- Healthcare Services

- Lung Cancer Liquid Biopsy Market

Lung Cancer Liquid Biopsy Market Size, Share, and Growth Forecast, 2026 - 2033

Lung Cancer Liquid Biopsy Market by Sample Type (Blood, Cerebrospinal Fluid (CSF), Plasma, Serum, Others), Clinical Application (Early Cancer Screening, Therapy Selection, Treatment Monitoring, Recurrence Monitoring, Other Applications), and Regional Analysis for 2026 - 2033

Lung Cancer Liquid Biopsy Market Share and Trends Analysis

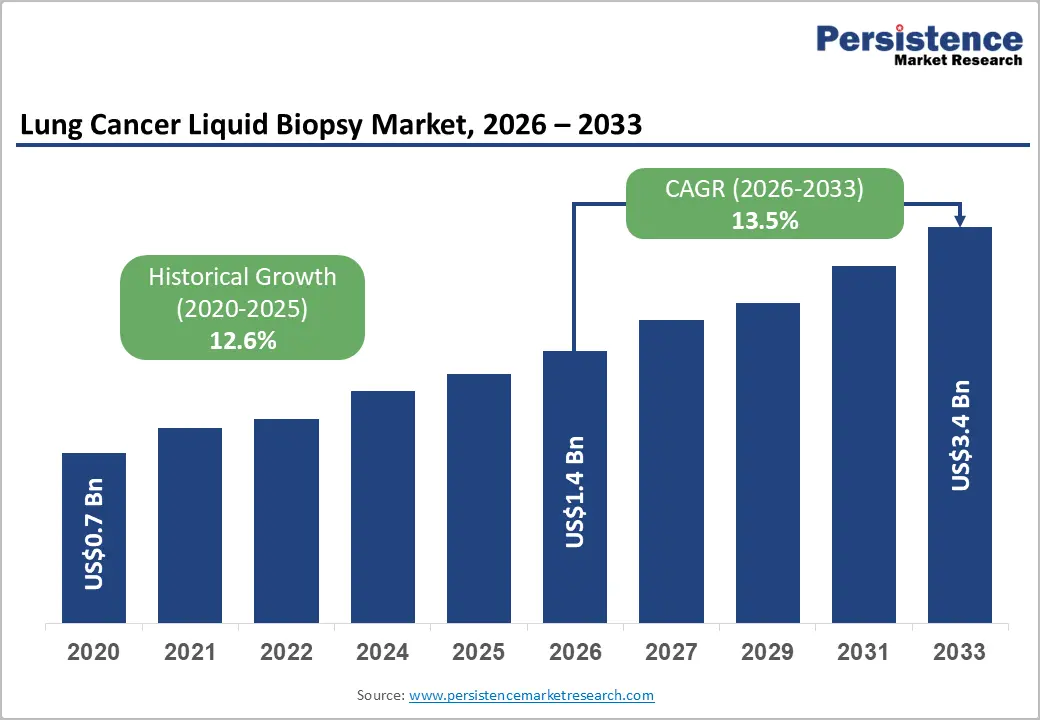

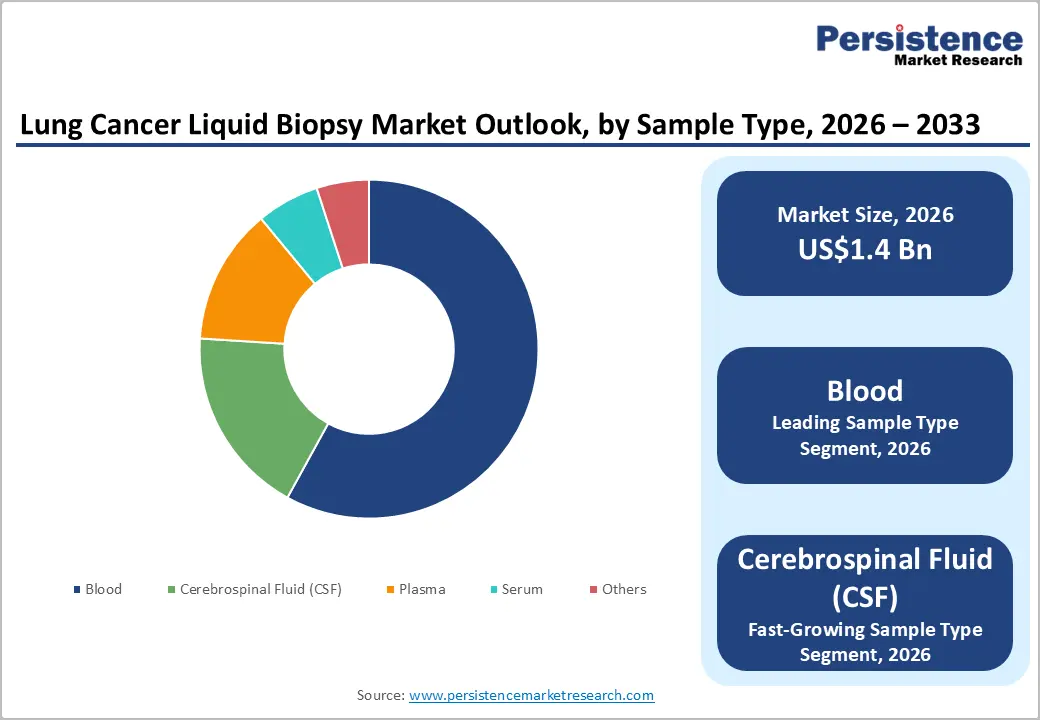

The global lung cancer liquid biopsy market size is likely to be valued at US$1.4 billion in 2026 and is estimated to reach US$3.4 billion by 2033, growing at a CAGR of 13.5% during the forecast period from 2026 to 2033, driven by demographic aging, rising cancer screening demand, expansion of precision oncology programs, regulatory acceleration for minimally invasive diagnostics, and broader clinical integration of genomic testing platforms.

Growth is reinforced by the increasing lung cancer burden linked to tobacco exposure and environmental pollution. Liquid biopsy adoption expands due to demand for early detection and therapy monitoring without invasive tissue sampling. Regulatory agencies, including the US Food and Drug Administration (FDA), are expanding companion diagnostic approvals, supporting clinical utility.

Key Industry Highlights:

- Leading Sample Type: Blood is set to hold around 58% revenue share in 2026, driven by widespread venipuncture adoption in serial treatment monitoring workflows.

- Fastest-growing Sample Type: Cerebrospinal fluid (CSF) is projected as the fastest-growing segment, driven by rising clinical evidence supporting CSF ctDNA analysis for CNS metastasis detection in advanced lung cancer.

- Leading Clinical Application: Therapy selection is estimated to hold roughly a 38% revenue share in 2026 due to integration in precision oncology workflows.

- Fastest-growing Application: Early cancer screening is forecast to record the fastest growth, driven by expanding national screening eligibility criteria and multi-cancer early detection product commercialization.

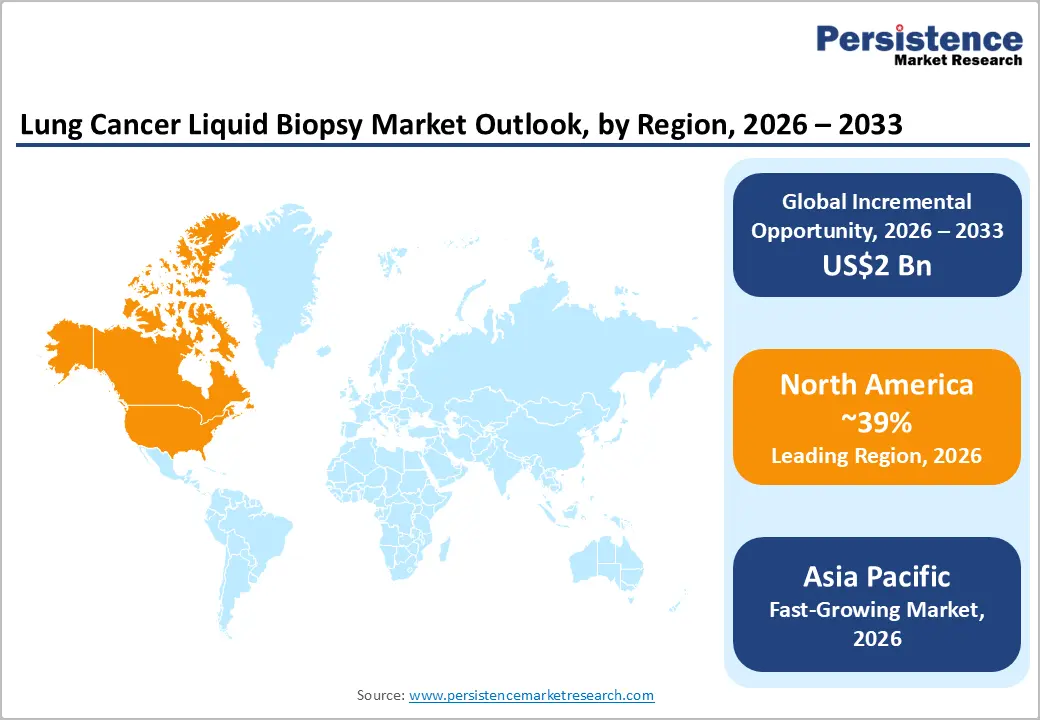

- Regional Leadership: North America is projected to capture roughly 39% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding cancer screening infrastructure.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Guardant Health and Foundation Medicine leveraging companion diagnostic approvals, reimbursement coverage, and integrated bioinformatics infrastructure to maintain competitive positioning.

DRO Analysis

Driver - Rising Lung Cancer Burden Amplified by Aging Demographics

The global increase in lung cancer cases is structurally linked to an aging population base, smoking prevalence in low- and middle-income countries, and occupational carcinogen exposure. The U.S. Centers for Disease Control and Prevention reported in 2025 that lung cancer remains the leading cause of cancer mortality in the U.S., with approximately 229,410 new diagnoses projected for that year. These case volumes create consistent clinical demand for early-stage detection tools that reduce diagnostic latency and improve patient stratification outcomes.

Aging patients frequently present with comorbidities that contraindicate invasive biopsy procedures. Liquid biopsy platforms address this clinical gap by delivering genomic profiling without procedural risk, enabling oncologists to make therapy decisions based on circulating tumor DNA data. This cause-and-effect relationship between patient frailty profiles and non-invasive diagnostic preference is a foundational driver for market adoption across hospital and outpatient settings.

Restraint - High Assay Development Costs Constraining Margin Scalability

Liquid biopsy assay development requires significant capital investment in sequencing infrastructure, bioinformatics pipelines, and clinical validation studies. These fixed cost structures compress margins, particularly for smaller diagnostic laboratories that lack the volume throughput to achieve economies of scale. The financial barrier limits competitive entry and concentrates market supply among a narrow set of well-capitalized players.

Laboratories operating in mid-income markets face compounded margin pressure as sequencing reagent costs are denominated in U.S. dollars while reimbursement rates are set in local currencies. Currency volatility and supply chain disruptions in semiconductor components used in sequencers further erode cost predictability, reducing capital allocation confidence among regional diagnostic operators considering capacity investments.

Opportunity - Multimodal Biomarker Integration for Early Detection Programs

Combining circulating tumor DNA with protein biomarkers, methylation signatures, and exosome-derived RNA into multimodal liquid biopsy panels represents a high-value growth pathway. Evidence from the National Cancer Institute-funded Circulating Cell-free Genome Atlas study demonstrated that multi-analyte panels achieved significantly higher sensitivity for early-stage lung cancer detection compared to single-biomarker approaches. Companies investing in panel development can command premium pricing in early screening markets and position products as population-level screening tools.

National lung cancer screening programs provide a policy infrastructure that multimodal panels can directly serve. The U.S. Preventive Services Task Force recommends annual low-dose CT screening for high-risk populations, but imaging capacity constraints in many health systems create an unmet demand for complementary blood-based pre-screening tools. Liquid biopsy panels capable of triaging CT referrals would address a concrete clinical bottleneck and unlock reimbursement pathways through risk-stratification billing codes.

Category-wise Analysis

Sample Type Insights

Blood sample is anticipated to secure around 58% of the lung cancer liquid biopsy market share in 2026, reflecting widespread clinical preference for minimally invasive venipuncture procedures that support serial monitoring without patient discomfort. Roche Diagnostics has commercialized blood-based ctDNA assays that are integrated into oncology treatment protocols across major cancer centers. This procedural simplicity, combined with established phlebotomy infrastructure in both hospital and outpatient settings, sustains blood as the dominant sample type across all clinical applications.

Cerebrospinal fluid (CSF) is expected to be the fastest-growing segment, propelled by growing evidence supporting CSF-derived ctDNA analysis for detecting central nervous system metastases in advanced lung cancer. Memorial Sloan Kettering Cancer Center has published clinical data demonstrating that CSF liquid biopsy outperforms plasma in detecting leptomeningeal disease. Rising adoption of next-generation sequencing in neurological oncology units is expanding CSF collection protocols, creating demand for specialized assay kits optimized for low-volume, high-sensitivity Central Nervous System (CNS) biomarker detection.

Biomarker Insights

Circulating nucleic acids are poised to dominate with a forecast market share of over 47% in 2026, powered by the clinical validation of cell-free DNA and cell-free RNA as reliable indicators of tumor mutational burden and treatment resistance emergence. Guardant Health's Guardant360 CDx, a commercially deployed circulating nucleic acid panel, illustrates the segment's clinical maturity and payer acceptance. Established sequencing workflows for circulating nucleic acid extraction and the availability of standardized library preparation kits accelerate laboratory adoption and support consistent diagnostic throughput.

Exosomes/Microvesicles are estimated to be the fastest-growing segment, fueled by emerging evidence that tumor-derived exosomes carry protein, RNA, and DNA cargo that provides complementary genomic information to plasma ctDNA. Researchers at MD Anderson Cancer Center demonstrated exosome-based biomarker signatures capable of distinguishing lung adenocarcinoma subtypes with high specificity. Advances in size-exclusion chromatography and microfluidic isolation technologies are reducing exosome purification complexity, enabling laboratories to integrate exosome profiling into existing diagnostic pipelines without prohibitive capital investment.

Clinical Application Insights

Therapy selection is likely to be the leading segment with a projected 38% of the lung cancer liquid biopsy market share in 2026, due to the critical role of biomarker-guided treatment decisions in targeted oncology, where liquid biopsy results determine eligibility for EGFR (Estimated Glomerular Filtration Rate) inhibitors, ALK (Anaplastic Lymphoma Kinase) inhibitors, and immunotherapy regimens. Foundation Medicine's companion diagnostic approvals for Non-Small Cell Lung Cancer (NSCLC) therapies exemplify this clinical utility.

Early cancer screening is anticipated to be the fastest-growing segment, fueled by growing clinical recognition that detecting lung cancer at stages I and II dramatically improves five-year survival rates, creating institutional pressure to develop blood-based screening alternatives to low-dose CT. Grail's Galleri multi-cancer early detection test, which includes lung cancer signals, has entered commercial deployment in the U.S. and the U.K.

Regional Insights

North America Lung Cancer Liquid Biopsy Market Trends

North America is expected to lead with an estimated 39% of the lung cancer liquid biopsy market share in 2026, supported by advanced oncology infrastructure, broad adoption of precision medicine, strong reimbursement frameworks, and extensive utilization of genomic testing. The growing integration of liquid biopsy into cancer screening and therapy monitoring programs continues to strengthen demand.

U.S. Lung Cancer Liquid Biopsy Market Insights

The U.S. is projected to account for nearly 82% of the North America market in 2026, driven by strong FDA support for companion diagnostics, extensive oncology research funding, and widespread availability of molecular testing services. The growing adoption of circulating tumor DNA analysis in therapy selection and treatment monitoring is supporting clinical utilization. Expansion of pharmaceutical clinical trials is further increasing demand for biomarker-based diagnostics.

Canada Lung Cancer Liquid Biopsy Market Insights

Canada is forecast to hold approximately 18% of the North America market in 2026, supported by the expansion of publicly funded cancer care programs and increasing adoption of precision oncology initiatives. Provincial healthcare systems are incorporating molecular diagnostic technologies into oncology pathways. Research collaborations between academic institutions and diagnostic companies are improving access to advanced testing solutions.

Europe Lung Cancer Liquid Biopsy Market Trends

Europe is expected to account for approximately 28% of the lung cancer liquid biopsy market share in 2026, supported by strong regulatory frameworks, increasing investment in cancer diagnostics, and growing implementation of personalized medicine strategies. Expansion of genomic medicine programs across healthcare systems is encouraging wider adoption of non-invasive testing technologies. Continuous investment in oncology infrastructure is strengthening market growth.

Germany Lung Cancer Liquid Biopsy Market Insights

Germany is expected to contribute nearly 24% of the Europe market in 2026, supported by a strong diagnostic manufacturing base, advanced healthcare infrastructure, and increasing utilization of molecular oncology testing. Expansion of precision medicine initiatives is driving demand for liquid biopsy solutions. Collaboration between healthcare providers and diagnostic companies is supporting clinical integration.

U.K. Lung Cancer Liquid Biopsy Market Insights

The U.K. is likely to represent around 19% of the Europe market in 2026, driven by growing adoption of genomic testing within National Health Service programs and increasing focus on early cancer detection. National research initiatives are supporting the validation of liquid biopsy technologies. Expansion of cancer screening pathways is contributing to market development.

Asia Pacific Lung Cancer Liquid Biopsy Market Trends

Asia Pacific is forecast to be the fastest-growing market for lung cancer liquid biopsy, stimulated by rising lung cancer incidence, expanding healthcare infrastructure, and increasing government investment in advanced diagnostics. Rapid growth in precision medicine adoption and broader access to molecular testing are creating favorable conditions for market expansion. Development of regional biotechnology capabilities is strengthening supply chains and innovation activities.

China Lung Cancer Liquid Biopsy Market Insights

China is projected to account for approximately 41% of the Asia Pacific market in 2026, supported by large-scale cancer screening initiatives, expansion of molecular diagnostic laboratories, and increasing healthcare expenditure. Government-backed healthcare reforms are improving accessibility to advanced cancer diagnostics. Growth in domestic biotechnology innovation is accelerating adoption of liquid biopsy technologies.

India Lung Cancer Liquid Biopsy Market Insights

India is forecast to contribute nearly 15% of the Asia Pacific market in 2026, driven by expanding private diagnostic networks, rising oncology awareness, and increasing investment in specialty cancer care centers. The growing availability of genomic testing services is supporting adoption across urban healthcare facilities. Strategic partnerships between hospitals and diagnostic providers are enhancing testing accessibility.

Competitive Landscape

The global lung cancer liquid biopsy market is moderately consolidated, with a small group of specialized diagnostic companies commanding the majority of clinical adoption and companion diagnostic partnerships. Guardant Health, Foundation Medicine (a Roche subsidiary), Illumina, Exact Sciences, and Grail collectively maintain strong positions through FDA-approved platforms, established payer reimbursement coverage, and integrated bioinformatics capabilities that smaller entrants cannot replicate at equivalent cost.

Market structure is influenced by the regulatory capital required to obtain companion diagnostic designations and the long clinical validation timelines needed to demonstrate analytical equivalence to tissue biopsy. These structural barriers sustain incumbent advantage while creating partnership opportunities for emerging players who possess novel biomarker intellectual property but lack commercial-scale laboratory infrastructure or regulatory affairs resources to navigate approval processes independently.

Key Industry Developments:

- In May 2026, GRAIL reported NHS-Galleri trial results at the 2026 ASCO Annual Meeting, demonstrating a substantial reduction in late-stage cancer diagnoses and reinforcing the clinical potential of liquid biopsy technologies for earlier detection of lung and other high-mortality cancers.

- In June 2025, Guardant Health received FDA Breakthrough Device Designation for its Shield Multi-Cancer Detection blood test, strengthening the advancement of liquid biopsy technologies for early detection of lung cancer and other high-mortality malignancies through a single blood draw.

Companies Covered in Lung Cancer Liquid Biopsy Market

- Guardant Health

- Roche

- Grail (Illumina)

- Exact Sciences

- Thermo Fisher Scientific

- Qiagen

- Bio-Rad Laboratories

- Burning Rock Biotech

- Berry Oncology

- Sysmex Inostics

- Biocept

- Menarini Silicon Biosystems

- Angle plc

- Veracyte

Frequently Asked Questions

The global lung cancer liquid biopsy market is projected to reach US$1.4 billion in 2026.

Rising prevalence of lung cancer, increasing adoption of precision oncology, and growing demand for minimally invasive early detection and treatment monitoring solutions drive the lung cancer liquid biopsy market.

The lung cancer liquid biopsy market is poised to witness a CAGR of 13.5% from 2026 to 2033.

Expansion of multi-cancer early detection programs, broader companion diagnostic applications, and advancements in circulating tumor DNA analysis create significant opportunities in the lung cancer liquid biopsy market.

Some of the key market players include Guardant Health, Foundation Medicine (a Roche subsidiary), Illumina, Exact Sciences, and Grail.