- Advanced Materials

- Synthetic Sapphire Market

Synthetic Sapphire Market Size, Share, and Growth Forecast 2026 – 2033

Synthetic Sapphire Market by Product Type (Monocrystalline Synthetic Sapphire, Polycrystalline Synthetic Sapphire), Manufacturing Method (Kyropoulos Method, Czochralski Method, Edge-Defined Film-Fed Growth [EFG], Heat Exchange Method [HEM]), Application (LED Substrates, Semiconductor Wafers, Optical Components, Consumer Electronics, Aerospace & Defense, Medical Devices, Industrial Equipment, Others), Industry, and Regional Analysis for 2026–2033

Synthetic Sapphire Market Size and Trend Analysis

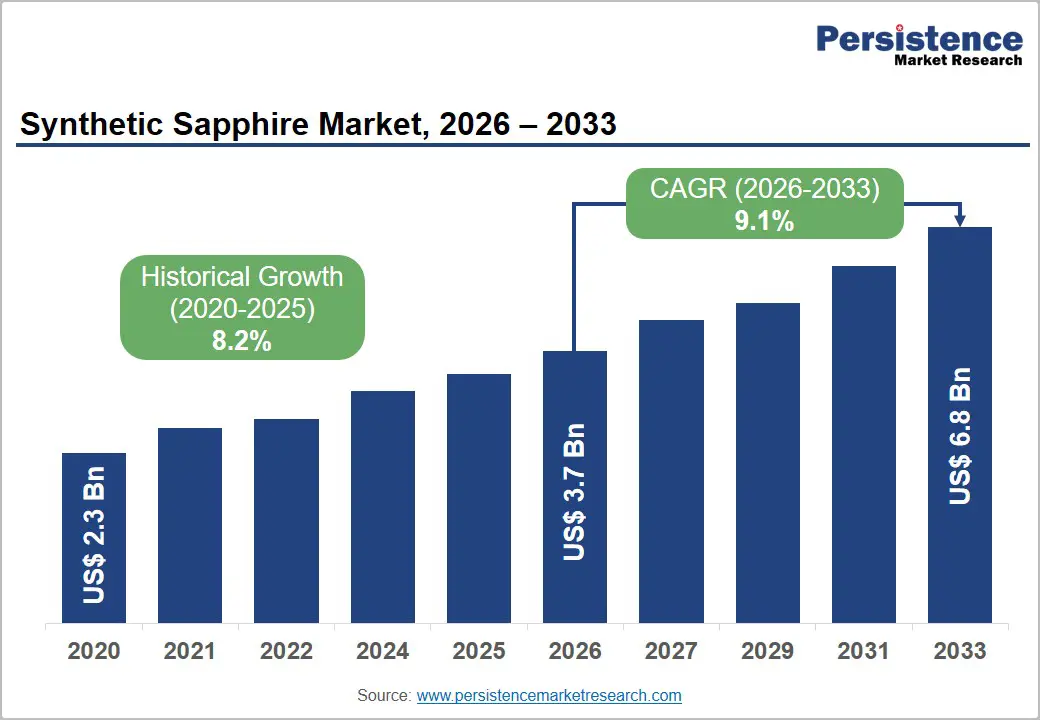

The global Synthetic Sapphire market size is likely to be valued at US$ 3.7 billion in 2026 and is projected to reach US$ 6.8 billion, expanding at a CAGR of 9.1% between 2026 and 2033. Market growth is primarily driven by the rising demand for LED substrates in energy-efficient lighting and display technologies, increasing adoption of sapphire-based GaN-on-Sapphire wafers in 5G RF semiconductors, and expanding utilization of optical sapphire windows in aerospace, defense, and industrial sensing applications.

Additionally, the rapid advancement of miniaturized optoelectronic devices, stringent defense-grade optical requirements, and the commercialization of Micro-LED displays requiring large-diameter sapphire substrates for superior optical purity and thermal stability are collectively reinforcing synthetic sapphire’s strategic importance across multiple high-growth industries globally.

Key Industry Highlights:

- LED Substrate Dominance: LED substrates accounted for approximately 38% of global market revenue in 2026, supported by increasing adoption of energy-efficient lighting systems and expanding utilization of GaN-on-sapphire technology in advanced displays.

- 5G Semiconductor Expansion: Semiconductor wafers for 5G applications are projected to expand at a positive CAGR, fueled by growing deployment of GaN-on-sapphire RF power amplifiers in global 5G infrastructure networks.

- Monocrystalline Segment Leadership: Monocrystalline synthetic sapphire dominated the product category with nearly 72% revenue share in 2026, owing to superior optical transparency, crystallographic precision, and demand from semiconductor and aerospace industries.

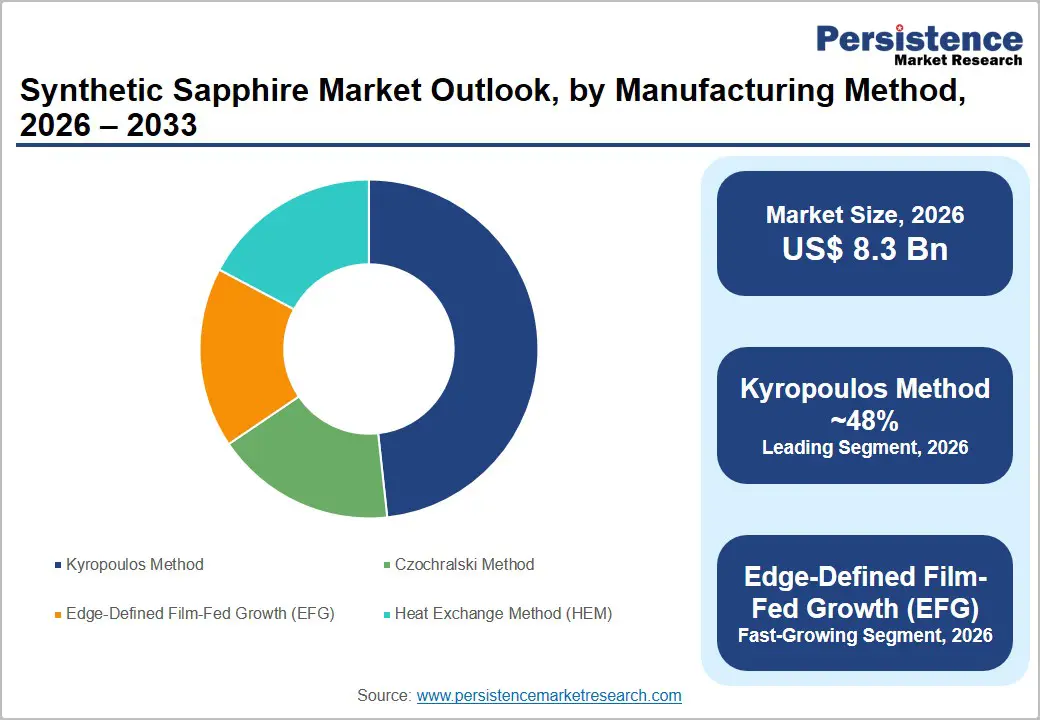

- Kyropoulos Method Dominance: The Kyropoulos manufacturing method accounted for approximately 48% of global production in 2026, benefiting from its capability to produce large-diameter, high-purity sapphire boules for premium semiconductor-grade wafers.

- Micro-LED Growth Opportunity: Commercialization of Micro-LED displays is creating substantial demand for 8-inch sapphire substrates, positioning advanced sapphire manufacturers for long-term supply agreements and premium-margin opportunities in consumer electronics.

- Electronics Industry Leadership: The electronics & semiconductor industry are likely to register approximately 55% of global synthetic sapphire revenue in 2026, driven by rising demand for LED chips, semiconductor wafers, and compound semiconductor technologies globally.

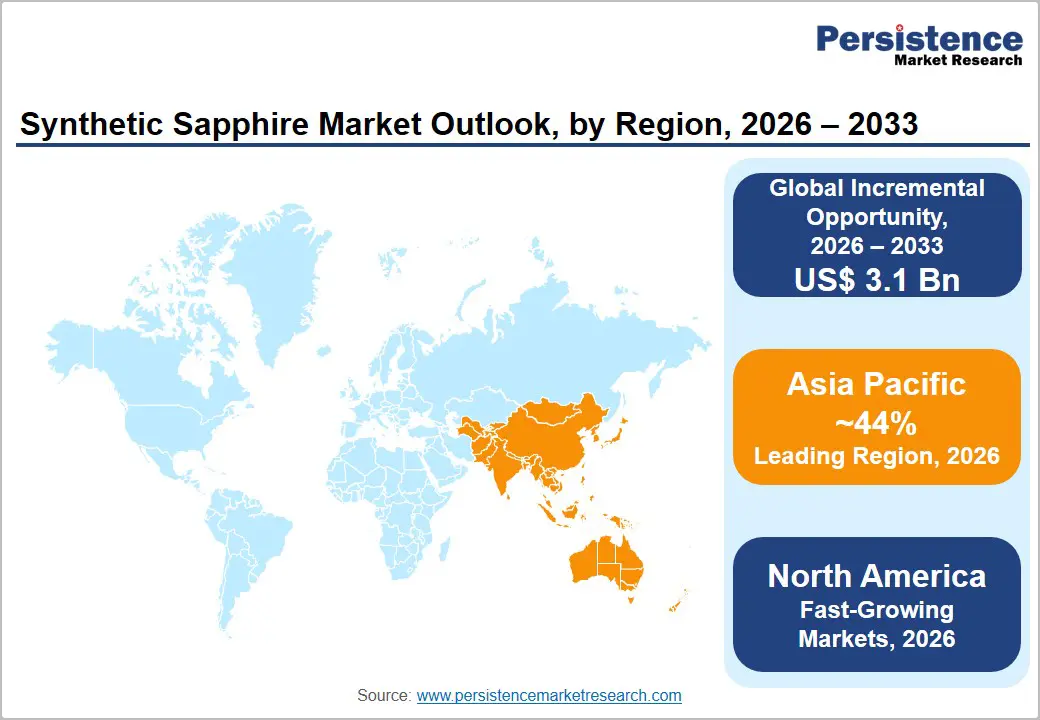

- Asia Pacific Dominance: Asia Pacific accounted for nearly 44% of global synthetic sapphire revenue in 2026 and is projected to experience healthy growth, supported by the strong presence of LED manufacturing and semiconductor investments in China, Japan, and South Korea.

- India High-Growth Potential: India represented approximately 8% of Asia Pacific demand in 2025 and is forecast to expand at a robust 12.1% CAGR, driven by LED adoption programs and semiconductor manufacturing investments.

Market Dynamics

Drivers - Surging Demand for LED Substrates and GaN-on-Sapphire Wafers in 5G and Lighting Applications

For synthetic sapphire producers and downstream electronics manufacturers, the concurrent growth of energy-efficient LED lighting and 5G RF Semiconductor Wafers represents the most consequential demand catalyst in the market's recent history and the competitive window for capacity investment is compressing as wafer diameter requirements escalate. Sapphire remains the dominant substrate material for GaN-on-Sapphire epitaxy used in LED manufacturing, with IEA data confirming that LED-based lighting now accounts for over 50% of global lighting energy savings, driving continuous growth in sapphire substrate procurement.

The deployment of 5G infrastructure, with the International Telecommunication Union (ITU) projecting 4.4 billion 5G connections globally by 2027, is simultaneously expanding demand for GaN-on-sapphire RF power amplifiers used in base station antenna arrays. Manufacturers capable of delivering 6-inch and 8-inch diameter polished sapphire wafers with sub-angstrom surface roughness specifications are capturing premium pricing as semiconductor fabs upgrade process nodes and integrate sapphire substrates into millimeter-wave component production lines.

Expanding Deployment of Optical Sapphire Windows in Aerospace, Defense, and Industrial Sensing

The expanding procurement of Optical Sapphire Windows and domes by defense agencies, aerospace OEMs, and industrial sensor manufacturers is delivering a structurally durable, high-margin demand stream for synthetic sapphire producers one that is largely insulated from consumer electronics cycle volatility and rewards producers with precision fabrication, optical coating, and tight transmission specification capabilities. Sapphire's exceptional hardness (9 on the Mohs scale), broad optical transmission range (0.15–5.5 micrometers), and resistance to abrasion and thermal shock make it irreplaceable for missile seeker domes, laser targeting windows, submarine optical ports, and high-temperature industrial camera lenses

The U.S. Department of Defense (DoD) fiscal year 2025 budget committed over US$ 145 billion to R&D, with next-generation missile, drone, and directed-energy weapon programs all specifying sapphire optical elements in their sensor payload architectures. Industrial machine vision, high-pressure process monitoring viewports, and medical endoscope optics are additional application segments where sapphire's combination of hardness, chemical inertness, and optical clarity is generating accelerating replacement demand for conventional glass and polymer window materials.

Restraints - High Energy Consumption and Production Cost of Large-Diameter Crystal Growth

The Kyropoulos and Czochralski crystal growth methods, which collectively account for the majority of commercial sapphire boule production, are inherently energy-intensive processes requiring furnace temperatures sustained at or above 2,050°C for periods of up to 30–40 days per growth cycle. This thermal intensity means that electricity constitutes 30–45% of total production costs for large-diameter sapphire boule manufacturers, creating significant exposure to industrial power tariff volatility, particularly in China and Eastern Europe, where a substantial proportion of global capacity is concentrated.

Energy cost pressures directly compress producer margins on commodity substrate grades and limit capacity expansion economics in regions with high industrial electricity prices, creating a structural barrier to supply-side scaling that constrains the market's ability to respond rapidly to demand surges.

Opportunities - Micro-LED Display Technology Creating High-Growth Demand for Large-Diameter Sapphire Substrates

The emerging commercialization of Micro-LED displays, projected to achieve significant consumer device penetration by the late 2020s, represents one of the most transformative demand growth opportunities for synthetic sapphire producers, as the technology's manufacturing process imposes substrate quality requirements that only large-diameter monocrystalline sapphire can reliably meet at scale. Apple Inc.'s sustained patent activity in Micro-LED display technology and Samsung Display's public commitments to a mass-production timeline confirm that leading consumer electronics OEMs are advancing Micro-LED toward commercial readiness across smartwatch, AR headset, and premium TV formats.

Micro-LED fabrication requires epitaxial GaN-on-Sapphire wafers with defect densities below 106 cm-2 and diameter specifications trending toward 8 inches, a technical threshold that eliminates most competing substrate options and concentrates procurement with the handful of sapphire producers capable of consistent large-diameter, ultra-low-defect crystal production. Sapphire substrate suppliers that invest now in 8-inch diameter Kyropoulos boule production capability and establish co-development partnerships with Micro-LED display pilot line operators will secure qualification positions that generate multi-year supply agreements once mass production programs launch, creating first-mover advantages that are inherently time-limited as OEM production ramp timelines firm up.

Category-wise Analysis

Product Type Insights

Monocrystalline synthetic sapphire is likely to command as a dominant product type, holding approximately 72% revenue share in 2026. This commanding share reflects monocrystalline sapphire's structural superiority across virtually all high-value applications: the absence of grain boundaries in its single-crystal lattice delivers optical transparency, mechanical strength, and surface perfection that polycrystalline alternatives cannot replicate. For LED Substrate production, GaN-on-Sapphire epitaxy requires monocrystalline c-plane sapphire wafers with crystallographic miscut tolerances below ±0.1° specifications, achievable only with single-crystal boules grown by Kyropoulos or Czochralski methods.

Polycrystalline synthetic sapphire is the fastest-growing sub-segment within the product type category. Expanding adoption in cost-sensitive industrial applications including furnace observation windows, wear-resistant mechanical seals, and LED streetlight diffusers highlights growth. Additionally, where polycrystalline sapphire's lower production cost per kilogram, relative to single-crystal equivalents, makes it the economically viable specification choice for large-format or high-volume applications where optical perfection is not a primary requirement.

Manufacturing Method Insights

The Kyropoulos Method holds the leading position in the manufacturing method category, accounting for approximately 48% of global synthetic sapphire production in 2026, underpinned by its unique capability to produce the largest single-crystal boule diameters commercially available, routinely yielding boules of 200–300 kg in advanced production facilities, making it the preferred method for semiconductor-grade wafer substrate production where large diameter and high crystal perfection are simultaneously required.

The Edge-Defined Film-Fed Growth (EFG) Method is the fastest-growing manufacturing approach, projected at a CAGR of approximately 12.3%. EFG's growth is driven by its exceptional capability to produce near-net-shape sapphire ribbons, rods, and tubes directly from the melt, eliminating the costly slicing and shaping operations required for boule-grown material, making it highly attractive for smartphone screen covers, smartwatch glass replacements, and continuous LED substrate ribbon production, where material utilization efficiency is a critical cost driver.

Application Insights

LED Substrates is the dominant application segment, representing approximately 38% of total global synthetic sapphire revenue in 2026. Sapphire's dominance as the LED substrate of choice is rooted in decades of GaN epitaxy process optimization: the c-plane sapphire surface provides the crystallographic template upon which gallium nitride epilayers are grown with sufficiently low defect densities to achieve commercial LED device efficiency levels.

The U.S. Department of Energy's annual LED luminaire efficiency reports have consistently documented the superior lumen-per-watt performance of GaN-on-sapphire LEDs relative to competing substrate approaches in the commodity lighting segment, cementing ongoing design-in preference among LED chip manufacturers. The emerging Micro-LED Display technology is set to sustain LED substrate demand at premium sapphire specifications well into the 2030s, reinforcing the application's structural market leadership.

Semiconductor Wafers (specifically RF Semiconductor Wafers for 5G applications) is the fastest-growing application segment, projected at a positive CAGR. The proliferation of 5G infrastructure globally with GaN-on-sapphire power amplifiers specified across millimeter-wave base station architectures is generating concentrated, high-specification demand for polished sapphire wafers that deliver the surface perfection and crystallographic quality required for advanced GaN HEMT device fabrication at 5G mmWave frequencies.

Industry Insights

The electronics & semiconductor industry is likely to register 55% revenue share in 2026 and accounts for a dominant position anchored by the massive and growing procurement of sapphire LED substrates and semiconductor wafers by chip manufacturers, LED epitaxy facilities, and compound semiconductor fabs across Asia Pacific, North America, and Europe. This segment's structural leadership reflects the irreplaceable role of synthetic sapphire across multiple semiconductor value chains: from LED chips in every display backlight and solid-state luminaire to GaN RF power devices in 5G infrastructure and gallium oxide power electronics in next-generation EV inverters, sapphire substrates and wafers sit at the critical foundation of multiple technology platforms with no near-term substitution pathway in premium performance tiers. The Semiconductor Industry Association (SIA) reports that global semiconductor sales reached US$ 527 billion in 2023, with compound semiconductor segments the primary synthetic sapphire consumers among the fastest-growing sub-sectors, directly sustaining elevated sapphire wafer demand.

The aerospace & defense end-use segment is the fastest-growing industry category, projected at a positive CAGR owing to the rise in defense procurement of sapphire optical elements for missile seekers, laser rangefinder windows, night-vision goggle lenses, and unmanned aerial vehicle (UAV) electro-optical payload windows applications where sapphire's combination of extreme hardness, broad spectral transmission, and environmental durability is technically irreplaceable and budget constraints are secondary to performance requirements.

Regional Insights

North America Synthetic Sapphire Market Trends

North America is likely to register 24% of the global synthetic sapphire market in 2026 driven by a world-class defense and aerospace procurement base, a highly developed semiconductor and optoelectronics industry, and sustained government investment in advanced materials manufacturing under the U.S. CHIPS and Science Act (US$ 52.7 billion committed). The region's demand is weighted toward high-value, premium-specification sapphire products defense-grade optical windows, semiconductor wafers for compound semiconductor fabs, and medical device components rather than commodity LED substrates, which positions North American demand toward higher revenue-per-unit metrics.

The U.S. Department of Defense's multi-billion-dollar annual investment in electro-optical and infrared (EO/IR) sensor systems spanning missile seekers, targeting pods, and reconnaissance payloads sustains consistent procurement of precision sapphire optical components. The region is moving toward localized sapphire supply chain development, with policy incentives encouraging domestic crystal growth capacity to reduce dependence on Asian suppliers for defense-critical applications.

U.S. Synthetic Sapphire Market Trends

The United States is likely to accounts for approximately 86% of North America's synthetic sapphire market in 2026 owing to the optical procurement growth and semiconductor fab investment under the CHIPS Act. The U.S. is home to critical sapphire producers including Rubicon Technology and Sapphire Technology, and the country's leading position in GaN semiconductor R&D and Micro-LED commercialization programs positions it as a key demand driver for premium substrate grades through the forecast period. The near-term trajectory strongly favors domestic supply chain buildout as national security concerns elevate sapphire's strategic material status.

Europe Synthetic Sapphire Market Trends

Europe is likely to represent approximately 18% of the global synthetic sapphire market in 2026, anchored by a sophisticated defense electronics sector, a well-developed LED luminaire manufacturing industry, and growing compound semiconductor investment under the European Chips Act (€43 billion committed to semiconductor manufacturing). Germany, France, the U.K., and Italy collectively concentrate the majority of European demand, driven by defense and aerospace procurement, precision optics manufacturing, and LED lighting component supply chains serving EU energy efficiency mandates under the Ecodesign Directive.

The EU's commitment to eliminating fluorescent and halogen lighting by 2023 under the Ecodesign Regulation has structurally reinforced LED adoption and by extension sapphire substrate demand across the European lighting supply chain. European defense procurement programs, including NATO's enhanced readiness initiatives and national fighter aircraft and drone platform modernizations, are sustaining demand for high-specification sapphire optical windows and laser protection elements across the region.

Germany Synthetic Sapphire Market Trends

Germany is likely to account for 26% of Europe's synthetic sapphire consumption in 2026, leading with a CAGR of approximately 8.6%. Germany's leadership reflects its world-class precision optics manufacturing sector anchored by companies including SCHOTT AG and Jenoptik which extensively specifies sapphire for industrial laser optics, scientific instrumentation windows, and high-temperature process sensors. The country's advanced automotive manufacturing sector is an emerging demand driver, with LiDAR sapphire window specifications entering volume production for next-generation assisted driving systems. Germany's trajectory favors sustained growth as precision manufacturing and defense investment sustain premium sapphire procurement.

U.K. Synthetic Sapphire Market Trends

U.K. represents approximately 18% of Europe's sapphire market in 2026 with demand anchored in the country's globally significant aerospace and defense manufacturing base including BAE Systems, Thales UK, and MBDA missile systems which specifies synthetic sapphire in missile seeker windows, laser rangefinder optics, and airborne EO/IR sensor payloads. The UK Ministry of Defence's sustained investment in next-generation combat aircraft and uncrewed systems sustains consistent high-specification optical sapphire procurement.

France Synthetic Sapphire Market Trends

France is likely to account for approximately 15% of Europe's synthetic sapphire market in 2026, supported by the country's aerospace and defense manufacturing sector with Safran, Thales, and Airbus specifying sapphire optical components in sensor and navigation systems and by a developed LED luminaire manufacturing industry serving EU energy efficiency mandates. The French government investment through Bpifrance in compound semiconductor and advanced optics manufacturing is gradually building domestic sapphire demand in emerging applications.

Italy Synthetic Sapphire Market Trends

Italy represents approximately 12% of Europe's synthetic sapphire market in 2026, driven by a combination of industrial laser optics manufacturing serving the country's significant laser machinery and advanced manufacturing equipment sector and growing adoption of sapphire in luxury goods applications including premium watchglass and high-end consumer electronics. Italy's ENEA research programs and defense procurement by the Italian Air Force for EO/IR sensor sapphire windows are additional demand contributors. The country's market is projected at a CAGR of approximately 8.1% through 2033, with industrial and luxury applications providing stable baseline demand.

Asia Pacific Synthetic Sapphire Market Trends

Asia Pacific is the leading regional market, accounting for approximately 44% of global synthetic sapphire revenue in 2026 and projected to expand at a CAGR exceeding 10.5% in the forecast period. The region's structural leadership reflects China's position as the world's largest synthetic sapphire crystal grower and LED substrate processor, Japan's globally advanced role in precision sapphire fabrication for semiconductor and optical applications, and South Korea's world-class LED and display manufacturing ecosystem. India is emerging as a significant demand market driven by government-backed LED adoption programs and nascent domestic semiconductor investment.

China Synthetic Sapphire Market Trends

China is more likely to register 52% of Asia Pacific's synthetic sapphire market share in 2026, reflecting the country's unmatched crystal growth manufacturing scale with producers including Harbin Aurora Optoelectronics, TDG Optoelectronics, and Crystalwise Technology operating large-scale Kyropoulos furnace arrays. Its domestic LED manufacturing expansion, 5G base station deployment, and Micro-LED display pilot production programs has fuelled the growth. Government policy under the Made in China 2025 initiative prioritizes compound semiconductor materials self-sufficiency, accelerating domestic sapphire substrate investment and import substitution.

India Synthetic Sapphire Market Trends

India is likely to account for approximately 8% of Asia Pacific's synthetic sapphire market share in 2026, with demand driven primarily by the government's UJALA (Unnat Jyoti by Affordable LEDs for All) scheme which distributed over 360 million LED bulbs and created the world's largest LED procurement program generating sustained demand for LED substrates. The India Semiconductor Mission's US$ 10 billion investment package attracts compound semiconductor fab investment that will generate domestic sapphire wafer procurement at significant scale attracting more growth.

South Korea Synthetic Sapphire Market Trends

South Korea is likely to account for 16% of Asia Pacific's synthetic sapphire market in 2026, anchored by the country's world-leading display and LED manufacturing ecosystem with Samsung, LG Electronics, and Seoul Semiconductor as major sapphire substrate consumers for high-brightness LED and display component production. Its aggressive investment in Micro-LED Display technology for premium television, AR/VR devices, and automotive displays applications that require ultra-high-specification GaN-on-sapphire substrates at 6-inch and 8-inch diameters where Korean display OEMs are targeting global leadership.

Competitive Landscape

The global synthetic sapphire market is moderately consolidated at the premium crystal production tier, where a limited number of technology-intensive producers led by Monocrystal (Russia/UAE), Rubicon Technology (U.S.), Crystalwise Technology (Taiwan), Saint-Gobain Crystals (France), and TDG Optoelectronics (China) hold dominant positions through proprietary crystal growth process IP, large-diameter boule production capability, and established OEM qualification relationships in semiconductor and defense applications.

Competitive differentiation centers on boule diameter leadership, crystal defect density specifications, and the ability to deliver consistent large-format material at volume. Key strategic themes include vertical integration from crystal growth through wafering and polishing, geographic diversification of production assets to serve regional supply security mandates, and R&D investment in next-generation large-diameter Kyropoulos furnaces for 8-inch wafer production targeting the Micro-LED opportunity.

Key Developments:

- March 2025: Monocrystal commissioned a new large-diameter Kyropoulos crystal growth facility in the UAE, strategically positioning the company to serve Middle Eastern defense customers and reduce geopolitical supply chain risk for its global semiconductor and optical sapphire customers amid ongoing sanctions concerns.

- November 2024: Rubicon Technology announced qualification completion for its 8-inch diameter polished sapphire wafer product line, becoming one of the first U.S.-based producers to achieve commercial-readiness for this format, targeting Micro-LED Display pilot line customers in South Korea and Japan.

- June 2023: Saint-Gobain Crystals expanded its Washougal, Washington sapphire production facility, increasing capacity for defense-grade optical sapphire windows and domes in response to growing U.S. DoD procurement demand for EO/IR sensor sapphire components in next-generation missile and drone programs.

Global Synthetic Sapphire Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 2.3 Bn |

| Current Market Value (2026) | US$ 3.7 Bn |

| Projected Market Value (2033) | US$ 6.8 Bn |

| CAGR (2026–2033) | 9.1% |

| Leading Region | Asia Pacific, ~44% market share (2026) |

| Dominant Segment (Product Type) | Monocrystalline Synthetic Sapphire, ~72% market share (2026) |

| Top-Ranking Application | LED Substrates, ~38% market share (2026) |

| Incremental Opportunity (2026–2033) | US$ 3.1 Bn |

Companies Covered in Synthetic Sapphire Market

- Monocrystal

- Rubicon Technology, Inc.

- Saint-Gobain Crystals

- Crystalwise Technology Co., Ltd.

- TDG Optoelectronics

- Harbin Aurora Optoelectronics Technology Co., Ltd.

- Kyocera Corporation

- Adamant Namiki Precision Jewel Co., Ltd.

- Sapphire Technology Co., Ltd.

- ILJIN Display Co., Ltd.

- Shinkosha Co., Ltd.

- Precision Sapphire Technologies

- GT Advanced Technologies (GTAT)

- Gavish

- Photox Optical Systems

Frequently Asked Questions

The global synthetic sapphire market is valued at US$ 3.7 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, expanding at a CAGR of 9.1% between 2026 and 2033. This growth represents an incremental opportunity of US$ 3.1 Bn, driven by LED substrate demand, 5G semiconductor wafer procurement, defense optical applications, and the emerging Micro-LED display technology revolution.

Surging global demand for LED Substrates and GaN-on-Sapphire semiconductor wafers for 5G RF components and energy-efficient lighting, underpinned by the ITU's projection of 4.4 billion 5G connections by 2027 and IEA data confirming LED lighting dominance in global energy savings.

Monocrystalline synthetic sapphire is likely to lead the product type category with approximately 72% of global market revenue in 2026 Its dominance is rooted in the single-crystal material's superior optical transparency, mechanical perfection, and crystallographic precision properties that LED substrate epitaxy, defense optical window fabrication, and semiconductor wafer applications require and that polycrystalline alternatives structurally cannot match. The ongoing industry migration toward 6-inch and 8-inch diameter wafer formats further concentrates procurement with monocrystalline Kyropoulos-method producers capable of scaling boule diameter without compromising crystal quality.

Asia Pacific is likely to lead the global synthetic sapphire market with approximately 44% of market revenue in 2026. The region's leadership is rooted in China's world-scale sapphire crystal growth manufacturing capacity which supplies the majority of global commodity LED substrate demand combined with South Korea's and Japan's globally advanced semiconductor, display, and precision optics industries that generate consistent high-specification sapphire wafer and optical component procurement.

The most strategically significant near-term opportunity includes – developing 8-inch diameter monocrystalline sapphire substrate capability for the Micro-LED Display production ramp. As Samsung Display, LG Display, and leading Chinese display OEMs advance Micro-LED toward mass-market commercialization with the global smartwatch, AR headset, and premium TV markets targeted they require ultra-high-specification GaN-on-Sapphire wafers at 8-inch format that the vast majority of current producers cannot supply.

Leading companies in the global Synthetic Sapphire market include Monocrystal, Rubicon Technology Inc., Saint-Gobain Crystals, Crystalwise Technology Co. Ltd., TDG Optoelectronics, Harbin Aurora Optoelectronics Technology Co. Ltd., Kyocera Corporation, Adamant Namiki Precision Jewel Co. Ltd., GT Advanced Technologies (GTAT), ILJIN Display Co. Ltd., Shinkosha Co. Ltd., and Precision Sapphire Technologies, among others.