- Hardware & Software IT Services

- Audit Management Software Market

Audit Management Software Market Size, Share, and Growth Forecast, 2026 - 2033

Audit Management Software Market by Component (Solutions, Services), Deployment Type (On-Premises, Cloud), Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, Government, Energy & Utilities, IT & Telecom, Others), and Regional Analysis for 2026 - 2033

Audit Management Software Market Share and Trends Analysis

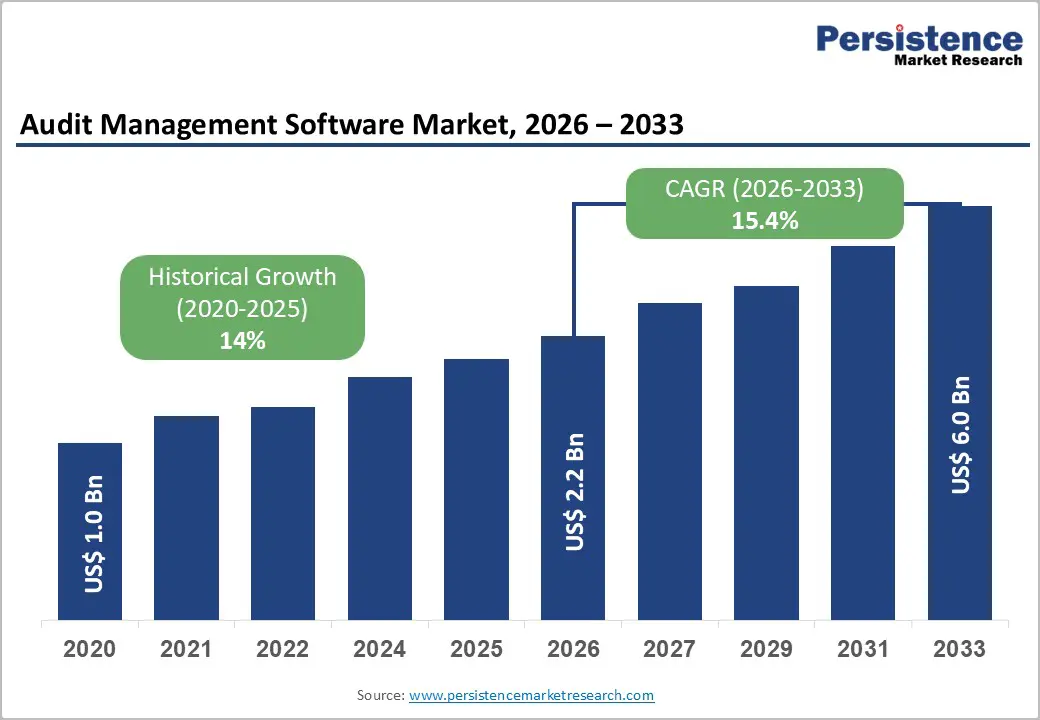

The global audit management software market size is likely to be valued at US$ 2.2 billion in 2026, and is projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 15.4% during the forecast period 2026−2033. Driving market expansion are the increasing complexity of regulatory requirements, the growing demand for real-time auditing, and the rapid adoption of cloud-based technologies.

As industries face heightened scrutiny and a greater need for robust risk management and compliance frameworks, audit management software become indispensable. Technological advancements in artificial intelligence (AI) and machine learning (ML) are further improving audit efficiency, reducing risks, and providing actionable insights, which are accelerating market growth. These combined trends are pushing businesses across various sectors to adopt more advanced and automated audit solutions, contributing to the continued expansion of the market.

Key Industry Highlights

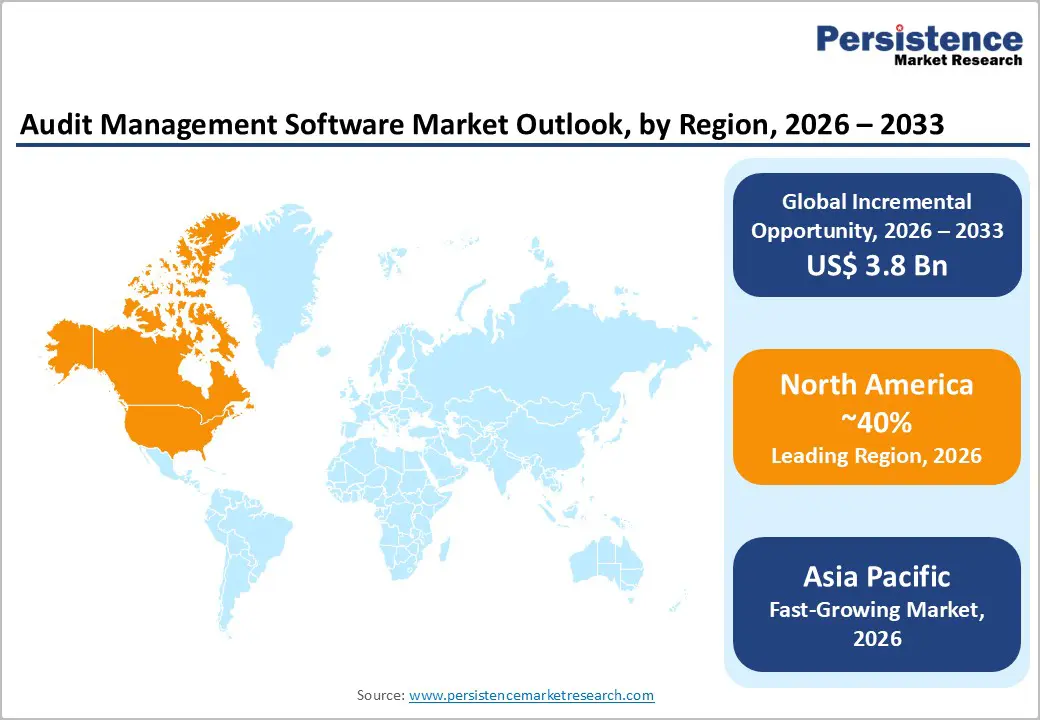

- Dominant Region: North America is predicted to hold a 40% market share in 2026, driven by a strong regulatory environment and advanced technological infrastructure.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, fueled by rapid digital transformation and increasing regulatory pressures.

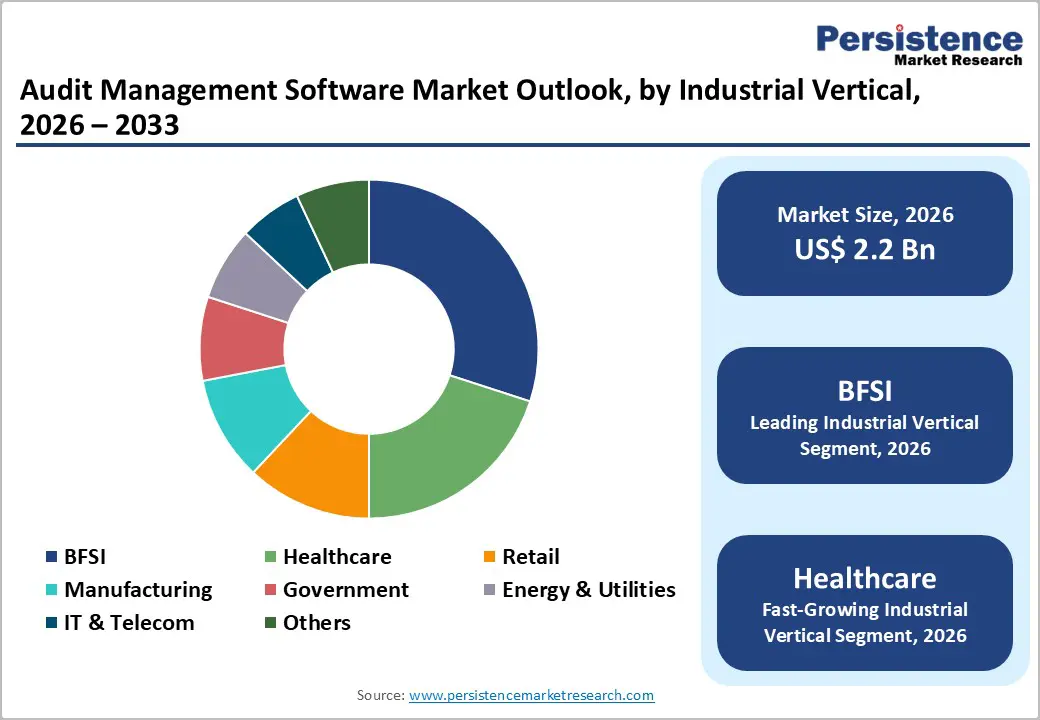

- Leading Industry Vertical: The BFSI sector is likely to lead with about 30% market share in 2026 due to increasing regulatory pressures, the need for stringent auditing, and compliance requirements.

- Fastest-growing Industry Vertical: The healthcare sector is slated to grow the fastest through 2033, on account of rising regulatory scrutiny and the heightened urgency for enhanced data protection.

- July 2025: Deloitte announced new generative AI (GenAI) capabilities and AI agents in its Omnia cloud-based global audit platform to automate tasks, detect anomalies, and enhance auditor efficiency.

| Key Insights | Details |

|---|---|

|

Audit Management Software Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 6.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

15.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Regulatory Compliance Requirements

As digitalization trends have picked up pace across industries, regulatory compliance requirements have grown stringent in tandem over the past decade, proving to be a primary driver of the audit management software market growth. With governments and industry bodies imposing stricter rules, businesses are under constant pressure to ensure they adhere to ever-evolving standards. This creates a need for automated, streamlined solutions that can handle complex auditing processes efficiently. Compliance management has become more intricate with global operations, requiring real-time tracking, auditing, and reporting to meet regulatory demands. Audit management software helps organizations navigate this complexity by providing centralized systems that ensure continuous monitoring and seamless updates to compliance protocols.

The growing penalties and reputational risks associated with non-compliance have intensified the demand for robust audit management solutions. A recent survey found that 80% of businesses report increased scrutiny from regulatory bodies, emphasizing the need for effective compliance tracking. Failing to meet these regulations can result in heavy fines, legal consequences, and lasting damage to reputation. Audit management software addresses these concerns by offering centralized systems that track compliance in real time, ensure transparency, and create reliable audit trails, reducing the potential for costly errors.

Persistent Data Security Concerns

Data security concerns remain a significant restraint for the adoption of audit management software. As businesses increasingly rely on cloud-based solutions, they face heightened risks related to data breaches, unauthorized access, and cyber-attacks. Audit management systems handle sensitive financial, operational, and regulatory data, making them prime targets for malicious actors. Organizations are reluctant to adopt these solutions without assurances that their data will be protected from external threats. Any breach could lead to significant financial losses, regulatory penalties, and irreparable damage to trust with clients and stakeholders.

The complexity of ensuring robust security measures further complicates the adoption process. Many businesses struggle to meet stringent data protection standards, particularly when audit management software involves cross-border data flows. Compliance with various data protection regulations, such as the General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA), is a challenge for organizations looking to ensure that the software aligns with their security requirements. The inability to safeguard sensitive data increases the risk of financial and reputational damage, which hinders widespread adoption across sectors dealing with high volumes of confidential information.

Technological Convergence with AI and Cloud Solutions

Technological convergence of AI and cloud solutions presents a key opportunity for the audit management software market. The integration of AI enables audit processes to become more intelligent and automated, reducing human error and enhancing efficiency. AI-driven tools can analyze vast amounts of data quickly, identify patterns, and provide predictive insights, enabling businesses to make more informed decisions. This allows organizations, including government entities, to streamline their auditing processes and uncover risks or inefficiencies that may have been overlooked using traditional methods. For example, in September 2025, the Comptroller and Auditor General (CAG) of India announced the development of an indigenous large language model (LLM) that will use decades of inspection reports and audit data to improve the efficiency, accuracy, and consistency of government audits.

The adoption of cloud solutions further enhances these capabilities by providing scalable, flexible, and cost-effective platforms for audit management. Cloud-based systems enable real-time collaboration and access to data from anywhere, increasing the speed and agility of audit functions. This convergence supports remote auditing, reduces infrastructure costs, and improves data security through advanced cloud encryption and backup mechanisms. As organizations seek to optimize their operations, the combination of AI and cloud technology opens new avenues for improving compliance, risk management, and operational transparency, making audit management more proactive and integrated within broader business strategies.

Category-wise Analysis

Component Insights

The solutions segment is poised to lead with a forecasted 70% of the audit management software market revenue share in 2026, as enterprises have been increasingly adopting comprehensive and automated software platforms that streamline audit workflows, enhance data accuracy, and minimize manual intervention. These software offerings have been providing capabilities such as centralized documentation, configurable workflows, and real-time analytics, which have been supporting organizations in strengthening internal controls and improving transparency. As businesses have been continuing to prioritize operational efficiency and regulatory compliance, robust software solutions have been becoming essential to address complex audit requirements, and this sustained focus is expected to have positioned the solutions segment as the primary driver of adoption in the near term.

The services segment has been anticipated to be the fastest-growing between 2026 and 2033, as the demand has been rising for tailored implementation, user training, and continuous support that ensure successful deployment of audit management platforms. Organizations have been seeking customized configurations, advisory input on process redesign, and expert guidance for smooth integration with existing enterprise systems, so that technology investments can deliver measurable improvements in risk management and compliance outcomes. This preference for specialized services such as change management, audit methodology consulting, and periodic optimization reviews has been expected to intensify as businesses have been working to keep their audit environments fully aligned with evolving regulatory requirements and industry best practices.

Deployment Type Insights

The cloud deployment model is likely to dominate with a projected 60% revenue share in 2026, owing to organizations embracing its scalability, substantial cost reductions, and adaptability to varying operational demands. Cloud platforms have been enabling enterprises to expand resources on demand, cut down on hardware expenses, and grant secure remote access from any location, which has been supporting the rise of distributed work environments across sectors. Businesses have been favoring this approach for its seamless updates and minimal upkeep needs, so it has been solidifying its top position while fostering innovation in audit processes.

The on-premises deployment model has been set to experience the fastest expansion from 2026 to 2033, propelled by entities in highly regulated fields such as banking and health care emphasizing data control and adherence to stringent norms. Companies have been opting for these systems to retain full authority over confidential information and tailor security features to precise standards, thereby mitigating risks in sensitive operations. This momentum has been building as firms have been pursuing fortified, bespoke audit tools that navigate shifting legal landscapes, which positions on-premises options for sustained acceleration amid rising compliance pressures.

Industrial Vertical Insights

The BFSI sector is set to secure a leading position in 2026, holding about 30% of the audit management software market revenues, as firms have been confronting heightened oversight and the imperative for rigorous verification procedures. BFSI entities have been deploying sophisticated platforms to deliver precise financial disclosures, mitigate operational hazards, and navigate intricate legal frameworks, which has been fortifying their resilience against scrutiny. Regulatory demands have been intensifying across jurisdictions, so organizations have been accelerating uptake of dependable automation tools, which has been establishing BFSI as the foremost consumer of these technologies in the foreseeable future.

The healthcare sector is positioned for the swiftest rise from 2026 to 2033, fueled by escalating oversight and the urgency for robust information safeguards. Healthcare providers have been confronting mandates such as the Health Insurance Portability and Accountability Act (HIPAA), prompting them to integrate verification systems that protect patient records and promote procedural clarity. Digital advancements have been reshaping operations, so institutions have been prioritizing fortified platforms to elevate safeguards and alignment with norms, which has been setting the stage for substantial expansion in this domain over the 2026-2033 forecast period.

Regional Insights

North America Audit Management Software Market Trends

North America is projected to hold a commanding 40% of the audit management software market share in 2026, driven by its robust regulatory landscape, advanced technological infrastructure, and the concentration of key industries such as finance, healthcare, and manufacturing. The region’s well-established financial sector, which faces stringent compliance requirements, has been fueling the demand for automated and dependable audit management solutions, positioning North America as the leader in this domain. The presence of a mature digital ecosystem has been accelerating the adoption of innovative technologies, allowing organizations to streamline processes and improve operational resilience.

The emphasis on data security and risk management has been pivotal in North America’s market dominance, as enterprises have been prioritizing solutions that provide robust protection against evolving cyber threats. With digital transformation progressing rapidly, businesses have been seeking advanced tools to safeguard sensitive information, especially in high-risk industries such as finance and healthcare. Cloud-based platforms have been playing a critical role by offering flexibility, scalability, and remote access, which has been making them essential for modern business operations and reinforcing North America’s leadership in the audit management software space.

Europe Audit Management Software Market Trends

Europe is slated to capture a substantial share of the audit management software market by 2033, as tighter regulatory expectations across sectors such as finance, healthcare, and energy have been increasing the cost of non-compliance. Requirements under the GDPR and the Markets in Financial Instruments Directive II (MiFID II) have been pushing organizations to automate evidence collection, strengthen controls, and maintain audit trails that support transparent, timely reporting. As oversight on privacy and disclosure has been intensifying, European enterprises have been adopting more advanced audit tools to reduce exposure, improve accountability, and sustain consistent compliance performance.

Market momentum has been building as digital transformation has been modernizing both enterprises and public institutions, with technology investments increasingly targeting faster audits, fewer manual errors, and more standardized workflows. Cloud deployment has been gaining ground because it has been offering scalability, flexibility, and lower total cost of ownership, while buyers have been balancing these advantages with data residency and third-party risk requirements. Public audit bodies have been formalizing governance for AI adoption, which has been signaling that AI-enabled audit capabilities are moving from experimentation to structured rollout. By 2033, several European organizations will have prioritized platforms that apply AI and machine learning to continuous monitoring, real-time analytics, and proactive risk identification, provided the solution also meets security, integration, and regulatory assurance needs.

Asia Pacific Audit Management Software Market Trends

Asia Pacific is forecasted to emerge as the fastest-growing regional market for audit management software between 2026 and 2033, stimulated by rapid digital transformation and intensifying regulatory pressures across emerging economies. As industries in key markets such as China and India have been expanding their global footprint, the requirement for scalable, automated solutions to streamline complex auditing processes has been accelerating. Businesses in these regions have been actively adopting advanced audit management platforms to navigate intricate regulatory environments and ensure greater transparency, which has been crucial for mitigating operational risks and enhancing overall efficiency.

The expansion of the financial sector and a sharpened focus on data security have been largely fueling this regional growth, as enterprises have been seeking to fortify their compliance frameworks against rising challenges. Cloud-based audit management solutions have been providing a cost-effective, secure avenue for managing audit workflows in real-time, thereby eliminating the need for heavy infrastructure investments. Furthermore, the integration of AI and machine learning into these systems has been empowering organizations to enhance decision-making and accelerate the analysis of large datasets.

Competitive Landscape

The global audit verification sector has been exhibiting moderate fragmentation. Prominent enterprises such as SAP, Oracle Corporation, and Wolters Kluwer N.V. have been commanding significant influence. These established entities have been leveraging their extensive distribution networks and comprehensive tool suites to maintain a robust presence alongside TeamMate. Meanwhile, smaller vendors have been focusing on specialized niches to attract unique customer segments, which has been creating a dual-layer competitive landscape. This dynamic will have shaped an environment where brand recognition and scale coexist with agility and creative problem-solving.

Innovation-led organizations such as Galvanize and AuditBoard have been integrating advanced technologies such as AI and cloud-hosted platforms to distinguish their software offerings. These firms have been providing scalable and automated systems that enhance operational efficiency while supporting data-driven decision-making through real-time analytics. By delivering customizable features that streamline workflows and improve risk mitigation, these challengers have been appealing to businesses seeking modern alternatives to legacy infrastructure. Such strategic positioning will have accelerated the adoption of sophisticated tracking solutions across various international industries.

Key Industry Developments

- In November 2025, Thomson Reuters launched its Agentic AI Solutions, transforming tax, audit, and accounting workflows through advanced automation and intelligent data insights.

- In November 2025, Mirza International appointed a new internal auditor for the fiscal year 2025-26, aiming to strengthen its financial oversight and compliance.

- In October 2025, PwC successfully launched an AI-driven audit platform, revolutionizing financial audits by enhancing efficiency, accuracy, and real-time data analysis.

Companies Covered in Audit Management Software Market

- SAP

- Oracle

- Deloitte

- PwC

- KPMG

- Galvanize

- AuditBoard

- Wolters Kluwer

- Ideagen

- TeamMate

Frequently Asked Questions

The global audit management software market is projected to reach US$ 2.2 billion in 2026.

Increasing need for regulatory compliance, risk management, and the adoption of AI and automation for more efficient auditing processes drive the market.

The market is poised to witness a CAGR of 15.4% from 2026 to 2033.

Growing demand for cloud-based solutions, the expansion in emerging markets, and the increasing need for advanced AI-driven audit tools key opportunities in the market.

Some of the key market players include SAP, Oracle, Deloitte, PwC, KPMG, and Galvanize.