- Bulk Chemicals

- Barium Carbonate Market

Barium Carbonate Market Size, Share, and Growth Forecast 2026 - 2033

Barium Carbonate Market by Form (Granular, Powder, Ultra-fine, Others), Source (Natural, Synthetic), Application (Bricks & Tiles, Specialty Glass, Electro-ceramics, Glazes & Enamels, Chemical Compounds, Others), Industry (Construction, Glass Manufacturing, Electronics, Chemical Industry, Oil & Gas, Others), and Regional Analysis for 2026 - 2033

Barium Carbonate Market Size and Trend Analysis

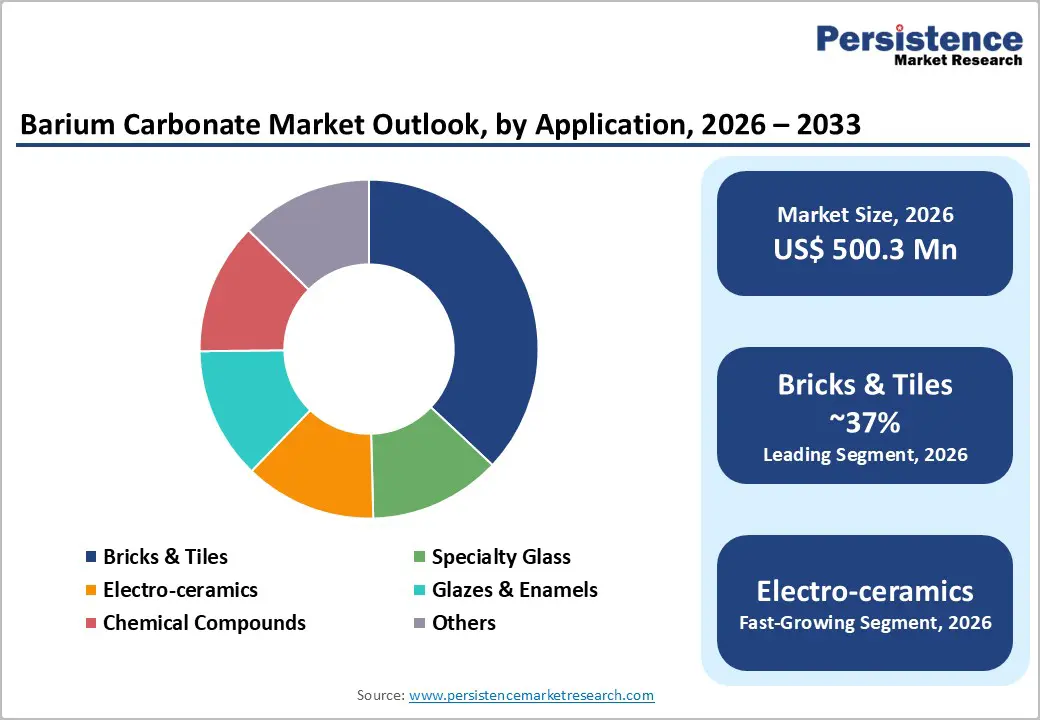

The global barium carbonate market is valued at US$ 500.3 million in 2026 and is projected to reach US$ 708.7 million by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The market growth is primarily propelled by accelerating demand from the construction ceramics sector, expanding specialty glass manufacturing, and the rising deployment of electro-ceramic components in advanced electronics. The construction industry, a principal consumer through brick and tile manufacturing, benefits from rapid urbanization across emerging economies, particularly in the Asia Pacific and Latin America. Concurrently, the proliferation of 5G networks and electric vehicle adoption is driving unprecedented demand for multilayer ceramic capacitors (MLCCs), which rely on high-purity barium carbonate as a precursor material, further reinforcing the market's upward trajectory through 2033.

Key Industry Highlights:

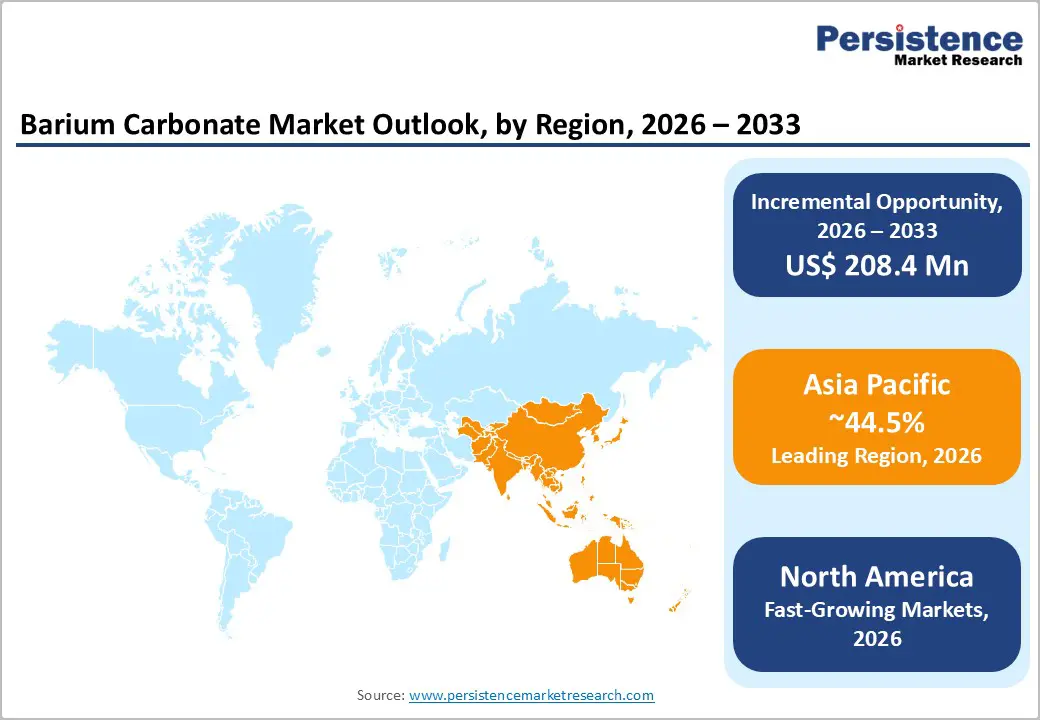

- Leading Region: Asia Pacific dominates the global Barium Carbonate market with 44.5% share in 2026, driven by China's integrated ceramics and tile manufacturing ecosystem, Japan's electronics-grade specialization, and India's expanding construction sector.

- Fastest Growing Region: North America is the fastest-growing region, with the United States driving regional demand through its mature glass manufacturing, electronics assembly, and specialty chemicals industries.

- Dominant Form Segment: Granular form holds the leading 42% share in the product form category, owing to superior handling properties, batch consistency, and reduced occupational dust exposure, making it the preferred grade for ceramic and glass kilns.

- Fastest Growing Segment: Electro-ceramics is the fastest growing application segment at 8.19% CAGR, fueled by soaring MLCC demand for 5G infrastructure, AI servers, and electric vehicle power electronics requiring high-purity barium titanate precursors.

- Key Opportunity: Ultra-fine and electronic-ceramic grade barium carbonate represents the most lucrative growth opportunity, as semiconductor miniaturization mandates sub-500 nm particles and trace contaminants below 50 ppm, commanding significant premium pricing.

| Key Insights | Details |

|---|---|

| Barium Carbonate Market Size (2026E) | US$ 500.3 Mn |

| Market Value Forecast (2033F) | US$ 708.7 Mn |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Surging Demand from the Global Construction and Ceramics Sector

The construction and ceramics industries remain the most significant demand drivers for barium carbonate worldwide. Barium carbonate is an essential additive in brick and tile manufacturing, functioning as an anti-scumming agent by reacting with soluble sulfate compounds to prevent unsightly efflorescence on masonry surfaces. As per data from Oxford Economics, global construction activity is anticipated to reach US$ 9.6 trillion in 2024, rising to US$ 9.9 trillion by 2025 and growing at a CAGR of 3.6% from 2025 to 2027.

Rapid urban development in cities like Jakarta, Manila, and São Paulo, where urbanization rates exceed 3% per year, translates directly into higher tile and brick consumption. In 2023, the Chinese ceramic tile industry reported a 6.2% year-on-year export growth, rising from 579 million sqm in 2022 to 615 million sqm in 2023, as per Ceramic World Web. This continued growth in ceramic tile production directly amplifies the consumption of barium carbonate globally.

Rapid Expansion of Electronics and Electro-ceramic Applications

The global electronics industry, particularly the multilayer ceramic capacitor (MLCC) segment, is emerging as a high-growth end-use driver for ultra-high-purity barium carbonate. Barium carbonate serves as a critical precursor in the synthesis of barium titanate (BaTiO3), the core dielectric material in MLCCs.

Advanced smartphones now integrate between 700 and 1,000 MLCC units per device, while modern ADAS-equipped vehicles require over 3,000 MLCCs each. The GSMA estimates that 5G networks will cover one-third of the world's population by 2025, supporting over 2 billion 5G connections. This structural shift in electronics manufacturing ensures sustained, long-term demand for high-purity electro-ceramic grade barium carbonate.

Restraints - Regulatory Pressure and Environmental Toxicity Concerns

Barium carbonate presents notable toxicity challenges that have prompted increasingly stringent regulatory scrutiny. In 2024, the European Union implemented stricter regulations requiring manufacturers handling barium compounds to adhere to enhanced safety and handling standards. Workplace exposure limits are being tightened across North America and Europe, adding compliance costs for manufacturers. This regulatory pressure disproportionately affects small and mid-tier producers that lack the resources to invest in enclosed-handling equipment or process redesigns, potentially constraining production capacity and market competitiveness in regulated markets.

Raw Material Price Volatility

Barium carbonate is synthesized primarily from barite (barium sulfate), a mineral whose pricing is subject to supply chain disruptions and geographic concentration. China dominates global barite output, and any disruption in Chinese mining or export policy can significantly impact global barium carbonate pricing. According to the World Integrated Trade Solution (WITS), China was the leading exporter of barium carbonate in 2023, with exports valued at US$ 60.63 million and a volume of 90.26 million kg. This heavy geographic concentration of production creates supply chain vulnerabilities that dampen price stability, posing profitability challenges for downstream manufacturers.

Opportunities - Rising Demand for Ultra-Fine Barium Carbonate in Semiconductor and Advanced Ceramics

The fastest-growing opportunity within the barium carbonate market lies in ultra-fine and high-purity grades, which are indispensable for advanced electronic and electro-ceramic manufacturing. As chip geometries shrink and switching frequencies rise, MLCC manufacturers require barium carbonate with trace contaminants below 50 ppm and particle sizes below 500 nm to maintain dielectric consistency.

Research published by the Royal Society of Chemistry in April 2024 demonstrated controllable precipitation strategies to produce BaCO3 nano- and microcarriers for advanced imaging applications, highlighting the growing scientific and commercial interest in precision barium compounds. Companies such as Sakai Chemical Industry Co., Ltd. and Nippon Chemical Industrial Co., Ltd. are already investing in R&D for high-purity grades, as highlighted in Nippon Chemical Industrial's Integrated Report 2024. Producers who can consistently deliver ultra-high-purity, particle-controlled grades are positioned to capture significant premium revenue within the electro-ceramics supply chain.

Infrastructure and Housing Programs in Emerging Economies

Developing economies across South Asia, Southeast Asia, and Sub-Saharan Africa represent a substantial and underpenetrated growth frontier for barium carbonate producers. Governments in countries such as India, Vietnam, and Indonesia are executing large-scale public housing and infrastructure programs that fuel demand for construction ceramics. India's construction chemicals market alone is projected to add INR 500 crore in turnover by 2028.

Furthermore, grants of €5 million and €4.5 million were awarded for 3D-printed ceramics development in Europe, alongside €30 million raised by Cerafiltec for capacity expansion, signaling accelerated investment in high-performance ceramics. Barium carbonate producers that establish cost-efficient production capacity close to these emerging markets will benefit from strong, sustained volume growth in the coming years.

Category-wise Analysis

Form Insights

Among all product forms, granular barium carbonate commands the dominant position in the market, accounting for approximately 42% of global revenue in 2024. The dominance of this form stems from its superior flowability and uniform mixing behavior, which are operationally critical in large-scale kilns used across ceramics, glass, and brick manufacturing. Granular barium carbonate offers reduced dust emissions compared to powders, aligning with tightening occupational health standards, particularly in the European Union and North American workplaces.

Industries favor granular material for its cleaner dosing, batch consistency, and reduced risk of surface defects in high-temperature ceramic firing. Ultra-fine barium carbonate, though a smaller segment, is the fastest-growing form, projected to advance at an 8.06% CAGR through 2030, driven by increasing specifications from MLCC and semiconductor-grade ceramic producers that demand sub-micron particle sizes and exceptional chemical purity.

Source Insights

Synthetic barium carbonate holds a commanding ~76% share of the global market in 2026, significantly outpacing naturally sourced varieties. The preference for synthetic grades is underpinned by consistently superior chemical purity, controlled particle morphology, and reproducible physical properties compared to naturally mined witherite. Synthetic production routes, principally the reaction of barium sulfide with carbon dioxide or soda ash, afford manufacturers full control over particle size distribution, residual sulfate levels, and heavy-metal contaminants, which are critical parameters for electro-ceramic and glass-grade applications.

Industries in Japan, South Korea, and Taiwan, where electronics-grade material standards are stringent, rely entirely on synthetic barium carbonate. As global demand continues migrating toward higher-value applications requiring consistent lot-to-lot performance, the synthetic segment is expected to further consolidate its dominant position through 2033.

Application Insights

Within the application landscape, the Bricks & Tiles segment holds the leading position with approximately 37% of total revenue. Barium carbonate's function as an anti-scumming agent, neutralizing soluble sulfates that would otherwise form white efflorescent deposits on fired masonry, makes it an indispensable additive in brick and tile production. Its role in improving color uniformity and frost resistance further cements its essentiality for quality-oriented manufacturers. Sustained construction activity across both residential and commercial real estate segments globally continues to generate steady tonnage demand.

The Electro-ceramics segment is the fastest-growing application, with a projected CAGR of 8.19% through 2030, driven by expanding MLCC production for 5G base stations, AI servers, and electric vehicle power electronics. Specialty Glass remains the second-largest application, benefiting from rising volumes of optical, solar, and automotive display glass.

End-use Industry Analysis

The Construction industry leads all end-use segments, capturing approximately 44% of global barium carbonate revenue. The sector's dominance reflects the scale of global building activity, encompassing residential housing, commercial infrastructure, and public works that collectively require enormous volumes of bricks, tiles, and ceramic components. According to Oxford Economics, total global construction output is expected to sustain a CAGR of 3.6% from 2025 to 2027, underpinning steady demand.

The Electronics end-use segment is the fastest growing, advancing at a projected 8.48% CAGR through 2030. This growth is driven by the structural shift toward digitalization, smart manufacturing, and electromobility, all of which depend on ceramic passive components produced from barium carbonate precursors. The Chemical Industry and Oil & Gas sectors represent smaller but stable demand pockets, utilizing barium carbonate as a precursor to various barium salts used in drilling muds and water treatment.

Regional Insights

North America Barium Carbonate Market Trends

North America continues to represent a substantial market for barium carbonate, with the United States driving regional demand through its mature glass manufacturing, electronics assembly, and specialty chemicals industries. The region maintains rigorous quality standards for high-purity barium carbonate, particularly for semiconductor-related and optical glass applications. Moreover, the U.S. CHIPS and Science Act has intensified domestic semiconductor investments, with over US$ 200 billion committed to new fabrication facilities through 2030, thereby reinforcing demand for high-purity electro-ceramic inputs.

The market is further supported by approximately 919,000 construction establishments as of Q1 2023, sustaining consistent brick and tile consumption. Additionally, evolving U.S. trade policies and revised tariff structures in 2025 have prompted importers to diversify sourcing away from China, increasingly favoring India and domestic suppliers.

Europe Barium Carbonate Market Trends

Europe’s barium carbonate market is shaped by stringent regulatory frameworks and a longstanding industrial foundation. Germany, Italy, and Spain serve as key demand hubs, supported by advanced ceramics, specialty glass production, and high-performance materials manufacturing. Recent enhancements to EU REACH regulations and the 2024 updates to barium compound safety standards have elevated compliance requirements, prompting greater investment in low-emission granular grades and enclosed-process technologies.

European tile manufacturers are also piloting hydrogen-ready kilns to align with EU Green Deal decarbonization objectives, generating additional demand for low-firing-temperature flux additives. The United Kingdom and France further contribute through automotive glass and specialty coatings. Strategic shifts, including Solvay S.A.’s 2024 divestiture to Latour Capital and Cerafiltec’s €30 million expansion, underscore ongoing regional investment in advanced ceramic materials.

Asia Pacific Barium Carbonate Market Trends

The Asia Pacific region holds a dominant position in the global barium carbonate market, accounting for approximately 44.5% of total demand in 2026. This leadership is primarily driven by China’s vertically integrated production framework and its strong presence in ceramics and electronics manufacturing. China alone exported 90.26 million kg of barium carbonate in 2023, valued at US$60.63 million, underscoring its status as the world’s largest producer and exporter.

Japan contributes significantly through its supply of high-purity grades for MLCC production, supported by ongoing investments from companies such as Sakai Chemical Industry and Nippon Chemical Industrial. India is rapidly emerging as a production hub, with expanding capacities aimed at both domestic and export markets. The region is projected to grow at a robust 9.02% CAGR through 2030, further reinforced by increased electro-ceramic demand following TSMC’s Kumamoto fab launch in 2024.

Competitive Landscape

The global barium carbonate market exhibits a moderately fragmented structure, with a mix of large-scale integrated chemical companies, specialty producers, and regional distributors. Asia Pacific producers, particularly from China and Japan, dominate volume production, while European and North American players differentiate through product quality, purity grades, and regulatory compliance. Key competitive strategies include vertical integration into barite mining to secure raw material supply, investment in granulation and ultra-fine milling technologies, and targeted M&A activity to consolidate market share. Companies increasingly compete on lot-to-lot chemical consistency and purity certifications rather than price alone, particularly in the fast-growing electro-ceramic and semiconductor-adjacent segments.

Key Developments:

- October 2025: Guizhou Redstar Co., Ltd. Launches new 6,000-ton/year high-purity barium carbonate project. To meet the market demand, Guizhou Redstar Co., Ltd. proposed an investment of 503Mn yuan in the construction of a 6,000-ton-per-year high-purity barium carbonate project within the existing plant area.

- December 2025: Nippon Chemical Industrial and TDK signed a basic agreement to begin discussions on a joint venture (JV) for material development. The objective is to explore the establishment of a joint venture for the development of electronic component materials, specifically ceramic materials for multilayer ceramic chip capacitors (MLCCs), and associated manufacturing processes.

- January 2026: The European Commission imposed definitive anti-dumping duties via Commission Implementing Regulation (EU) 2026/71 on barium carbonate from China and India, published on 13 January 2026. All provisional duties collected under EU 2025/1724 are to be definitively collected, with excess amounts secured above the definitive rates to be released.

Top Companies in Barium Carbonate Market

- Solvay S.A. (Belgium) is a global specialty chemicals leader with over 160 years of industrial heritage. Until the 2024 divestiture, it was a leading European barium carbonate producer supplying glass, ceramics, and chemical applications. With reported group revenues of approximately €4.3 billion in 2025, Solvay leverages its global distribution network and deep application expertise to serve regulated industrial markets. Its strategic portfolio restructuring underscores a broader trend of specialization within the chemicals sector.

- Sakai Chemical Industry Co., Ltd. (Japan) is a premier Japanese specialty chemicals company and one of the most technically advanced barium carbonate producers globally. The company is a critical supplier to the MLCC and electro-ceramic manufacturing ecosystem across Japan, South Korea, and Taiwan. Sakai's core competitive advantage lies in sub-500 nm particle precision, ultra-high purity, and exceptional lot-to-lot consistency tailored for high-frequency and miniaturized capacitor applications.

- Shaanxi Ankang Jianghua Group Co., Ltd. (China) is one of China's largest barium carbonate producers, operating a vertically integrated supply chain from barite mining through chemical conversion to finished barium compounds. The company serves primarily the domestic Chinese market for construction ceramics, glass, and chemical intermediates, while also exporting to the Asia Pacific markets. Its scale and cost efficiency position it as a high-volume benchmark supplier for granular and standard-grade barium carbonate.

Companies Covered in Barium Carbonate Market

- Honeywell International Inc.

- Sakai Chemical Industry Co., Ltd.

- Nippon Chemical Industrial Co., Ltd.

- Shaanxi Ankang Jianghua Group Co., Ltd.

- Hebei Xinji Chemical Group Co., Ltd.

- Chemical Products Corporation

- Hubei Jingshan Chutian Barium Salt Corp. Ltd.

- American Elements

- AG Chem Group

- Guizhou Redstar Developing Co., Ltd.

- Brenntag North America Inc.

Frequently Asked Questions

The global Barium Carbonate market is valued at US$ 500.3 Mn in 2026 and is projected to reach US$ 708.7 Mn by 2033, growing at a CAGR of 5.1% during the forecast period 2026-2033. The historical CAGR from 2020 to 2025 stood at 4.6%, reflecting steady foundational demand from construction ceramics and specialty glass.

The two primary growth drivers are the rapid expansion of the global construction and ceramics industries, supported by rising urbanization in the Asia Pacific and Latin America, and the accelerating adoption of electro-ceramics and MLCC components in 5G, AI server, and electric vehicle applications. Global construction output is projected to surpass US$ 9.9 trillion by 2025, while the MLCC market is expected to reach US$ 18 billion by 2033.

Granular barium carbonate is the leading segment by form, accounting for approximately 42% of total market revenue in 2026. Its leadership is attributed to superior flowability, batch consistency, and compliance with occupational health standards, making it the preferred choice for high-temperature ceramic and glass manufacturing processes.

Asia Pacific is the leading region, capturing approximately 44.55% of global demand in 2026. The region's leadership reflects China's large-scale ceramics production, Japan's specialization in electronics-grade barium compounds, and India's rapidly expanding construction sector.

The most significant opportunity lies in the ultra-high-purity and ultra-fine barium carbonate segment, serving the semiconductor-grade electro-ceramic supply chain. As MLCC miniaturization advances and specifications demand particle sizes below 500 nm with trace metal contaminants below 50 ppm, producers capable of consistently meeting these exacting standards can capture substantial premium margins in the growing electronics manufacturing ecosystem.

Leading players in the global Barium Carbonate market include Solvay S.A., Sakai Chemical Industry Co., Ltd., Shaanxi Ankang Jianghua Group Co., Ltd., Honeywell International Inc., Nippon Chemical Industrial Co., Ltd., Hebei Xinji Chemical Group Co., Ltd., Chemical Products Corporation, and American Elements, among others.