring ABO/RhD forward and reverse grouping blood group typing generates the highest annual reagent and automated analyzer utilization rate of any transfusion testing application, anchoring its dominant application segment revenue position globally.

End-user Insights

Blood banks represent the dominant end-user segment in the blood transfusion diagnostics market in 2026, combining the highest testing volumes per facility, the most comprehensive regulatory compliance testing requirements, and the greatest concentration of capital equipment investment. Independent blood collection organizations including American Red Cross, NHS Blood and Transplant (NHSBT), Etablissement Français du Sang (EFS), German Red Cross Blood Service (DRK-BSD), and China’s National Blood Services, collectively process tens of millions of donation units annually, each requiring comprehensive pre-release testing across blood group typing, infectious disease NAT/serology, and compatibility testing.

FDA 21 CFR 606 and EU Blood Directives 2002/98/EC and 2004/33/EC impose stringent testing documentation requirements on licensed blood establishments, ensuring that blood bank end-users sustain the most rigorous and highest-value testing procurement programs in the market.

Regional Insights

North America Blood Transfusion Diagnostics Market Trends and Insights

North America accounted for approximately 46.8% of the global blood transfusion diagnostics market in 2025, supported by stringent FDA blood safety regulations, high voluntary blood donation rates, and rapid deployment of automated NAT and immunohematology systems. The region benefits from strong institutional frameworks, including AABB accreditation and FDA CBER oversight, which mandate validated infectious disease screening and compatibility testing.

Growing adoption of fully automated transfusion workflows across hospital laboratories and blood centers is further accelerating market expansion. Increasing investments in molecular blood screening and workforce shortages in transfusion laboratories are encouraging the adoption of high-throughput automated analyzers from major manufacturers such as QuidelOrtho, Bio-Rad, and Immucor.

U.S. Blood Transfusion Diagnostics Market Trends and Insights

The U.S. represented nearly 84.5% North America in 2026, driven by advanced transfusion infrastructure and extensive donor screening programs. The American Red Cross collects over 6.5 million blood units annually, creating sustained demand for serological and NAT testing systems. Major healthcare systems are increasingly adopting integrated automation platforms to reduce manual intervention and improve turnaround efficiency in hospital blood banks.

Canada Blood Transfusion Diagnostics Market Trends and Insights

Canada accounted for around 9.4% of the regional market in 2026, supported by Canadian Blood Services’ nationwide modernization initiatives. Increasing implementation of automated blood grouping and infectious disease testing technologies across provincial transfusion laboratories is strengthening demand. The country is also witnessing growing investments in digital laboratory management and standardized transfusion safety protocols.

Europe Blood Transfusion Diagnostics Market Trends and Insights

Europe captured nearly 28.6% of the global blood transfusion diagnostics market in 2026, supported by harmonized blood safety regulations under the EU Blood Directive and IVDR compliance requirements. Rising adoption of automated immunohematology systems and centralized blood screening laboratories is driving regional growth. European healthcare systems are increasingly investing in advanced infectious disease screening technologies and digital transfusion management platforms to improve blood traceability and patient safety.

Regulatory pressure for CE-IVDR-certified diagnostic products is accelerating technology upgrades across national blood services and hospital laboratories, benefiting established suppliers such as Grifols, Bio-Rad, and Werfen.

Germany Blood Transfusion Diagnostics Market Trends and Insights

Germany is approximately 23.8% of the European market in 2026 due to its highly structured blood banking network and strong regulatory oversight by the Paul-Ehrlich-Institut. German Red Cross Blood Services are investing in next-generation automation platforms and high-throughput NAT systems to strengthen donor screening efficiency and operational standardization.

UK Blood Transfusion Diagnostics Market Trends and Insights

The UK contributed close to 19.7% of the regional market in 2026, supported by NHS Blood and Transplant’s large-scale automated blood screening operations. The country continues expanding the deployment of integrated immunohematology analyzers and digital transfusion monitoring systems to optimize blood safety management and reduce laboratory workload pressures.

Asia Pacific Blood Transfusion Diagnostics Market Trends and Insights

Asia Pacific is projected to register the fastest CAGR of approximately 9.8% during the forecast period, with the region accounting for nearly 18.9% share in 2026. Expanding blood donation programs, rising healthcare expenditure, and increasing government mandates for infectious disease screening are driving market growth. Countries across the region are modernizing blood banking infrastructure through automation and NAT adoption to improve transfusion safety standards. Growing awareness regarding transfusion-transmitted infections and increasing investments in public healthcare laboratories are further supporting demand for advanced blood screening technologies.

China Blood Transfusion Diagnostics Market Trends and Insights

China represented nearly 41.6% of the Asia Pacific market in 2026, supported by one of the world’s largest blood collection systems with over 24 million annual donations. Provincial blood stations are increasingly adopting NAT screening platforms under National Health Commission mandates, while domestic manufacturers continue expanding their presence in molecular diagnostics.

India Blood Transfusion Diagnostics Market Trends and Insights

India accounted for approximately 18.4% of the regional market in 2026 and is emerging as one of the fast-growing countries globally. Expansion of the National Blood Transfusion Council’s NAT implementation programs across more than 2,700 licensed blood banks is accelerating procurement of automated screening systems and infectious disease testing platforms.

Competitive Landscape

The global blood transfusion diagnostics market is moderately consolidated, with a small number of specialized IVD companies commanding the majority of blood banking diagnostic revenues globally. Grifols, S.A., Immucor, Inc. (now part of Werfen, S.A.), Bio-Rad Laboratories, Inc., and QuidelOrtho Corporation collectively dominate the immunohematology reagent and analyzer segment. Roche, Abbott, and Siemens Healthineers lead in infectious disease NAT and serology platforms.

Key competitive differentiators include reagent-analyzer closed-system integration, NAT multiplex capability breadth, global blood bank installation base depth, and CE-IVDR and FDA compliance infrastructure. Emerging trends include molecular immunohematology genotyping platforms and AI-assisted image analysis for agglutination reading.

Key Developments:

- In October 2025, QuidelOrtho Corporation showcased its continued commitment to advancing transfusion medicine at the Association for the Advancement of Blood & Biotherapies 2025 Annual Meeting. The company’s participation followed recent FDA clearance of its Micro Typing Systems (MTS) DAT Card and reflected the ongoing expansion of its direct antiglobulin testing and broader immunohematology diagnostics portfolio.

- In March 2025, Grifols entered into a strategic partnership with Inpeco, a global provider of total laboratory automation technologies, to deliver integrated instrumentation, robotics, and software solutions for transfusion medicine laboratories. The collaboration is designed to help blood banks and hospital laboratories modernize operations, streamline workflows, and improve overall efficiency.

Companies Covered in Blood Transfusion Diagnostics Market

- Grifols, S.A.

- Immucor, Inc.

- Bio-Rad Laboratories, Inc.

- QuidelOrtho Corporation

- F. Hoffmann-La Roche Ltd

- AliveDx (formerly Quotient Limited)

- Merck KGaA, Darmstadt, Germany

- Abbott Laboratories

- Werfen, S.A.

- DiaSorin S.p.A.

- Beckman Coulter, Inc.

- Siemens Healthineers AG

- Haemonetics Corporation

- BAG Health Care GmbH

- bioMérieux S.A.

- Others

Frequently Asked Questions

The global blood transfusion diagnostics market is projected to be valued at US$ 6.4 billion in 2026, driven by WHO-documented 118.5 million annual global blood donations each mandating comprehensive pre-release testing, FDA 21 CFR 606/610 compliance requirements for U.S. blood establishments, and the systematic implementation of NAT screening mandates across China’s 24M+ and India’s NBTC-mandated 2,760+ licensed blood bank networks.

Rising blood donation volumes, stringent regulatory mandates for transfusion-transmitted infection screening, and increasing adoption of automated serological and molecular diagnostic platforms are the primary demand drivers for the blood transfusion diagnostics market.

North America leads with approximately 47% market share in 2025, anchored by the U.S. FDA’s comprehensive blood establishment licensing framework under 21 CFR 606/610/640, AABB accreditation mandating automated immunohematology and NAT testing workflows, and the American Red Cross’ 6.8 million annual unit collection requiring comprehensive diagnostic testing. The region’s ASCP-documented transfusion medicine workforce shortage is simultaneously accelerating walk-away automated analyzer investment.

The key growth opportunity lies in expanding nucleic acid testing (NAT) and molecular immunohematology adoption across emerging markets as governments modernize blood banking infrastructure and strengthen national blood safety programs.

Key players include Grifols S.A. (ERYTRA®), Immucor Inc. (GALILEO Neo®), Bio-Rad Laboratories (ID-Cards™), QuidelOrtho Corporation (Vision Max®), F. Hoffmann-La Roche Ltd (cobas® s 201), AliveDx (MosaiQ®), Abbott Laboratories (m2000), Werfen S.A., bioMérieux S.A., Siemens Healthineers AG (ADVIA Centaur®), BAG Health Care GmbH, DiaSorin S.p.A., Haemonetics Corporation, Merck KGaA, and Hologic Inc. (Gen-Probe), among others.