- Pharmaceuticals

- Hemophilia Market

Hemophilia Market Size, Share, and Growth Forecast 2026 - 2033

Hemophilia Market by Disease Type (Hemophilia A, Hemophilia B, Hemophilia C, Others), by Treatment (Factor Replacement Therapy, Non-factor Replacement Therapy, Gene Therapy, Others), by Route of Administration (Intravenous, Subcutaneous, Nasal, Oral), by End-user (Hospitals, Specialty Centers, Homecare Settings), by Regional Analysis, 2026 - 2033

Hemophilia Market Size and Trend Analysis

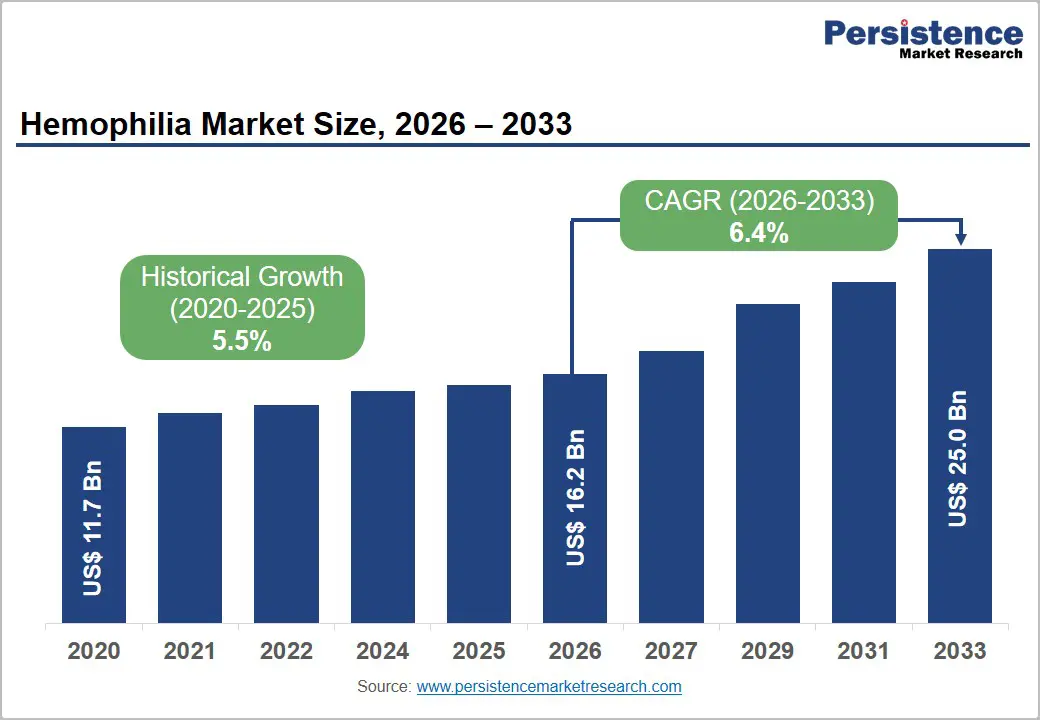

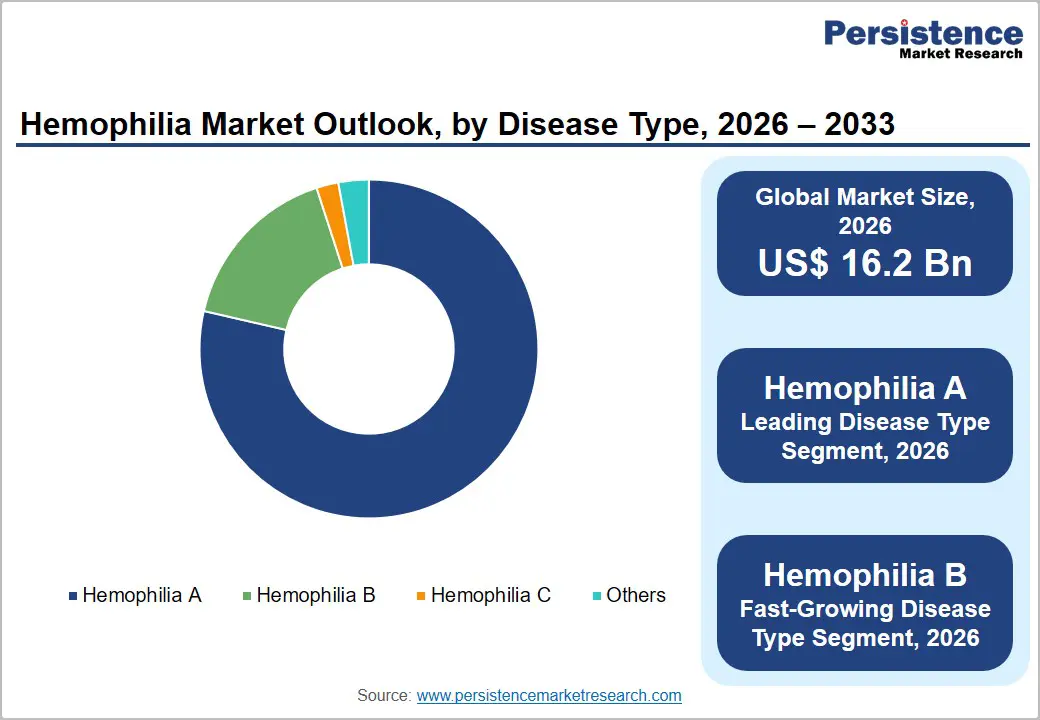

The global hemophilia market size is expected to reach US$ 16.2 billion in 2026 and US$ 25.0 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Sustained market expansion is primarily driven by the rising global prevalence of hemophilia, advances in extended half-life clotting factor concentrates, and the rapid emergence of gene therapy as a transformative treatment modality. According to the World Federation of Hemophilia (WFH), approximately 1 in 10,000 males is born with hemophilia A, and around 1 in 50,000 males is born with hemophilia B. Growing awareness, expanding access to prophylactic treatment in developing economies, and favorable regulatory frameworks for orphan drugs collectively reinforce the strong growth trajectory of this market through 2033.

Key Highlights

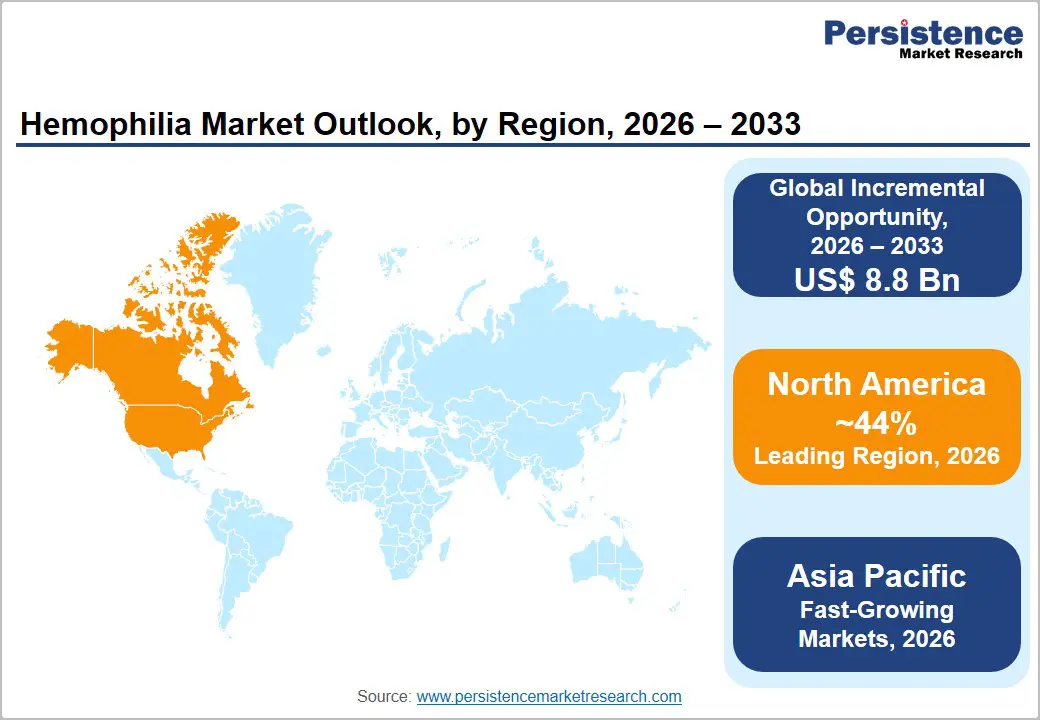

- Leading Region: North America holds approximately 44% of the global hemophilia market share in 2025, driven by the U.S.'s robust HTC network, favorable orphan drug regulations, and high per-capita treatment expenditure across factor and non-factor therapies.

- Fast-Growing Market: Asia Pacific is emerging as the highest-growth region, propelled by China's NRDL expansions, India's biosimilar manufacturing scale-up, Japan's advanced HI coverage, and large undiagnosed patient populations across ASEAN nations seeking accessible treatment.

- Dominant Disease Type Segment: Hemophilia A accounts for ~79% of the disease type segment in 2025 due to its significantly higher prevalence (~1 in 5,000 males), intensive factor VIII utilization requirements, and a substantially larger approved therapy portfolio, including Hemlibra®.

- Fast-Growing Treatment Modality: Gene therapy is the fastest-growing treatment category, driven by FDA/EMA approvals of Hemgenix® and Roctavian™, a 20+ program active pipeline, and outcomes-based reimbursement models that are progressively enabling commercial uptake globally.

- Opportunity: With over 75% of global hemophilia patients in low-income countries remaining untreated per WHO, emerging market entry via biosimilar factor concentrates and government-funded programs in India, China, and ASEAN offers significant incremental revenue potential.

Market Dynamics

Drivers - Rising Hemophilia Burden and Expanding Prophylaxis Adoption

The increasing global burden of hemophilia is a primary catalyst for market growth. The World Federation of Hemophilia 2023 Global Survey reported that over 869,000 people worldwide are identified with inherited bleeding disorders, including more than 312,000 with hemophilia A and over 66,000 with hemophilia B.

Despite this, a significant proportion, particularly in low- and middle-income countries, remains undiagnosed or undertreated. The shift from on-demand treatment to prophylactic regimens is accelerating adoption of factor concentrates and novel therapies. Programs such as the WFH Humanitarian Aid Program have amplified awareness, encouraging governments in Asia, Latin America, and the Middle East to bolster national bleeding disorder programs, directly fueling demand for hemophilia therapeutics and diagnostics worldwide.

Innovation in Extended Half-Life (EHL) and Non-Factor Therapies

Breakthrough innovations in extended half-life (EHL) factor concentrates and non-factor replacement therapies are reshaping the hemophilia treatment landscape. Products such as Hemlibra® (emicizumab) by F. Hoffmann-La Roche Ltd have demonstrated up to an 87% reduction in treated bleeds compared to prior prophylaxis in the HAVEN clinical trial series. EHL products, by reducing injection frequency from daily or alternate-day to once-weekly or biweekly regimens, significantly improve patient adherence and quality of life. The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have provided expedited pathways for novel therapies, fostering a robust pipeline. These innovations are broadening the treatable patient base and creating substantial incremental revenue opportunities for market participants.

Restraints - High Treatment Costs and Affordability Barriers

The cost of hemophilia therapy remains one of the most formidable barriers to market penetration. Annual treatment costs for severe hemophilia A with standard factor VIII concentrates can exceed US$ 250,000–US$ 400,000 per patient in high-income countries, according to National Hemophilia Foundation (NHF) data. Novel gene therapies, such as Hemgenix® (etranacogene dezaparvovec), which is launched at approximately US$ 3.5 million per dose, place access further out of reach for most patients globally. In lower-income countries, reimbursement infrastructure is often inadequate, limiting treatment uptake and constraining the addressable market for premium therapies.

Inhibitor Development and Treatment Complexity

Inhibitor development the formation of neutralizing antibodies against infused clotting factors complicates treatment management for approximately 30% of patients with severe hemophilia A and 3–5% with hemophilia B, as reported in literature published in the Journal of Thrombosis and Hemostasis. Inhibitor patients require more complex and expensive bypassing therapies or immune tolerance induction (ITI) protocols. This medical complexity increases the overall treatment burden, reduces product efficacy, and creates clinical and economic challenges for healthcare payers, thereby limiting broader adoption of standard factor replacement therapies.

Market Opportunities

Gene Therapy: A Paradigm-Shifting Investment Opportunity

Gene therapy represents the most transformative opportunity in the hemophilia market, with the potential to offer functional cures rather than lifelong management. CSL Behring's Hemgenix®, approved by the FDA in November 2022 for hemophilia B, and BioMarin's Roctavian™ (valoctocogene roxaparvovec), approved by the EMA in August 2022 for hemophilia A, mark the dawn of a new therapeutic era. The global gene therapy pipeline for hemophilia included over 20 active clinical programs as of 2024, according to the American Society of Gene and Cell Therapy (ASGCT). As outcomes data matures and reimbursement models evolve, such as outcomes-based payment agreements, gene therapy is poised to unlock significant long-term revenues and reshape competitive positioning for companies that lead in this space.

Expanding Reach in Emerging Economies Through Biosimilar Factor Concentrates

Emerging economies in Asia Pacific, Latin America, and the Middle East represent high-growth opportunity zones, particularly as biosimilar and recombinant factor concentrates gain regulatory traction. The Indian government's National Policy for Rare Diseases (2021) and China's inclusion of hemophilia treatments under the National Reimbursement Drug List (NRDL) are enabling broader patient access. WHO data indicates that over 75% of people with hemophilia in low-income countries remain untreated. With biosimilar factor VIII products now attracting regulatory attention under the EMA's biosimilar guidelines and analogous frameworks in India and China, companies entering these markets with cost-effective solutions stand to capture substantial unmet demand, particularly for prophylactic regimens in the pediatric population.

Category-wise Analysis

Disease Type Insights

Hemophilia A dominates the global hemophilia market, commanding approximately 79% of total market revenue in 2026. This overwhelming share reflects the condition's higher prevalence; hemophilia A is roughly four times more common than hemophilia B, affecting approximately 1 in 5,000 male births globally, per the Centers for Disease Control and Prevention (CDC). The large diagnosed patient base, combined with frequent and intensive factor VIII infusion requirements, drives substantial product utilization. Furthermore, the hemophilia A pipeline is considerably larger and more advanced, with multiple EHL factor VIII products, non-factor therapies such as Hemlibra®, and gene therapy candidates already approved or in late-stage trials, reinforcing segment leadership through the forecast period.

Treatment Insights

Factor Replacement Therapy (FRT) remains the leading treatment segment, accounting for approximately 65% of the hemophilia treatment market in 2026. This dominance is underpinned by decades of clinical validation, established reimbursement frameworks, and the extensive use of both plasma-derived and recombinant clotting factor concentrates across all severity levels of hemophilia A and B. According to data from the WFH Annual Global Survey, clotting factor concentrates remain the cornerstone of prophylaxis and on-demand regimens globally. The introduction of extended half-life variants by companies including Takeda Pharmaceutical, Novo Nordisk, and CSL Behring has further entrenched FRT leadership by improving dosing convenience and patient compliance while reducing treatment burden.

End-user Insights

Hospitals represent the dominant end-user segment in the hemophilia market, capturing approximately 52% of total market share in 2026. Hemophilia treatment centers (HTCs) embedded within tertiary-care hospital systems serve as the primary setting for diagnosis, initiation of prophylactic regimens and immune tolerance induction protocols, and management of acute hemarthrosis and surgical interventions. The U.S. Health Resources & Services Administration (HRSA) federally funds a nationwide network of 140+ HTCs that function as integrated, multidisciplinary care hubs. Similarly, European Hemophilia Consortium (EHC)-affiliated treatment centers across Germany, France, and the U.K. centralize advanced care. The clinical complexity of hemophilia management ensures that hospitals will maintain their dominant position throughout the forecast period.

Regional Insights

North America Hemophilia Market Trends and Insights

North America dominates the global hemophilia market, with an estimated 44% market share in 2025, supported by advanced access to treatments, robust reimbursement systems, and rapid adoption of innovative therapies, including gene therapies and extended half-life (EHL) products. The region benefits from established hemophilia treatment infrastructure, robust clinical research funding, and high healthcare expenditure. Increasing uptake of prophylactic therapies and value-based reimbursement models continue to strengthen regional growth prospects through 2033.

U.S. Hemophilia Market Trends and Insights

The U.S. accounts for nearly 82.4% of the North American hemophilia market and remains the global leader in hemophilia innovation and commercialization. More than 140 federally supported Hemophilia Treatment Centers (HTCs), strong orphan drug incentives, and rapid FDA approvals are accelerating the adoption of advanced therapies such as Hemgenix® and Roctavian™. The country also leads in gene therapy clinical trials and in penetration of premium-priced biologic treatments.

Canada Hemophilia Market Trends and Insights

Canada contributes approximately 11.7% of the regional market, driven by universal healthcare coverage and strong reimbursement support for recombinant clotting factors and non-factor therapies. Health Canada’s streamlined approval pathways and increasing adoption of prophylactic treatment regimens are supporting market expansion. The country is also witnessing growing investments in rare disease management programs and patient-centric hemophilia care networks.

Europe Hemophilia Market Trends and Insights

Europe is the second-largest hemophilia market globally, holding around 29.6% of global revenue in 2026. Growth is supported by centralized approvals through the European Medicines Agency (EMA), increasing adoption of recombinant therapies, and strong public healthcare funding across major EU economies. Western European countries continue to dominate treatment demand, while Eastern Europe is gradually improving patient access through national reimbursement reforms and awareness initiatives supported by regional advocacy organizations.

Germany Hemophilia Market Trends and Insights

Germany accounts for nearly 24.8% of the European hemophilia market and is a major hub for hemophilia research and plasma-derived product manufacturing. The country benefits from advanced healthcare infrastructure, high rates of biologics adoption, and the presence of leading manufacturers such as CSL Behring and Octapharma. Strong insurance coverage and continued investment in rare disease innovation further support market growth.

UK Hemophilia Market Trends and Insights

The UK accounts for approximately 18.2% of Europe’s hemophilia market. The country maintains strong demand for recombinant and EHL therapies through NHS-backed reimbursement programs. Increased political and healthcare focus following the Infected Blood Inquiry has accelerated investments in safer treatment alternatives and comprehensive patient monitoring systems. Continued MHRA regulatory alignment is also supporting access to novel therapies post-Brexit.

Asia Pacific Hemophilia Market Trends and Insights

Asia Pacific is projected to register the fastest CAGR of approximately 8.9% through 2033, fueled by expanding healthcare infrastructure, improving diagnostic capabilities, and growing government support for rare disease management. Rising awareness, increasing access to biologics, and the expansion of biosimilar manufacturing in emerging economies are strengthening regional growth. Large untreated patient populations and improving reimbursement frameworks continue to create significant long-term opportunities for global hemophilia therapy providers.

China Hemophilia Market Trends and Insights

China accounts for nearly 38.6% of the Asia Pacific hemophilia market, supported by rising healthcare expenditure and the inclusion of key hemophilia therapies in the National Reimbursement Drug List (NRDL). Government-led rare disease initiatives under Healthy China 2030 are improving access to diagnosis and treatment. The country is also expanding domestic biopharmaceutical manufacturing and gene therapy research capabilities.

India Hemophilia Market Trends and Insights

India holds an estimated 17.4% share of the regional market and is emerging as a high-growth destination due to its large undiagnosed patient base and increasing public healthcare initiatives. Expanding domestic production of biosimilar clotting factors and support from the Hemophilia Federation of India (HFI) are improving treatment affordability. Growing awareness programs and state-funded hemophilia care schemes are further accelerating market penetration.

Competitive Landscape

Market Structure Analysis

The global hemophilia market is moderately consolidated, with a small number of established biopharmaceutical and plasma-derived therapy companies controlling the majority of revenue. Takeda Pharmaceutical, CSL Behring, Novo Nordisk, Bayer AG, and F. Hoffmann-La Roche Ltd collectively command a significant market share through diversified portfolios spanning plasma-derived concentrates, recombinant factors, EHL products, and non-factor therapies. Key competitive differentiators include depth of clinical pipeline, gene therapy positioning, rare disease regulatory expertise, and global distribution reach. The competitive landscape is increasingly shaped by strategic collaborations and licensing agreements, particularly around gene therapy IP, alongside biosimilar entrants from India and China pressuring pricing in emerging markets.

Key Market Developments

- In May 2026, Pfizer Inc. announced that the European Commission (EC) approved an expanded indication for HYMPAVZI® (marstacimab), covering patients aged 12 years and older weighing at least 35 kg with hemophilia A accompanied by FVIII inhibitors or hemophilia B with FIX inhibitors.

- In May 2026, CSL Canada announced that the first Canadian patient received HEMGENIX® (etranacogene dezaparvovec), a one-time gene therapy for hemophilia B, at London Health Sciences Centre (LHSC), marking a major milestone in advancing gene therapy access and innovative hemophilia care across Canada.

- In June 2025, Novo Nordisk announced that it would present new hemophilia research at the International Society on Thrombosis and Haemostasis (ISTH) Congress held from June 21–25, highlighting data across hemophilia A and B with and without inhibitors, including findings related to clotting activity, thrombin generation, bleeding events, treatment outcomes, patient administration preferences, physician satisfaction, and global real-world management of joint bleeds.

- In October 2024, the U.S. Food and Drug Administration approved Hympavzi (marstacimab-hncq) for routine prophylaxis in patients aged 12 years and older with hemophilia A or B without inhibitors, introducing the first treatment of its kind targeting a protein involved in the blood clotting pathway.

Hemophilia Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 11.7 Bn |

| Current Market Value (2026) | US$ 16.2 Bn |

| Projected Market Value (2033) | US$ 25.0 Bn |

| CAGR (2026-2033) | 6.4% |

| Leading Region | North America, 44% share |

| Dominant Treatment | Factor Replacement Therapy, 54.8% share |

| Top-ranking Disease Type | Hemophilia A, 78.6% |

| Incremental Opportunity | US$ 8.8 Bn |

Companies Covered in Hemophilia Market

- Takeda Pharmaceutical Company Limited

- CSL Behring LLC

- Pfizer Inc.

- Bayer AG

- BioMarin Pharmaceutical Inc.

- Spark Therapeutics, Inc.

- Sanofi S.A.

- F. Hoffmann-La Roche Ltd

- Novo Nordisk A/S

- Octapharma AG

- Grifols, S.A.

- Swedish Orphan Biovitrum AB (publ) (Sobi®)

- Kedrion Biopharma

- uniQure N.V.

- Biogen Inc.

- Others

Frequently Asked Questions

The global hemophilia market is estimated to be valued at US$ 16.2 billion in 2026. The market is projected to expand at a CAGR of 6.4% from 2026 to 2033, reaching US$ 25.0 billion by 2033, driven by growing prevalence, adoption of extended half-life therapies, and the commercialization of gene therapy.

Rising prevalence of hemophilia, increasing adoption of prophylactic therapies, expanding access to recombinant and gene therapies, and improved diagnosis rates are driving growth in the global hemophilia market.

North America leads the global hemophilia market with approximately 44% market share in 2025. The United States is the primary growth driver, underpinned by its 140+ federally funded Hemophilia Treatment Centers, robust insurance reimbursement, and the commercialization of multiple advanced therapies including gene therapy products.

The largest opportunity lies in the commercialization and broader adoption of gene therapies offering long-term or potentially curative treatment outcomes for hemophilia patients.

Leading companies in the global hemophilia market include Takeda Pharmaceutical Company Limited, CSL Behring LLC, Pfizer Inc., Bayer AG, BioMarin Pharmaceutical Inc., F. Hoffmann-La Roche Ltd, Novo Nordisk A/S, Octapharma AG, Grifols S.A., Sanofi S.A., Spark Therapeutics Inc., uniQure N.V., Biogen Inc., Swedish Orphan Biovitrum AB (Sobi®), and Kedrion Biopharma, among others.