- Pharmaceuticals

- Chronic Pain Market

Chronic Pain Market Size, Share, and Growth Forecast 2026 - 2033

Chronic Pain Market by Product Type (OTC Products, Prescription Drugs), Drug Class (NSAIDs, Opioids, Local Anesthetics, Acetaminophen), Indication, Route of Administration, Distribution Channel, and Regional Analysis, 2026 - 2033

Chronic Pain Market Size and Trend Analysis

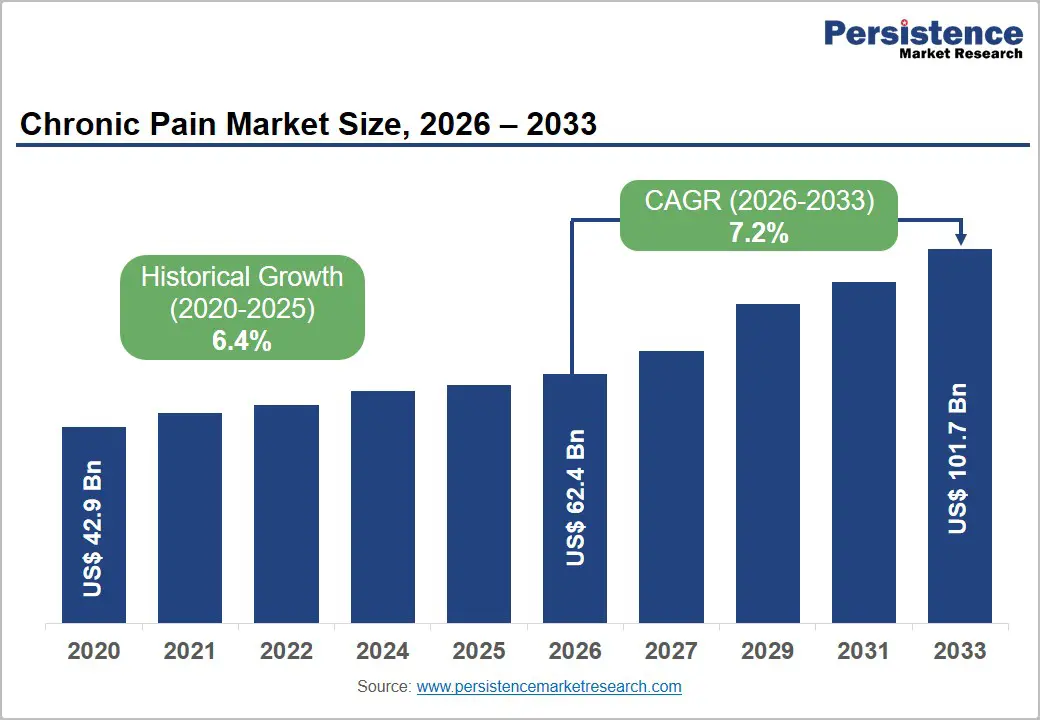

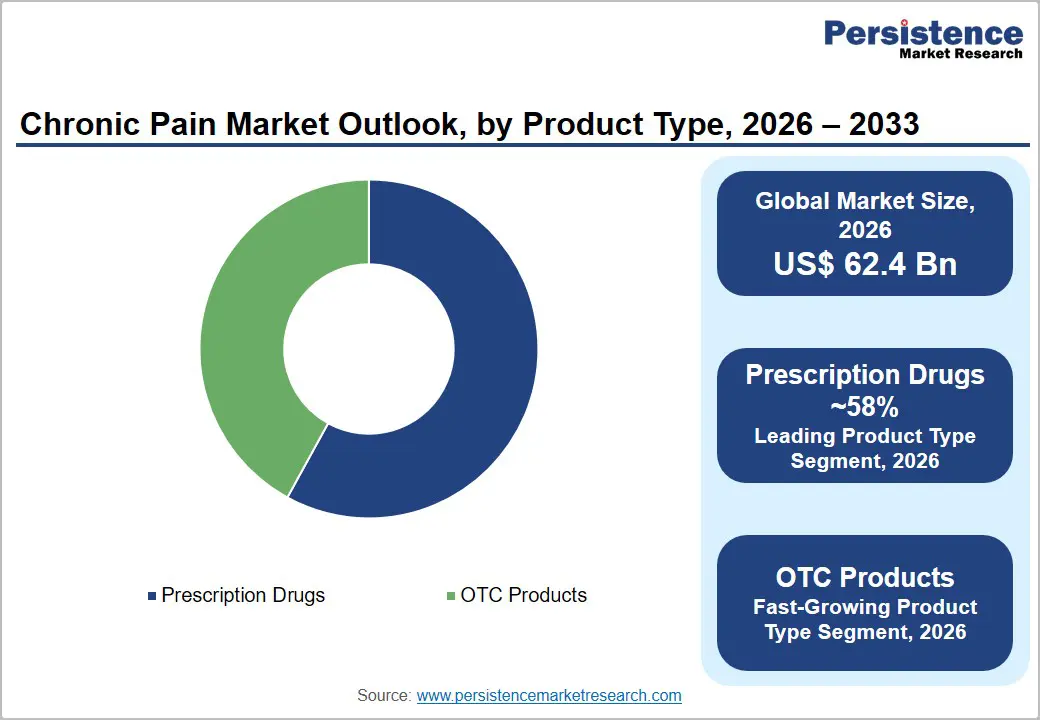

The global chronic pain market size is expected to be valued at US$ 62.4 billion in 2026 and projected to reach US$ 101.7 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The rising prevalence of musculoskeletal disorders, neuropathic pain, arthritis, cancer pain, and age-related chronic conditions worldwide has fuelled the demand for treating chronic pain. Rise in aging population and growing healthcare awareness are significantly expanding demand for prescription and over-the-counter pain management therapies.

According to the World Health Organization (WHO), ~20% of adults globally suffer from chronic pain, creating sustained long-term therapeutic demand. Additionally, healthcare systems are increasingly emphasizing non-opioid pain management approaches following stricter opioid prescribing regulations and updated clinical guidelines from organizations such as the CDC. Continuous innovation in targeted analgesics, topical therapies, and novel non-opioid drug development is further supporting chronic pain market expansion globally.

Key Industry Highlights

- Leading Region: North America holds ~38% market share, supported by high chronic pain prevalence, strong reimbursement systems, OTC analgesic demand, and innovative drug approvals.

- Fast-Growing Region: Asia Pacific records the fastest growth due to aging populations, rising chronic pain prevalence, expanding healthcare access, and increasing generic analgesic adoption.

- Dominating Product Segment: Prescription drugs dominate the market with ~59% share, driven by strong demand for neuropathic, cancer, and musculoskeletal pain management therapies.

- Fast-Growing Product Segment: OTC analgesics are growing rapidly due to rising self-care trends, expanding e-commerce pharmacies, convenient accessibility, and increasing non-opioid pain management preference.

- Key Opportunity: Non-opioid neuropathic pain therapies present major opportunities, supported by growing patient populations, innovative pipeline drugs, and increasing focus on targeted analgesic mechanisms.

Market Dynamics

Drivers - Rise in Global Burden of Chronic Pain and Aging Population

The growing prevalence of chronic pain worldwide is a major factor driving demand for chronic pain therapeutics. Rising incidence of musculoskeletal disorders, arthritis, diabetic neuropathy, cancer-related pain, and spinal conditions continues increasing the need for long-term pain management solutions. According to the Global Burden of Disease Study 2022, low back pain and musculoskeletal disorders remain among the leading causes of disability-adjusted life years (DALYs) globally.

In the United States, the National Institutes of Health (NIH) estimates that nearly 50 million adults suffer from chronic pain, while approximately 19.6 million experience high-impact chronic pain that significantly limits daily activities and work productivity.

The rapidly aging global population is further accelerating chronic pain prevalence and therapeutic demand. Older adults are more susceptible to degenerative joint diseases, osteoporosis, neuropathic conditions, and post-surgical pain requiring long-term treatment. The U.S. Census Bureau projects that adults aged 65 years and above will outnumber children under 18 by 2034, highlighting a major demographic shift supporting sustained pain management demand. Increasing healthcare utilization among elderly populations is expected to drive long-term growth across prescription analgesics, OTC pain therapies, and non-opioid chronic pain treatment solutions globally.

Restraints - Opioid Regulatory Restrictions and Prescribing Limitations

Strict regulatory controls surrounding opioid prescribing continue to restrain growth within the chronic pain therapeutics market. Governments and healthcare agencies globally are implementing tighter regulations to reduce opioid misuse, addiction, and overdose-related deaths. In the United States, the CDC’s 2022 Clinical Practice Guideline for Prescribing Opioids introduced stricter recommendations regarding opioid dosage, duration, and patient monitoring.

Additionally, the FDA’s Risk Evaluation and Mitigation Strategy (REMS) requirements for extended-release and long-acting opioids have increased compliance obligations for manufacturers and healthcare providers, limiting opioid prescription growth across multiple pain indications.

Regulatory tightening has also reduced commercial opioid production and supply availability. The U.S. Drug Enforcement Administration (DEA) has progressively lowered aggregate production quotas for Schedule II opioid medications to control distribution volumes. These restrictions are creating significant commercial challenges for companies heavily dependent on opioid-based pain portfolios. Pharmaceutical manufacturers are increasingly required to diversify product pipelines toward non-opioid analgesics, neuromodulation therapies, and targeted pain management solutions.

While these regulations improve patient safety and reduce abuse risks, they continue to place financial and operational pressure on the broader prescription chronic pain therapeutics market.

Opportunities - OTC Analgesic Innovation and the Self-Care Megatrend

The growing self-care trend and rising consumer preference for non-prescription pain management solutions are creating substantial opportunities within the OTC analgesics segment. Consumers are increasingly managing mild-to-moderate chronic pain independently through topical analgesics, oral pain relievers, patches, and gel-based therapies without frequent physician consultations.

According to the Consumer Healthcare Products Association (CHPA), the U.S. OTC analgesic category generates annual retail sales exceeding US$ 4 billion. Increasing awareness regarding self-medication convenience, affordability, and accessibility is supporting strong demand growth across retail pharmacies, supermarkets, and online healthcare platforms worldwide.

Innovation in OTC pain relief products is further accelerating market expansion. Pharmaceutical companies are developing advanced topical NSAIDs, sustained-release patches, and combination analgesic formulations with improved efficacy and enhanced skin penetration technologies. Additionally, the FDA’s Rx-to-OTC switch program is enabling several prescription pain therapies to transition into non-prescription availability, broadening patient access and commercial opportunities.

Expanding e-commerce pharmacy distribution and digital healthcare adoption are also strengthening OTC analgesic sales globally. Companies investing in innovative delivery formats and non-opioid consumer pain management products are expected to capture significant long-term growth opportunities within the chronic pain market.

Category-wise Analysis

Product Type Insights

Prescription drugs dominate the chronic pain market product type segment, commanding ~59% of total market revenue in 2026. This leadership reflects the clinical complexity and severity of chronic pain management particularly in neuropathic, cancer, and severe musculoskeletal pain indications where physician-supervised, regulated pharmaceutical interventions remain the standard of care. Branded prescription analgesics from Pfizer, AbbVie, and Johnson & Johnson command significant per-unit revenue premiums over OTC products.

The NIH's National Pain Strategy emphasizes individualized, multimodal prescription treatment approaches for high-impact chronic pain, sustaining clinician preference for prescription drug-based pain management protocols across hospital, specialty clinic, and long-term care settings globally.

Drug Class Insights

NSAIDs (Non-Steroidal Anti-Inflammatory Drugs) represent the dominant drug class segment, accounting for ~38% of the chronic pain drug class market in 2026. NSAIDs are the most broadly prescribed and utilized analgesic drug class globally, addressing inflammatory pain mechanisms across musculoskeletal disorders, arthritis, and post-operative pain.

The American College of Rheumatology (ACR) guidelines endorse NSAIDs as first-line pharmacological therapy for osteoarthritis and rheumatoid arthritis pain management. Generic ibuprofen, naproxen, and diclofenac dominate high-volume prescribing and OTC sales globally, while selective COX-2 inhibitors including Pfizer's Celebrex® (celecoxib) maintain significant prescription market share in patients requiring NSAID therapy with reduced gastrointestinal risk profiles.

Distribution Channel Insights

Retail pharmacies represent the leading distribution channel for chronic pain products, capturing ~44% of total channel revenue in 2026. Retail pharmacies including national chains such as CVS Health, Walgreens Boots Alliance, and Rite Aid in the U.S. serve as the primary dispensing point for both OTC analgesics and prescription chronic pain drugs at the community level, offering accessibility, convenience, and pharmacist counseling services. The National Community Pharmacists Association (NCPA) reports over 60,000 community pharmacies operating across the United States alone.

Retail pharmacy's dominant position is being reinforced by the rapid growth of in-store analgesic category management, loyalty programs, and telepharmacy integration, sustaining its channel leadership through the forecast period.

Regional Insights

North America Chronic Pain Market Trends and Insights

North America is likely to dominate the global chronic pain market, accounting for ~38% market share in 2026. The region benefits from high chronic pain prevalence, advanced healthcare infrastructure, strong insurance reimbursement systems, and widespread access to prescription and OTC analgesics. Increasing cases of arthritis, neuropathic disorders, cancer pain, and musculoskeletal conditions continue driving therapeutic demand. The post-opioid crisis landscape is also accelerating the transition toward non-opioid pain management therapies and innovative analgesics.

Additionally, strong pharmaceutical R&D investments and FDA approvals for novel pain treatments are supporting market expansion. Growing consumer preference for self-care and OTC pain relief products further strengthens regional market growth.

U.S. Chronic Pain Market Size

The United States represents ~87% of North America’s chronic pain market revenue in 2026, supported by a large patient population and strong pharmaceutical spending. According to NIH estimates, ~50 million Americans suffer from chronic pain, creating sustained demand for prescription and OTC analgesics. The country benefits from advanced reimbursement systems under Medicare and private insurance programs. Increasing adoption of non-opioid therapies and new drug approvals are further strengthening the market.

Additionally, strong retail analgesic sales, rising musculoskeletal disorders, and expanding pain management programs across hospitals and specialty clinics continue supporting long-term chronic pain therapeutics demand nationwide.

Europe Chronic Pain Market Trends and Insights

Europe represents the second-largest chronic pain therapeutics market globally, driven by well-established healthcare systems and broad reimbursement coverage for pain management therapies. Rising prevalence of musculoskeletal disorders, neuropathic pain, arthritis, and cancer-related pain continues supporting analgesic demand across the region. Countries including Germany, France, Italy, and the UK benefit from aging populations that require long-term chronic pain treatment.

Strong generic pharmaceutical manufacturing presence also improves affordability and accessibility of analgesics. Furthermore, increasing adoption of multimodal pain management strategies and clinical guidelines from organizations such as the European Pain Federation (EFIC) are encouraging wider use of non-opioid and targeted chronic pain therapies.

Germany Chronic Pain Market Size

Germany is likely to register ~21% of Europe’s chronic pain market revenue in 2026, supported by its strong healthcare reimbursement framework and advanced pharmaceutical sector. The country’s statutory health insurance system ensures broad patient access to prescription analgesics across hospitals, retail pharmacies, and outpatient settings. Rising elderly population and increasing prevalence of arthritis, neuropathic disorders, and musculoskeletal conditions continue driving demand for chronic pain therapies.

Germany also benefits from a strong generic drug manufacturing industry led by companies such as Teva and Stada, improving cost-effective analgesic availability. Continuous focus on pain management innovation and healthcare quality further supports market expansion across the country.

UK Chronic Pain Market Size

UK is likely to contribute ~16% of Europe’s chronic pain market revenue in 2026, driven by growing chronic disease prevalence and strong National Health Service (NHS) support for pain management programs. Chronic pain affects more than 28 million adults in the country, creating substantial demand for both branded and generic analgesics. NICE clinical guidelines continue supporting evidence-based treatment for neuropathic and musculoskeletal pain conditions.

Rising elderly population and increasing arthritis prevalence are further accelerating therapeutic demand. Additionally, expanding awareness regarding non-opioid pain management approaches and improved access to prescription therapies through public and private healthcare channels continue strengthening market growth.

Asia Pacific Chronic Pain Market Trends and Insights

Asia Pacific is the fastest-growing chronic pain market globally, driven by expanding healthcare infrastructure, rising pharmaceutical access, and increasing elderly population across major economies. Countries including China, India, Japan, and South Korea are witnessing growing prevalence of arthritis, neuropathic disorders, and cancer-related pain conditions.

Improving healthcare spending and broader insurance coverage are increasing patient access to prescription and OTC analgesics. Additionally, the region benefits from strong generic pharmaceutical manufacturing capabilities that improve affordability of pain therapies. Rising awareness regarding chronic pain management and growing adoption of non-opioid treatment approaches are further accelerating market growth across hospitals, clinics, and retail pharmacy channels.

India Chronic Pain Market Size

India represents ~12% of the Asia Pacific chronic pain market revenue in 2026, supported by its large patient population and rapidly growing pharmaceutical industry. According to the Indian Society for the Study of Pain (ISSP), ~190 million people in India suffer from chronic pain conditions. Rising prevalence of arthritis, lower back pain, cancer pain, and diabetic neuropathy is increasing demand for analgesic therapies nationwide. The country’s strong branded generic drug sector led by companies such as Sun Pharmaceutical and Cipla improves affordability and accessibility of pain medications.

Expanding healthcare infrastructure and growing awareness regarding chronic pain treatment continue supporting long-term market growth.

Japan Chronic Pain Market Size

Japan accounts for ~23% of Asia Pacific chronic pain market revenue in 2026, primarily driven by its rapidly aging population and high prevalence of musculoskeletal disorders. According to Statistics Japan, almost 30% of the country’s population is aged above 65 years, significantly increasing chronic pain treatment demand.

Japan has an advanced healthcare infrastructure and strong adoption of specialty prescription analgesics and interventional pain management therapies. Organizations such as the Japan Pain Clinic Society continue promoting multidisciplinary pain management approaches. Rising cases of arthritis, neuropathic pain, and osteoporosis-related conditions are further supporting sustained demand for chronic pain therapeutics across hospitals and specialty care centers.

Competitive Landscape

The global chronic pain market is moderately consolidated at the branded prescription tier, with major pharmaceutical companies including Pfizer Inc., AbbVie Inc., Johnson & Johnson, Novartis AG, Sanofi, and AstraZeneca maintaining significant branded analgesic revenue.

The generic segment is highly fragmented, with Teva Pharmaceutical, Sun Pharmaceutical, and Boehringer Ingelheim competing on cost and distribution scale. Key competitive differentiators include novel mechanism pipeline depth, non-opioid positioning, and chronic disease indication breadth. Emerging trends include patient-reported outcome (PRO) integration in trial designs for regulatory approval, digital pain management companion app development, and precision medicine biomarker approaches identifying patient subpopulations most likely to respond to targeted analgesics.

Key Developments:

- In September 2025, AbbVie submitted a New Drug Application (NDA) to the U.S. FDA for tavapadon, a once-daily oral selective dopamine D1/D5 receptor partial agonist developed for Parkinson’s disease treatment.

- In January 2025, Vertex Pharmaceuticals Incorporated announced that the U.S. FDA approved JOURNAVX™ (suzetrigine), an oral non-opioid NaV1.8 pain signal inhibitor for treating adults with moderate-to-severe acute pain.

Companies Covered in Chronic Pain Market

- Pfizer Inc.

- Hoffmann-La Roche AG

- AbbVie Inc.

- Johnson & Johnson (Janssen Pharmaceuticals)

- Novartis AG

- AstraZeneca

- Abbott

- Sanofi

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Bayer AG

- Boehringer Ingelheim International GmbH

- Endo, Inc.

- Vertex Pharmaceuticals Incorporated

- Others

Frequently Asked Questions

The global chronic pain market is estimated to be valued at US$ 62.4 billion in 2026.

Rising chronic pain prevalence, growing musculoskeletal disorders, expanding non-opioid drug development, increasing elderly population, and FDA approvals for innovative analgesics are strongly driving market demand.

North America leads the market due to high chronic pain prevalence, strong reimbursement systems, advanced healthcare infrastructure, and widespread adoption of prescription pain therapies.

Non-opioid neuropathic pain therapies represent the largest opportunity due to inadequate existing treatments, rising patient demand, and increasing late-stage pipeline drug development activities.

Major companies include Pfizer Inc., AbbVie Inc., Vertex Pharmaceuticals, Johnson & Johnson, Novartis AG, and Sanofi.