- Advanced Materials

- Marble and Stone Market

Marble and Stone Market Size, Share, and Growth Forecast 2026 - 2033

Marble and Stone Market by Product Type (Marble, Granite, Limestone, Sandstone, Slate, Others), Form (Blocks, Slabs, Tiles, Monuments and Sculptures, Others), Finish Type (Polished, Honed, Flamed, Brushed, Sandblasted, Others), Application (Flooring, Wall Cladding, Countertops & Kitchen Surfaces, Roofing, Monuments & Memorials, Landscaping & Outdoor Applications, Decorative Applications, Others), End-userr, and Regional Analysis, 2026 - 2033

Marble and Stone Market Size and Trend Analysis

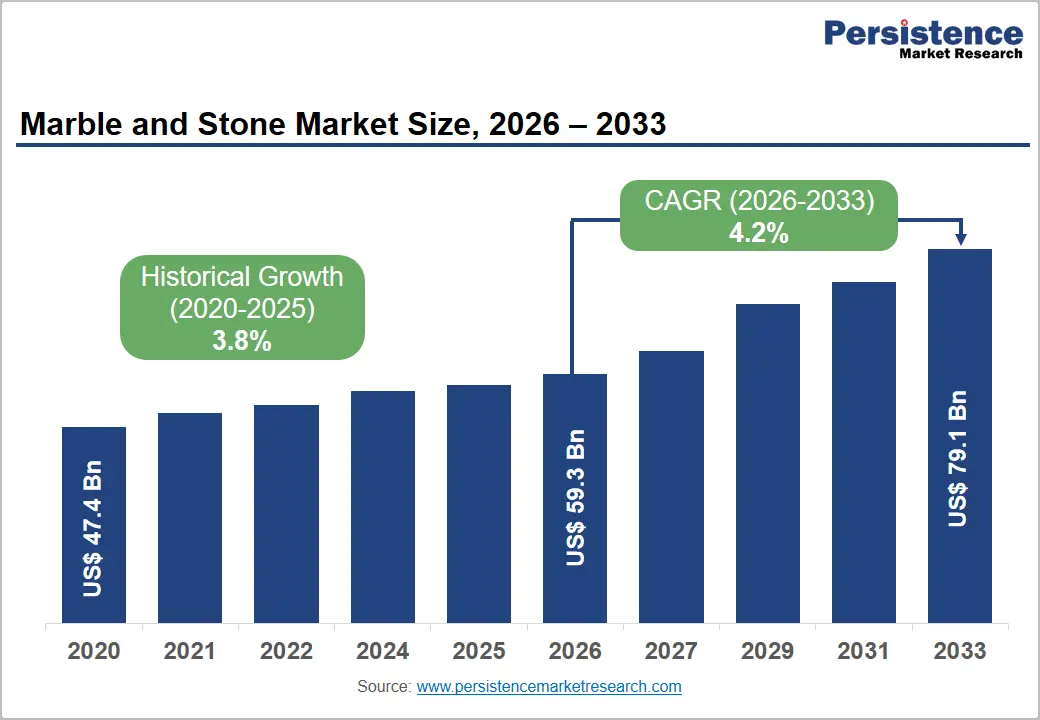

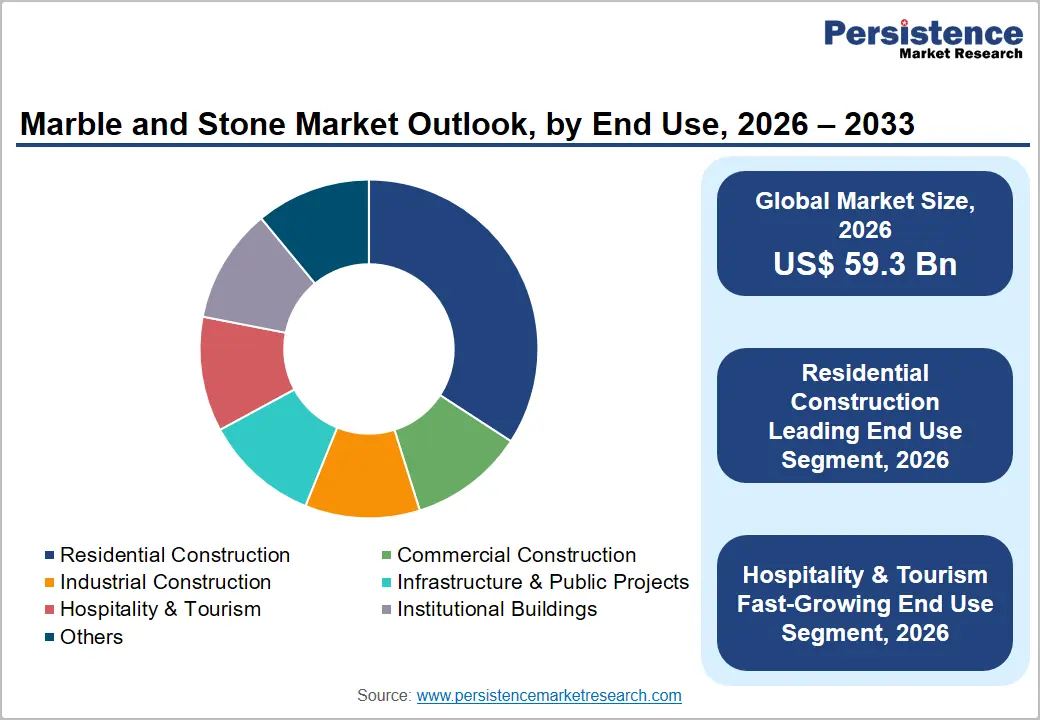

The global marble and stone market size is expected to be valued at US$ 59.3 billion in 2026 and projected to reach US$ 79.1 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Steady investments in residential, commercial, and infrastructure construction activities across major economies, along with increasing consumer preference for premium natural stone materials in interior and exterior architectural applications.

The demand is further strengthened by the expansion of luxury real estate developments, rising hospitality and tourism infrastructure projects, and the growing use of marble and granite in high-end flooring, wall cladding, countertops, and decorative surfaces. Rapid urbanization across the Asia Pacific and the Middle East & Africa is also contributing significantly to consumption growth. In addition, the emergence of digital stone sourcing platforms and online visualization technologies is improving market accessibility for buyers, designers, distributors, and quarry operators across both developed and emerging regions.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the global marble and stone market with approximately 38% share in 2025, driven by China's vast construction demand base and India's world-class quarrying and processing industry supplying both domestic and export markets.

- Fastest Growing Region: Asia Pacific is also the fastest-growing region, projected at a CAGR of 5.5% through 2033, catalyzed by India's premium housing expansion, Southeast Asia's hospitality construction boom, and rising middle-class demand for natural stone interior finishes.

- Dominant Product Type: Granite dominates the product type category with approximately 34% market share in 2025, sustained by its superior durability, versatile application range, and commercially mature global supply chain spanning India, Brazil, China, and Norway.

- Fast-Growing End-user: Hospitality & tourism is the fastest-growing end-user segment, propelled by unprecedented hotel and resort development pipelines in the Middle East, Southeast Asia, and Africa, where five-star specifications mandate natural stone across all public-area and guest-room finishes.

- Key Opportunity: Investing in sustainability certification and digital visualization capabilities: ESG-driven procurement mandates in EU institutional projects and rising online specification behavior are rewarding certified, digitally visible stone producers with specification preference and measurable price premiums.

Market Dynamics

Drivers - Accelerating Luxury Residential and Commercial Construction Activity in Emerging Economies

The rapid expansion of premium residential and commercial construction across Asia Pacific, the Middle East, and Latin America is creating strong long-term demand for marble and natural stone products. Rising urbanization, growing middle-class income levels, and increasing preference for premium interior finishes are encouraging the adoption of marble, granite, and decorative stone in luxury housing, hospitality, and infrastructure projects. Countries such as India, China, Nigeria, and Egypt are witnessing significant housing development activity, supporting demand for flooring, wall cladding, and architectural stone applications.

The commercial construction sector is also contributing substantially to market growth, particularly through large-scale hotel, resort, and mixed-use developments. Luxury hospitality projects across Southeast Asia, the Gulf countries, and Africa increasingly utilize natural stone in lobbies, bathrooms, facades, and public spaces to enhance aesthetics and durability. Manufacturers with strong quarry access, advanced processing facilities, and global export networks are well-positioned to benefit from this sustained multi-year market expansion.

Rising Demand for Natural Stone in High-End Interior Design and Renovation Markets

The renovation and remodeling market in North America and Europe is creating stable long-term demand for premium natural stone products, particularly in residential interior applications. Aging housing infrastructure, rising home improvement spending, and growing consumer interest in luxury home upgrades are driving the use of marble and granite in kitchens, bathrooms, flooring, and wall cladding. Renovation activity remains especially strong in high-income residential markets where homeowners prioritize premium aesthetics, durability, and long-term property value enhancement.

Consumer preference for natural stone is increasing in the luxury remodeling segment due to its distinctive appearance, natural veining patterns, and perception as a high-end, durable material. Marble and granite continue to gain preference in upscale kitchen and bathroom renovation projects over several engineered alternatives. Companies investing in advanced slab display centers, digital visualization platforms, and partnerships with architects, interior designers, and remodeling showrooms are strengthening their competitive position. These specification-driven sales channels also support premium pricing and stronger customer retention compared to traditional commodity-based distribution models.

Restraints - Substitution Pressure from Engineered Stone and Large-Format Porcelain Surfaces

The marble and stone market is facing growing competitive pressure from engineered quartz and large-format sintered stone materials, particularly in countertop and wall cladding applications. These alternatives offer advantages such as uniform appearance, low maintenance requirements, stain resistance, and competitive pricing, making them increasingly attractive to residential and commercial buyers. Their availability in standardized designs and large panel formats is also improving installation efficiency and reducing material wastage in construction projects.

The substitution threat is especially significant in the mid-range construction and renovation segment, where buyers prioritize affordability, consistency, and ease of maintenance over the natural uniqueness of stone surfaces. Sintered stone products are also gaining popularity in façade and interior cladding applications due to their lightweight structure and high durability. As competition intensifies, natural stone manufacturers are focusing on product differentiation through premium aesthetics, exclusive quarry sourcing, craftsmanship, and sustainability positioning. Companies are also emphasizing the authenticity, natural variation, and long-term value of marble and granite to maintain competitiveness in high-value applications.

Logistics Complexity, High Transportation Costs, and Supply Chain Fragility

Natural stone's physical characteristics, high density, fragility under mechanical stress, and the requirement for climate-controlled or padded transportation, impose logistics costs and supply chain risks that structurally disadvantage the industry relative to manufactured surface alternatives and constrain margin expansion for processors and distributors. Shipping a standard 20-foot container of marble slabs from a quarry in Carrara, Italy, or Rajasthan, India, to a distribution warehouse in North America or Northern Europe can cost US$ 3,000-7,000, depending on fuel surcharges and port conditions, a cost that frequently represents 15-25% of the total ex-works value of the cargo.

This logistics intensity is compounded by the industry's exposure to port congestion, fuel price volatility, and, as demonstrated during the COVID-19 pandemic disruption of 2020-2021, the fragility of global container shipping infrastructure under demand shock. New market entrants and smaller regional processors without scale-efficient logistics arrangements face structurally higher landed costs than large integrated operators such as Levantina or Polycor Inc., creating a meaningful competitive disadvantage in price-sensitive distribution channels.

Opportunities - Expansion into Sustainable and Responsibly Sourced Stone Certification Markets

The increasing integration of ESG considerations into construction material procurement is creating significant growth opportunities for marble and stone producers that can demonstrate sustainable and responsible operations. Institutional and commercial construction projects in Europe and North America are increasingly prioritizing materials with certified environmental performance, ethical sourcing practices, and transparent supply chains. Green building certifications and low-carbon construction targets are encouraging architects, developers, and public agencies to select natural stone suppliers that can provide verified sustainability documentation and lifecycle impact assessments.

Leading architecture and engineering firms are incorporating sustainability-focused material standards into public infrastructure, healthcare, education, and commercial building projects, where procurement decisions increasingly favor certified suppliers over low-cost alternatives. Stone producers investing in responsible quarry management, carbon footprint reduction initiatives, ethical labor compliance, and third-party sustainability certifications are gaining stronger access to premium institutional projects. Companies in countries such as Portugal, Spain, Turkey, and India are particularly well-positioned to benefit from this shift. Early adoption of sustainability standards is also helping suppliers secure long-term specification relationships and premium pricing advantages.

Digital Stone Commerce and Virtual Visualization Platforms as a Market Expansion Tool

The digitization of natural stone sourcing and specification is creating strong near-term growth opportunities for marble and stone producers and distributors. Online platforms and digital showrooms are transforming how architects, interior designers, contractors, and homeowners discover and purchase natural stone products. Digital channels allow buyers to compare materials, review slab variations, and evaluate applications remotely, helping suppliers expand beyond traditional regional distribution networks and access a wider customer base across residential and commercial construction markets.

The growing role of online research in renovation and construction decisions is increasing the importance of digital product libraries, high-quality texture visualization, and streamlined customer engagement tools. Advanced technologies such as augmented reality visualization are enabling customers to virtually place marble or granite slabs within real interior spaces, improving purchasing confidence and increasing conversion rates. Companies that invest in digital infrastructure, virtual showrooms, and integrated sales platforms are strengthening customer acquisition and brand visibility while reducing reliance on large physical showroom networks. Early adopters of these technologies are gaining a competitive advantage in specification-driven and premium-value market segments.

Category-wise Analysis

Product Type Insights

Granite dominates the marble and stone market with approximately 34% of global market share in 2025 due to its exceptional durability, broad application scope, and strong global supply availability. Its high resistance to heat, scratches, and wear makes it a preferred material for countertops, flooring, wall cladding, and infrastructure applications across residential and commercial sectors. Major quarrying and processing operations in India, Brazil, China, and Norway have established an extensive international supply chain, supporting stable exports and competitive pricing.

Granite also benefits from strong demand in high-traffic applications such as airports, hotels, office buildings, and public infrastructure, where long-term performance is critical. Its combination of aesthetic variety, mechanical strength, and cost-effectiveness continues to support widespread adoption across both premium and mid-range construction projects, reinforcing its leading market position globally.

Form Insights

Slabs hold the leading share in the marble and stone market, accounting for approximately 42% of global revenue in 2026 due to their strong demand in premium architectural and interior applications. Large-format slabs are widely used for countertops, feature walls, luxury flooring, and commercial installations where seamless aesthetics and natural veining patterns are highly valued. The growing popularity of open-concept kitchens, luxury bathrooms, and upscale hospitality interiors has significantly increased slab consumption across residential and commercial projects.

Stone processors are investing heavily in advanced cutting, polishing, and book-matching technologies to produce high-quality slabs for designer-driven applications. Slabs also generate higher average selling prices compared to tiles and cut-to-size formats, making them the most profitable category for integrated manufacturers and distributors serving premium construction and remodeling markets worldwide.

Finish Type Insights

Polished finish leads the finish type segment with approximately 52% share in 2026 due to its strong association with luxury interior aesthetics and premium construction standards. The finish enhances the natural color depth, veining, and reflective appearance of marble and granite, making it highly preferred for countertops, hotel lobbies, flooring, and decorative wall applications. Architects, designers, and homeowners continue to favor polished stone for high-end residential and commercial interiors because of its elegant visual appeal and premium perception.

The dominance of polished finishes is further supported by advanced stone processing technologies, particularly in Italy and other major stone manufacturing regions, which ensure consistent surface quality and gloss levels. Despite rising interest in matte and textured finishes, polished stone remains the standard specification across many large-scale hospitality, retail, and luxury housing developments globally.

Application Insights

Flooring represents the largest application segment in the marble and stone market with approximately 38% share in 2026, supported by extensive use across residential, commercial, hospitality, and institutional buildings. Natural stone flooring is widely preferred for its durability, premium appearance, and long service life, particularly in high-traffic environments such as hotels, airports, shopping malls, hospitals, and office complexes.

Large infrastructure and public development projects in Asia Pacific and the Middle East continue to generate substantial procurement volumes for marble and granite flooring materials. Luxury residential construction also contributes significantly to flooring demand, as homeowners increasingly prefer natural stone for living spaces, hallways, and bathrooms. The segment benefits from the material’s ability to enhance property value while offering superior resistance to wear and long-term maintenance advantages compared to several alternative flooring materials.

End-user Insights

Residential construction remains the leading end-user segment in the marble and stone market with approximately 36% share in 2025, driven by strong demand for premium interior and exterior building materials. Homeowners increasingly prefer marble, granite, and other natural stones for kitchens, bathrooms, flooring, staircases, and decorative wall applications due to their durability, visual appeal, and long-term property value enhancement.

Rise in luxury housing development and renovation activity across North America, Europe, Asia Pacific, and the Middle East continues to support stable demand growth. Natural stone is widely perceived as a premium and permanent construction material, making it highly attractive for upscale residential projects. Growing consumer spending on home aesthetics, combined with increasing interest in personalized and high-quality interiors, is further strengthening the adoption of marble and stone products across global residential construction markets.

Regional Insights

North America Marble and Stone Market Trends and Insights

North America is likely to account for approximately 21% of the global marble and stone market in 2026, driven by a structurally robust residential renovation market, sustained commercial construction activity in major metropolitan areas, and a mature natural stone specification culture reinforced by interior design professionals and premium retail distribution networks. The U.S. renovation cycle, anchored in an aging housing stock, elevated home equity levels, and lifestyle-driven investment in premium kitchen and bathroom spaces, delivers consistent demand for granite countertops, marble tiles, and limestone wall cladding.

The region is trending toward sustainable stone certification and digital procurement channels, and market participants that align product positioning with these structural shifts will outperform peers relying on traditional trade-only distribution.

U.S. Marble and Stone Market Size

The United States accounts for approximately 82% of North America's marble and stone market in 2026, supported by a US$ 420 billion+ home improvement sector and robust commercial construction pipelines in luxury residential, hospitality, and institutional segments. U.S. Geological Survey (USGS) data consistently identify the country as one of the world's largest importers of dimension stone, with Italy, India, Brazil, Turkey, and China as the primary supply origins.

Europe Marble and Stone Market Trends and Insights

Europe holds approximately 26% of the global marble and stone market share in 2026, the largest regional share, anchored by Italy, Spain, Portugal, Greece, and Turkey as both the world's leading stone-producing nations and major consumer markets with deep architectural and cultural traditions of natural stone use. The region's demand is shaped by a sophisticated specification culture, extensive building restoration activity across historic cities, and a regulatory environment under the EU Green Deal that is increasingly rewarding sustainably certified natural materials over synthetic alternatives.

European producers face rising domestic labor costs and energy-intensive processing challenges, but their brand equity, particularly the Carrara marble and Portuguese limestone appellations, sustains premium pricing power in global export markets. The region's trajectory favors sustainability-certified, digitally marketed premium stone products.

Germany Marble and Stone Market Size

Germany represents approximately 17% of Europe's marble and stone market in 2026, supported by the country's large commercial construction sector, an active building renovation market, and a professional specification culture that prioritizes material quality and longevity. German architecture's preference for natural stone in public buildings, transport infrastructure, and premium residential developments sustains consistent import volumes, primarily from Italy, Portugal, and India. Germany's market is forecast to grow at a steady pace, with sustainability-certified stone gaining specification preference in public sector procurement.

U.K. Marble and Stone Market Size

The U.K. accounts for approximately 13% of Europe's marble and stone market in 2026, driven by premium residential construction in London and the South East, a robust commercial interior fit-out market, and sustained demand for natural stone in heritage building restoration projects. The country's strong interior design culture, anchored by institutions such as the Design Council and a globally influential interiors media sector, sustains specification demand for premium marble and limestone products. The U.K. market is expected to grow moderately, with renovation and hospitality development sustaining demand.

France Marble and Stone Market Size

France represents approximately 11% of Europe's marble and stone market in 2026, underpinned by a premium residential construction sector, significant hospitality development activity, particularly in Paris and the French Riviera, and a culturally embedded preference for natural stone in both new-build and restoration applications. The French government's MaPrimeRenov program is sustaining renovation investment in the residential building stock, supporting consistent demand for stone flooring and cladding upgrades. France's market trajectory favors premium marble and limestone products with documented heritage provenance and sustainability credentials.

Asia Pacific Marble and Stone Market Trends and Insights

Asia Pacific is the largest volume market and the fastest-growing region for marble and stone, accounting for approximately 38% of global demand in 2026 and projected to expand at a CAGR of approximately 5.5%. China dominates the region as both the world's largest consumer and producer of natural stone, with its commercial and residential construction pipelines, despite near-term macroeconomic headwinds, sustaining enormous absolute procurement volumes. Companies seeking to scale in Asia Pacific must invest in localized specification marketing, partnerships with regional EPC contractors, and agile supply chain arrangements that can respond to project-driven demand volatility.

India Marble and Stone Market Size

India accounts for approximately 20% of Asia Pacific's marble and stone market in 2026, driven by rapid expansion in premium residential construction, government-funded infrastructure projects, and a domestic stone processing industry of global scale, with Rajasthan alone producing an estimated 60% of India's marble and granite output. The Ministry of Mines, Government of India, data confirms India as one of the world's top stone exporting nations. India's market is among the region's fastest-growing, supported by PMAY housing programs and a rapidly expanding hospitality construction pipeline.

Japan Marble and Stone Market Size

Japan represents approximately 10% of the Asia Pacific's marble and stone market in 2026, with demand concentrated in the country's premium commercial construction sector, spanning luxury retail, high-specification office developments, and five-star hospitality, and in the well-developed residential renovation market. Japan's design culture values natural stone for its authenticity and permanence, sustaining import demand from Italy, Spain, Portugal, and India despite the country's relatively mature construction market. Japan's stone market is forecast to grow at a measured pace, with premiumization and hospitality renovation driving value over volume.

South Korea Marble and Stone Market Size

South Korea is likely to account for approximately 8% of the Asia Pacific's marble and stone market in 2026, supported by strong demand from the country's premium residential apartment sector, where marble and granite lobbies, elevator halls, and bathroom finishes are standard specifications, and by active commercial and hospitality construction in Seoul and major regional cities. South Korean developers' preference for imported Italian marble and Brazilian granite in premium developments sustains consistently high-value import volumes. The market is expected to grow steadily, driven by urban regeneration and premium residential development.

Competitive Landscape

The global marble and stone market is highly fragmented at the quarrying and primary processing tier, with thousands of independent quarry operators across Italy, Turkey, India, China, Brazil, Spain, and Portugal competing primarily on raw material access and extraction cost. However, the market increasingly rewards vertical integration and brand differentiation at the processing, finishing, and distribution tiers, where companies such as Levantina, Antolini Luigi & C. SpA, Margraf, Polycor Inc., and Cosentino have built durable competitive advantages through proprietary quarry rights, premium brand positioning, expansive slab display infrastructure, and digital product marketing.

Key differentiators among market leaders include exclusive stone variety portfolios, certification of sustainability and ethical sourcing, architectural specification relationships, and investment in digital visualization platforms. A dominant emerging strategic theme is the shift toward direct-to-specifier marketing, bypassing traditional distributor tiers to build relationships with architecture firms, interior designers, and hospitality procurement agencies, a model that compresses channel costs and elevates brand premium simultaneously.

Key Developments:

- May 2026: HMG Stones announced plans to invest INR 40 crore in FY27 to expand machinery, automation, and retail infrastructure, including a new experience center near Bengaluru airport, while targeting revenue growth to INR 120-150 crore.

- March 2026: Keystone Marble & Granite launched a new eco-friendly granite collection featuring responsibly sourced and sustainably processed granite slabs for residential and commercial interiors, targeting growing demand for environmentally conscious countertop and surface materials.

Companies Covered in Marble and Stone Market

- Levantina

- Polycor Inc.

- Antolini Luigi & C. SpA

- Fox Marble

- Kangli Stone Group

- Best Cheer Stone Group

- Marcolini Marmi

- Margraf

- Intermarmor

- Cosentino

- MSI Surfaces

- Daltile

- RK Marble

- Classic Marble Company

- Pokarna Limited

- Bhandari Marble Group

- Emil Group

- Laminam

- Granitifiandre (SaintGobain Group)

- Porcelanosa Group

Frequently Asked Questions

The global marble and stone market size is valued at US$ 59.3 billion in 2026 and is projected to reach US$ 79.1 billion by 2033, growing at a CAGR of 4.2%.

Global rise in construction activity, renovation, and remodeling projects.

Asia Pacific leads with around 38% share, supported by strong construction and quarrying industries.

Sustainability certification and digital visualization tools are emerging as major growth opportunities.

Key players include Levantina, Polycor Inc., Antolini Luigi & C. SpA, Cosentino, MSI Surfaces, and Pokarna Limited.